JQC - JQC: Good Historical Performance But Distribution May Be Strained

2023-08-09 16:14:10 ET

Summary

- The high inflation rate in the U.S. has caused real wages and income to decline, putting pressure on people's budgets.

- Investors can mitigate the impact of inflation by investing in closed-end funds that specialize in generating income.

- The Nuveen Credit Strategies Income Fund offers an attractive 11.24% distribution yield and has outperformed comparable indices in recent years.

- The fund currently yields 11.24%, but it is questionable whether or not it can sustain this distribution going forward.

- The fund is currently trading at a very attractive discount to the net asset value.

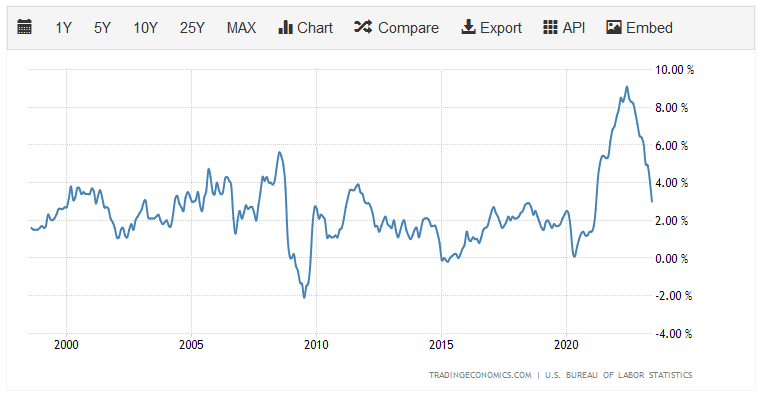

There can be little doubt that one of the biggest problems faced by most Americans today is the incredibly high inflation rate that has been dominating the economy over the past two years. While everyone reading this will undoubtedly be quite familiar with this problem as we have all been experiencing it in our daily lives, it is immediately apparent by looking at the consumer price index. This index claims to measure the price of a basket of goods that is regularly purchased by the average person. This chart shows the year-over-year rate of change in the index for each month over the past 25 years:

{kind=link}

As we can clearly see, the index has been increasing at a much more rapid rate than normal over the past two years or so. This is mostly due to the pandemic, which saw the Federal Reserve and the Federal government increase the money supply by about 40% in two years, a rate that far exceeded the actual economic growth of the economy. Unfortunately for the average person, food and energy prices experienced a significant portion of the price increases so inflation could not be easily avoided by eschewing luxuries. This high rate of inflation has caused real wages and income to decline since the pandemic, pressuring the budgets of many people.

We have even seen a growing number of people resort to desperate measures such as dumpster diving and pawning possessions in order to make ends meet. It is also quite possible that some of the strength that has been seen in recent employment situation reports has been due to people taking on second jobs just to keep their heads above water.

As investors, we are certainly not immune to this. After all, we require food for sustenance and energy to heat our homes just like anyone else. We also might want to enjoy a few luxuries from time to time. All of these things cost more money than they did only two short years ago. Fortunately, we do not need to resort to the same desperate measures as some people in order to maintain our lifestyles. After all, we have the ability to put our money to work for us to earn the extra money that is needed to survive today.

One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in the generation of income. These funds are unfortunately not very well followed by the financial media and many investment advisors are unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have to make an informed investment decision. This is a shame because these funds offer a number of advantages over ordinary open-ended and exchange-traded funds. In particular, a closed-end fund is able to employ certain strategies that allow it to deliver a higher yield than any of the underlying assets or just about anything else in the market.

In this article, we will discuss the Nuveen Credit Strategies Income Fund ( JQC ), which is one fund that can be used by investors seeking income. The fund’s very attractive 11.24% distribution yield is certainly a testament to this as it is certain to grab the attention of any yield-seeking investor. I have discussed this fund before, but a few months have passed since that time, so naturally a few things have changed. This article will, therefore, focus specifically on these changes as well as provide an updated analysis of the fund’s financial condition.

About The Fund

According to the fund’s webpage , the Nuveen Credit Strategies Income Fund has the objective of providing its investors with a high level of current income. This is not especially surprising considering that the name of the fund implies that it will be investing primarily in debt securities. CEF Connect confirms this, stating that 96.66% of the fund’s assets are invested in bonds:

CEF Connect

It makes a great deal of sense for a bond fund to be focused on the generation of current income. After all, bonds by their very nature deliver all of their investment returns directly through payments made to the investor. An investor purchases a bond at face value, receives a stream of coupon payments over the life of the bond, then receives the face value back when the bond is redeemed at maturity. Over the life of the bond, the only net investment returns are the coupon payments made to the bondholder. There are no net capital gains because the bond has no inherent link to the growth and prosperity of the issuing entity.

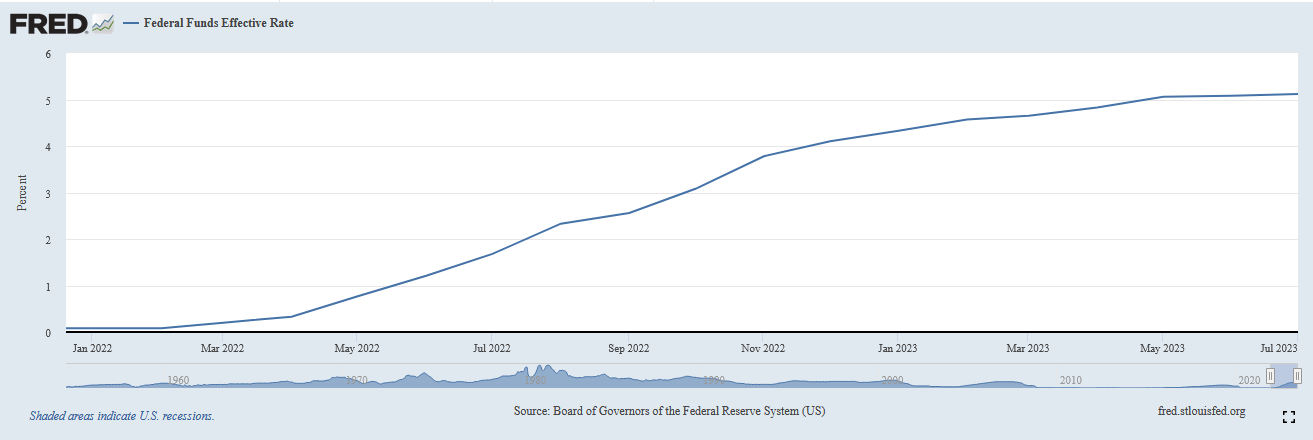

At this point, some readers may point out that capital gains are possible to obtain with bonds. That is true, but only if one trades them prior to maturity. This is because a bond’s price typically varies with interest rates. It is an inverse correlation, so when interest rates rise, bond prices decrease. The reverse is also true. As everyone reading this is certainly well aware, the Federal Reserve has been aggressively raising interest rates over the past fifteen months or so in an effort to combat the multi-decade high inflation rate plaguing the American economy. As we can see here, the effective federal funds rate has gone from 0.08% in January 2022 to 5.08% today:

{kind=link}

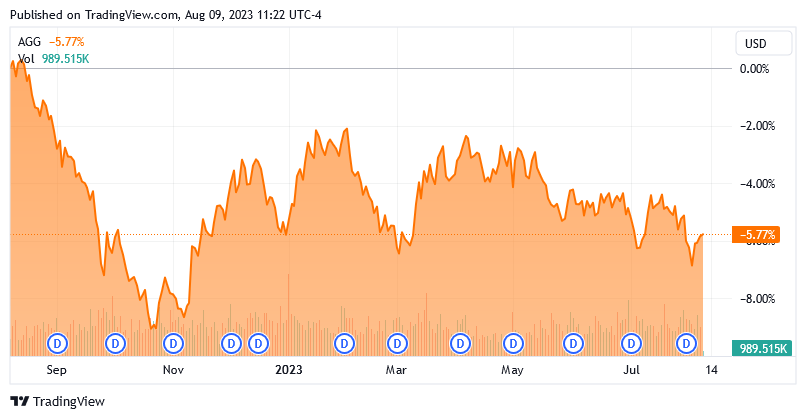

That is one of the most rapid interest rate increases in the history of the Federal Reserve. We have seen similar rate increases all around the world, although not all of them have been so aggressive. As of right now though, Japan and China are the only two countries in the G20 that have not raised interest rates, and some market observers think that the Bank of Japan is on the verge of doing so. This caused a great deal of carnage in the bond markets over the past year. As of the time of writing, the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 5.77% over the past twelve months:

{kind=link}

This is due to the fact that the coupon yields on bonds correlate to the market interest rate at the time of issuance. Thus, a bond that is issued today will pay someone that buys the bond at face value a much higher coupon rate than a person that bought a similar bond last year. As such, there is no reason for someone to purchase an existing bond today when they could purchase a brand-new one with a much higher yield. As such, the price of the existing bond needs to decline so that it offers a comparable yield-to-maturity as a brand-new bond with identical characteristics.

This process of bond prices varying with interest rates has no real effect on someone that purchases the bond directly. In fact, a bond investor that purchases a bond at issuance with the intent of holding it to maturity is guaranteed not to lose money as long as the issuer does not default. A bond fund may or may not hold a bond for its entire lifetime, but unfortunately, the market price of its shares will bounce around based on the value of the bonds in the portfolio. As such, the decline in bond prices had a negative impact on the share price of the Nuveen Credit Strategies Income Fund over the past year. As we can see here, this fund’s share price is down 9.61% over the past twelve months:

{kind=link}

At first glance, that is definitely worse than the broad-market bond index that was just mentioned. However, it is important to keep in mind that the Nuveen Credit Strategies Income Fund has a much higher yield. This allowed it to deliver a better total return than the Bloomberg U.S. Aggregate Bond Index over the period in question:

{kind=link}

One of the unusual characteristics of closed-end funds is that their share prices do not always reflect the performance of the underlying portfolio. This fund is no exception to this rule. As we can see here, the fund’s portfolio outperformed its share price year-to-date and over the trailing one-year period, but the performance difference balances out somewhat over longer periods:

{kind=link}

In this case, the fund’s net asset value total return reflects what the portfolio actually delivered. As we can clearly see, the portfolio has generally been outperforming the fund’s market price in recent months. This is especially apparent when we look at the fund’s trailing six-month return, which saw the share price decline even though the fund’s portfolio actually delivered a positive total return. This scenario could present us with the opportunity to essentially acquire the fund’s assets for less than they are actually worth. We will discuss that in more detail near the end of this article.

It may not be a perfect comparison to benchmark the Nuveen Credit Strategies Fund against the broad-market bond index. The fund’s webpage suggests that it can include things that are not included in the index:

“Under normal circumstances, the fund will invest at least 80% of its assets at the time of purchase in loans or securities that are senior to its common equity in the issuing company’s capital structure, including but not limited to debt securities and preferred securities. The fund invests at least 70% of its managed assets in adjustable rate senior secured and second lien loans, and up to 30% opportunistically in other types of securities across a company’s capital structure, primarily income-oriented securities such as high yield debt, convertible securities, and other forms of corporate debt.”

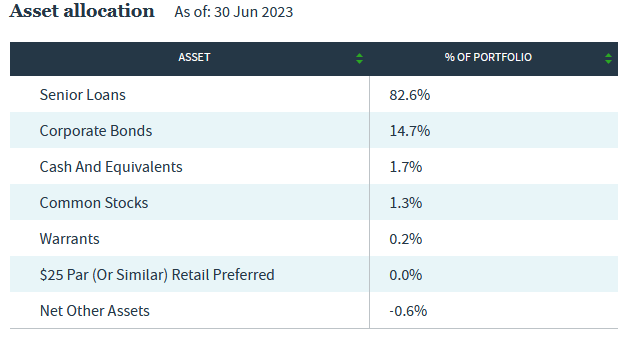

That description strongly implies that the fund is investing primarily in floating-rate leveraged loans, much like the Eaton Vance Floating-Rate Income Trust ( EFT ), which we discussed earlier this week. This does appear to be true, as 82.6% of the fund’s portfolio is currently invested in these securities:

{kind=link}

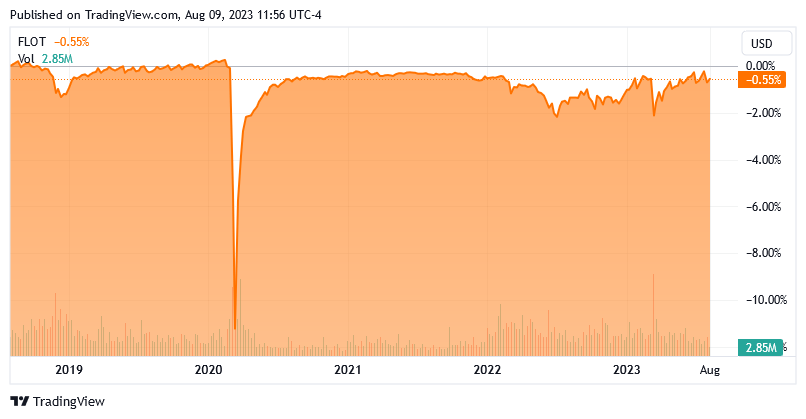

These securities should perform much better than traditional bonds in a rising-rate environment. This is because they do not have the problem of newly issued securities having a higher coupon rate than existing securities. Indeed, the fact that the interest rate paid by these securities changes based on the interest rate in the market should ensure that they always deliver a competitive yield with brand-new debt securities that have identical characteristics. Thus, the price of these securities should be relatively flat over time. That is certainly the case with the iShares Floating Rate Bond ETF ( FLOT ), which claims to track the Bloomberg U.S. Floating Rate Note Index. This chart shows the index fund’s price over the past five years:

{kind=link}

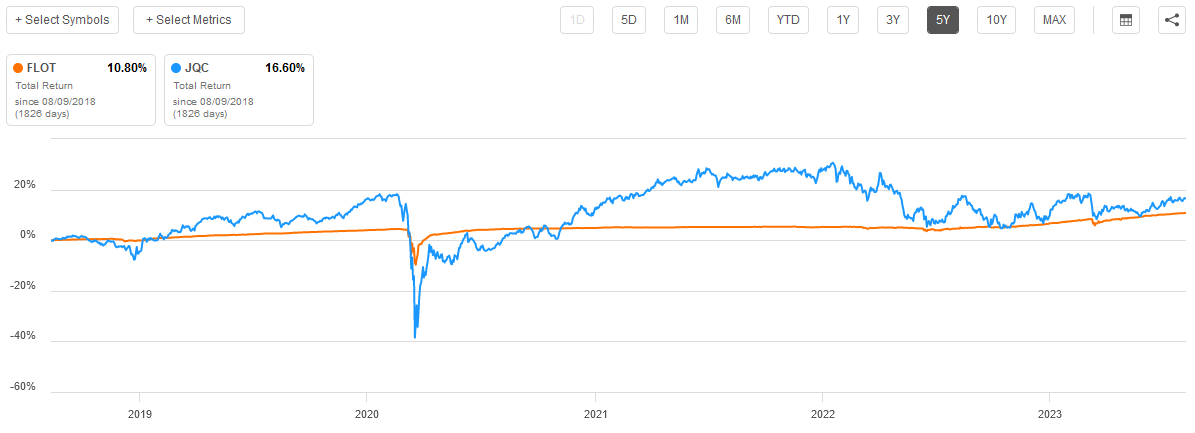

As we can see, the index has been almost perfectly flat, excluding a very short period of time right around the outbreak of the COVID-19 pandemic. That implies that it should be exceedingly difficult to generate any sort of capital gains by trading these securities. As we have already seen, the Nuveen Credit Strategies Income Fund has most certainly not been flat over time. It has still managed to outperform the floating rate index over the five-year period, though:

{kind=link}

This is almost certainly due to the flexibility that the Nuveen fund has compared to the indices. As the fund’s description states, it can invest anywhere from 70% to 100% of its assets into floating-rate securities. That still gives it the potential to invest up to 30% of its assets in fixed-rate securities. This can give it advantages in both rising and falling rate environments. For example, fixed-rate securities will go up when interest rates go down, but floating-rate securities will not. The fund could thus profit by putting assets into fixed-rate securities and trading them. In a rising-rate environment, it would make more sense to put all of its assets into floating-rate securities to prevent losses. This has apparently allowed this fund to outperform both comparable indices over time. While past performance is no guarantee of future results, there are certainly some reasons to expect that this fund will do somewhat better than the indices going forward.

Leverage

In the introduction to this article, I stated that closed-end funds such as the Nuveen Credit Strategies Income Fund have the ability to employ certain strategies that have the effect of boosting the effective yield of the portfolio beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund is borrowing money and using those borrowed funds to purchase debt securities. As long as the yield of the purchased securities is higher than the interest rate that the fund has to pay on the borrowed money then the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, it is important to keep in mind that this strategy is much less effective today with borrowing rates at 6% than it was eighteen months ago when borrowing rates were at 0%. This is because the difference between the borrowing rate and the yield of the purchased securities is going to be much less than it used to be.

Unfortunately, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt because that would expose us to too much risk. I do not generally like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. This fund’s levered assets comprise 38.48% of its total assets currently, so it is, unfortunately, a bit above that level. However, in this case, it may be okay. As already mentioned, the majority of the fund’s assets should prove relatively stable in price over time. Those assets that are more variable in price are still far less volatile than common stocks. The risk from the fund’s leverage should not be too bad here, but we do still want to ensure that its leverage does not go much higher and expose us to more risk than we want.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Nuveen Credit Strategies Income Fund is to provide its investors with a high level of current income. In order to achieve that objective, the fund purchases various debt securities that deliver their investment returns primarily through direct payments made to the investors. The fund then applies a layer of leverage to boost the effective yield of the portfolio. It passes the payments that it receives through to its shareholders, so we can assume that the fund would have a very high distribution yield itself.

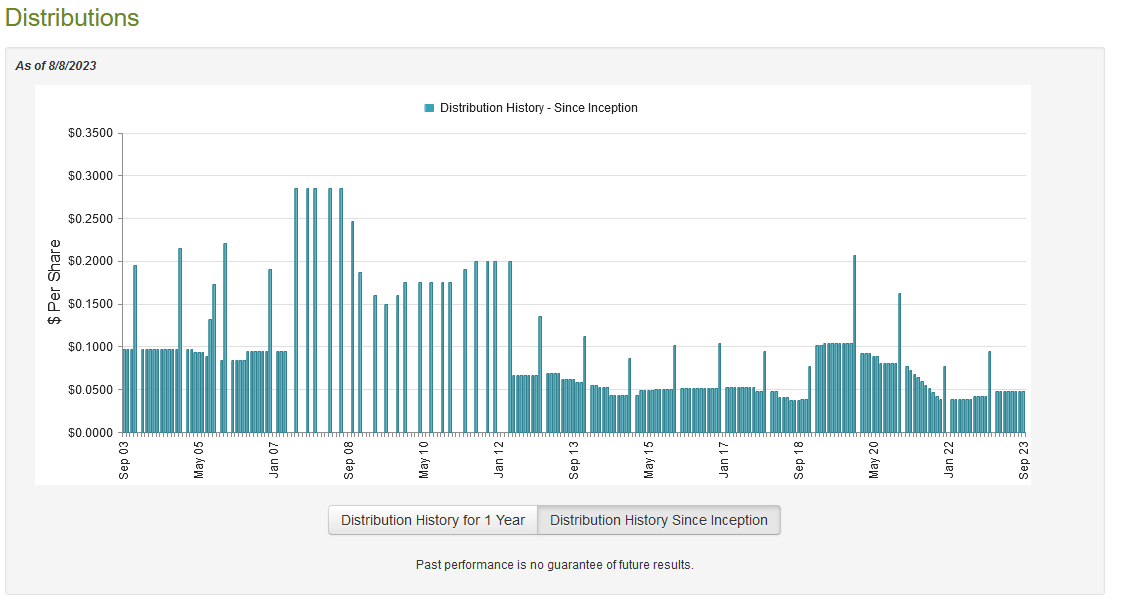

This is certainly the case, as the fund pays a monthly distribution of $0.0475 per share ($0.57 per share annually), which gives the fund an 11.24% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over the years:

{kind=link}

This distribution history will almost certainly prove to be a turn-off for those investors that are seeking a safe and secure source of income to use to pay their bills and finance their lifestyles. That is certainly a problem since these are the investors that are going to be most interested in an income-focused fund like this one. However, it is not atypical for a debt fund to vary its distributions over time since the returns of these funds are significantly affected by interest rates that tend to fluctuate based on the supply and demand for money and Federal Reserve policy.

As I have pointed out before, the fund’s history is not necessarily the most important thing for anyone that is considering buying the fund today. This is because a new purchaser will receive the current distribution at the current yield and will not be negatively impacted by the fund’s past. Thus, the most important thing today is determining the fund’s ability to sustain its distribution at the current level. Let us investigate this.

Unfortunately, we do not have a particularly recent document to consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on January 31, 2023. As such, it will not include any information about the fund’s performance over the past six months. This is disappointing as the market has overall been much stronger year-to-date than it was in 2022 so the fund has probably had the opportunity to get capital gains since this report was published.

However, this report will still give us a good idea of how well the fund performed over much of 2022, and a fund’s performance during a challenging market can offer good insights into its quality. After all, anyone can make money during a bull market, but it is much more difficult to be profitable in a bear market.

During the six-month period, the Nuveen Credit Strategies Income Fund received $51,014,824 and $950,167 in various fees from the assets in its portfolio. This gives the fund a total investment income of $51,964,991 during the six-month period. It paid its expenses out of this amount, which left it with $34,401,848 available for shareholders. That was unfortunately not enough to cover the $36,411,094 that the fund paid out in distributions, although it did get pretty close. It is still somewhat concerning to see this though, as we typically like debt funds to be able to completely finance their distributions out of net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distributions that it pays out. For example, it might be able to exploit changes in bond prices and generate some capital gains. The fund was generally unsuccessful at that, as might be expected. It reported net realized losses of $42,903,161 but this was partially offset by $24,061,293 in net unrealized gains. Overall, the fund’s net assets declined by $20,851,114 after accounting for all inflows and outflows during the period. This is certainly concerning as the fund failed to cover its distribution during this six-month period. It also failed during the previous year, as its net assets were down $110,681,250 during the full-year period that ended on July 31, 2023. As such, we will want to keep a very close eye on the fund’s annual report which will probably be released in the next few weeks. If it does not manage to stem the tide of losses, it may be forced to cut its distribution.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund, the usual way to value it is by looking at the net asset value. The net asset value of a fund is the total current value of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund’s assets for less than they are actually worth. I mentioned this possibility earlier in this article. This is, fortunately, the case with this fund today.

As of August 8, 2023 (the most recent date for which data is available as of the time of writing), the Nuveen Credit Strategies Income Fund had a net asset value of $5.82 per share but the shares currently trade for $5.08 each. This gives the fund’s shares a discount of 12.71% on the net asset value. This is a very substantial premium that is relatively in line with the 12.86% premium that the shares have had on average over the past month. Thus, the price certainly looks right today.

Conclusion

In conclusion, investors today are desperate for additional sources of income to maintain their lifestyles in today’s inflationary environment. The Nuveen Credit Strategies Income Fund is one way that this income can be obtained, as the fund’s 11.24% is certainly sufficient to provide anyone with a very high level of income.

The fund has performed quite well relative to the broad market indices in recent years, which is almost certainly due to its flexible strategy. The biggest problem here is that the Nuveen Credit Strategies Income Fund distribution could be at risk of a cut unless the fund manages to achieve improved financial performance in the first half of this year. That is possible, but still uncertain at this time. We will obviously know more when its annual report is released so potential investors are advised to keep an eye out for that release.

For further details see:

JQC: Good Historical Performance, But Distribution May Be Strained