JOUT - Johnson Outdoors: Price Decline Opens Up Value Opportunity Again - Upgrade To BUY

2023-10-09 17:17:10 ET

Summary

- Johnson Outdoors' stock price has fallen by over 20% since I downgraded the stock to Hold in January 2023.

- The near-term outlook for sales is challenging, however the company has sufficient capital to comfortably manage through a lengthy period of soggy demand.

- High levels of inventory are a concern and the potential for a one-off write-down in the carrying value of finished goods is a near-term earnings risk.

- Cash and investments represent ~30% of the company’s current market capitalization.

- Based on a normalized earnings valuation framework, I am upgrading JOUT to a BUY.

Introduction

I first published on Johnson Outdoors Inc ( JOUT ) almost a year ago, arriving at a Buy rating with the stock then trading at around $55 per share. By early January 2023, JOUT’s share price had increased by ~23% from my Buy recommendation level, and after reviewing the company’s 4Q22 result, I downgraded JOUT to HOLD. Since my January 2023 downgrade, JOUT has fallen by over 20% and at ~$53, the share price is now below the level at which I initiated with a Buy rating in November 2022. In this note, I will provide an update on the company and consider whether or not the share price decline provides an opportunity to take a more bullish stance. I refer readers unfamiliar with JOUT to my November 2022 article for detailed background information regarding the company.

Operating Performance Trends

JOUT released 3Q23 results on August 3, 2023. Whilst pre-tax profit was slightly above 3Q22 levels, there was not much to get excited about in the numbers. JOUT is a seasonally cyclical business – the third fiscal quarter traditionally falls within the strongest selling season for JOUT’s warm-weather outdoor recreation products – and so it makes sense to compare 3Q23 against 3Q22 to get a sense of the underlying trends.

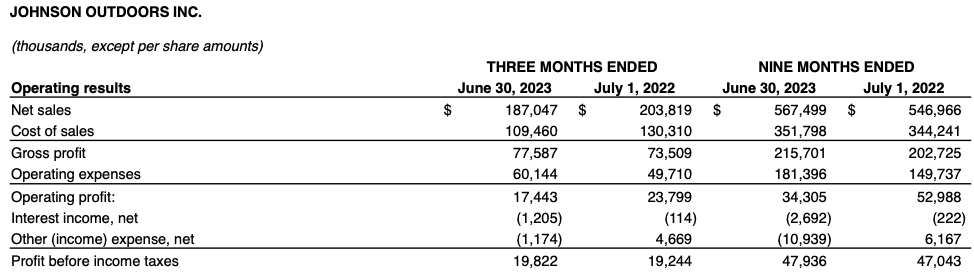

Exhibit 1:

Source: JOUT 3Q23 Profit Announcement, page 2.

{kind=link}

3Q23 gross profit came in +5.5% versus 3Q22, however much higher expenses in 3Q23 resulted in operating profit falling by -26.7% relative to 3Q22. In terms of margins, the gross margin improved to 41.5% (3Q23) from 36.1% (3Q22) but the operating profit margin outcome was weaker, coming in at 9.3% (3Q23) versus 11.7% a year earlier. At the profit before tax level, JOUT enjoyed the benefit of higher interest rates on its healthy cash balance in 3Q23, which boosted earnings by ~$1.1m relative to 3Q22. The year-to-date comparison against FY22 isn’t all that pleasing either, with gross profit up by 6.4% but operating profit down by -35.3% in FY23. Exhibit 2 provides a slightly longer-term perspective and shows that the 3Q operating margin in 2023 was lower than the corresponding quarter in each of the three prior years.

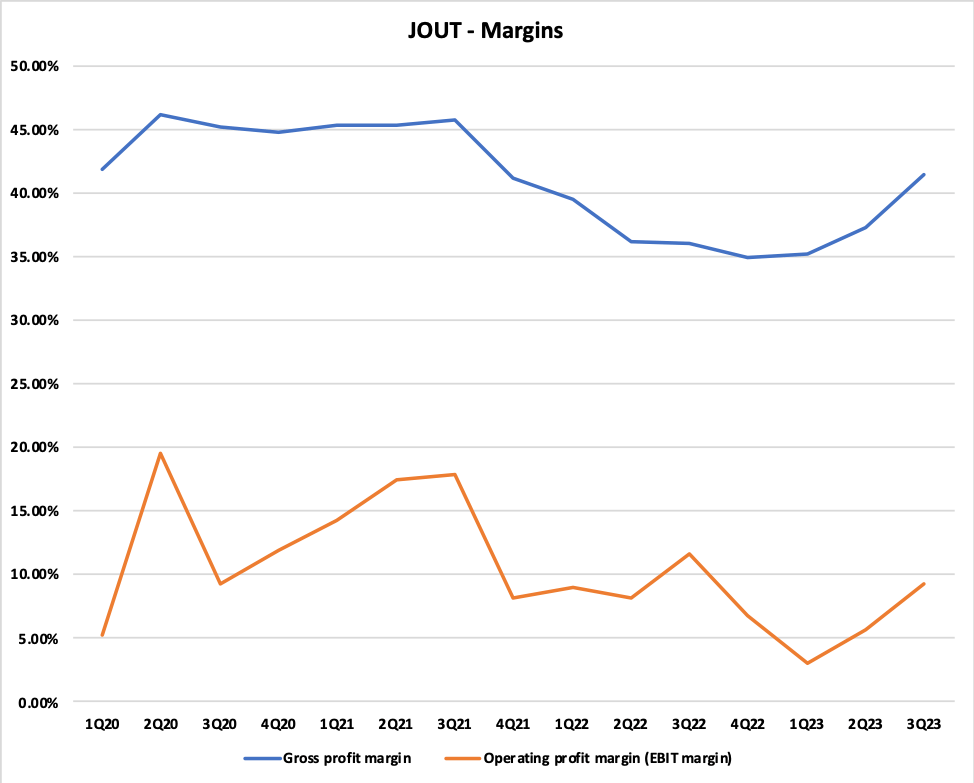

Exhibit 2:

Source: Created by author using data from JOUT quarterly reports.

{kind=link}

It is worth highlighting here that there can be some accounting ‘noise’ in JOUT’s operating profit margin trends. In simple terms, JOUT reports an expense item within operating profit relating to deferred compensation which is offset by a reversing item at the ‘Other income/expense’ line. Looking at 3Q23 versus 3Q22, there was a -$5.1m delta at the operating profit level relating to the deferred compensation charge. If I back out this item, then the adjusted 3Q23 operating profit result would have been -5.3% lower than the 3Q22 print (rather than -26.7% unadjusted), and the 3Q23 adjusted operating margin would actually have improved slightly from the 3Q22 level.

It was pleasing to see the gross profit margin move back up above 40% in 3Q23. As Exhibit 2 shows, JOUT’s gross margin was consistently above 40% for eight quarters prior to the downturn that commenced at 1Q22. If we look further back, JOUT’s average gross profit margin for the years FY06 to FY19 inclusive was ~40.7%, and was ~44.4% in both FY18 and FY19. With cost pressures from freight and raw material inputs easing, I think we can expect JOUT’s gross margin to remain north of 40%, albeit with some seasonality. That being said, I do not expect that we will see JOUT returning to the 45% gross profit margin level achieved during the Covid-boom period. My overall assessment of JOUT’s recent operating trends is that the sales environment remains challenging, but that on an underlying basis the company is doing a pretty good job at managing both the gross margin and the operating profit margin.

Supply Chain, Logistics and Inventory Management

I have previously written about the problems that JOUT has experienced with management of its supply chain, logistics, and inventory levels. It remains an open question as to whether or not JOUT’s problems in these areas have been due to external factors (supply chains were significantly disrupted by Covid across many industries) or internal factors (poor management, over-reliance on a limited number of suppliers).

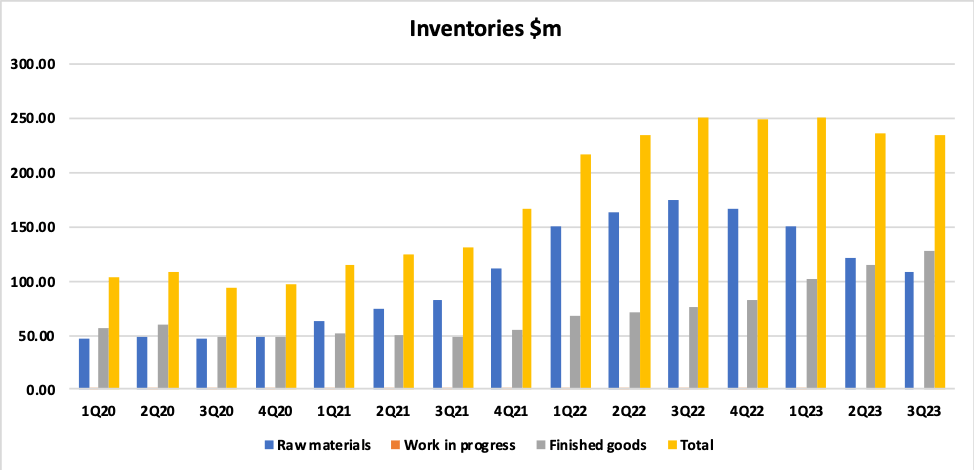

Balance sheet inventory levels averaged ~16.3% of net sales for the five-year period ending FY20. Inventory spiked to 22.2% of net sales in FY21, and increased to 33.4% of net sales in FY22. Inventory levels peaked in dollar terms at 1Q23, hitting $251.5m, up massively from FY19 inventory of ~$95m. Thankfully, inventory has reduced over recent quarters, coming in at ~$235m at 3Q23. Relative to net sales over the last twelve months, 3Q23 inventory represents ~30.8% of net sales – this is an improvement from the FY22 read, but it is still worryingly high.

Exhibit 3:

Source: Created by author using data from JOUT quarterly reports.

{kind=link}

With inventory at such high levels, and having been so for several quarters, there is a material risk that JOUT may need to write-down reported inventory values in coming periods. As Exhibit 3 shows, the ramp up in inventories of raw materials in FY21 and FY22 has now fed through into high inventory levels of finished goods. The outlook for sales in JOUT’s markets is challenging in my view due to a) softening of demand due to Covid having pulled forward sales, and b) cost-of-living pressures causing a drop-off in consumer discretionary spend. The combination of high inventory levels and a soft demand outlook is a clear near-term negative for the JOUT investment case.

What About Value?

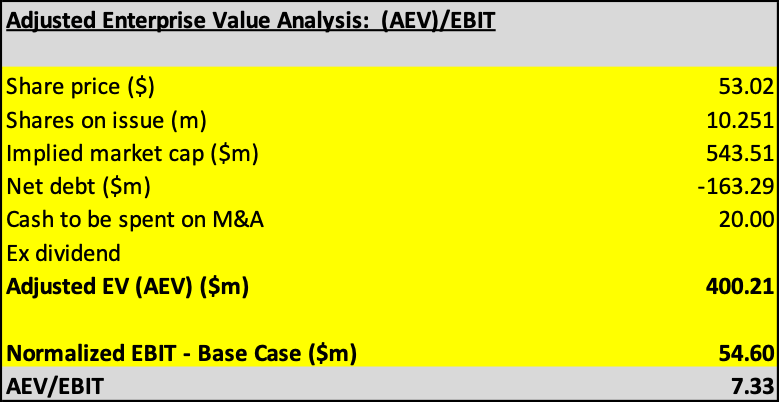

For manufacturing and retail stocks, my preferred valuation metric is EV/EBIT. Exhibit 4 sets out my calculation of AEV/EBIT, where AEV is the adjusted enterprise value, and EBIT is my current Base Case normalized EBIT. JOUT has no long-term debt and as of 3Q23 the company had cash and investments totalling $163m (representing ~30% of JOUT’s current market capitalization).

Based on management commentary over recent quarters, I would not be surprised if JOUT used some of its cash balance to invest in a business that would give the company better control over its supply chain. In my calculation of AEV, I therefore allow for an acquisition spend of $20m (which is assumed to be neutral from an earnings perspective).

Exhibit 4:

Source: Created by author using data from JOUT quarterly reports.

{kind=link}

For a small-cap manufacturer of consumer goods such as JOUT, I would typically regard an EV/EBIT multiple in the range of 9x to 11x as representing around fair value. Based on a current share price of $53.02 (market close October 6, 2023), my analysis points to JOUT trading on a EV/EBIT multiple of ~7.3x.

Summary & Conclusion

- The near-term sales outlook for JOUT is challenging, with consumers tightening up on discretionary spending.

- High inventory levels are concerning and provide the potential for a one-off negative hit to earnings from a write-down of the value of finished goods.

- JOUT’s balance sheet is very strong, with no debt and cash and investments of ~$163m as at 3Q23.

- JOUT has sufficient balance sheet capacity to manage through a period of soggy trading conditions, although the company may be tempted to chew up some of this cash with an acquisition.

- JOUT’s share price has fallen by over 20% since I downgraded it to a HOLD in January 2023.

- Based on a normalized earnings valuation framework, JOUT offers appealing value. I am upgrading JOUT to BUY (at around $53 per share).

For further details see:

Johnson Outdoors: Price Decline Opens Up Value Opportunity Again - Upgrade To BUY