VCLT - JPST: Relatively Safe Above-4% Dividend Yields

2023-03-05 07:12:30 ET

Summary

- Many investors are currently sitting in cash amid the uncertain stock market.

- In these circumstances, JPMorgan Ultra-Short Income ETF (JPST) with its above 4% yield certainly has an appeal.

- To make my point, I make a comparison with another short-term ETF as well as two high-yielding bond funds.

- I also assess the risks, namely if the Federal Reserve starts to ease monetary policy.

- Historically, JPST has also demonstrated better capital preservation ability, which together with the possibility of the Fed remaining hawkish in 2023, signifies a relatively safe above-4% yield.

With the high level of uncertainty prevailing in the stock market, there are many who are left with a lot of cash in their bank accounts and are wondering where to invest. To provide a solution that is in line with income-oriented investing, the objective of this thesis is to show how investors can earn a regular amount of money using the JPMorgan Ultra-Short Income ETF ( JPST ), which has displayed less volatility compared to the broader market.

Thus, as shown in the blue chart below, its one-year performance has been relatively stable despite a return of -0.32% while the S&P 500 has known many ups and downs and returned -7.77%.

I first provide some insights as to the need to invest in a high-yield short-term income-focused ETF taking into consideration the inflation factor, and how high consumer prices not only impact people's daily purchasing power but also their investment, especially if they are invested in fixed income like bonds.

High Inflation affecting Investments

At the start of 2023, inflation began to ease slightly as seen in the chart below. This decline, however, comes after several months of rising consumer prices, with inflation going above 9% in June 2022.

Factors responsible for this are the COVID-19 pandemic which disrupted supply chains, and rising demand which has driven up the cost of many products. For example, upbeat demand coupled with insufficient supply has driven up the price of lumber together with a sharp increase in production costs, including raw materials and wages. These are then often passed on to consumers just like gasoline whose prices depend on the price of crude oil.

In addition, there is also the effect of inflation on people’s investments as the distributions received tend to remain fixed while they pay more for groceries purchased. This implies that high consumer prices also eat away at your savings and investment income on a daily basis in addition to silently eroding your purchasing power.

To address the issue, some investors have opted for the fixed-income asset class, namely bonds, but it is important to understand how these are impacted by high inflation. In this respect, the bonds issued by governments or certain investment-grade companies are high-quality with a low default rate and are among the most widely held debt instruments. These investment-grade bonds must be rated BBB or better and are sought after for the income they generate as well as their lower risk profiles.

However, inflation can hurt bondholders in different ways. First, depending on the prevailing interest rate and the yields perceived, the income deposited to your bank account will allow you to buy fewer goods and services as the inflation rate moves higher. Then, bonds also suffer from rising interest rates as their prices, especially those with longer maturities are particularly vulnerable to higher rates as I will illustrate below.

This is when an ETF like JPST starts to make sense.

The Appeal of JPST

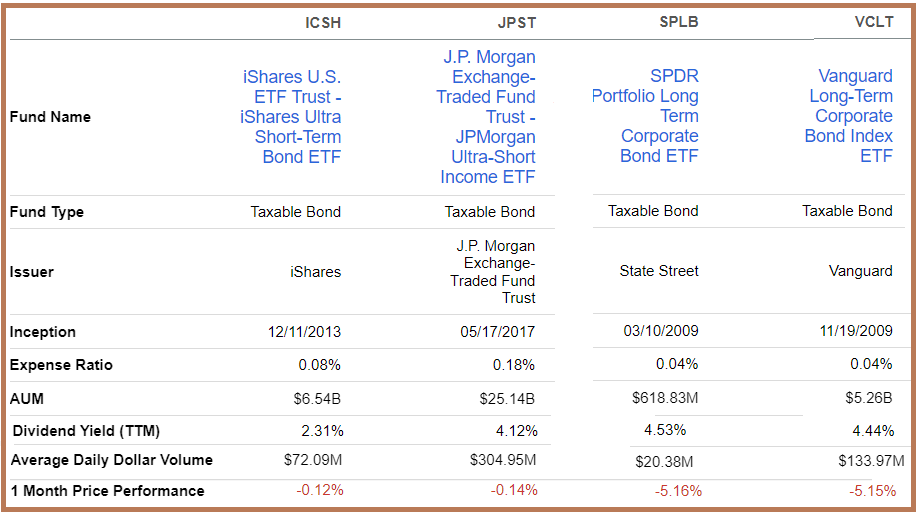

First, it is a very liquid ETF with assets under management or AUM of $25.14 billion and an average daily dollar volume of $306 million which are both on the high sides when compared to the iShares Ultra Short-Term Bond ETF ( ICSH ) for example. These are pictured below.

{kind=link}

Comparison of ICSH and JPST (seekingalpha.com)

Going into more detail, the JPMorgan ( JPM ) fund invests in a diversified portfolio of 585 short-term and investment-grade corporate bonds, with a duration of 0.59 years. These are very short-duration compared to debt instruments which are issued for 2 to 5 years or more.

Another of its difference compared to bonds with fixed interest rates is that it includes both fixed and floating rates. On top, compared with passive ICSH, JPST is more of an actively managed ETF in terms of credit and duration exposure. This is the reason that it charges higher fees of 0.18%.

More important for the sake of this thesis, JPST pays dividends at a higher yield of 4.12%, or a 30-day SEC yield of 4.48% . Now compare this with the 0.35% APY (Annual Percentage Yield) for those holding cash in a regular bank savings account, but, here, the advantage is that you can withdraw your money at any time. You can also get a higher interest rate in a GIC (Guaranteed Investment Certificates) account which is a term deposit account, but your money is locked up for a specified period. The same is the case for an above 4% brokered CD (certificate of deposit) account, on a 1-year, 2-year, or 5-year basis.

Therefore, with its above 4% yield, which is paid on a monthly basis, JPST constitutes an alternative to having your money locked in the bank under some term deposit account.

Exploring further, there are long-duration bonds like the SPDR Portfolio Long Term Corporate Bond ETF ( SPLB ) and the Vanguard Long-Term Corporate Bond Index ETF ( VCLT ) which also pay high dividends of above 4%, but, investors should also pay attention to interest rate risks as I invoked earlier. The adverse impact of rates moving higher is evident when looking at both ETFs' one-month downsides of 5% as per the above table.

JPST's Distributions and Risks

On top, as interest rates are hiked, the monthly distributions made to JPST's shareholders get incremented as shown in the table below. Detailing further, one can notice how the $0.02294 paid in April 2022 surged to $0.15436 in March of this year. This means that on an investment of $10K, monthly payments have increased from $22.9 to $154.3 within one year, which is simply great.

Monthly Dividend distributions (am.jpmorgan.com)

This all happened due to the Federal Reserve increasing rates rapidly in 2022 in their attempt to tame inflation and which translated into higher dividend yields for JPST. Now, after such a surge, one cannot stop wondering what will happen in case the Federal Reserve has to urgently reduce rates in case of a protracted economic slowdown. In this case, the distributions will surely go down.

However, at this juncture, another factor that is important to consider is the capital preservation aspect. For this purpose, one has to look at the price performance. In this case, looking at the longer term, it is found that JPST has delivered three-year and five-year performances of -0.81% and +0.2%, with these periods including Fed fund rates being at extreme levels, or both at near-zero and record highs as shown below.

Consequently, based on historical performance, it can be deduced that in case the Fed were to start the process of monetary easing, distributions would certainly be impacted. However, the degree of impact would certainly be amortized throughout 2023 given that the minutes from the last meeting of the FOMC (Federal Open Market Committee) hint that the Fed should continue to tighten monetary policy in its resolve to tame inflation, implying that interest rates are likely to remain high for the foreseeable future, in turn, keeping up the dividend yield, unless there is a recession.

Conclusion

This is the reason that it is important to have a long-term perspective.

Thus, over the last five years, even with a reduction in distributions as per the dividend history , JPST has delivered total returns of 9.78% as shown in the orange chart below. For investors, total returns are obtained when one opts to reinvest the dividends instead of cashing them out, and this provides an indication of the resilience of the fund to navigate adverse market conditions.

To sum up, this thesis has shown that the solution for income seekers wanting to venture out of cash is to opt for JP Morgan's JPST. Its share price has been oscillating within the $50 to $50.85 range for the last five years except during the Covid crash when it fell to the $49 level, before recouping back losses rapidly. This implies that it provides a high level of capital preservation over the long term which is comparable to what you would obtain from a term deposit, but with the added advantage that it is more liquid. Thus, it makes for a relatively safe investment while delivering above-4% dividend yields in the form of regular monthly income.

Finally, currently available at $50.15 a share, the income ETF could gain another $0.7, which explains my bullish position.

For further details see:

JPST: Relatively Safe Above-4% Dividend Yields