JPC - JPC: This CEF Might Be Worth Considering Following The Recent Distribution Cuts

2023-04-06 14:23:38 ET

Summary

- High inflation has resulted in investors being desperate for more income in order to maintain their lifestyles.

- Nuveen Preferred & Income Opportunities Fund invests in a leveraged portfolio of preferred stock and bonds in order to provide it with a very high yield to its shareholders.

- The JPC closed-end fund was devastated by the monetary tightening environment over the past year, but it appears that the worst is probably behind us.

- The fund has had to cut its distribution twice in the past year, but it still yields 8.19% and can probably sustain this.

- The JPC fund is currently trading at an attractive valuation and might be worth purchasing today.

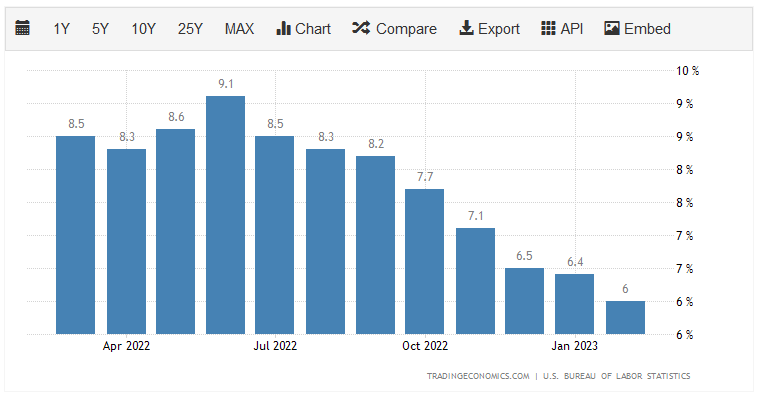

Without a doubt, the biggest problem facing most Americans today is the incredibly high rate of inflation that has dominated the economy for the past eighteen months. There has not been a single month over the past year in which the consumer price index appreciated by less than six percent over the trailing twelve-month period:

{kind=link}

This has pressured the budgets of most consumers, as well as forced many of them to resort to things such as spending down their savings or going into debt simply to maintain their lifestyles. I discussed this in a recent blog post . This has overall had an especially devastating effect on those of lesser means, as inflation has been most prevalent in the necessary areas of food and energy. In some cases, this has caused people to resort to taking on second jobs or entering into the gig economy simply to obtain the extra money that they need to keep their bills paid.

Fortunately, as investors, we can put our money to work for us in order to generate the extra income that we need to maintain our lifestyles in today's environment. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are, admittedly, not particularly well followed in the financial media and even many investment planners are unfamiliar with them. As such, it can be difficult to find information about these assets. That is unfortunate since these funds provide investors with easy access to a diversified portfolio of assets that is capable of employing certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets.

In this article, we will discuss the Nuveen Preferred & Income Opportunities Fund ( JPC ), which is one fund that can be used to earn an income. It is fairly good at this task since the fund yields 8.19% as of the time of writing, which is higher than just about anything else in the market. I have discussed this fund before, but as several months have passed since that time, a few things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund's financial condition since it has released a new financial report since we last discussed it. Therefore, let us continue onward and see if this fund would be a good addition to our portfolios today.

About The Fund

According to the fund's webpage , the Nuveen Preferred & Income Opportunities Fund has the stated objective of providing its investors with a high level of current income. This is hardly surprising considering that the name implies that this is a fixed-income fund. The fund's portfolio confirms it as nearly all of the portfolio is invested in either preferred stock or bonds:

CEF Connect

As the name of the securities implies, fixed-income securities deliver nearly all of their investment returns in the form of direct payments to the investors. This is because these securities have no link to the growth and prosperity of the issuing firm, so we cannot depend on them for capital gains. After all, a company will not increase the interest rate that it pays its creditors just because its profits go up. These securities instead deliver a yield that is dependent upon interest rates in the economy.

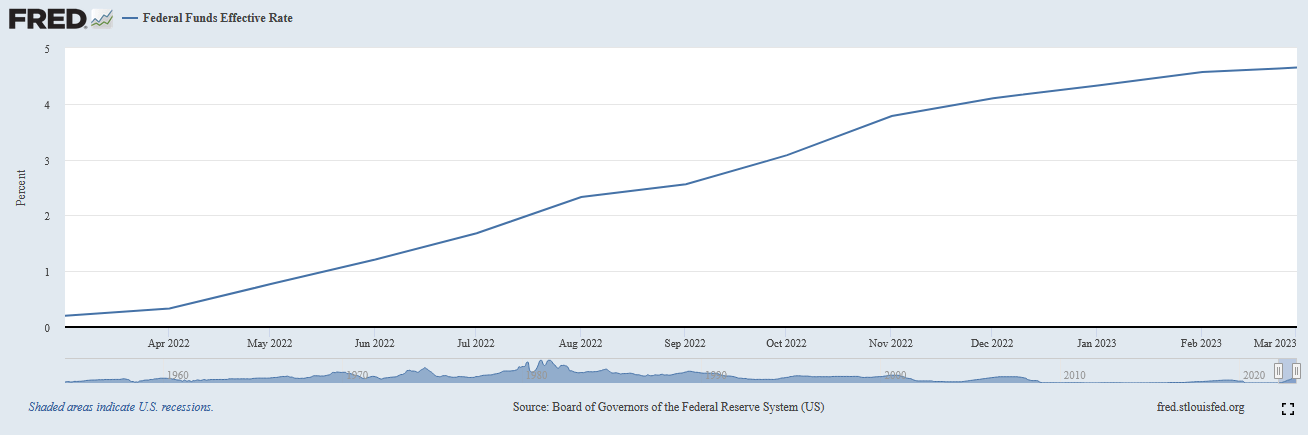

This could be a good thing today. After all, as everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates since March of 2022 in an attempt to combat the high level of inflation in the economy. This is evident by looking at the federal funds rate, which is the interest rate that the nation's commercial banks charge each other for overnight loans. As we can see here, in March 2022, the federal funds rate sat at 0.20% but today the effective federal funds rate is 4.65%:

{kind=link}

This means that the interest rate of newly issued bonds is much higher than it was a year ago. This is necessary since nobody will lend money at less than the federal funds rate. The same thing applies to preferred stock since rising interest rates mean that the dividend yield paid by preferred stock must also increase to maintain the premium over risk-free Treasury securities. Who would buy a preferred stock yielding 4% when a money market fund is yielding 4.50% and is lower risk, after all? Thus, any new security that this fund adds to its portfolio will have a higher yield than it would have received a year ago. This should result in rising income for the fund, all else being equal.

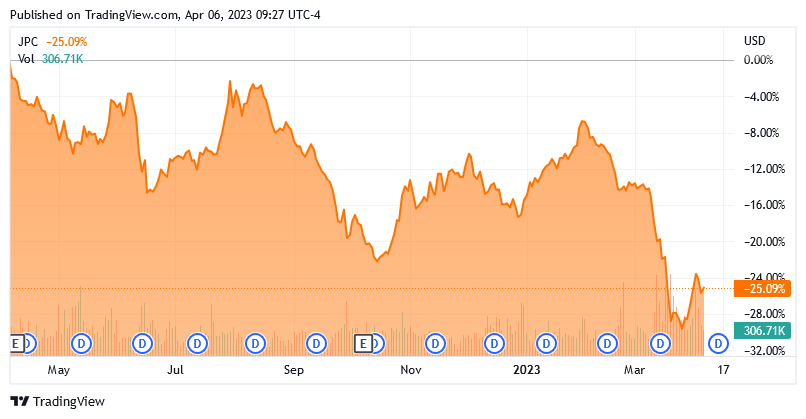

However, all else is not equal in this case. This is because the market price of bonds and preferred stock declines when interest rates increase. That also makes sense because newly-issued securities will have a higher yield than existing ones in such an environment. Thus, nobody will purchase an older bond when a higher yield can be obtained by purchasing a brand-new one with identical characteristics. This hurts the fund because it has to realize a loss by selling an existing security in order to buy a newly issued one with a higher yield. This is the reason why fixed-income funds are hurt by rising interest rates despite the fact that yields increase in that environment. Fortunately, bonds always pay their face value at maturity so by holding a bond for long enough, the fund will not lose money, but it takes a while for that to work itself out. The fact is that funds like this one tend to suffer when interest rates rise rapidly. We can certainly see that in this fund, as the shares of the Nuveen Preferred & Income Opportunities Fund are down 25.09% over the past year:

{kind=link}

Fortunately, the worst is probably behind us. The market and analysts are currently projecting that the Federal Reserve will hike by another quarter-point in May and then pause to evaluate the conditions in the economy. The market is also predicting that the Federal Reserve will cut rates by September, but Chairman Powell has stated that this is not likely to happen. There are a number of signs that the economy will enter a recession in the near future though, so it is possible that the central bank will cut. Regardless, it seems unlikely that we will see the federal funds rate go up significantly from today's level. As such, it seems unlikely that we will see this fund suffer too much more than it already has.

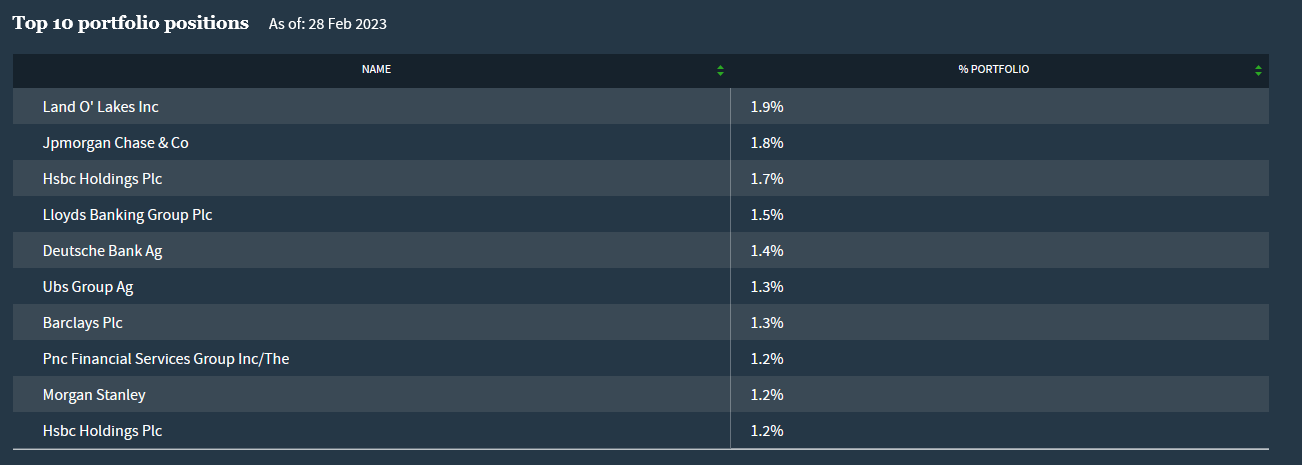

As I mentioned in my previous article on the fund, the Nuveen Preferred & Income Opportunities Fund is heavily exposed to the banking sector. This is still the case, which can be clearly seen by looking at the largest positions in the fund:

{kind=link}

This is something that might be concerning considering that we have seen three major American and one major Swiss bank collapse over the past month. However, as I pointed out in a previous report , the problems that caused Silicon Valley Bank to collapse were largely unique to that bank. The same is true with both Silvergate and Signature Bank. That is not to say that all other banks will be immune to collapse since the inherent problem is that banks used depositors' funds to purchase bonds that have fallen in value due to rising interest rates, but most banks have better risk management programs in place and better diversification of bond maturities across their portfolios. Thus, we probably do not have to worry too much about a wave of bank failures wiping out the fund's portfolio.

The fact that this fund has a great deal of protection against idiosyncratic risk also provides us with a certain level of comfort. As my long-time readers on the topic of closed-end funds are no doubt well aware, I do not like to see any single position in a fund account for more than 5% of the fund's assets. This is because that is approximately the level at which an asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if that asset accounts for too much of the portfolio, then this risk will not be completely eliminated. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not. If that asset accounts for too much of the portfolio, it could end up dragging the entire fund down with it in such a scenario. As we can see above though, there is no individual asset that accounts for such an outsized proportion of the portfolio, so this does not appear to be a risk that we really need to worry about. This fund appears to be well diversified enough that problems at any individual firm should not really affect the entire fund.

Leverage

In the introduction to this article, I stated that closed-end funds like the Nuveen Preferred & Income Opportunities Fund have the ability to use certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase preferred stock and other fixed-income assets. As long as the interest rate that the fund has to pay on the borrowings is lower than the yield of the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we can expect the fund to decline more than its benchmark indices during periods of rising rates. This indeed happened as the fund underperformed both the U.S. Preferred Stock and U.S. Aggregate Bond Indices over the past twelve months. For this reason, we want to ensure that the fund does not have too much leverage, since that would expose us to too much risk. I do not usually like to see a fund's leverage exceed a third as a percentage of its assets for that reason. Unfortunately, as of the time of writing, the Nuveen Preferred & Income Opportunities Fund has leveraged assets comprising 40.66% of its portfolio, so it is significantly above that one-third level. As such, it appears that this fund is exposing us to more risk than we would really like. The fact that this is a fixed-income fund means that its assets are safer than a common stock fund so it can probably carry more leverage, but this is still higher than we really want. As such, the fund may be exposing its investors to too much leverage today.

Distribution Analysis

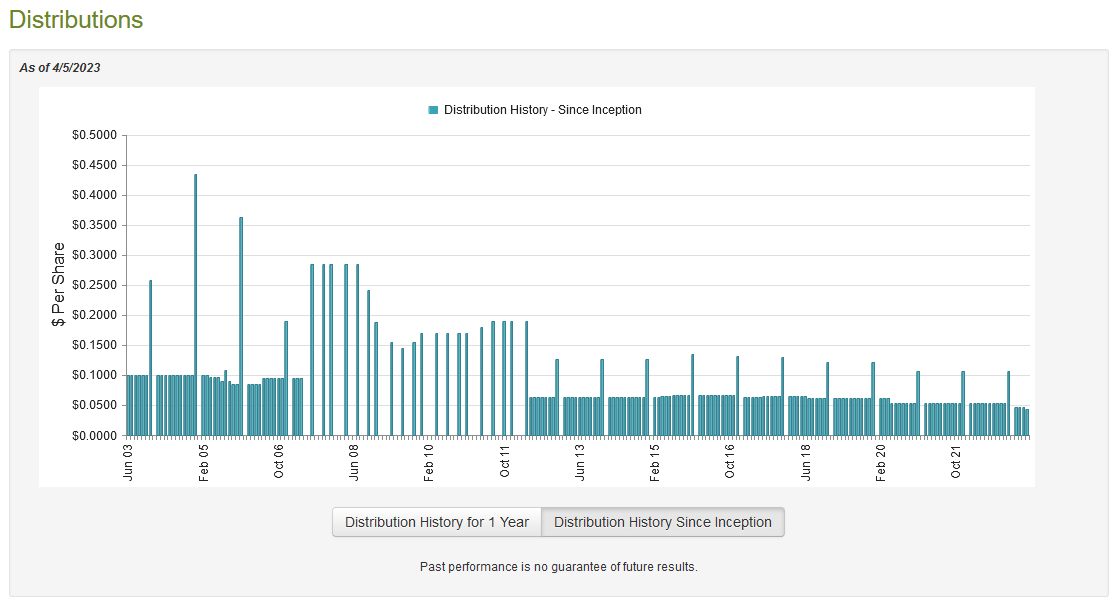

As stated earlier in this article, the primary objective of the Nuveen Preferred & Income Opportunities Fund is to provide its investors with a high level of income. In order to accomplish this goal, the fund invests primarily in preferred stock and bonds that deliver the lion's share of their investment returns through the direct payments that they make to investors. The fund then applies a layer of leverage to boost the overall yield of the portfolio. As such, we can safely assume that this fund will have a respectable yield itself. This is certainly the case as it currently pays out a monthly distribution of $0.0440 per share ($0.528 per share annually), which gives it an 8.19% yield at the current price. The fund has, unfortunately, not been consistent about its payout over its history. In fact, it cut the distribution twice over the past twelve months:

{kind=link}

That history, particularly the recent cuts, will likely reduce the appeal of this fund in the eyes of those investors that are looking for a safe and secure source of income that can be used to pay their bills and finance their lifestyles. However, most fixed-income funds have been forced to cut their distributions over the past years as the rising interest rates have been forcing them to lock in capital losses even as their income increases. As already mentioned though, it seems likely that the worst effects of this are in the past. In addition, anyone buying the fund today will receive the current distribution at the current yield. Thus, the most important thing for a new investor is how well the fund can maintain its current distribution.

Fortunately, we have an incredibly recent report that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on January 31, 2023. This is much newer than the report that we had the last time that we analyzed the fund, and it is more current than the financial reports available for just about any other fund. As such, it should give us a pretty good idea of how the fund weathered the second half of last year and give us a pretty good idea of its current condition. During the six-month period, the Nuveen Preferred & Income Opportunities Fund received $8,504,141 in dividends and $34,526,761 in interest from the assets in its portfolio. When combined with a small amount of income from other sources, the fund had a total income of $43,092,005 during the period. It paid its assets out of this amount, which left it with $25,992,201 available for investors. That was, unfortunately, not enough to cover the $32,781,600 that the fund actually paid out in distributions, but it did get somewhat close. This may explain the distribution cuts though as the fund could be attempting to align its distributions to net investment income as the current environment makes it difficult to depend on capital gains.

Speaking of capital gains, the fund was more successful at achieving them than one might think. The Nuveen Preferred and Income Opportunities Fund had net realized losses of $3,787,714 during the period, but it also had net unrealized capital gains of $7,488,743 over the course of six months. Overall, the fund's assets declined by $3,088,370 during the period after accounting for all inflows and outflows. That is disappointing, but it is a pretty good sign. It seems likely that the fund's recent distribution cuts will allow it to be sustainable for a while, although it is possible that another rate hike will force it to cut again.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Nuveen Preferred & Income Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. A fund's net asset value is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of April 5, 2023 (the most recent date for which data is currently available as of the time of writing), the Nuveen Preferred & Income Opportunities Fund had a net asset value of $7.10 per share but the shares currently trade for $6.45 per share. This gives the fund's shares a 9.15% discount to net asset value at the current price. This is quite a bit better than the 7.71% discount that the shares have traded at on average over the past month. Overall, the price appears right today.

Conclusion

In conclusion, the Nuveen Preferred & Income Opportunities Fund looks like a reasonable way to earn a respectable yield today. Although the fixed-income market has been devastated over the past year, it appears that the worst is likely behind us, and the fund probably will not continue to decline in price going forward. This comes from the fact that the Federal Reserve is widely expected to pause after one more rate hike amid a deteriorating economy. The fund can probably sustain its distribution now that it has cut it a few times and it is trading at an attractive price. Overall, this Nuveen Preferred & Income Opportunities Fund might be worth purchasing today.

For further details see:

JPC: This CEF Might Be Worth Considering Following The Recent Distribution Cuts