JRI - JRI: Real Assets Belong In Your Portfolio But This Distribution Looks Strained

2023-11-21 11:01:35 ET

Summary

- The Nuveen Real Asset Income and Growth Fund specializes in investing in real assets such as real estate, infrastructure, and energy distribution systems.

- Short-term performance of real estate assets has been adversely affected by high mortgage costs and reduced demand for office space.

- Despite short-term fluctuations, real assets provide long-term protection against inflation, and the fund offers a high yield of 9.68%.

- The fund's net asset value continues to decline, which causes some concern over the sustainability of its distribution.

- The fund is trading at a reasonably attractive discount on net asset value right now.

The Nuveen Real Asset Income and Growth Fund (JRI) is a closed-end fund, or CEF, that specializes in providing its shareholders with a very high level of income by investing in real assets, such as real estate, infrastructure, and energy distribution systems. Some of these assets have not performed well in today's high-interest-rate environment. This is particularly true for real estate, as the current cost of mortgages has reduced the demand for buyers to purchase real estate, and the trend to remote work has reduced the demand for office space in many cities.

However, over the long term, real assets do a better job at protecting your wealth from the ravages of inflation than paper securities, due to the fact that they are in limited quantities and require real human or mechanical labor to construct and improve. As such, everybody should have some exposure to assets such as the ones contained in this fund. The fact that this fund boasts a 9.68% yield at the current price also helps a lot as that yield is sufficiently high for investors to not have to panic over short-term market fluctuations.

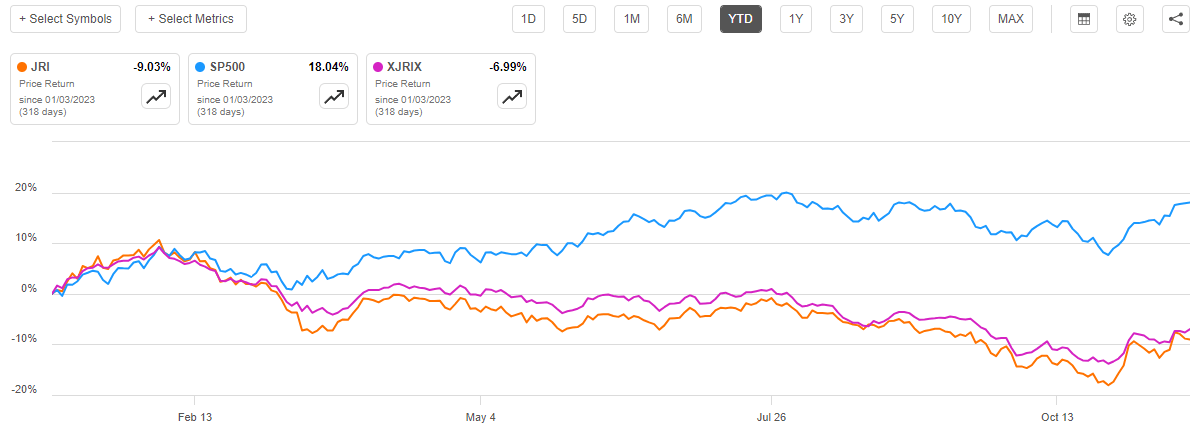

As regular readers may recall, we have discussed this fund in the past, but it has been quite a while. My previous article on the Nuveen Real Asset Income and Growth Fund was published on December 28, 2022. In that article, I was concerned about the fund's declining net asset value as it appeared that it was overdistributing and destroying its asset base. Unfortunately, that has continued to be the case this year as the fund's net asset value is down 6.99% since the start of January. This is better than the fund's share price performance though, as the fund's shares are down 9.03% year-to-date. The fund's net asset value and its share price have both performed considerably worse than the S&P 500 Index:

{kind=link}

At first, this may appear to run contrary to the statement that real assets can help protect your wealth. However, short-term fluctuations in real asset valuations are always possible considering that supply and demand for these assets play a role, and as already mentioned the demand for real estate has fallen off considerably over the past two years. Over the long term, most real assets hold their value in the face of inflation due to the simple fact that they cannot be created out of thin air.

As nearly a year has passed since we last discussed the Nuveen Real Asset Income and Growth Fund, it is logical to assume that a great many things have changed. Therefore, let us revisit this fund and analyze these changes as we attempt to determine whether or not buying this fund makes sense today.

About The Fund

According to the fund's website , the Nuveen Real Asset Income and Growth Fund has the primary objective of providing its investors with a high level of current income and long-term capital appreciation. This makes sense considering the fund's strategy and the asset types that it invests in. The website explains:

The Fund seeks to deliver a high level of current income and long-term capital appreciation by investing in real asset-related companies across the world and the capital structure, including common stocks, preferred securities, and debt. Real asset-related companies include those engaged in owning, operating, or developing infrastructure projects, facilities, and services, as well as REITs.

Up to 40% of its assets may be debt securities, all of which may be rated below investment grade, though no more than 10% of its assets may be invested in securities rated CCC+/Caa1 or lower at any time. Non-U.S. exposure represents 25% to 75% of the Fund's managed assets. The fund uses leverage, and to a limited extent may also opportunistically write call options, seeking to enhance its risk-adjusted total returns over time.

As I have pointed out in various previous articles, most funds that have a primary objective of providing current income to their shareholders are best served by investing in fixed-income securities due to the simple fact that the yield on common stocks is incredibly low. The iShares U.S. Real Estate ETF ( IYR ) only yields 3.10% at the current price, and the iShares U.S. Utilities ETF ( IDU ) only yields 2.82% right now. These are generally considered to be among the highest-yielding sectors in the market, and even their yields pale in comparison to what can be easily obtained by investing in fixed-income securities. Meanwhile, common stocks are far better for capital appreciation due to the simple fact that bonds deliver no net capital gains over their lifetimes. I have explained this in various previous articles. The Nuveen Real Asset Income and Growth Fund invests in both common equities and fixed-income securities, so it is able to deliver the best of both worlds per its objective.

The fund's portfolio is currently fairly well-balanced between common equity and fixed-income securities. As we can see here, the fund currently has 42.73% of its portfolio invested in common equity along with smaller proportions to various types of fixed-income securities:

CEF Connect

Overall, the fund does have a higher allocation to fixed-income securities than it does to common stock. This works pretty well for the provision of income. After all, as already mentioned, both bonds and preferred stock have considerably higher yields than common equities right now. As such, these securities will provide the fund with a higher level of income than could be obtained by investing in a portfolio of 100% common equity.

Unfortunately, preferred securities are not nearly as good at protecting the value of your wealth over time. This is because the value of both bonds and preferred stocks is a function of interest rates and has no link to the value of the underlying real assets. When an apartment building increases in value, all of that increase goes directly to the common equity holders. Thus, the fact that this fund is more heavily weighted to fixed income means that it will not be entirely effective at achieving our goal of protecting our wealth against the loss of purchasing power that comes with inflation. That is probably not too bad right now, as real asset values have not really been increasing over the past year or two, but in the long term, it could be problematic. We will want this fund to be more heavily weighted to common stock if the Federal Reserve cuts rates and reignites inflation.

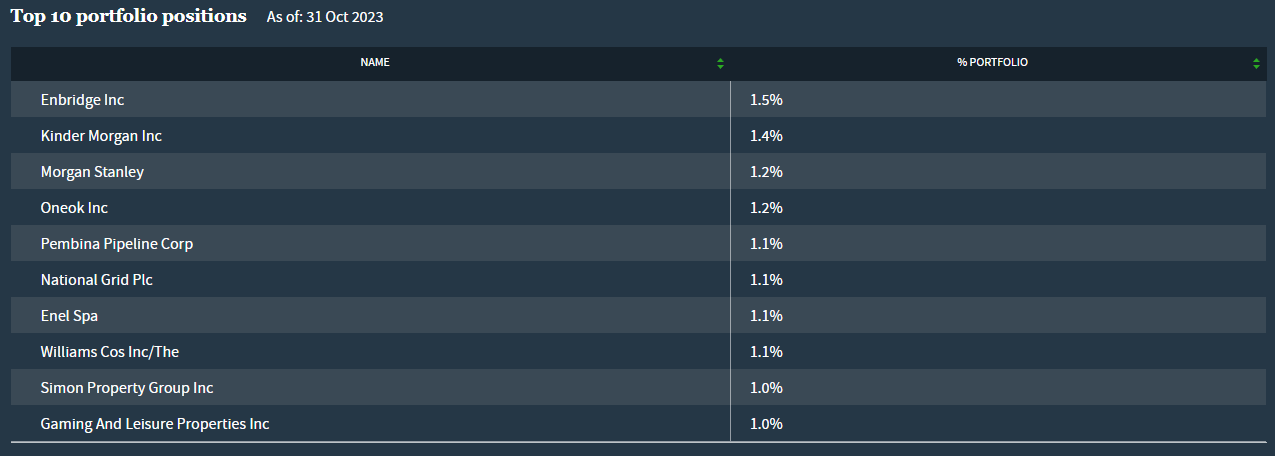

The last time that we looked at the fund, the Nuveen Real Asset Income and Growth Fund's largest positions were dominated by pipeline companies and real estate investment trusts. That is still the case today, although there have certainly been a few changes to the portfolio. Here are the largest positions in the fund as of October 31, 2023:

{kind=link}

We do still see a number of pipeline companies in the fund, although there is more diversity than the last time that we looked at the fund. For example, National Grid (NGG) and Enel (ENLAY) are both utilities and are both newcomers to the fund. NextEra Energy (NEE) and The Southern Company (SO) were both on the list the last time that we saw it, and as both companies are now gone it appears that the fund has swapped utility holdings. There are fewer pipeline companies today, as TC Energy (TRP) and Enterprise Products Partners (EPD) have been removed and replaced with ONEOK (OKE). Simon Property Group (SPG) and Gaming and Leisure Properties (GLPI) are both new additions to the fund, replacing Kimco Realty (KIM) and Public Storage (PSA). Finally, Morgan Stanley (MS) has been added to the fund for some reason. Morgan Stanley's position in a real asset fund is rather confusing, as it does not seem to fit with the fund's overall strategy of investing in infrastructure companies and real estate investment trusts. The bank's weighting at 1.2% of total assets is negligible though, so it is not really a big deal.

As long-time readers are no doubt well aware, I do not generally like to see any individual position in a closed-end fund accounting for more than 5% of the fund's total assets. That is because this is about the point at which an asset begins to expose the portfolio as a whole to idiosyncratic risk. I explained the concept of idiosyncratic risk in a few previous articles on closed-end funds. To paraphrase myself:

Idiosyncratic risk is that risk which any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then it will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not and if that asset accounts for too much of the fund's portfolio, then it may end up dragging the entire fund down with it.

Fortunately, we can see that this fund does not have outsized exposure to any individual asset. The largest position in the fund is Canadian pipeline giant Enbridge (ENB), and that position's 1.5% weighting is nowhere near enough to have an effect on the portfolio by itself. After all, even if for some reason Enbridge's shares went to $0, it would only reduce the fund's net asset value by 150 basis points. As such, this fund appears to be pretty well diversified in terms of individual company weightings. We should not need to worry about individual company risk here.

As we have already seen, there have been quite a few changes to the fund's portfolio over the past year. This could very easily lead someone to believe that the fund engages in a great deal of trading and has a very high turnover. This is not entirely incorrect, as the Nuveen Real Asset Income and Growth Fund had a 71.00% annual turnover last year. That is a bit higher than many common stock funds and it is substantially above the turnover of most fixed-income funds. As such, the fund's trading expenses might be a drag on the overall performance.

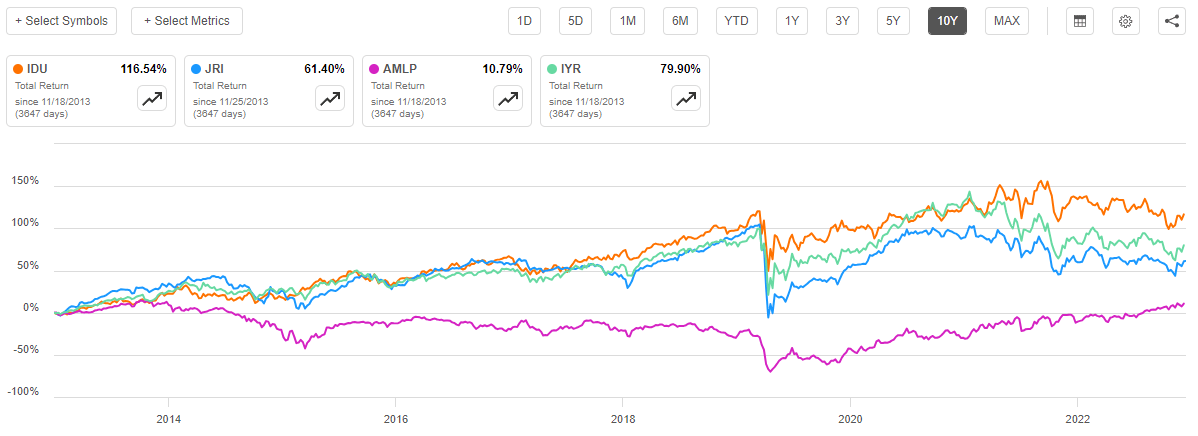

The Nuveen Real Asset Income and Growth Fund underperformed the U.S. Real Estate and U.S. Utilities indices over the past ten years on a total return basis. However, it did manage to beat the Alerian MLP Index (AMLP), which tracks pipeline partnerships:

{kind=link}

Thus, it is possible that the fund's substantial trading expenses have hurt its performance relative to index funds that have much fewer expenses of this nature. However, it could also be the case that the fund's pipeline positions have caused the fund's performance to disappoint relative to real estate and utilities. After all, pipeline companies did experience two crashes over the past ten years that other sectors largely managed to avoid. As a result of this exposure, we would expect that the fund's performance would be worse than either utilities or real estate, and that is exactly what we see.

Leverage

As is the case with most closed-end funds, the Nuveen Real Asset Income and Growth Fund employs leverage as a method of boosting its effective yield and returns beyond that of any of the underlying assets in the fund. I explained how this works in a variety of previous articles on such funds:

In short, the fund borrows money and uses that borrowed money to purchase both the common stock and fixed-income securities issued by companies that own real assets, such as infrastructure companies, utilities, and real estate investment trusts. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will normally be the case.

It is important to note though that leverage is much less effective at boosting a fund's total return today than it was a few years ago. This is because the difference between the rate that the fund has to pay on the borrowed money and the return that it can get from the purchased assets is much lower than it was during the zero-interest-rate era.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much leverage since that would expose us to an excessive amount of risk. I generally prefer a fund's leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the Nuveen Real Asset Income and Growth Fund has leveraged assets comprising 31.22% of its portfolio. That is reasonably conservative compared to many other closed-end funds, which is probably a good thing considering the current weakness of real estate investment trusts in the current environment and the occasional price shocks that we have seen in the pipeline sector.

Overall, this fund appears to be maintaining a reasonable balance between the risk and reward so we should not need to worry too much about its distribution right now.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Nuveen Real Asset Income and Growth Fund is to provide its investors with a high level of current income and long-term capital appreciation. In order to achieve this objective, the fund invests in infrastructure companies and real estate investment trusts. These two sectors tend to have higher yields than most others in the market today, although neither sector has an attractive yield compared to fixed-income securities. This fund does include fixed-income securities issued by these companies though, so it can make a nice income that way. It collects all of the dividends and distributions paid out by the securities that it purchases and even uses leverage to control more securities than it could solely with its assets. The fund then pays out all of this money along with any capital gains that it manages to realize to its investors, net of its own expenses. It can be assumed that this business model would result in the fund having a very high yield.

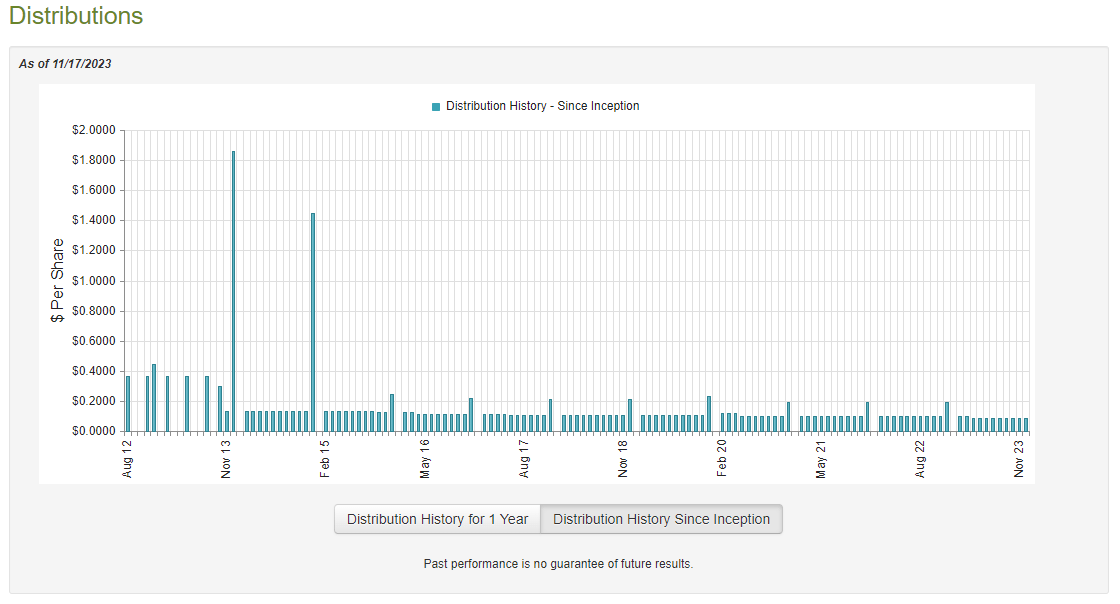

This is certainly the case, as the fund currently pays out a monthly distribution of $0.0870 per share ($1.044 per share annually), which gives the fund a 9.68% yield at the current price. Unfortunately, this fund has not been particularly consistent with respect to its distribution. As we can see here, the distribution has been steadily declining since 2013:

{kind=link}

This is certainly not the sort of thing that we want to see in a highly inflationary environment, such as the one that we are in today. After all, inflation is constantly reducing the purchasing power of the distribution so anyone who is depending on the distribution to pay their bills or finance their lifestyle expenses will want to see an increasing payout over time. Fortunately, the yield is high enough that a portion of it could be reinvested into shares of this fund (or some other fund) to grow the aggregate distribution that you receive.

With that said, the fund's distribution is not necessarily the most important thing for anyone who purchases the fund today. This is because anyone who buys the fund right now will receive the current distribution at the current yield. This new buyer will not be affected by the actions that the fund has taken in the past, as the only thing that really matters is how well the fund can sustain the current distribution going forward. Let us investigate that.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is obviously a much newer report than the one that we had available to us the last time that we discussed this fund so it should provide us with insight into why the fund had to cut its distribution earlier this year. It should also give us an idea of how well this fund was able to take advantage of the market euphoria during the first half of this year, which could have given it some potential to earn capital gains.

During the six-month period, the Nuveen Real Asset Income and Growth Fund received $10,880,042 in dividends and distributions along with $5,651,785 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources and subtract the foreign withholding taxes that the fund had to pay, we get a total investment income of $16,288,168 over the period. The fund paid its expenses out of this amount, which left it with $8,876,042 available for shareholders.

This was obviously nowhere close to enough to cover the amount that the fund paid out during the period. Over the course of six months, the fund paid total distributions of $14,852,440 to its investors. At first glance, this could be concerning as the Nuveen Real Asset Income and Growth Fund does not have sufficient net investment income to cover its payouts.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. In particular, the fund might be able to realize some capital gains that could be paid out as distributions. Unfortunately, it generally failed at this task during the period. During the six-month period, the fund reported net realized losses of $14,690,409, which it managed to offset with $18,361,535 net unrealized gains. Overall, the fund's net assets declined by $2,718,496 after accounting for all inflows and outflows during the period.

Thus, the fund failed to fully cover its distribution, just as it did during the previous full-year period. During the full-year 2022 period, the fund's net assets declined by $105,460,022 after accounting for all inflows and outflows. Thus, we now have a situation where the fund's net assets have been declining for eighteen straight months. This is not sustainable and certainly explains the distribution cut back in April.

Unfortunately, it appears that even the lower distribution might not be sustainable. The fund's net asset value is down 6.71% since July 1, 2023:

{kind=link}

Thus, Nuveen Real Asset Income and Growth Fund is paying out more than its investments are making. This is a bad sign, and we will certainly want to examine the fund's financial statements when it releases its full-year numbers in a few months to determine how sustainable it is likely to be going forward. This is a very large decline though, so it does not bode well.

Valuation

As of November 17, 2023 (the most recent date for which data is available as of the time of writing), the Nuveen Real Asset Income and Growth Fund has a net asset value of $12.65 per share but the shares only trade for $10.85 each. This gives the fund's shares a 14.23% discount on the net asset value at the current price. That is a very reasonable discount, although it is not as good as the 15.20% discount that the fund's shares have averaged over the past month. As such, it might be possible to get a better price by waiting a bit, but generally speaking, a double-digit discount is a very reasonable entry price for any closed-end fund. Right now looks fine to enter if you are interested in owning this fund.

Conclusion

In conclusion, the Nuveen Real Asset Income and Growth Fund invests in companies that own real assets such as real estate and energy distribution infrastructure. These real assets should be able to act as a store of value and protect your wealth from the ravages of inflation. There has certainly been some short-term pressure on some of the fund's holdings though, due mostly to the fact that utilities are frequently purchased for their dividends and the demand for real estate has fallen in response to rising mortgage rates. Over the long term though, real assets should hold their value and every investor should have at least some exposure to them.

Unfortunately, Nuveen Real Asset Income and Growth Fund's distribution appears to be strained as its net asset value has been declining for at least eighteen months and it appears that it is struggling to maintain it so far in the second half of this year. Thus, it might be a good idea to be prepared for another possible distribution cut.

For further details see:

JRI: Real Assets Belong In Your Portfolio, But This Distribution Looks Strained