JOUT - Johnson Outdoors Inc.: Corrective Actions Required Downgrade To Sell

2024-01-05 13:29:32 ET

Summary

- Johnson Outdoors' FY23 results disappointed the market, triggering a well-justified share price fall of ~18%.

- Conditions in the outdoor recreation goods market show no sign of near-term improvement.

- With sales under pressure, the company has not done enough to tackle operating expense growth.

- Inventory remains at highly elevated levels and a write-down in carrying values appears increasingly likely.

- Based on a lack of confidence in JOUT’s ability to deliver sustainable medium-term earnings growth, I am downgrading the stock to a sell.

Introduction

In early October 2023, I upgraded Johnson Outdoors Inc ( JOUT ) to a Buy rating, with the stock then trading at around $53 per share. Very shortly after the upgrade, the stock fell by around -5%, before commencing a rally in late October that continued through until the end of the year. Prior to the US equity market entering its recovery phase, JOUT hit a low of ~$47.50, at which point my Buy call was looking rather badly timed. However, JOUT then followed the broader market upwards. When the share price hit $55 in early December, I happily wiped the egg off my face. That sense of relief proved to be very temporary, as JOUT’s December 8, 2023 4Q23 report triggered a fall of ~18% to ~$44.70. JOUT’s price subsequently staged another comeback, rallying up to around $53 per share, but has since fallen back to ~$48.50. After such a rollercoaster ride since October, I was curious to see what my review of the company’s 4Q23 materials would uncover.

Value Trap Concerns

I have previously written that I find arguments that family/founder-owned businesses can be good investments rather persuasive. Features of family/founder-owned businesses that support sustainable earnings growth include: consistent and strong corporate culture, longer-term time horizons, innovation driven by continual reinvestment, robust balance sheets, and skin in the game. The fact that Chairman and CEO Helen Johnson-Leipold and members of her family and related entities hold approximately 75% of JOUT’s voting stock was one of the reasons that JOUT originally popped up on my radar.

However, having followed the company quite closely for eighteen months or so, I am starting to wonder whether or not JOUT is exhibiting a quite common downside of family/founder ownership – being the inability of minority interests to agitate and drive change when the family/founder’s management of the business is floundering. I have covered other family/founder-owned companies that have proved to be value traps for that very reason. Exhibit 1 below, extracted from the JOUT FY23 Form 10-K , suggests to me that investors in the company should be mindful of the stock’s value trap potential.

Exhibit 1:

{kind=link}

Source: JOUT FY23 Form 10-K, page 16.

A Miserable End to FY23

CEO Helen Johnson-Leipold commented on the FY23 as follows:

The end of the elevated pandemic-driven demand of the past few years, combined with higher inventory levels at retail, resulted in lower sales and profits for our 2023 fiscal year.

Source: JOUT FY23 Result Release, page 1.

The CEO’s comment seems to mainly attribute the poor FY23 outcome to a normalization of the temporarily high demand for outdoor recreation goods during the pandemic. As such, readers might be tempted to conclude that weakness in FY23 was driven by external factors beyond management’s control – but that would be a generous and naïve interpretation in my view.

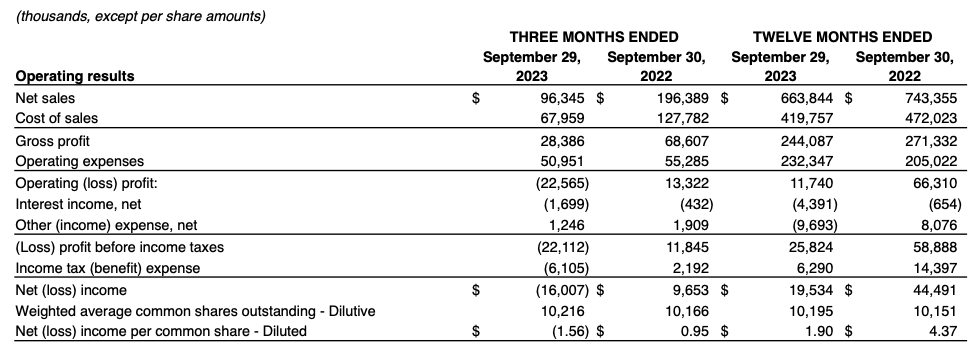

After some signs of improvement in 3Q23, JOUT delivered a dismal 4Q23 result, with a quarterly operating loss of -$22.6m. The FY23 operating profit of just $11.7m was the worst result since the Great Financial Crisis of 2007/2008. Lower sales and higher operating expenses delivered a fall in operating profit of ~82% relative to FY22. Interestingly, the gross profit margin for FY23 of 36.8% was actually slightly up on the FY22 gross profit margin of 36.5%.

Exhibit 2:

{kind=link}

Source: JOUT 4Q23 Result Announcement, page 2.

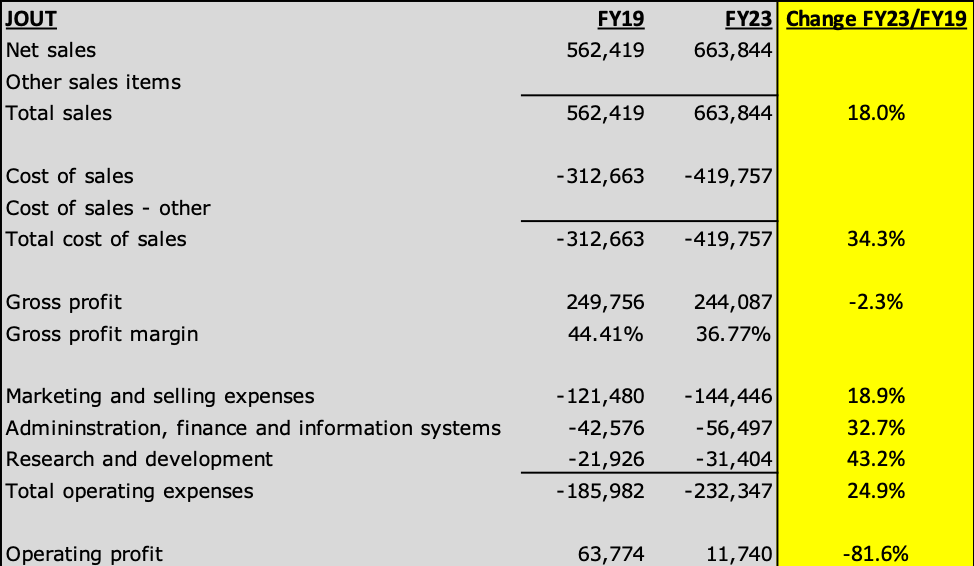

In Exhibit 3 below, I compare JOUT’s FY19 (pre-pandemic) and FY23 financials – this will help to assess whether management’s narrative that FY23 reflects a return to pre-pandemic normality holds water.

Exhibit 3:

{kind=link}

Source: Created by author using data from JOUT quarterly reports.

Despite FY23 sales being 18% above FY19 levels, JOUT’s operating profit has fallen by -2.3% relative to the pre-pandemic FY19, driven by a material contraction in gross margin. The real financial pain however has come through at the operating expenses level, with FY23 operating expenses almost 25% higher than FY19 levels. Whilst I do have some sympathy with management’s argument that JOUT was dealing with a challenging sales environment in FY23, the analysis above highlights that the primary driver of JOUT’s problems relative to the pre-pandemic era has been growth in operating expenses, which presumably management has some control over.

Inventory Level Concerns Continue

In previous JOUT research, I have analyzed and discussed my concerns regarding JOUT’s elevated inventory levels. In October 2023, I described JOUT’s inventory balance as ‘worryingly high’. JOUT’s inventory hit a new high at 4Q23 – in retrospect, I was perhaps not worried enough.

Inventory levels would have been even higher at 4Q23 had JOUT not heavily written down Eureka! tent inventory ($2m of which was donated to a non-profit organization in the period). Excess inventory is a big problem for JOUT. I have highlighted the risk of inventory write-downs in previous JOUT notes; the lack of progress from JOUT to tackle the problem leaves me feeling increasingly concerned. Management’s commentary in the 4Q23 Q&A session suggests that excess inventory is also a problem for JOUT’s retail partners. There is a clearly a lot of unsold outdoor recreation stock sitting on wholesale and retail shelves, gathering dust. Management appears to be hoping that inventory will decline over FY24E:

Inventory remains elevated and is higher than last year by about $12.8 million. We're focused on carefully managing inventory levels as we navigate a challenging marketplace. And I expect we'll see inventory levels decline by the end of the fiscal year. CFO David Johnson

As long as the marketplace and the consumer behaves as we expect, I think we're in okay shape. We obviously have to get those inventory levels down, but if we have a season that we expect, we'll be able to do that. CFO David Johnson

Source: JOUT 4Q23 Transcript , Seeking Alpha.

Should we take comfort from this guidance on inventory? I think not. Firstly, inventory levels are extremely elevated – so even if inventory does fall slightly in FY24E, it will remain much higher than historical levels (both in absolute dollar terms – refer Exhibit 4, and also expressed as a percentage of net sales – refer Exhibit 5). Secondly, the CFO’s response in the FY23 Q&A session regarding how FY24E has started, points to a continuation of weak demand and sales:

So as we look kind of look into the next quarter, we're still seeing a challenging marketplace. So, we're hopeful for a good season, but right now it looks pretty challenging. CFO David Johnson

Source: JOUT 4Q23 Transcript, Seeking Alpha.

Exhibit 4:

{kind=link}

Source: Created by author using data from JOUT quarterly reports.

Exhibit 5:

{kind=link}

Source: Created by author using data from JOUT quarterly reports.

Lack of Action on Costs

JOUT’s revenue line has been under pressure for several quarters, and unless management has been completely asleep at the wheel, they must have predicted that the outdoor recreation goods market would continue to be soggy for a while. In that case, I’d have expected JOUT to begin taking material action on the cost line. Unfortunately, this hasn’t occurred, and management’s plans for FY24E cost reductions are rather underwhelming. In the FY23 Q&A session, the CFO referred to a cost saving program for FY24 that was mostly focused on the product cost line, but there was no detail provided regarding the level of savings being targeted and the associated expected impact on gross margin. At the operating expense level, investors were only offered the rather vague assurance that management would be looking across the enterprise for efficiencies. This lack of a sense of urgency to aggressively reduce costs is disappointing.

Conclusion & Rating

The combination of a continuation of challenging sales conditions for the outdoor recreation goods market, JOUT’s extremely elevated inventory levels, and a lack of action to reduce operating expenses, leaves me feeling very negative regarding the near-term outlook for the company. Further, I am concerned by what appears to be low-quality decision-making and operational execution from JOUT’s management team and board; I therefore lack confidence regarding the ability of the company to deliver sustainable and medium-term earnings growth.

I conclude this review of JOUT with a downgrade to Sell. Although I will continue to monitor this stock, I do not expect to be able to put forward a strong investment case for JOUT until the company has taken actions on both operating expenses and excess inventory.

For further details see:

Johnson Outdoors Inc.: Corrective Actions Required, Downgrade To Sell