JNCE - Jounce: Gilead's GS-1811 Buyout Allows A Further Bounce

Summary

- Jounce has recently announced that it has sold its entire rights to immunotherapy candidate GS-1181 to Gilead for $67 million.

- I expect the biotech company to now have around $170 million cash, with a market cap of about $55 million.

- In line with bearish biotech times, the stock moved up 85% post-market to finally end the day only 35% higher.

- Jounce’s pipeline look promising and impressive, including three Phase 2 trials.

Thesis

Jounce Therapeutics ( JNCE ) has been on my radar for quite a while, in light of its impressive pipeline, oversold-looking chart, and the Gilead deal on immunotherapy candidate GS-1181. That Gilead deal has been the subject of recent news, as Gilead (GILD) has bought out all the rights to it for $67 million. Jounce could have received much more in milestone payments, if these would have been met, but nobody knew when these payments were due, nor how Gilead was to take GS-1181 forward. If anything, I see the deal as a vote of confidence in Jounce’s current pipeline. The company is now flush with cash to weather the current biotech storm, however long it may still last.

After having gone up more than 85% post-market, Jounce’s stock ended the trading day 35% up, with 34 million shares exchanged. That’s quite a bit of shares, but the added value represents less than one third of the cash value added.

It would take about 200% for Jounce’s stock to reach cash level, and given its current assumed cash position and the potential of its Phase 2 assets in its pipeline, I believe a Strong Buy rating is in place here.

Company and share price

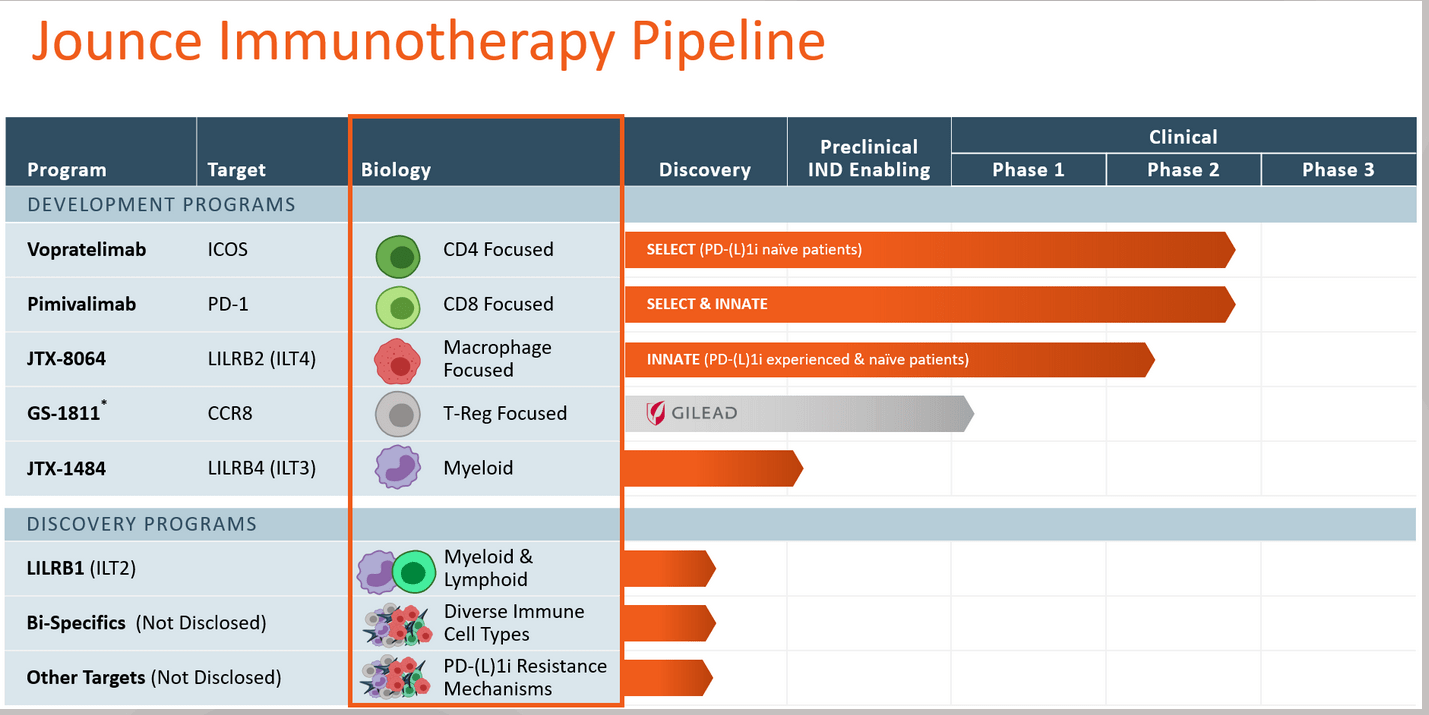

Jounce is a biotech company with three Phase 2 drug candidates, one preclinical stage candidate and three discovery programs. Its pipeline is shown below.

Company pipeline (Corporate Presentation)

{kind=link}

One needs to exclude GS-1811 from its pipeline as that has just been sold to Gilead. I will say something on this first, as it has been the subject of recent news.

Jounce focuses on targets in the tumor microenvironment, that means in solid tumors. Seeking Alpha contributor Biologics’ last year’s coverage took a deep-dive into that pipeline. At the time, the company’s market cap was still $367 million. Currently it is trading at one seventh of that price; the sell-off has been endless. This chart shows its share price over a year’s time.

Jounce stock price one year (Ycharts)

{kind=link}

Consequences of the sale of GS-1811

GS-1811, or formerly JTX-1811, was an anti-CCR8 antibody that had been designed to selectively deplete immunosuppressive tumor-infiltrating T regulatory cells in the tumor microenvironment, which Gilead had licensed from Jounce in August 2020. GS-1811 had CCR8 as its target, and had the potential of activating the immune system through this new pathway, but was still in Phase 1 trials. The August 2020 license deal , with an $85 million upfront payment and $35 million equity investment by Gilead, came with interesting milestone payments, as it allowed Jounce to receive up to $645 million in milestone payments and high single digit to mid-teens royalties. On December 27, 2022, Gilead bought out remaining contingent payments all at once for $67 million, thereby also terminating operational requirements as they had been set forth in the August 2020 license agreement.

The December 27, 2022 press release came with the announcement from Jounce that the Gilead payment allowed it to extend its cash runway, which was important at this time given the challenges in capital markets for biotech companies.

One could criticize Jounce for having sold this asset too soon, and obviously the bearish-minded investors did, but one could also look at it the other way round. Jounce knew this asset well, and was best placed to assess the chances of it making through Phase 1, 2 and 3 trials. The details of the license agreement with Gilead, as amended, were never published, and so nobody knew which milestone payments were due. However, the last quarterly call mentioned that only $40 million had been paid so far, which make it appear that milestone payments were rather small in Phase 1, and would probably become higher the further the asset got in development. It is likely that the truly big payments would only be due once the asset passed Phase 2 and Phase 3 trials. Those moments would be years away, also taking into account the duration of the Phase 1 trial which was particularly long, ending only in February 2025. Meanwhile, Gilead could at any time have lowered its interest in having the asset proceed through trials, resulting in payments not becoming due so easily.

If Jounce made the decision, I believe it may be to boost its cash position to develop its own assets further. In that sense, I see the Gilead buyout as a vote of confidence in these assets, which the market at this time gives a negative value. Interestingly, at the end of one trading day after the news, Jounce's market cap had gone up only $17 million. If one would assume that Jounce’s cash position is currently about $170 million, to reach the level of Jounce’s cash position, the market cap would need to increase about 200%.

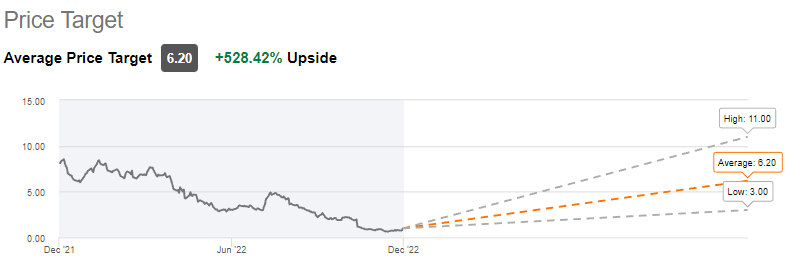

I think the potential upside in light of analyst ratings confirms the major potential here, at +528% on average.

Analyst price targets (Seeking Alpha)

{kind=link}

Obviously, some very bearish sentiment has taken down this stock, as the same sentiment has taken down some others on good news recently, such as Aptevo ( APVO ) or Harpoon Therapeutics ( HARP ).

The potential for that downtrend to continue is, in my eyes, less likely than the opposite.

Consequences for Jounce’s cash position

Jounce’s cash position at the end of September 2022 was $130.3 million compared to $220.2 million as of December 31, 2021. That means its cash burn is quite high, with approximately $120 million over the course of a year. Part of that cash burn will have been related to operational requirements for GS-1811, and will now no longer be due, as Gilead will take over all duties related to that drug candidate.

That means the cash burn may go down, but still with such a burn, Jounce was right to start looking for cash at a given point. And looking for cash in inflationary and bearish biotech times appears to be much tougher than before. Biotech companies with a low cash position may need to either wind down clinical operations, sell some of their assets, or simply end operations fully. Celyad Oncology ( CYAD ) is an example , and I expect others with little cash to follow. I expect big pharma to scoop up some assets of companies with little cash in the upcoming months, either before or after having to wind down operations. Jounce is off the hook for now.

Jounce’s pipeline

Introduction

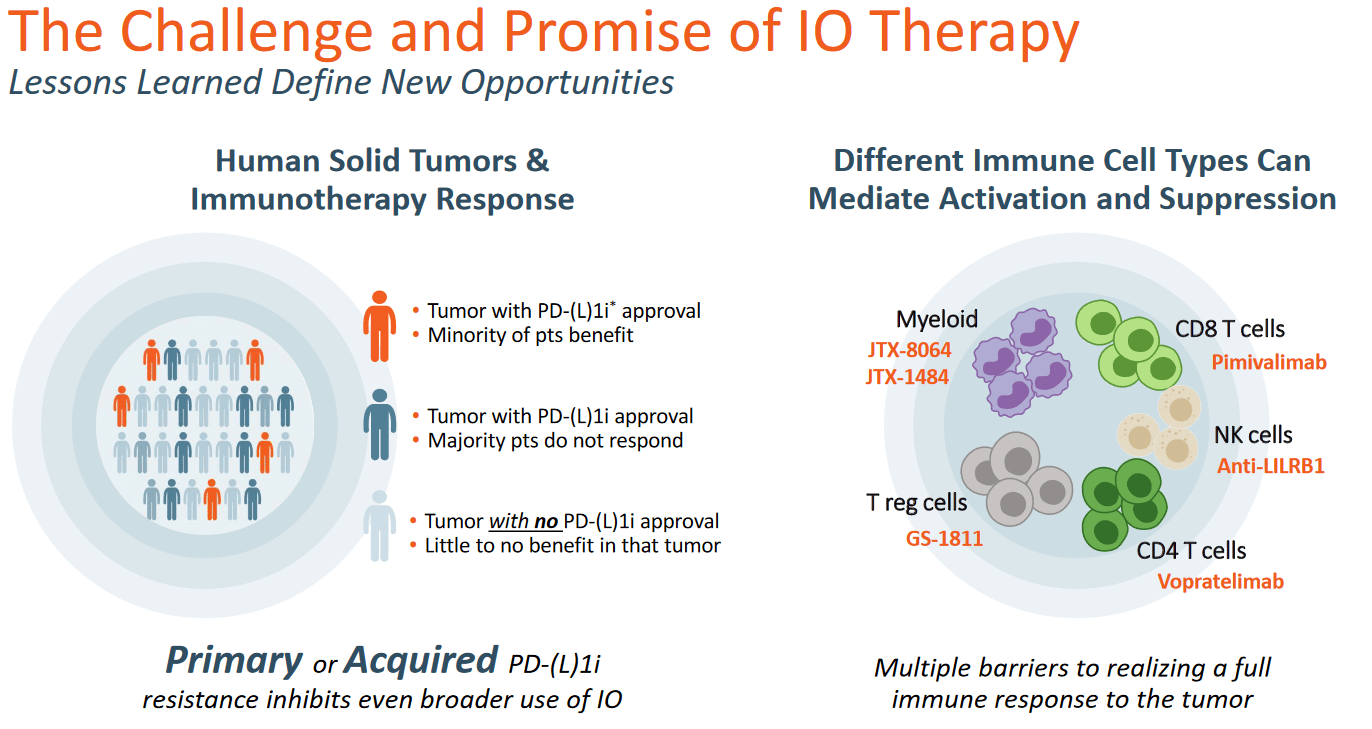

Jounce’s translational discovery platform allow identification of targets to develop drug candidates, which has so far results in a number of interesting drug candidates, one of which Gilead had shown interest in.

The company’s pipeline aims to develop next generation immunotherapy products, targeting different targets in different cell types of the immune system, and taking into account that patients on existing immunotherapy either do not react or develop resistance against such therapy.

IO opportunity and drug candidate targets slide (Corporate Presentation)

{kind=link}

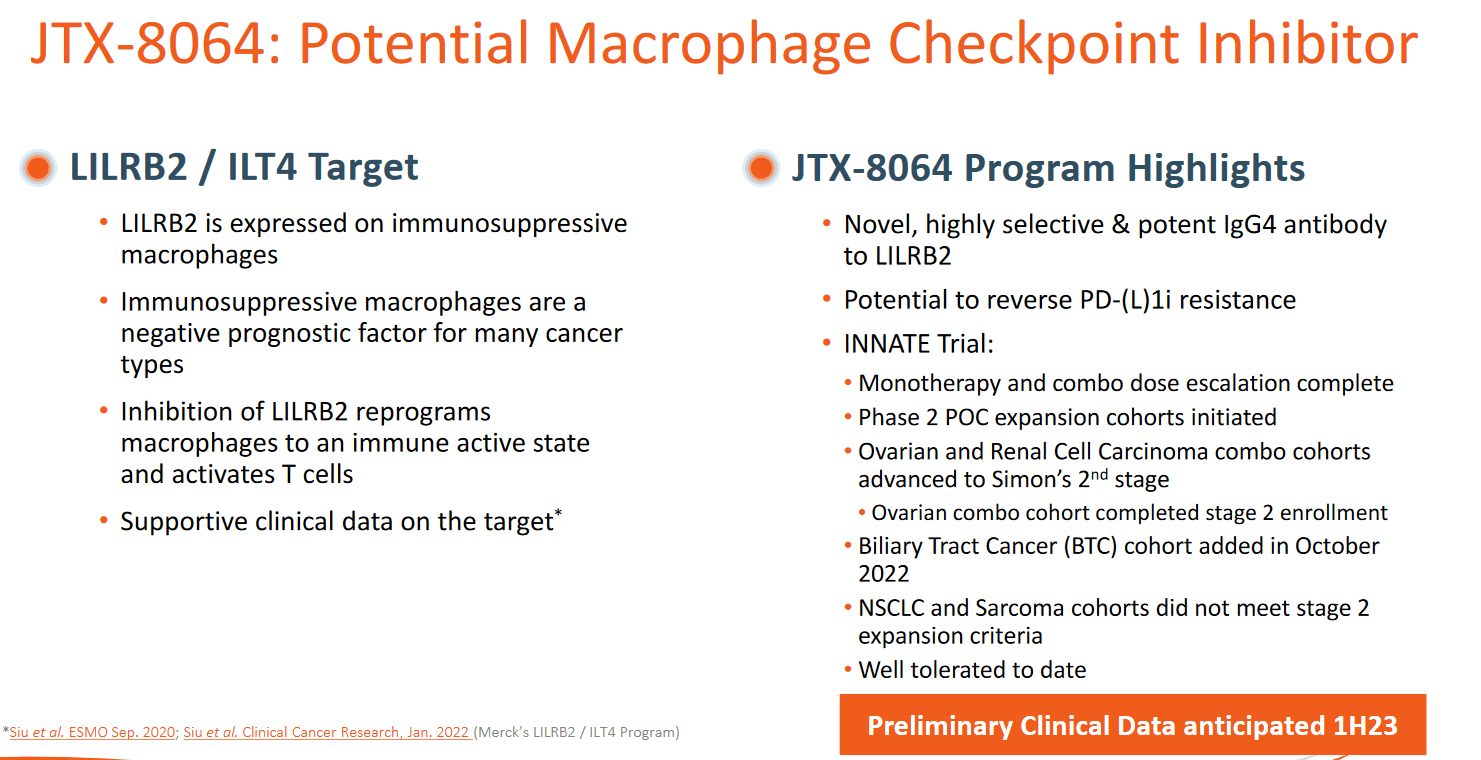

JTX-8064

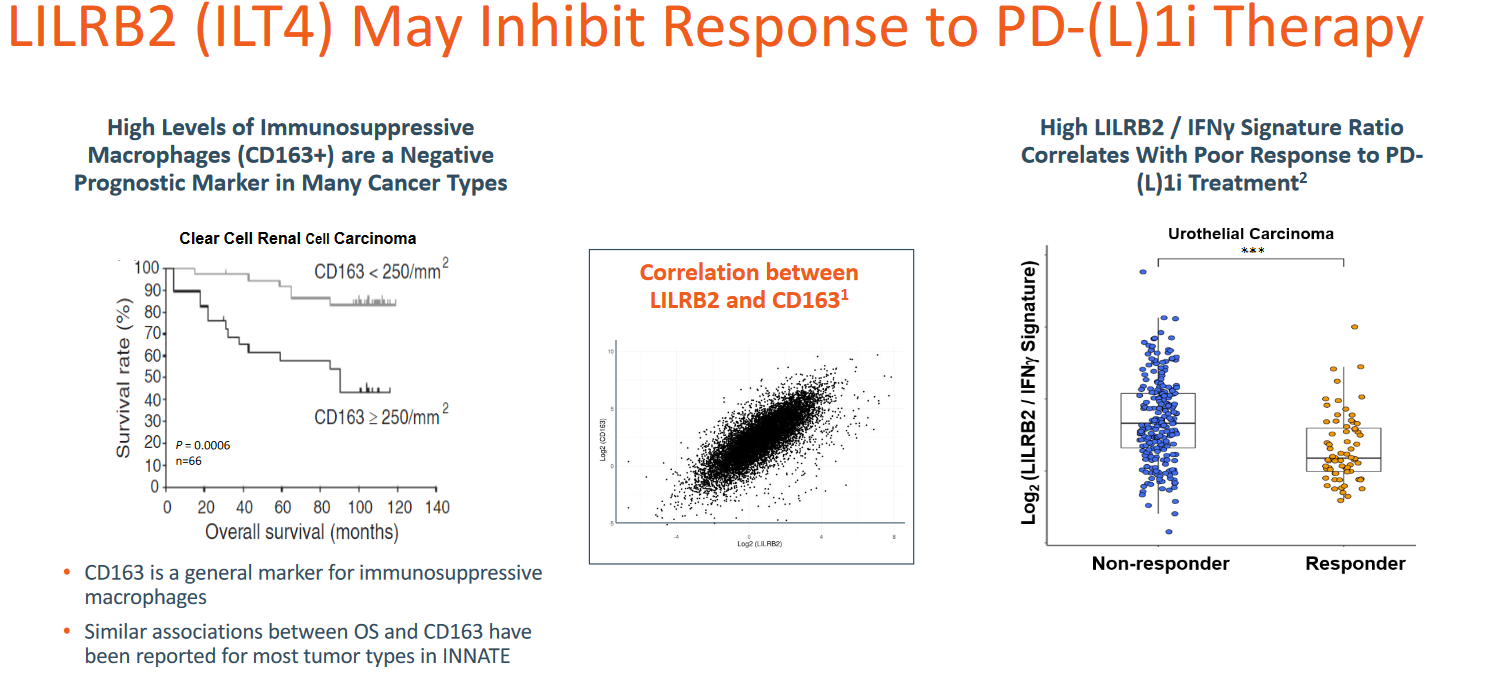

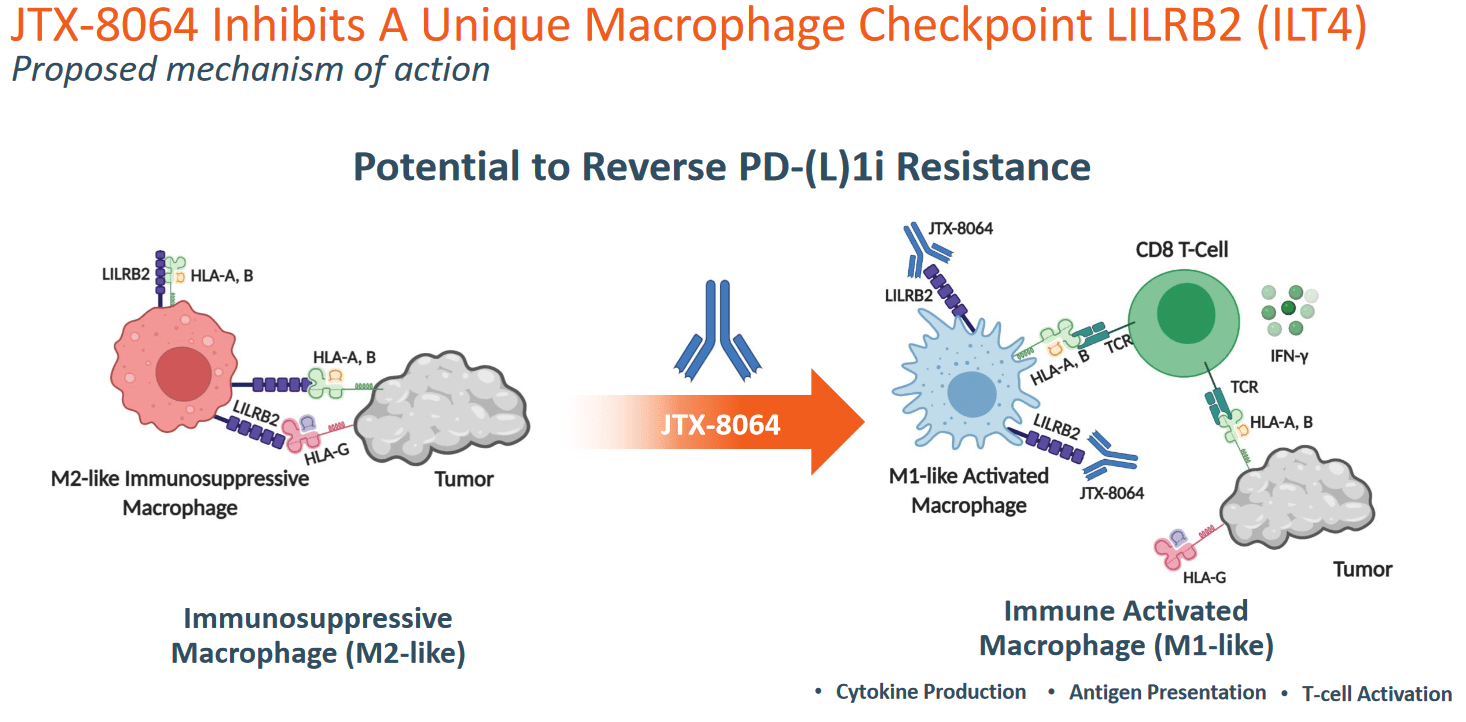

The company’s prime candidate is JTX-8064, a potential macrophage checkpoint inhibitor targeting LILRB2/ILT4 to prevent immunosuppression and activate T cells in the TME, with the potential to reverse PD-((L))1i resistance.

JTX-8064 MoA slide (Corporate presentation)

{kind=link}

The target, LILRB2/ILT4, could namely be implicated in resistance to PD-((L))1i therapy, and has as its goal to reverse that resistance.

JTX-8064 preclinical results slide 1 (Corporate presentation) JTX-8064 MoA slide 2 (Corporate Presentation)

{kind=link}

{kind=link}

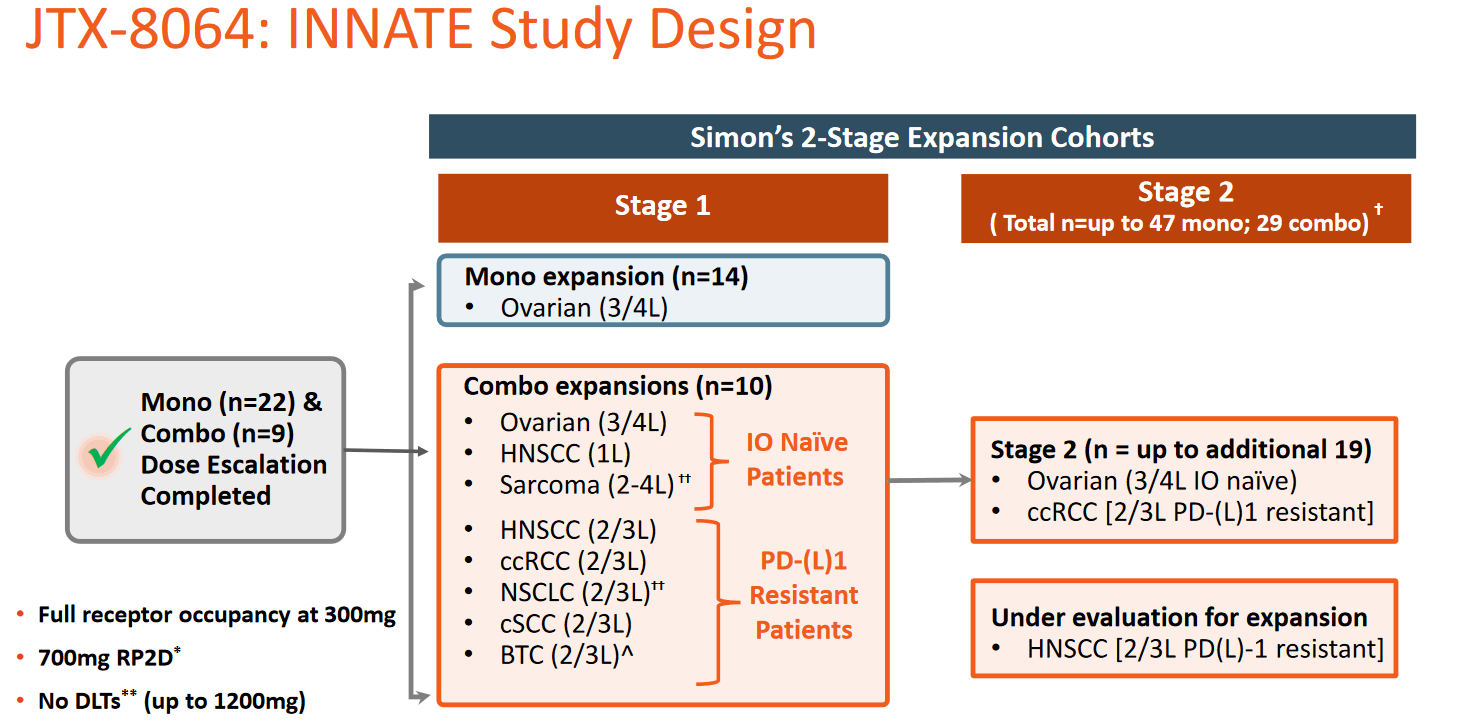

JTX-8064 is in a Phase 1/2 open label trial for solid tumors, which is currently in the Phase 2 part of that trial expecting to end in January 2024. It is well tolerated, and data generated so far show most promise in ovarian cancer and renal cell carcinoma. The ovarian combo cohort has completed the stage 2 enrollment, and a biliary tract cancer cohort has been added in October 2022. Preliminary data are due in the first half of 2023, which will entail data on all mono and combo dose escalation study arms, and preliminary biomarker data.

JTX-8064 Innate study (Corporate Presentation)

{kind=link}

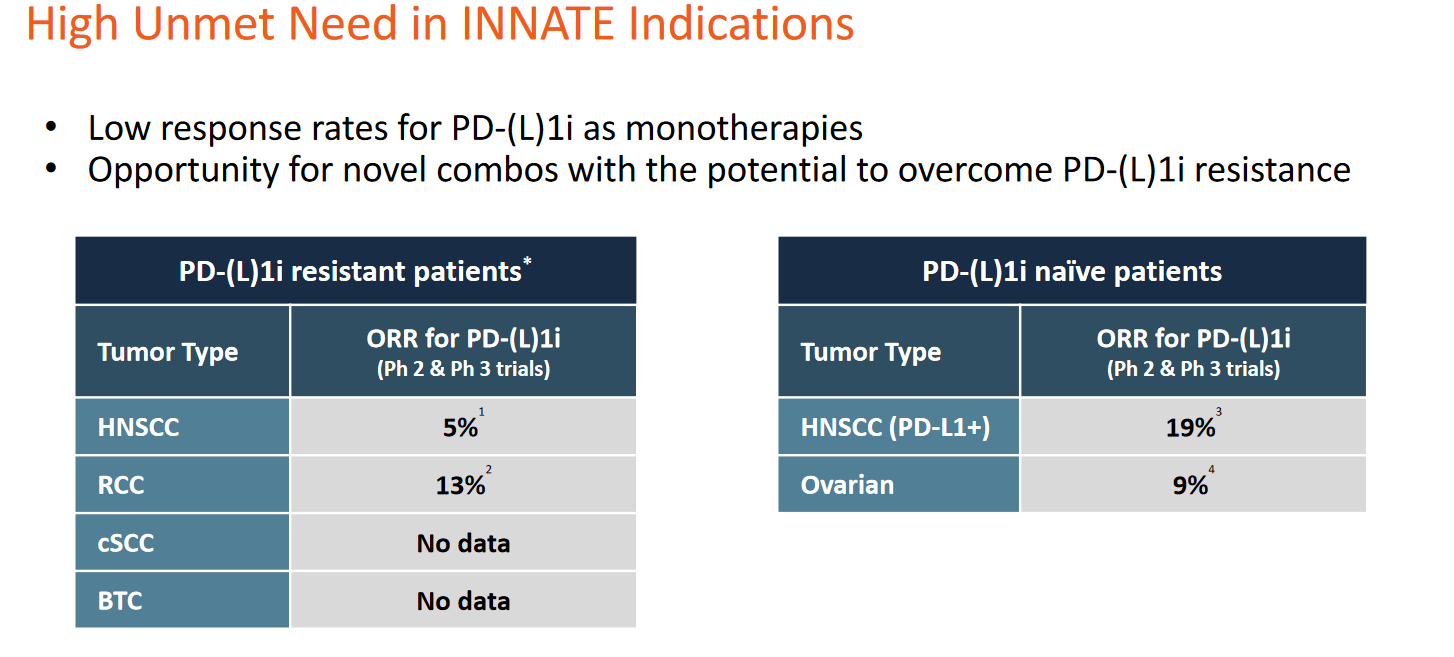

The unmet medical need in some of these indications is high, given the high level of resistance to existing immunotherapy.

Unmet need slide (Corporate Presentation)

{kind=link}

Vopratelimab

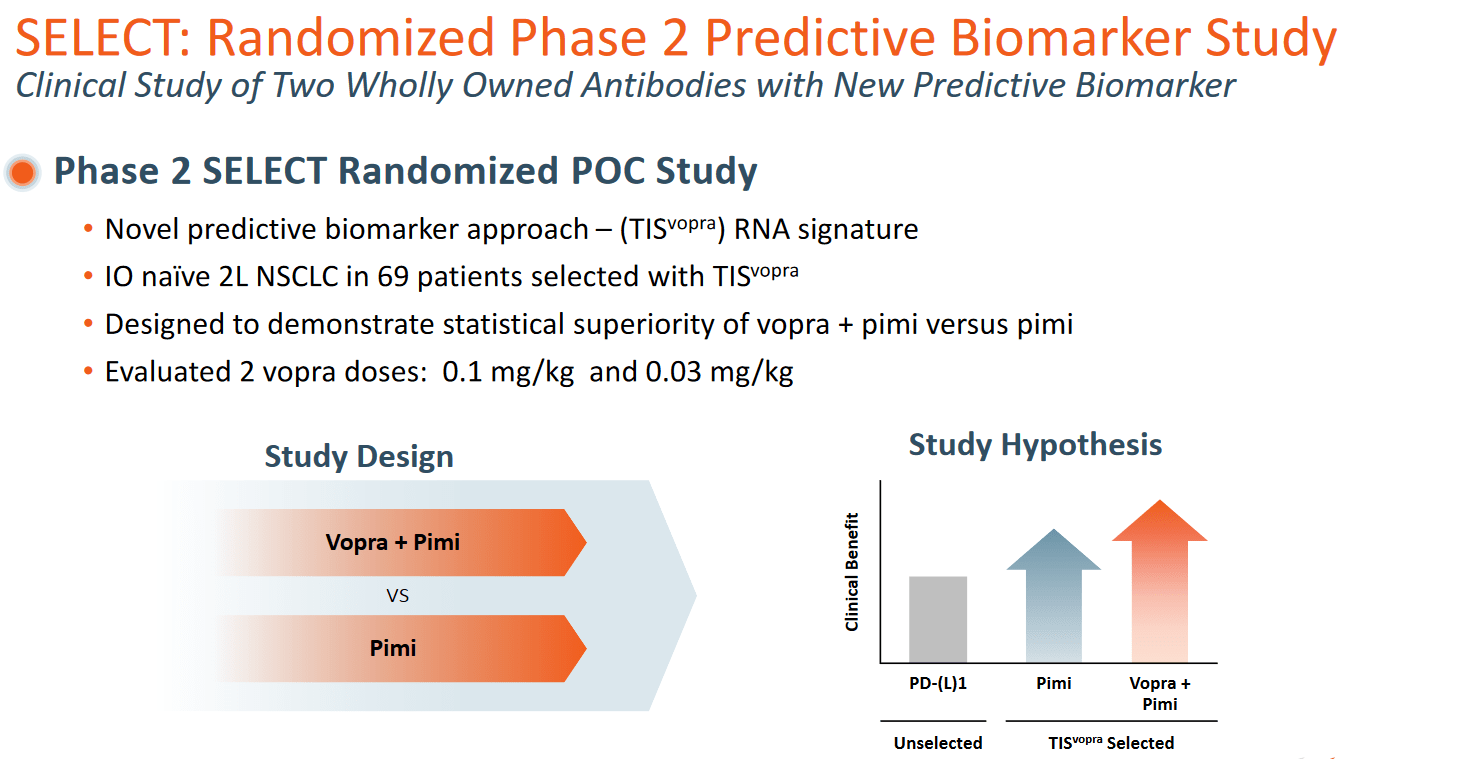

Vopratelimab is an IgG1 agonist antibody targeting the inducible co-stimulatory of T cells or ICOS to activate and proliferate hi CD4 T cells. It is in a Phase 2 trial as a standalone therapy or in combination with pimivalimab in non small cell lung cancer. The estimated study completion date is March 2023, with 75 patients having enrolled.

Vopratelimab study slide (Corporate Presentation)

{kind=link}

The low dose cohort saw a 40% response rate versus 27.8% for pimi alone, and 80% six-month progression-free survival versus 36% for pimivalimab alone.

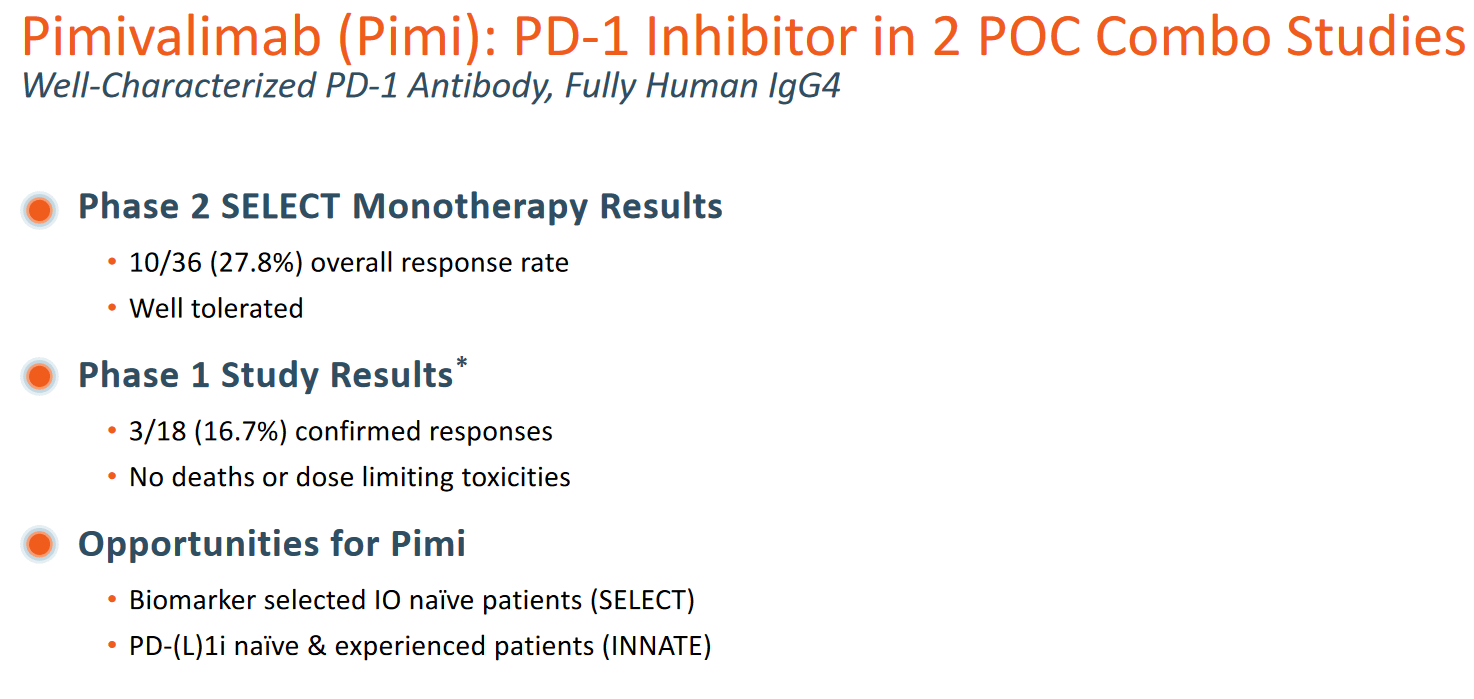

Pimivalimab

Pimivalimab is a PD-1, which is in Phase 2 trials with Vopratelimab in biomarker-selected patients. It is well tolerated, and has shown an overall response rate of 27.8% in monotherapy.

Pimivalimab study slide (Corporate presentation)

{kind=link}

In addition, Jounce has several programs in the discovery and preclinical stage.

My take on these assets

Some of Jounce’s assets are actually quite far along, and particularly its flagship asset looks promising. If any of these assets make it to market, the return on investment can be in the billions of dollars. The current market of immunotherapy candidates is $44 billion and is expected to grow to $74 billion by 2026. In its August 5, 2022 note, HC Wainwright analyst S. Ramakanth expected JTX-8064 to generate risk-adjusted revenues of $59M in 2025, growing to $786M in 2030.

At a market cap of about $50 million, the market is currently giving all of these assets, nor Jounce’s platform for identification of targets and creation of immunotherapy candidates, any value. That is in direct contrast to the deal that had materialized with Gilead in August 2020, and just materialized in another $67 million being paid to Jounce. Jounce intends to keep reaping benefits from that platform, and intends to keep filing IND’s each 12-18 months.

It is almost non-sensical for the market to give all of this a negative enterprise value at all, let alone at levels seen right now. In my eyes, the very bearish climate, with probably a good amount of tax-loss selling, creates a great opportunity here.

Financials

As mentioned above, Jounce had $130.3 million in cash at the end of September 2022, compared to $220.22 million as of December 31, 2022. The recent Gilead deal adds $67 million in cash.

In light of its previous cash burn, I expect this cash injection to bring Jounce’s cash level to $170 million in cash, or more than three times its current market cap.

With operations relating to GS-1811 reduced, I expect this to give Jounce a cash runway lasting mid-2023. Prior to the Gilead deal, the company itself considered its cash to last until 2024.

Risks

Investing in biotech companies entails several risks. Some assets may not deliver the expected results, or may be outperformed by those of competitors. Companies may need to divest certain assets, as they are revising their pipelines. Regulatory authorities may decide to place restrictions on trials, or may place trials on hold.

The current cash position of Jounce seems to be secured for now, but the situation may be different a year from now.

After having gone up more than 85% postmarket, Jounce’s stock ended the trading day 33% up, with 34 million shares exchanged. That is a lot, with 51 million shares outstanding, a float of 24.7 million, with 20% held by insiders and 82% held by institutions. Jounce’s market cap of $50 million gives it a negative enterprise value of about double that amount.

Conclusion

I see Jounce at this time as a very interesting biotech company to invest in. Its market cap is ridiculously low, trading at less than one third of its cash position. With three Phase 2 trials ongoing, the market has decided to give the assets in trials a negative value, as if they were all to fail.

The assets themselves tell a different story; they are, in fact, all promising drug candidates. I am particularly looking at JTX-8064, and the upcoming data in the first half of 2023. There is a multi-billion marketing potential here. JTX-8064 is in an open label study, meaning Jounce may have an idea on the data that it is to present in the coming months.

I believe that the recent Gilead deal, representing another $67 million in value and thereby totaling about $200 million in payments and equity investments for this drug candidate, is a sign of Jounce’s confidence in its own pipeline, upcoming data, and translational drug discovery platform.

Jounce is currently trading at about a $55 million market cap, with about $170 million in cash. Getting this company’s market cap just to cash level would represent more than 200% profits, and I believe the company's Phase 2 assets are worth much more.

I believe all of the above translates into a strong buy rating, which I am giving to Jounce at this stage.

For further details see:

Jounce: Gilead's GS-1811 Buyout Allows A Further Bounce