JPS - JPS: It May Make Sense To Accumulate A Position In This Affordable CEF

Summary

- Inflation still remains high year-over-year, and people are still in need of extra income to maintain their lifestyles.

- Nuveen Preferred & Income Securities Fund invests in a portfolio of preferred stock and bonds to provide a high level of income.

- The closed-end fund has suffered from a declining market price due to rising rates, which will likely continue for a while.

- The fund can probably maintain its distribution at the current level, although the cut a few months ago is likely discouraging for many.

- The JPS fund is currently trading at a very attractive discount to the net asset value.

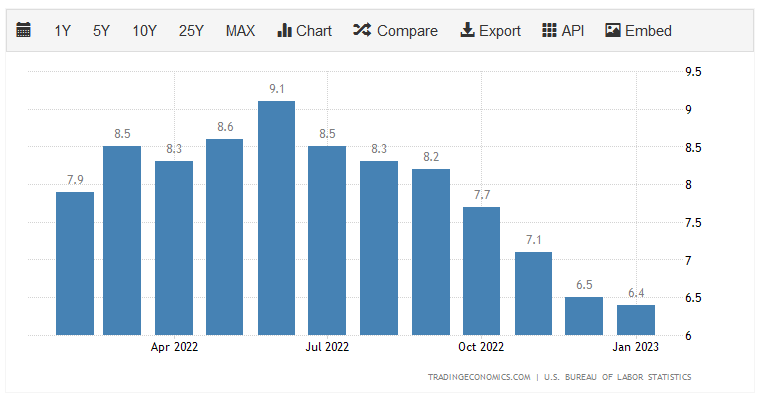

It is unlikely to be a surprise to anyone reading this that one of the biggest challenges facing American households today is the incredibly high rate of inflation that has dominated the economy over the past year. Although the reported rate has come down a bit in the past few months, there has still not been any single month over the past year in which the consumer price index did not increase by at least 6.4% compared to the equivalent month of the prior year:

{kind=link}

This has naturally strained the budgets of many households, particularly those of limited means. As I have pointed out a few times before, a recent Prudential Pulse survey reveals that approximately 81% of Generation Z members and 77% of Millennials have entered the gig economy, or are considering doing so, in order to get the extra money that they need to keep themselves fed and their bills paid.

Fortunately, as investors, we can put our money to work for us in order to obtain the extra money that we need to maintain our standard of living in the current economy. Therefore, we do not necessarily need to take on second jobs to accomplish this task. One of the best ways that we can increase our incomes is by purchasing shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are not the most heavily followed asset class in the market, but they are quite nice because they provide easy access to a diversified portfolio of assets that can in many cases deliver a higher yield than any of the underlying assets possesses.

In this article, we will look at the Nuveen Preferred & Income Securities Fund ( JPS ), which is one closed-end fund that focuses on income. This is evident in the fact that the fund yields 6.80% as of the time of writing. That is not quite as high as some other closed-end funds, but it is still substantially more than the 1.58% yield of the S&P 500 Index (SP500), and it is high enough to generally be useful as a source of income. I have discussed this fund before, but a few months have passed since then, and as such a few things have changed. This article will, therefore, focus specifically on these changes and revisit the fund's finances.

About The Fund

According to the fund's webpage , the Nuveen Preferred & Income Securities Fund has the stated objective of providing its investors with a high level of current income while still ensuring the preservation of capital. This is not a particularly surprising objective for a fixed-income fund. After all, fixed-income investments are generally preferred by those that wish to preserve their capital. For example, a bond will pay out its face value at maturity, assuming the company remains solvent. Although a preferred stock does not usually have a maturity date, these assets do not fluctuate in value nearly as much as common stock or many other assets in the market. The biggest reason for this is that they have no inherent link to the growth and prosperity of the underlying company. After all, a company does not increase the interest rate that it pays its creditors just because its profits go up. Likewise, a company with declining profits still has to pay the same interest to its creditors. As the name implies, Nuveen Preferred & Income Securities is heavily weighted to bonds and preferred stock:

CEF Connect

As we can see, fully 96.25% of the CEF is invested in traditional fixed-income securities like bonds and preferred stock. We also see a very small exposure to convertible securities, which are a hybrid of fixed-income securities and common stock. As already mentioned, these securities do not have a direct link to the growth and prosperity of the issuing companies so we should see a bit more stability here than we would with a common stock fund. However, fixed-income securities do have interest-rate risk. This is because rising interest rates cause fixed-income prices to fall and vice versa. The reason for this is that newly issued securities will have a yield that corresponds to the market interest rate at the time of issuance. As a result, nobody will buy an existing security with a lower yield if they could purchase an otherwise brand-new one with a higher interest rate, which is often the case during periods of rising interest rates. The same thing happens in reverse during periods of declining interest rates. Thus, the price of existing securities must adjust with market interest rates so that they deliver a comparable yield to brand-new securities with identical characteristics.

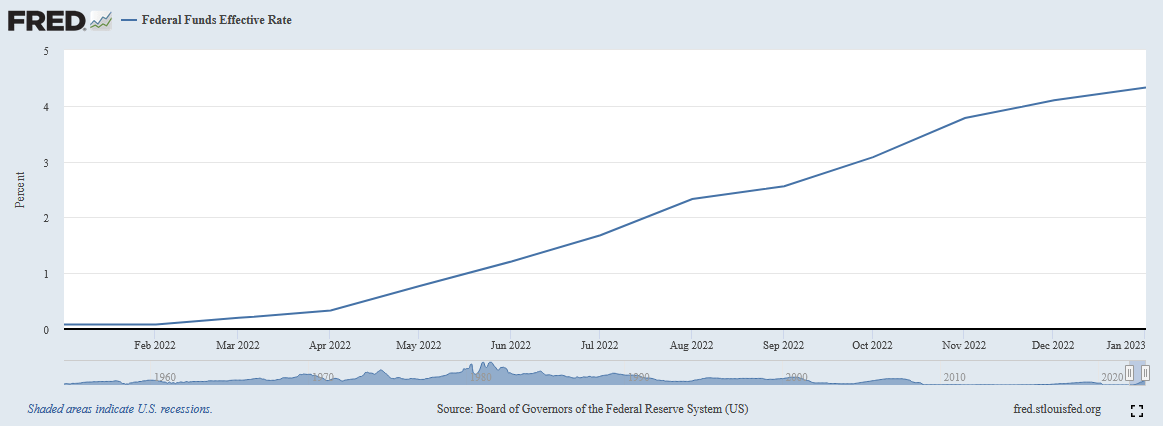

As everyone reading this is no doubt aware, the Federal Reserve has been aggressively raising the federal funds rate over the past year to combat the inflation devastating the economy. Back in February 2022, the effective federal funds rate sat at 0.08% but today it sits at 4.33%:

{kind=link}

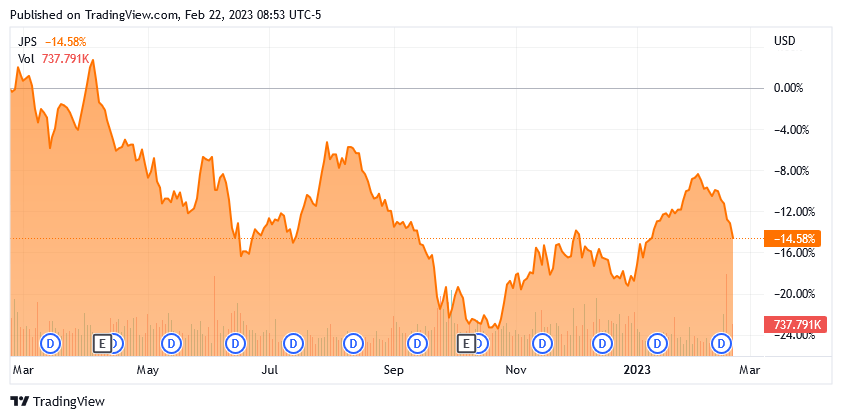

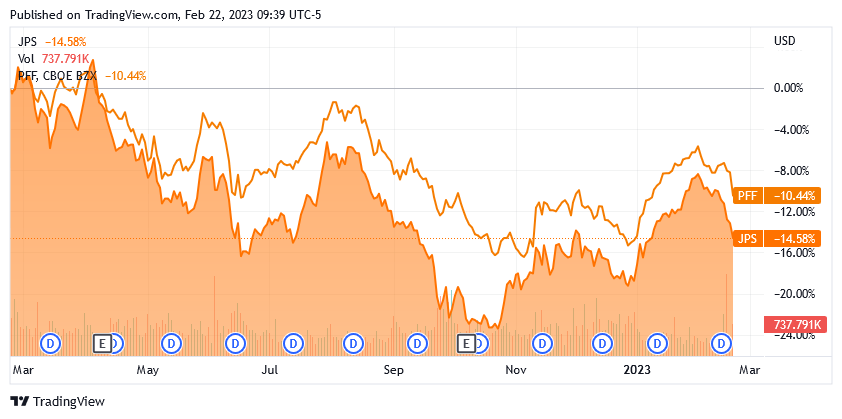

The Federal Reserve has suggested in recent conference calls and other public statements that it will continue to raise the rate over the next several months. That is something that contrasts with the view that was widely held by the market during most of January and early February, but it lines up with the view that I published in a blog post late last year. As fixed-income prices tend to decline when interest rates rise, we can expect this to exert some downward pressure on the fund. That would follow on the heels of a 14.58% price decline that the fund exhibited over the trailing twelve-month period:

{kind=link}

Thus, risk-averse investors may not want to purchase until the Federal Reserve has finished its monetary tightening regime. That is something that is very difficult to predict right now. It is not necessarily a bad idea though to dollar cost average the fund over the next several months as that should help ensure that it proves to be a profitable trade overall, especially when the fund's yield is considered.

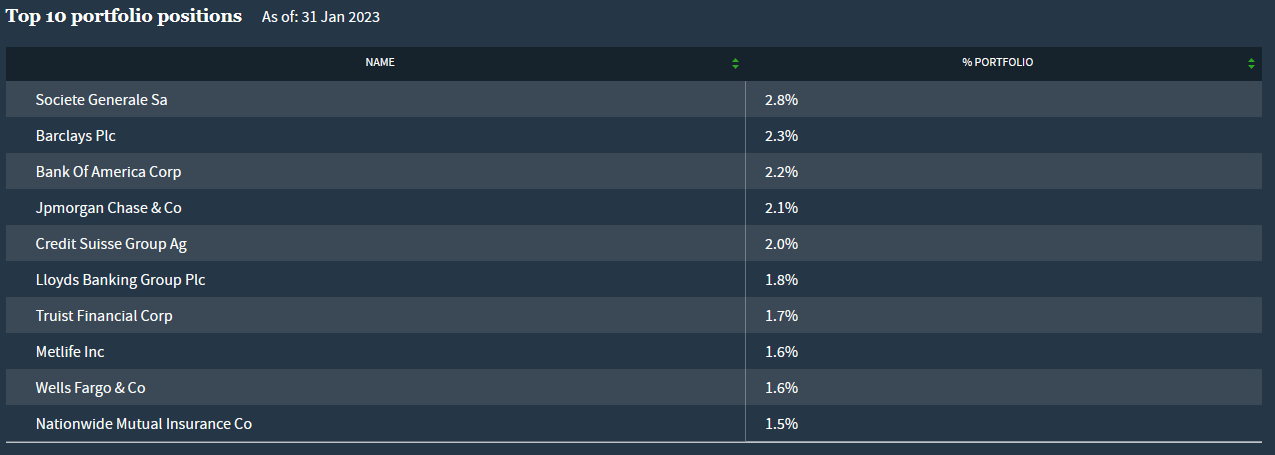

As we noted the last time that we looked at this fund, the Nuveen Preferred & Income Securities Fund contains significant exposure to major financial institutions such as banks and insurance companies. That continues to be the case today as all its largest positions fall into that category:

{kind=link}

This is not exactly unusual for a fund that has such significant exposure to preferred stock. As we have already seen, 43.31% of the fund is currently invested in this security type. The reason why this is not surprising is that the banking sector is by far the largest issuer of preferred stock due to international banking regulations. In short, regulations require that a bank maintain a certain percentage of its assets in the form of Tier one capital. Tier one capital refers to those assets of the bank that are not simultaneously a liability to another party (such as a depositor). When a bank needs to increase its Tier one capital due to regulatory requirements, it must issue either preferred stock or common stock. In many cases, the bank will opt to issue preferred stock to avoid unduly diluting the common stockholders. We do not see a requirement like this in any other industry and since debt is generally cheaper than preferred stock, most companies in other sectors will simply issue debt when they need to raise capital. Therefore, banks are by default the largest issuer of preferred stock and any preferred stock fund will have significant exposure to the banking sector. That is not necessarily a bad thing as banks tend to be very financially resilient regardless of economic circumstances. After all, we have seen cases in the past of national governments ensuring that banks will not collapse or fail to honor their obligations.

There were a number of weighting changes to the fund's largest positions list since the last time that we looked at the fund. This could be easily explained by one asset outperforming another in the market, but admittedly it would be rare for preferred stocks from the same sector to deliver significantly different performance. There are also three new companies on the list. These are JPMorgan Chase ( JPM ), Lloyds Banking Group ( LYG ), and Nationwide Mutual Insurance replacing UBS ( UBS ), BNP Paribas ( BNPQF ), and Charles Schwab ( SCHW ). The fact that there were so many changes in only two months may lead one to believe that this fund has a very high turnover. That is, however, not the case as the fund's annual turnover currently sits at 12.00%, which is not especially high for a fixed-income fund. The reason that this is important is that it costs money to trade stocks or other assets, which is billed directly to the investors. That creates a drag on the portfolio's performance and makes things more difficult for the fund's management. After all, management needs to generate sufficient excess returns to cover these expenses as well as have enough left over to deliver a return that is acceptable to the investors. This is a task that few management teams manage to achieve with any sort of consistency and it is one of the biggest reasons why few actively-managed funds manage to beat a comparable index fund.

This fund is not an exception to this general rule. As we can see here, the ICE Exchange-Listed Preferred & Hybrid Securities Index, represented here by iShares Preferred and Income Securities ETF ( PFF ), outperformed the Nuveen fund over the past twelve months:

{kind=link}

Admittedly, the Nuveen Preferred & Income Securities Fund does have a higher yield than the index, but by itself, this is not enough to close the gap. Overall, an investor in the closed-end fund would have lost more money than an investor in the index over the period.

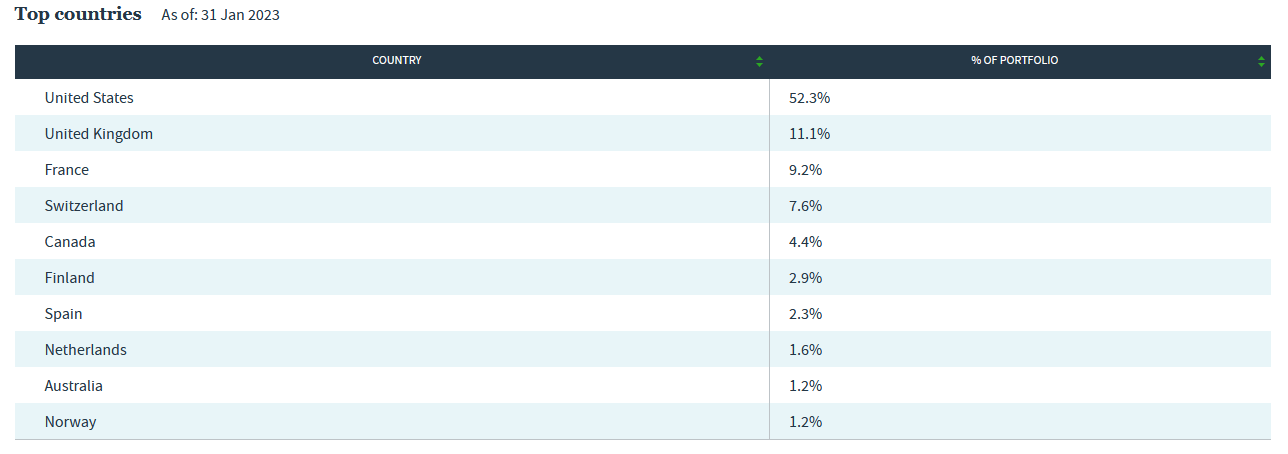

With that said, the Nuveen fund is not a perfect comparison to the index fund. One major difference can be immediately identified by looking at the fund's largest holdings above, as this fund has several foreign issuers listed among its largest positions. In fact, only 52.3% of the fund's assets are in securities issued by American firms:

{kind=link}

This is something that is very different from the index fund as that fund only includes American issuers. It is nice to see foreign issuers represented in the closed-end fund, however. This is because of the protection that it affords us against regime risk. Regime risk is the risk that some government or other authority will take some action that has an adverse impact on a company that we are invested in. The only realistic way to protect ourselves against this risk is to ensure that only a relatively small proportion of our assets are exposed to any individual country. As we can see, this fund is certainly doing that to a great degree but as the United States only accounts for a bit less than a quarter of the global gross domestic product, it is not doing a perfect job of achieving international diversification. As such, we want to ensure that we have international exposure from other sources to ensure that we are not too overly exposed to any individual nation across our entire portfolios.

Leverage

As stated in the introduction, closed-end funds like the Nuveen Preferred & Income Securities Fund have the ability to utilize certain strategies that boost their yields beyond those of any of the underlying assets. One of these strategies is to employ leverage. In short, the fund is borrowing money and using that borrowed money to purchase bonds and preferred stock. As long as the purchased assets have higher yields than the interest rate that the fund has to pay for the borrowed money, the strategy works pretty well to boost the yield of the overall portfolio. As the fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword because leverage increases both gains and losses. This could be another reason why the Nuveen Preferred & Income Securities Fund underperformed the index over the past twelve months. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason. Unfortunately, the fund is a bit above this level as its levered assets comprise 37.87% of the portfolio as of the time of writing. While this is higher than the level that we really want to see, it is probably acceptable because of the generally safe nature of the fixed-income assets that the fund invests in. Investors should still keep an eye on the fund's leverage though to ensure that the level does not get much higher.

Distribution Analysis

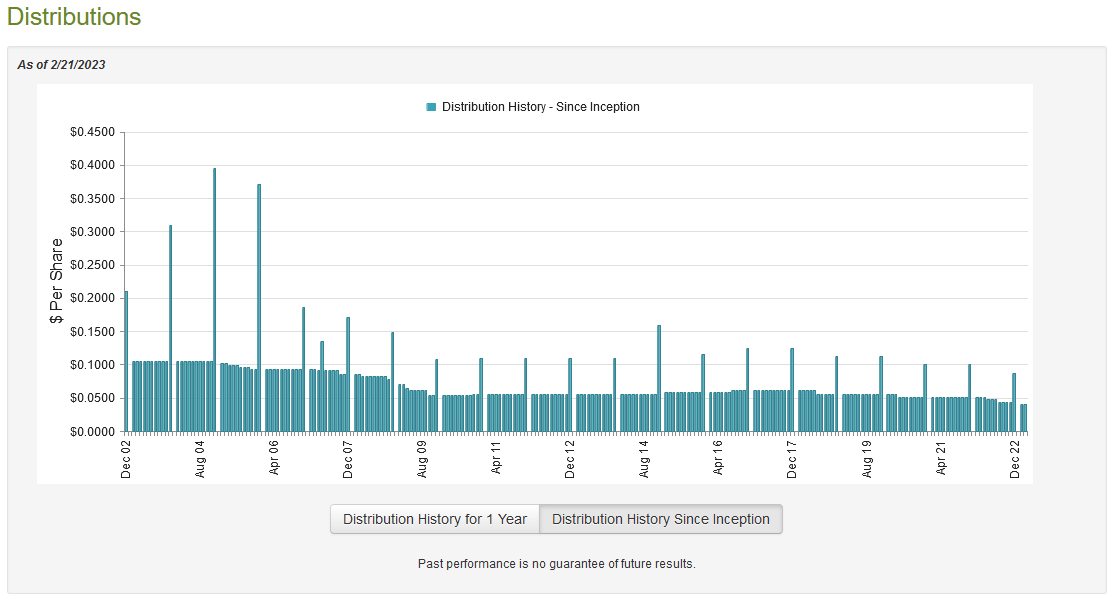

As mentioned earlier in this article, the primary objective of the Nuveen Preferred & Income Securities Fund is to provide its investors with a high level of current income. In order to accomplish this objective, it purchases preferred stock and bonds that deliver most of their investment return via direct payments made to investors. The fund then applies leverage to increase its effective yield. As such, we can assume that the fund likely has a remarkably high yield. This is certainly true as the fund pays a monthly distribution of $0.0405 per share ($0.486 per share annually), which gives it a 6.80% yield at the current price. The fund has unfortunately not been particularly consistent about this payout, as its distribution has varied significantly over the years:

{kind=link}

This is not exactly unexpected as many fixed-income funds tend to vary their distributions with time. This is due to the impact that interest rate changes have on the fortunes of these funds. However, the fact that the distribution has declined over the past year could still reduce the fund's appeal for those investors that are looking for a stable and secure source of income with which to pay their bills and finance other expenses. With that said though, anyone buying today will receive the current distribution at the current yield, so the fund's history is perhaps not the most important thing. We, therefore, want to have a look at its finances to determine how sustainable its distribution is likely to be.

Unfortunately, we do not have a particularly recent report available to us for this purpose. The fund's most recent financial report corresponds to the full-year period that ended on July 31, 2022. As such, it will not include any information about the fund's performance over the past six months. As we did see a distribution cut during this period, this is disappointing as it would have been nice to get some insight into the causes of this. However, the Federal Reserve's monetary tightening began in March 2022, which was the event that had the biggest impact on the fixed-income markets over the past year. We will be able to see the effect that this had on the fund in this report. During the full-year period, the Nuveen Preferred & Income Securities Fund received a total of $21,322,198 in dividends and $136,024,336 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total investment income of $157,602,354 during the period. It paid its expenses out of this amount, leaving it with $118,936,222 available for investors.

Unfortunately, that was not enough to cover the $121,278,321 that the fund actually paid out in distributions. It did get fairly close, however. At first glance, this is something that will likely be concerning for those investors that are looking for sustainability.

There are, however, other methods that the fund can use to obtain the money that it needs to cover its distribution. For example, it could have capital gains that it can pay out. As might be expected from the turbulence in the fixed-income markets that followed the Federal Reserve's rate hikes, the fund generally failed at this task during the period. However, it did achieve net realized gains of $545,509 but this was offset by $338,880,802 net unrealized losses. Overall, the fund saw its assets decline by $331,275,438 after accounting for all inflows and outflows.

This is likely the reason for the distribution cut, as the smaller the fund's asset base, the more difficult it is to generate enough returns to cover the distribution. However, considering how close the fund came to covering the distribution solely out of its net investment income, it can probably afford to maintain its distribution given the savings from the lower distribution. The fund's current payout is probably reasonably safe.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Nuveen Preferred & Income Securities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can buy them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of February 21, 2022 (the most recent date for which data is currently available), the Nuveen Preferred & Income Securities Fund has a net asset value of $8.01 per share but it only trades for $7.17 per share. This gives the fund's shares a 10.49% discount to net asset value at the current price.

This is a much more attractive price than the 7.18% discount that Nuveen Preferred & Income Securities Fund shares have traded at on average over the past month. Thus, the current level looks to be a very attractive price to pay for the fund today.

Conclusion

In conclusion, although inflation has come down somewhat, it is still high enough that most people need more income to maintain their standard of living. The Nuveen Preferred & Income Securities Fund appears to be a good way to get this extra income. Admittedly, the fund's yield is not as high as some other closed-end funds offer, but it is still better than most things in the market, and it is more than high enough to provide a nice boost to anyone's income. The fund does have a great deal of exposure to interest rates, which unfortunately means that its price will drop some more over the coming months as the Federal Reserve seems unlikely to pivot or to stop its tightening in the near term. The current distribution does appear to be sustainable, though, and the valuation is quite attractive. Overall, it may make sense to accumulate a position in Nuveen Preferred & Income Securities Fund over time.

For further details see:

JPS: It May Make Sense To Accumulate A Position In This Affordable CEF