JOUT - Johnson Outdoors: Lower Price Isn't Attractive Enough Yet

2023-12-22 23:39:35 ET

Summary

- Johnson Outdoors manufactures and sells recreational outdoors products, such as fishing, diving, camping, and watercraft recreation gear.

- The company's revenues have fallen back into a more sustainable level after experiencing heightened sales during the Covid pandemic.

- The company is experiencing slow demand and a comeback of typical seasonality, deteriorating margins and Johnson Outdoors' revenues in Q4.

- I believe that a financial recover is still highly likely on a medium-term basis.

- The lower stock price doesn't justify a very attractive investment case just yet in my opinion, as the stock seems to be priced for a recovery.

Johnson Outdoors ( JOUT ) is a small cap company that manufactures and sells recreational outdoors products. The company operates in four segments, most notable of which is the fishing segment producing fishing motors, fish finders, downriggers and more under the Minn Kota, Hummingbird, and Cannon brands. The company also sells in diving, camping, and watercraft recreation segments. The company recently decided to quit its Eureka! brand in the camping segment to focus on the more dominant Jetboil brand.

{kind=link}

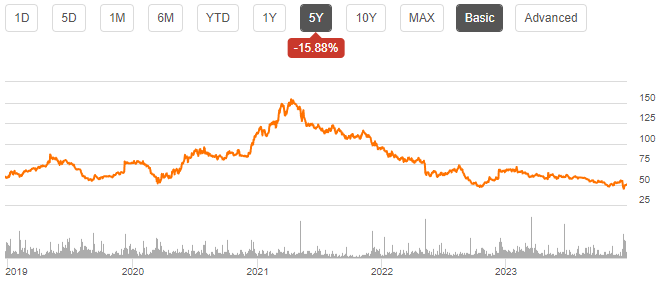

After the company experienced heightened sales during the Covid pandemic, Johnson Outdoors’ revenues have fallen back into a more sustainable level, temporarily deteriorating margins. Due to the fall, the stock hasn’t performed very well in recent times – currently, Johnson Outdoors’ stock only stands at around a third of the 2021 stock peak.

{kind=link}

Revenues Are Now with the Trend Line

After the Covid pandemic boosted the sales of Johnson Outdoors’ products, the company experienced a sharp increase in demand in FY2021 with a revenue growth of 26.5%. Since, revenues have begun to fall back into the more historical trendline. From FY2003 to FY2023, Johnson Outdoors has had a revenue CAGR of 3.8%. From FY2019 to FY2023, the CAGR is 4.2% - when accounting for a higher inflation in the period, the current FY2023 revenues seem to fall within the long-term trend line.

{kind=link}

FY2023 & Q4 Turmoil: A Temporary Slump

Johnson Outdoors reported its Q4/FY2023 results on the 8 th of December. Although revenues have already previously had decreases back into the trend line, the Q4 revenue slump seems more concerning – revenues decreased by a whopping 50.9% year-over-year into $96.3 million, well below any quarterly revenues since the Covid pandemic began. With the lower level in revenues, the company’s earnings also decreased into negative territory through pressured gross margins and negative operating leverage; in Q4, the EBIT margin was -23.4% compared to a previous year EBIT margin of 6.8%. The margin freefall came after already weaker margins in recent quarters. Prior to the pandemic, Johnson Outdoors achieved low double-digit EBIT margins, but the FY2023 margin only stands at 1.8%.

During the pandemic, as supply chains were largely disturbed and demand was heightened, Johnson Outdoors’ normal seasonality pattern was disturbed. Retailers largely had an inventory strategy switch-up from “just-in-time” -inventory management to “just-in-case” management, keeping higher levels of inventory. Johnson Outdoors’ seasonality was disturbed as a result, as can be seen in the long-term quarterly revenues. With the return back into a more normal market environment, the seasonality seems to be coming back, as CEO Helen Johnson-Leipold communicated in the Q4 earnings call . As Q4 is a very weak quarter for the company’s products historically, the return to seasonality patterns had a significant impact on the year-over-year revenue freefall with the Q4/FY2022 not experiencing the same seasonality.

{kind=link}

The management didn’t provide a clear outlook for FY2024, but did communicate in the Q4 earnings call that a soft market environment has continued into the first months of the fiscal year as retailers still have high inventories, and the consumer spending is pressured by macroeconomic instability – I believe that the revenues are likely to fall from a sustainable trend line temporarily due to the low demand. The company has also recently made the decision to exit its Eureka! product line in the camping segment, focusing more on the Jetboil product line. The decision is estimated to affect Johnson Outdoors’ total revenues quite insignificantly, with the management expecting a total revenue effect of less than a percent.

Until Johnson Outdoors’ demand recovers, I expect the company’s margins to stay very low. Prior to the pandemic, from FY2015 to FY2019 Johnson Outdoors had an average gross margin of 42.5%, but the margin has fallen into 36.8% in FY2023 as the company seems to have compensated the lower demand through a lower pricing. The current margins don’t seem to signify a longstanding issue in my opinion; I would expect the gross margin to rise back with a recovery in demand, and a higher level in sales to bring some operating leverage, bringing Johnson Outdoors’ EBIT margin back close to pre-pandemic levels.

Recovery Doesn’t Have Significant Upside Yet

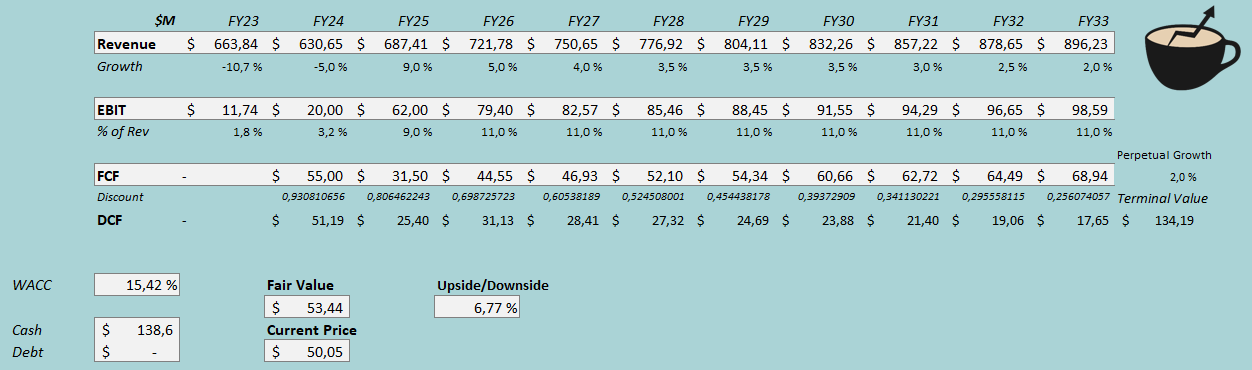

To estimate a fair value for the stock, I constructed a discounted cash flow model. In the model, I still estimate a weak FY2024 with the Eureka! exit and a slow demand with a revenue fall of -5% and only slightly higher margins than in FY2023. Afterwards, I estimate the demand to recover with a FY2025 growth of 9% that slows down into a more historical growth rate, ending up at a perpetual growth of 2%. With the revenue growth, I see a margin recovery as likely – I estimate a FY2026 EBIT margin of 11.0%, 30 basis points below the FY2019 level. As Johnson Outdoors currently has a very large inventory, I estimate the company to have good cash flows in FY2024 despite quite poor earnings with a shrinking inventory.

The mentioned estimates along with a cost of capital of 15.42% craft the following DCF model with a fair value estimate of $53.44, around 7% above the stock price at the time of writing. The stock seems to be roughly correctly valued for a financial recovery.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Johnson Outdoors has decided to maintain a firm balance sheet , as the company doesn’t have any debt used for financing purposes. I estimate the company’s financing strategy to stay the same, with a long-term debt-to-equity ratio of 0%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.89% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July.

Yahoo Finance estimates Johnson Outdoors’ beta at 0.82 . I don’t see the low beta to be a reasonable assumption in the CAPM, as the financials have shown a great deal of turmoil with the macroeconomic turbulence, also represented during the great financial crisis. For a more appropriate beta, I use a beta of 1.90, taken from the average of three peer companies’ betas – Solo Brands’ beta of 2.81 , MasterCraft’s beta of 1.71 , and Marine Products’ beta of 1.17 . Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity and WACC of 15.42%.

Takeaway

Johnson Outdoors is experiencing weak demand and returning seasonality after a pandemic-boosted market, pushing the company’s margins and revenues lower. I am not very concerned about the long-term financial profile, but expect a series of weak quarterly upcoming earnings. The stock seems to be valued fairly with my financial estimates; I’d want a slightly lower price to consider the investment case very attractive. For the time being, I have a hold rating.

For further details see:

Johnson Outdoors: Lower Price Isn't Attractive Enough Yet