AMGN - Johnson & Johnson: Rock Solid 3% Yield With Over 10% Return Potential (Rating Upgrade)

2024-01-04 13:29:38 ET

Summary

- Johnson & Johnson's stock has underperformed the market, but its strong performance and secure balance sheet make it an attractive investment during uncertainty.

- The company's Q3 results showed solid growth, and it raised its full-year outlook, projecting a 13% year-over-year growth in EPS.

- JNJ offers a solid 3% dividend yield backed by a 61-year track record. Its AAA balance sheet rating and 46% payout ratio ensure strong safety and reliability.

- The stock's current blended P/E stands at 16.2x, under the 20-year average of 17.7x, signaling a discount and offering a margin of safety.

- With an anticipated 5% annual EPS growth over the next two years, I'm building a case for returns exceeding 10%.

In my previous coverage of Johnson & Johnson ( JNJ ) in September 2023, I rated the stock as a hold because I didn't see significant drivers for growth. This was despite the Kenvue Inc. ( KVUE ) spin-off, which was supposed to unlock the value of its more profitable pharmaceutical and medical technology sectors.

With the spin-off , JNJ received $13.2 billion in cash and traded 1.54 billion shares of Kenvue for JNJ shares, resulting in a 7.3% reduction in JNJ's outstanding shares. Consequently, they now hold a 9.5% stake in the newly separated consumer health entity.

After splitting from Kenvue, JNJ revised its full-year 2023 earnings guidance to $10.07 to $10.13, a decrease from the initial projection of $10.70 to $10.80 issued in July. To me, this adjustment highlighted management's uncertainty regarding future growth.

{kind=link}

My neutral stance on the stock has panned out, as the returns have been lackluster, hovering around 0%. In comparison, the S&P 500 index has surged ahead, outperforming the company by nearly 6%.

As we step into 2024, uncertainties about the economy linger, with a potential GDP slowdown and the possibility of a hard landing on the horizon.

Given these circumstances, I think it is an opportune moment to consider investing in defensive businesses trading at discounted rates, with quality earnings, and JNJ fits that description.

Let me walk you through why I think so.

Business Update

Lately, the pharmaceutical buzz has revolved around GLP-1 drugs. Beyond their role in managing blood sugar and aiding weight loss, these medications appear to offer significant additional advantages. Studies suggest that certain drugs in this category might reduce the risk of heart-related conditions like heart failure, strokes, and kidney disease. People using these drugs have reported improvements in blood pressure and cholesterol levels.

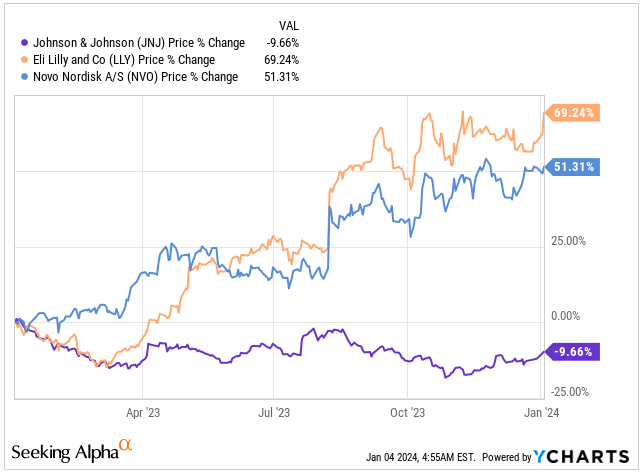

As a result, companies like Eli Lilly and Company ( LLY ), boasting a remarkable 69.2% return last year, and Novo Nordisk A/S ( NVO ), with a solid 51.3% return, have dominated discussions in the pharmaceutical arena. Meanwhile, legacy medical companies, despite their robust strengths and established positions in the market, have somewhat been left behind in the buzz.

{kind=link}

Amid the uncertainties clouding the economy and the potential impact of elevated interest rates on both economies and heavily indebted companies, JNJ stands out for its consistently strong performance.

This strength is attributed to its in-demand products and rock-solid AAA-rated balance sheet, which helped it weather last year's steep rate hikes, as demonstrated in its robust Q3 results .

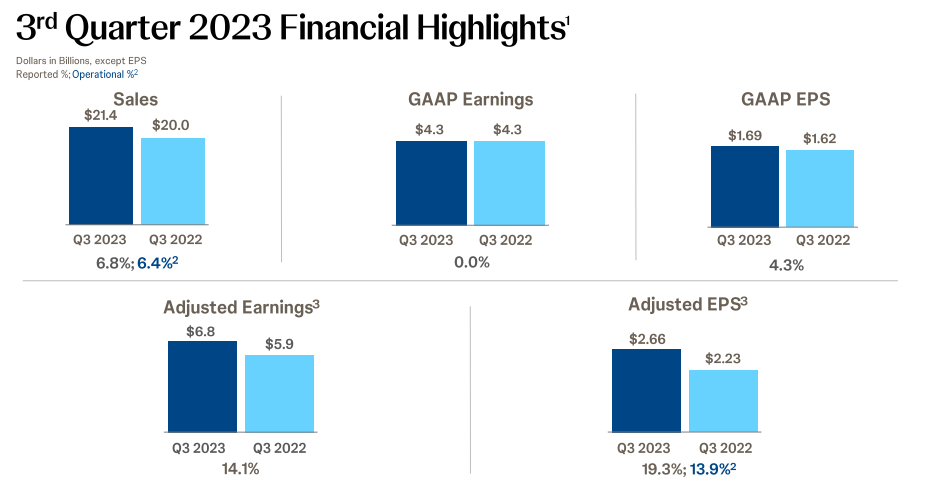

In specific figures, global revenues hit $21.4 billion, marking a 6.8% increase over the previous year. Even in constant currency, there was a solid 6.4% growth. Sales surged by 11.1% in the U.S., while internationally, growth was at 1.6%.

{kind=link}

It's worth noting that this growth was somewhat hindered by the absence of COVID-19 vaccine sales compared to the previous year and the loss of exclusivity for its ZYTIGA medication. Yet, achieving mid-single-digit growth in such an uncertain market is impressive.

Despite a challenging inflationary landscape, JNJ maintained robust margins in Q3. Its gross profit margin remained steady at 69.1%, while the operating profit margin expanded from 28.3% to approximately 30%.

Despite a near doubling of net interest expenses to $182 million, they only accounted for a negligible 0.8% of total revenues.

This was due to the company's substantial $19.7 billion cash reserve generating strong interest income, partly offsetting the increased interest expenses on its $26.1 billion in long-term debt.

Consequently, the bottom line looked strong, with EPS helped by buybacks reaching $1.69, a 4.3% increase from last year's $1.62.

Looking ahead, I foresee JNJ maintaining its strong performance, aligning with management's guidance.

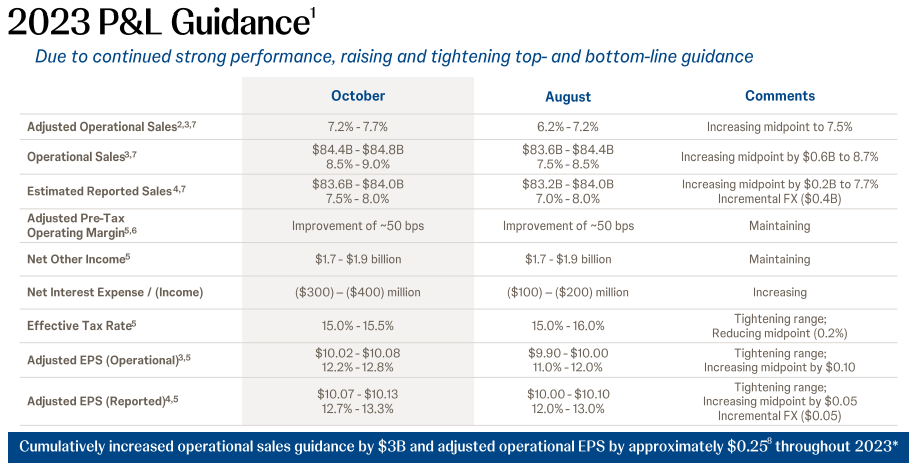

In light of its Q3 results, the company raised its full-year outlook, projecting EPS between $10.07 and $10.13, indicating a 13.0% year-over-year growth at the midpoint.

This surpasses the previous midpoint growth of 12.5%, a promising estimate given the current economic landscape.

{kind=link}

Return To Shareholders

JNJ boasts a legendary dividend growth track record spanning 61 years.

Not only that, but right now, there are just two companies holding AAA ratings: Microsoft and JNJ.

This highlights JNJ's secure balance sheet, suggesting that its dividends are well-supported and there's ample room for long-term growth.

At the moment, JNJ's yield sits at a reasonable 2.96%, appealing to income-focused investors, with a modest 44% payout ratio.

To give you some context:

- Merck & Co., Inc. ( MRK ) yields 2.68%.

- Amgen Inc. ( AMGN ) yields 2.99%.

- AbbVie Inc. ( ABBV ) yields 3.86%.

- Abbott Laboratories ( ABT ) yields 2.01%.

…but none of these companies boast the same level of financial strength as JNJ does.

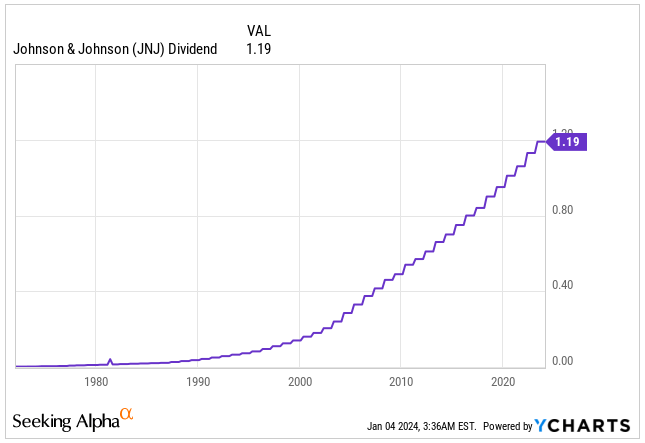

In real terms, the current yield translates to $1.19 per share after the recent 5.3% dividend increase in April.

This increase aligns with a consistent trend over the past five years, averaging a 5.83% annual dividend growth.

This steady growth keeps pace with inflation over the long run, though it's unlikely to accelerate significantly in the future.

Dividend Per Share (Seeking Alpha)

{kind=link}

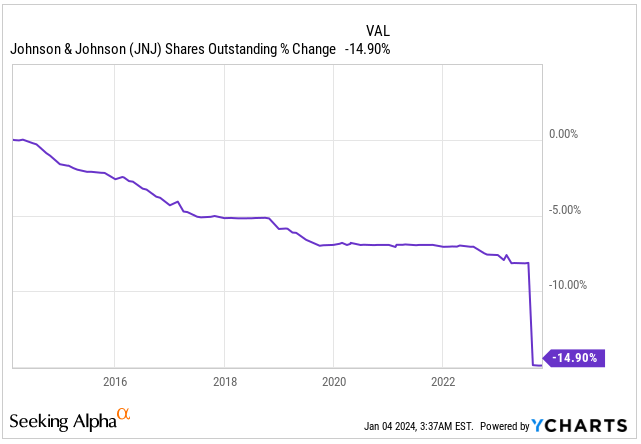

JNJ is also engaged in returning value to shareholders through share buybacks. Over the past ten years, the company has trimmed the number of outstanding shares by nearly 15%. However, it's important to note that the 7.3% reduction last year stemmed directly from the exchange of JNJ shares for Kenvue shares during the spin-off.

Discounting the spin-off's effect, the reduction in shares would have been around 7% over the last decade, which, personally, I find to be a slower pace than I'd prefer.

Shares Outstanding (Seeking Alpha)

{kind=link}

Valuation

When it comes to considering an entry into this stock, I think the current valuation is quite compelling.

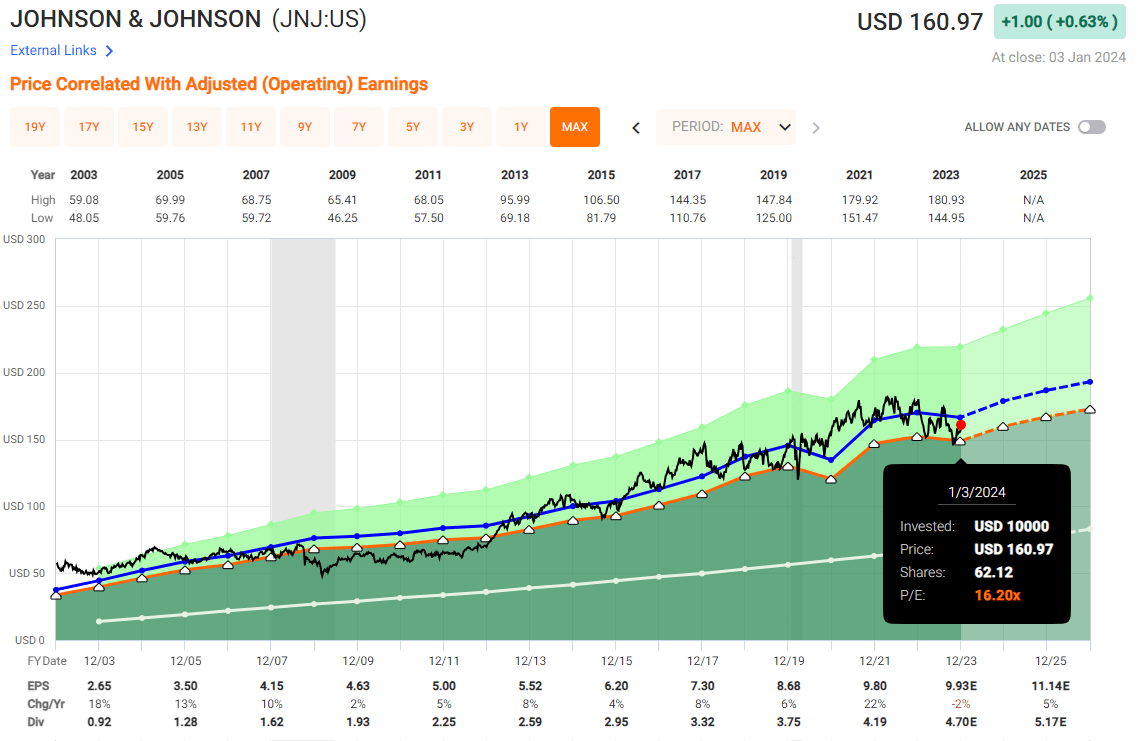

Right now, JNJ is trading with a Blended P/E ratio of 16.2x, slightly below the 20-year average of 17.7x. This suggests there's a slight discount available if you're looking to buy shares.

However, we need to keep an eye on future growth. Over the past two decades, the EPS growth has averaged around 5.3%.

Analysts' EPS projections for FY24 indicate a midpoint of $10.66 for JNJ, signaling a 5.6% increase from the $10.09 midpoint guidance for FY23 provided by management.

If JNJ hits $10.66 EPS in FY24, the stock is presently trading at 15x its forward earnings, notably under the 16.7x non-GAAP forward P/E over the last 5 years.

A similar level of growth is anticipated for FY25 before easing down to 3% by 2026.

{kind=link}

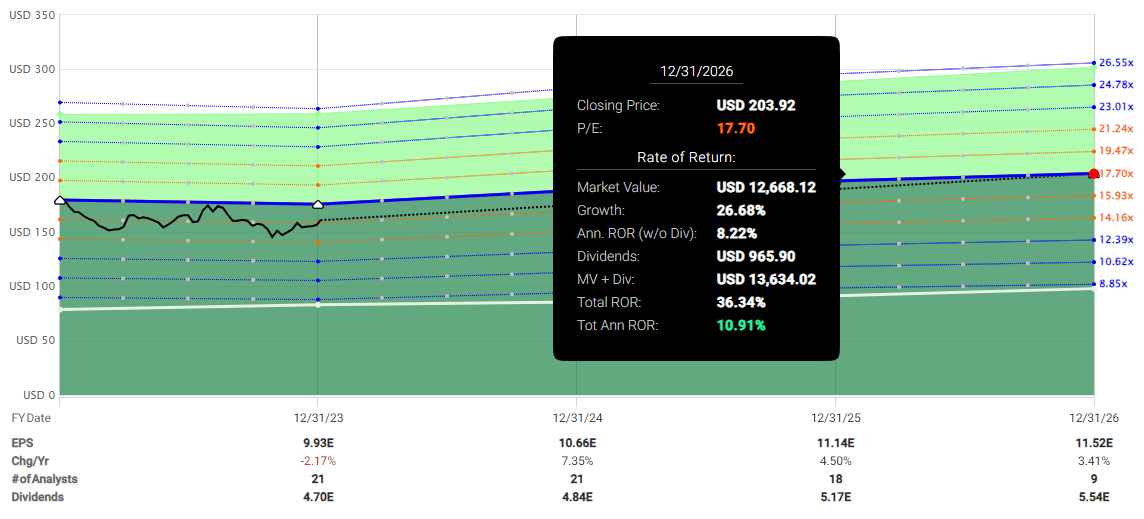

Understanding the future growth trajectory is crucial here, especially with expectations hovering between 3% to 5%. In light of this, I believe the blended P/E of 17.7x seems justifiable.

Considering this, the potential total return appears to be around 10.9% by the end of 2026. This seems quite reasonable, especially given today's economic uncertainties. Even if we encounter a mild recession, I expect JNJ's earnings to remain resilient.

In my view, JNJ would make an excellent addition to any dividend growth portfolio or serve as a defensive stock pick for those seeking to minimize portfolio volatility.

JNJ Potential Return (FAST Graphs)

{kind=link}

Takeaway

Initially, I had reservations about the unclear growth strategy and the lowered guidance for FY23 following the Kenvue spin-off aimed at unlocking growth in JNJ's more profitable pharmaceutical and medical technology sectors. My worries have proven to be timely as JNJ heavily underperformed the market.

However, the Q3 earnings marked a positive first step towards stability, leading to an adjustment, or rather a narrowing, of the guidance for Q4 2023.

Considering that the economy still seems robust but the outlook for 2024 remains highly uncertain, I believe it's a good time to consider adding defensive businesses that could withstand a potential mild recession or even worse conditions.

Currently, JNJ is trading slightly below its fair value, with enough of a margin of safety. Considering earnings are anticipated to grow by around 5% over the next two years, the potential return exceeds 10%.

In today's climate, this represents an enticing value proposition.

For further details see:

Johnson & Johnson: Rock Solid 3% Yield With Over 10% Return Potential (Rating Upgrade)