JPT - JPC: Some Interest Rate Risk But The Opportunity For Yield Is Very Real

2023-09-26 16:54:28 ET

Summary

- The Nuveen Preferred & Income Opportunities Fund offers a high level of income with an 8.37% current yield, exceeding inflation and short-term U.S. Treasuries.

- The JPC closed-end fund's performance has been disappointing, with a decline in share price, but investors still made money through distributions.

- The JPC fund's future performance depends on the interest rate trajectory, which is uncertain, but rates are expected to decline over the long term.

- The fund failed to cover its distribution in the most recent reporting period, but it has cut its distribution since then and it is uncertain how well-covered the distribution is.

- The fund is currently trading at an incredibly attractive discount on net asset value.

The Nuveen Preferred & Income Opportunities Fund ( JPC ) is a closed-end fund, or CEF, that investors can use to earn a high level of income from their portfolios. The fund’s 8.37% current yield stands as testament to this, as this is one of the few assets available in the market that has a yield exceeding both inflation and short-term U.S. Treasuries. As might be expected though, there are some risks involved as the fund’s fixed-income portfolio comes with a great deal of interest rate risk. The market and the Federal Reserve currently expect that it will not be necessary for the central bank to raise rates any further, but JPMorgan’s ( JPM ) CEO Jamie Dimon disagrees and suggests that a 7% federal funds rate is still possible.

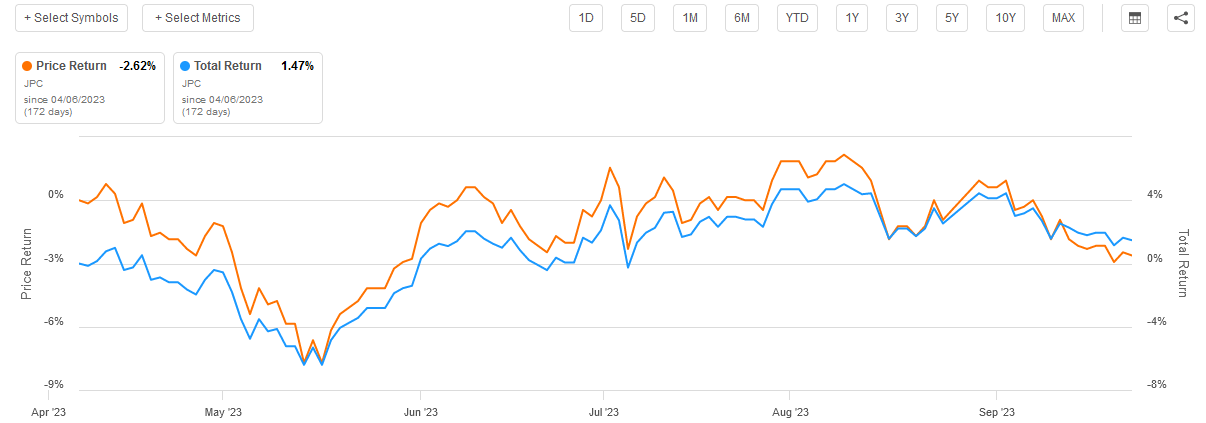

We last discussed the Nuveen Preferred & Income Opportunities Fund back in April. The fund has, unfortunately, delivered a rather disappointing performance since that time as its shares have declined by 2.62%, but investors have still made money when the distribution is considered:

{kind=link}

The fund’s future performance will depend a great deal on the forward trajectory of interest rates, which is an uncertain risk at the moment. However, the long-term trajectory of interest rates will almost certainly be negative due to the fact that most governments in developed nations have high levels of debt and large unfunded obligations that ensure that they cannot carry high interest rates for an extended period. Thus, the fund might still make sense for someone who is looking for a high level of current income today and can hold it for an extended period.

As it has been almost half a year since we last discussed this fund, many things have changed, and we should consider revisiting our thesis to see if it still holds true. This article will focus specifically on these changes as well as provide an updated analysis of the fund’s financial condition.

About The Fund

(There is currently a proposal to combine the Nuveen Preferred and Income Fund (JPT) and the Nuveen Preferred & Income Securities Fund ( JPS ) into this fund. A shareholder vote was conducted to this end in early August but no information has been released since then. This article is written from the perspective of JPC in isolation and does not consider the other two funds due to the lack of any outlook. JPC will be the sole surviving fund if the merger goes through, so the information here should remain valid except that the fund will be considerably larger.)

According to the fund’s website , the Nuveen Preferred & Income Opportunities Fund has the primary objective of providing its investors with a high level of current income. As is typically the case, the website provides a more in-depth description of the fund’s objectives and strategies:

The Fund seeks to provide high current income and secondarily, total return, by investing at least 80% of its managed assets in preferred and other income producing securities, including hybrid securities such as contingent capital securities and up to 20% opportunistically in other securities, primarily income-oriented securities such as corporate and taxable municipal debt and common equity.

The fund’s description above specifically mentions preferred stock as a focus for the fund’s asset deployment, but it does not exclude other types of securities. In fact, the fund is primarily invested in preferred stock, although it does have a sizable allocation to bonds and convertible securities:

CEF Connect

As we can see, 56.64% of the fund’s assets are invested in preferred stock, making it the majority of the fund’s holdings. When we consider this, the fund’s stated focus on the generation of current income makes a great deal of sense. After all, preferred stocks deliver the majority of their investment return to shareholders in the form of direct payments to investors. As I have noted in several previous articles, these securities act much like bonds that have no maturity date. When preferred stocks are first issued, they are assigned a par value, which works much like the face value of a bond. The preferred stock’s price then varies around that face value, depending on how the preferred stock’s yield compares to the current market interest rate. While most preferred stock has no maturity date, it may be callable by the issuing company after a specified date. If the stock is callable, then the issuing company can usually buy it back at the par value. Thus, we can think of the par value much like the face value of a bond.

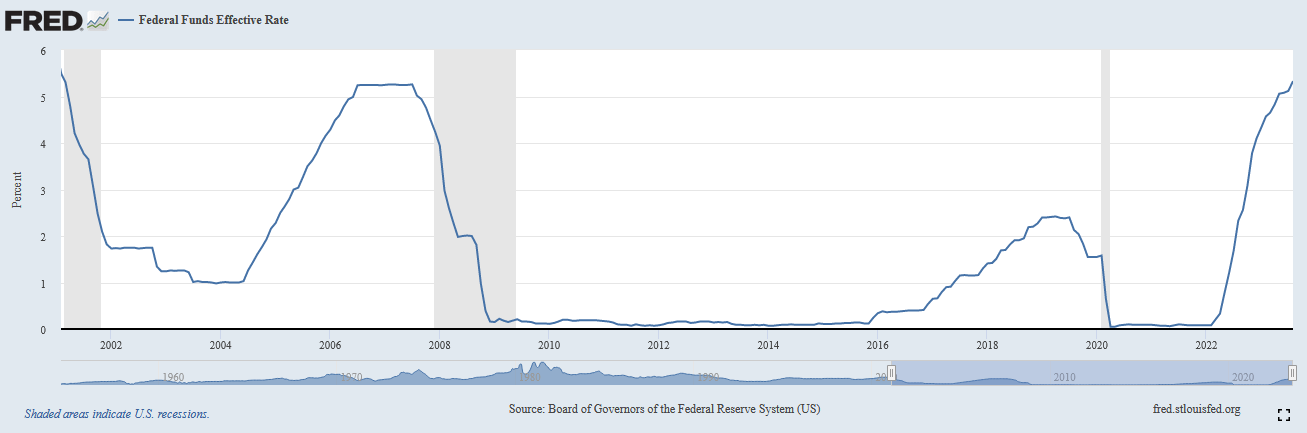

As preferred stock is priced like a bond with no maturity date, it is affected by interest rates in the same way as bonds. In short, there is an inverse relationship between the security prices and the market interest rate. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively hiking interest rates since March 2022 in an attempt to reduce the high inflation rate that is plaguing the economy. As of the time of writing, the effective federal funds rate is 5.33%, which is the highest rate that the United States has experienced since the tail end of the Internet bubble:

Federal Reserve Bank of St. Louis

{kind=link}

Obviously, this rate is quite a bit higher than it was the last time that we discussed this fund. As was mentioned in that previous article, the federal funds rate at that time was 4.65% so the rate today is 68 basis points higher. This is probably the biggest reason why the fund’s share price has declined since that time. After all, the increase in the interest rate caused the price of the securities held by the fund to go down. While the market price of closed-end funds does not always perfectly match the value of the securities in the fund’s portfolio, there is a definite correlation in most cases.

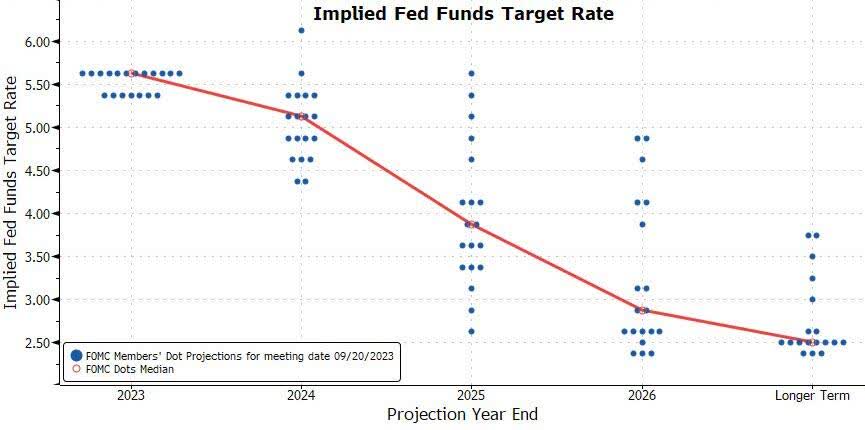

As such, the most important factor for determining the forward trajectory of the fund’s share price is the direction of interest rates. This is a difficult thing to determine as it depends on numerous factors, including inflation, politics, and the ability of the economy to adapt. As of right now, the members of the Federal Open Market Committee currently expect that rates have peaked and will decline over the next few years:

Poll of FOMC Participants With Respect to Interest Rate Risk (Zero Hedge)

{kind=link}

As we can see, the median prediction right now is for rates to drop to 5% next year, 3.5% to 4% in 2025, and around 3% by 2026. However, we can still see some uncertainty here, particularly over the next year or two as outlier member responses showed some predictions that are far above the median. However, this points to the expectation that interest rates will begin to decline next year, although the decline may be much slower than some market bulls and investors expect.

However, as stated in the introduction, the CEO of JPMorgan, the largest bank in the United States, believes that substantially higher rates are not out of the question. A review of the article reveals that his analysis of the situation suggests that stagflation could be a very real possibility, as rising prices for crude oil and other necessary natural resources offset any monetary tightening that results from the Federal Reserve policies. There are some things that support this stagflationary outlook, particularly with respect to energy prices. According to Rystad Energy , global investment into crude oil and natural gas production will only come in at $579 billion this year. That is substantially lower than the $887 billion that was invested into production capacity in 2014. This has been a problem for many years, which has resulted in a global shortfall (supply relative to demand) of around two million barrels per day right now. This is naturally pushing up energy prices due to the economic law of supply and demand and considering that energy is an input into pretty much everything else, it contributes to price increases all across the economy. This could very easily push us into a stagflation situation that resembles the 1970s when an Arabian oil embargo had a similar effect. In such a situation, the Federal Reserve might try to hike interest rates further to slow down the resulting inflation, resulting in the situation suggested by Mr. Dimon.

Obviously, any increase in interest rates would have a negative impact on the market price of the Nuveen Preferred & Income Opportunities Fund. However, in the absence of an increase in interest rates then it seems certain that the worst is behind us. In that case, the fund should be able to provide income as it always has, but capital gains may take a while to appear since the Federal Open Market Committee’s projections are that interest rates will remain at higher levels than most of us are used to for several years.

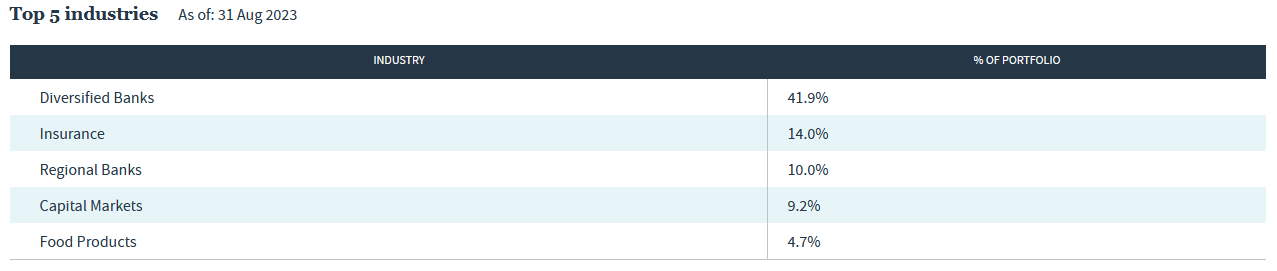

In my previous article on this fund, I noted that the Nuveen Preferred & Income Opportunities Fund is very heavily exposed to the banking sector. This continues to be the case today as 41.9% of the fund is invested in securities issued by banks:

{kind=link}

This is very common for preferred stock funds. As I explained in a previous article on another preferred stock fund:

The banking sector is by far the largest issuer of preferred stock in the market. One reason for this is international banking regulations. As a result of Basel III, banks are required to maintain a certain percentage of their assets in the form of Tier One capital. This is defined as that portion of a bank’s capital that is not simultaneously a liability to somebody else, such as a depositor. This is essentially the bank’s ‘own money.’ Whenever regulations require a bank to increase its Tier One capital, it has to issue either common stock or preferred stock. Most bank managers will opt to issue preferred stock in these situations in order to avoid diluting the common stockholders. In other industries, there are no regulations such as these and so most companies will opt to issue debt instead of preferred stock because debt is quite a bit cheaper to service. Thus, by default, banks are the largest issuers of preferred stock and any preferred stock fund will be heavily invested in the banking sector.

As everyone reading this is no doubt well aware, the banking sector had some serious issues earlier this year as three large regional banks collapsed and another few regional banks came pretty close to collapse. This was caused by rising interest rates reducing the value of the loans (primarily U.S. Treasury securities) held on their balance sheets. As depositors attempted to withdraw their money, these banks were forced to sell these Treasury securities and realize losses. This is a problem that extends far beyond those few regional banks though, as nearly all American depository institutions are currently sitting on enormous amounts of unrealized losses. The Federal Reserve’s Bank Term Funding Program allows banks to pledge their depreciated Treasuries as collateral for loans sufficient to cover all withdrawals against them. As of the time of writing, regional banks have borrowed approximately $108 billion from this facility, and the Federal Reserve has pledged to make more money available if needed as depositors pull money out of banks and put it into higher-yielding assets such as money market funds.

Regardless, though, the central bank seems determined to ensure that there are no more banking system collapses, so we should not need to worry too much about the risks of this fund being exposed to the banking system. In fact, this fund is less heavily exposed to banks than most other preferred stock funds so everything seems okay here.

Leverage

One strategy that the Nuveen Preferred & Income Opportunities Fund employs to boost the effective yield of its portfolio well beyond that of any of the underlying assets is leverage. I explained how this works in my previous article on this fund:

In short, the fund borrows money and uses that borrowed money to purchase preferred stock and other fixed-income assets. As long as the interest rate that the fund has to pay on the borrowings is lower than the yield of the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. For this reason, we want to ensure that the fund does not have too much leverage, since that would expose us to too much risk. I do not usually like to see a fund’s leverage exceed a third as a percentage of its assets for that reason.

As of the time of writing, the Nuveen Preferred & Income Opportunities Fund has leveraged assets comprising 37.79% of its portfolio. This is above our desired one-third level, although it is not as bad as the 40.66% leverage that the fund had the last time that we discussed it. This is a positive sign, as it indicates that the fund may be reducing its debt and the risks that the debt poses to shareholders. Fixed-income assets tend to be somewhat less volatile than common equity, so preferred stock funds can usually sustain a bit higher leverage than common equity funds. As such, this fund’s leverage is probably okay right now, but it does still present risks if interest rates go up further. We should keep an eye on this, but by itself, it is not a reason to avoid the fund.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Nuveen Preferred & Income Opportunities Fund is to provide its investors with a high level of current income. In pursuance of that objective, the fund has assembled a portfolio of preferred stock and other securities that deliver the majority of their investment returns in the form of direct payments to their owners. These securities tend to have yields that are well above the risk-free rate, so we can expect a reasonable yield from them. This fund takes things a step further and applies a layer of leverage to its portfolio in order to boost its yield far above that of any of the assets themselves. The fund then takes the income generated by this strategy and pays it out to the fund’s investors, net of any expenses.

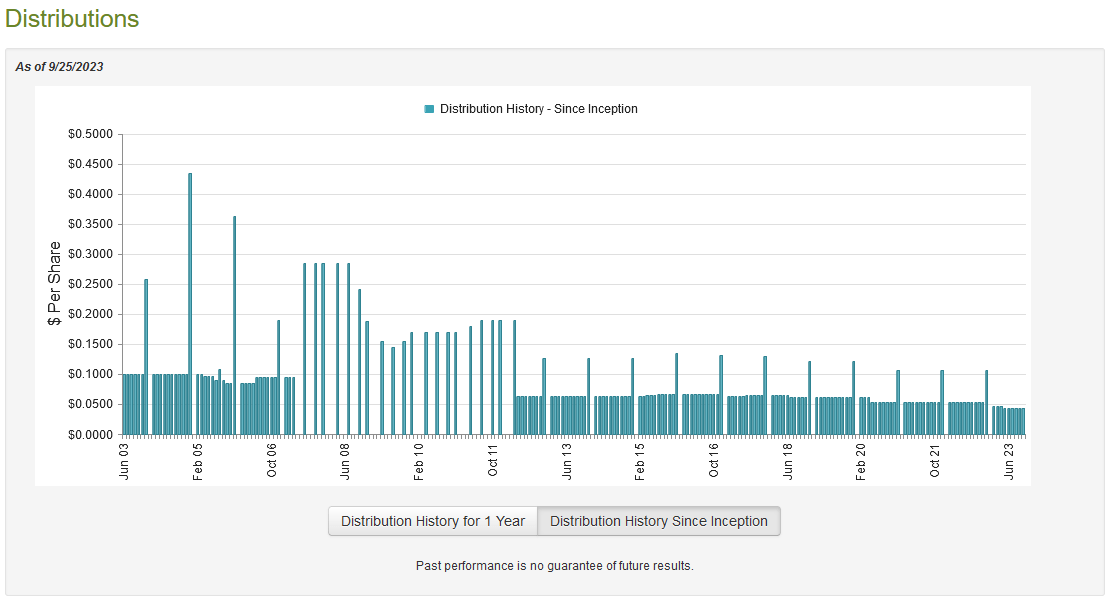

We might expect that this strategy would allow the fund to boast a fairly impressive yield itself. That is certainly the case, as the Nuveen Preferred & Income Opportunities Fund pays a monthly distribution of $0.0440 per share ($0.528 per share annually), which gives it an 8.37% yield at the current share price. Unfortunately, the fund has not been especially consistent with its distribution over the years. In fact, it has both raised and reduced it several times since inception:

{kind=link}

This will probably be something of a turn-off for those investors who are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. The fact that the fund cut its distribution twice in the past twelve months will definitely be a turn-off. However, most fixed-income funds have delivered a similar disappointing performance in recent months as rising interest rates have resulted in most of these funds taking pretty hefty losses.

As I have pointed out before, the fund’s history is not necessarily the most important thing for an investor today. After all, anyone buying the fund today will receive the current distribution at the current yield. This new buyer will not be affected by the actions that the fund has taken in the past. The most important thing for such a person is the fund’s ability to sustain its distribution at the current level. Let us investigate this.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on January 31, 2023. As such, it will not include any information about the fund’s performance over most of this year. That is disappointing since this has been a rather interesting year for fixed-income funds. During the first several months of 2023, the market was incredibly optimistic that a change in monetary policy and a cut in interest rates would be coming, and that it was bidding up the prices of fixed-income securities.

While this belief ultimately proved to be incorrect, there was still a great deal of potential for a fund like this one to make some profits selling securities in such a market. This report will not provide us with any insight into whether or not the fund had any success in doing this. Rather, all it will give us is some insight into how well the fund navigated the extremely challenging conditions of 2022.

During the six-month period, the Nuveen Preferred & Income Opportunities Fund received $8,504,141 in dividends along with $34,526,761 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we arrive at a total investment income of $43,092,005 during the six-month period. The fund paid its expenses out of this amount, which left it with $25,992,201 available for shareholders. This was, unfortunately, nowhere near enough to cover the $32,781,600 that the fund actually paid out in distributions during the period. At first glance, this is likely to be concerning as we would normally like a fixed-income fund to completely pay its distributions out of net investment income.

Fortunately, there are other methods through which the fund can obtain the money that it needs to pay its distributions. For example, it might have been able to take advantage of price fluctuations and sell securities for a profit. The fund had mixed results at this task during the period, as it reported net realized losses of $3,787,714 but these were more than offset by $7,488,743 in net unrealized gains. However, this was not sufficient to cover the difference between the fund’s distributions and its net investment income. Overall, the fund’s net assets declined by $3,088,370 over the six-month period after accounting for all inflows and outflows. This comes on the heels of a $144,652,152 net asset decline during the preceding full-year period.

Thus, the fund’s net assets declined for eighteen months as of the date of this report. That certainly explains why the fund’s managers thought that it was necessary to cut the distribution. Unfortunately, we will have to wait until the fund releases its full-year financial statements in order to determine whether or not the distribution is sustainable at today’s level. We can expect this to occur within the next few weeks.

Valuation

As of September 25, 2023, the Nuveen Preferred & Income Opportunities Fund has a net asset value of $7.39 per share but the shares only trade for $6.27 each. This gives the fund’s shares a 15.16% discount on net asset value at the current price. This is an incredibly large discount that is significantly better than the 11.89% discount that the shares have had on average over the past month. Thus, the price today certainly appears to be reasonable.

Conclusion

In conclusion, the Nuveen Preferred & Income Opportunities Fund is a solid preferred stock closed-end fund for anyone who is seeking to earn a high level of income from their assets. The fund’s attractive 8.37% yield beats most things in the market, and it is one of the few assets that provides a positive real return right now.

Unfortunately, the fund is highly exposed to interest rate risk as assets are currently priced as though the Federal Reserve will not raise rates at all from today’s levels and will instead cut sometime in the first quarter of next year. If that proves to be incorrect, it could drive down the price of the fund’s shares.

Unfortunately, we also do not know for certain how sustainable the distribution is likely to be at the current level, and a more risk-averse investor may want to wait until the fund releases its full-year financial statements before buying in for that reason. However, the price today is incredibly attractive, so we have an opportunity that may not last for very long.

For further details see:

JPC: Some Interest Rate Risk, But The Opportunity For Yield Is Very Real