VNQ - Jones Lang LaSalle Q4 Results: Weakened Real Estate Market But Shares Remain A Bargain

2023-03-06 02:28:22 ET

Summary

- Jones Lang LaSalle's Q4 and FY2022 results reflected the current headwinds in the real estate market, but there are reasons to be optimistic the downturn will be short.

- The company remains confident it can achieve its 2025 financial targets of $10 billion to $11 billion in fee revenue with a 16% to 19% adjusted EBITDA margin.

- Despite the headwinds, JLL stock's valuation remains very attractive, and significantly below our estimated fair value.

We really enjoy following the earnings calls from Jones Lang LaSalle ( JLL ) and CBRE Group ( CBRE ) because they share a lot of information regarding the state of the real estate market, which can be useful even for investors buying ETFs like the popular Vanguard Real Estate ETF ( VNQ ). For example, what we heard from both companies reinforced our view that one of the most challenged sectors continues to be offices, and as a result investors should be particularly cautious before investing in office REITs such as Boston Properties ( BXP ) and Kilroy Realty ( KRC ). According to JLL Research volume for the global office leasing market was down ~19% y/y in the fourth quarter, and global office vacancy rates increased to ~14.9%, with increases across all regions. While increasing interest rates have affected most real estate sectors, including multi-family, retail, and industrial, it is the office segment that is showing the most significant weakness, given the additional headwind from the work-from-home trend. Office cap rates have increased considerably since the end of 2019, when they were mostly in the rage of 3.75% to 4.25%, and now they are around 6% to 7%.

Focusing on JLL's earnings, we heard a very similar story to that of CBRE's results . Basically that their resilient business lines are performing relatively well, these are businesses like property management and workplace management. At the same time, transactional business lines are seeing significant declines. JLL reported seeing a rapid slowdown in the fourth quarter in investment sales and leasing volumes, but it expects the current slowdown to be relatively short. The company is looking forward to a strong recovery in the transactional environment during the second half of this year.

JLL Research estimates that global commercial real estate investments were $203 billion in Q4, a 56% y/y decline. There is, however, significant dry powder waiting to invest, with an estimated ~$386 billion sitting on the sidelines. One of the reasons the company is relatively optimistic about the second half of 2023 is that it expects this dry powder to be deployed once interest rates stabilize and the bid-ask spreads normalize. During the earnings call, JLL reaffirmed that it is confident it can achieve its 2025 financial targets of $10 billion to $11 billion in fee revenue and a 16% to 19% adjusted EBITDA margin. It also expects to realize $125 million of cost savings in 2023 from its cost savings initiatives.

JLL Investor Presentation

Q4 and FY2022 Results

In FY2022 consolidated fee revenue rose 7% to $8.3 billion, while adjusted EBITDA declined 14% to $1.2 billion. The adjusted EPS of $15.71 represents a decline of ~17% y/y despite the lower share count. In Q4 fee revenue declined ~16% y/y, despite resilient business lines such as workplace management collectively growing ~12%. In the fourth quarter adjusted EBITDA fell 42% y/y to $339 million, while Q4 non-GAAP EPS was $4.36. JLL Technologies saw significant valuation declines in the quarter, but we remain optimistic about its long-term potential given its impressive historical IRR.

JLL Investor Presentation

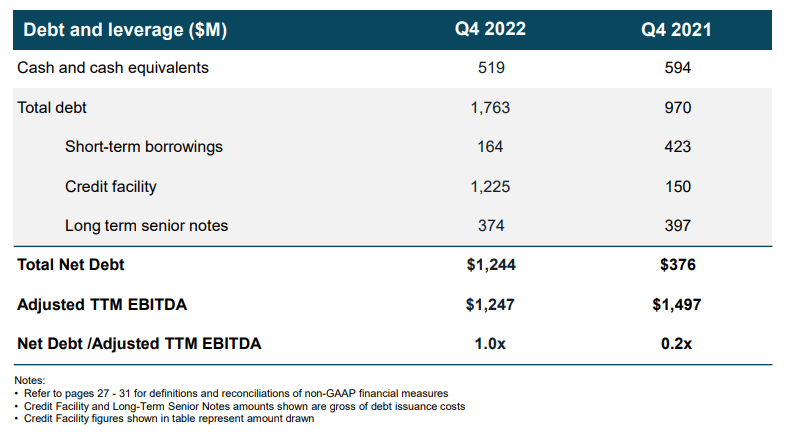

Balance Sheet

JLL completed ~$600 million in share repurchases during 2022, reducing the share count by ~5%. It expects to resume buying back shares in 2023 after pausing during Q4 2022. JLL ended the year with net leverage of 1.0x, which is at the midpoint of its target range, and up from 0.2x a year earlier. Its total liquidity is ~$2.6 billion when including its $2.1 billion undrawn credit facility.

{kind=link}

Valuation

While it is evident that JLL is facing significant headwinds due to the weakening real estate sector, partly as a result of the rising interest rate environment, its valuation remains very attractive. Both the trailing twelve months and the forward price/earnings ratios are currently below the ten year average p/e multiple.

JLL appears to see significant value in its shares at current prices, given that it has been very aggressive with its share repurchasing activity. This has resulted in a very high net common payout yield, and a significant reduction in shares outstanding.

Based on our estimates for future earnings for JLL we believe the net present value of its future earnings stream to be approximately $258. With shares currently trading at $173, we believe they are significantly undervalued by ~33%. We are therefore maintaining our 'Strong Buy' rating, despite 2023 looking like a challenging year for the company.

| Adj. EPS |

| Discounted @ 10% |

| FY 23E |

| 14.81 |

| 13.46 |

| FY 24E |

| 17.28 |

| 12.24 |

| FY 25E |

| 19.83 |

| 11.13 |

| FY 26E |

| 20.62 |

| 11.80 |

| FY 27E |

| 21.45 |

| 12.31 |

| FY 28E |

| 22.31 |

| 11.64 |

| FY 29E |

| 23.20 |

| 11.01 |

| FY 30E |

| 24.13 |

| 10.41 |

| FY 31E |

| 25.09 |

| 9.84 |

| FY 32E |

| 26.09 |

| 9.30 |

| FY 33E |

| 27.14 |

| 8.79 |

| Terminal Value @ 3% terminal growth |

| 428.42 |

| 136.51 |

| NPV |

| $258.44 |

Risks

JLL's earnings are very highly correlated to the general state of the real estate industry, which is currently facing considerable headwinds, particularly in the office sector. Should a recession arrive this year things would get even more complicated for the company. That said, these risks are mitigated by the company's strong balance sheet and its business diversification. JLL is currently benefiting from some of its business segments proving very resilient to difficult economic conditions, in particular its property management and workplace management businesses.

Conclusion

After reviewing JLL's Q4 and FY2022 results we are maintaining our 'Strong Buy' rating. It looks like the first half of 2023 will be particularly tough for the company, but there are reasons to believe the second half of the year should see some improvement. There is a significant risk of recession, which would further complicate things for the company. Despite these short-term headwinds, we are optimistic about the company's future, especially after JLL reaffirmed its FY2025 financial targets. We believe shares are trading with a significant discount to fair value, creating a potential opportunity for patient long-term investors.

For further details see:

Jones Lang LaSalle Q4 Results: Weakened Real Estate Market, But Shares Remain A Bargain