PFF - JRS: Limited Exposure To Troubled Real Estate Sectors And A Very Attractive Yield

2023-11-03 14:11:30 ET

Summary

- The Nuveen Real Estate Income Fund offers a high level of income to investors through investments in real estate securities.

- Despite concerns about rising interest rates, most real estate companies have held up well, providing an opportunity for income-focused investors.

- The JRS closed-end fund currently yields 10.33%, higher than most other options in the market, but its performance has been disappointing with a 10.92% loss for investors since August 2023.

- The JRS fund managed to cover its distribution in the first half of the year, but only through unrealized gains. These may have since been wiped out.

- The fund's shares are currently trading at a very attractive discount on the net asset value.

The Nuveen Real Estate Income Fund ( JRS ) is a closed-end fund, or CEF, that specializes in providing a high level of income to investors by investing in securities issued by real estate investment trusts and similar entities. The real estate sector in general has been under a great deal of pressure due to rising interest rates. However, apart from the commercial office space sub-sector, the cash flows of most of the companies have held up just fine. This is partly because things like apartment buildings, data centers, and other real estate companies that are not having issues with tenant retention are able to increase their rents to compensate for rising expenses due to inflation as well as higher interest expenses as mortgages adjust upward (many landlords have adjustable-rate mortgages). In other words, the sector is generally holding up better than the market seems to think and that may have created an opportunity for income-focused investors to obtain very high yields. Indeed, the Nuveen Real Estate Income Fund yields 10.33% at the current price, which is substantially higher than most other things in the market right now.

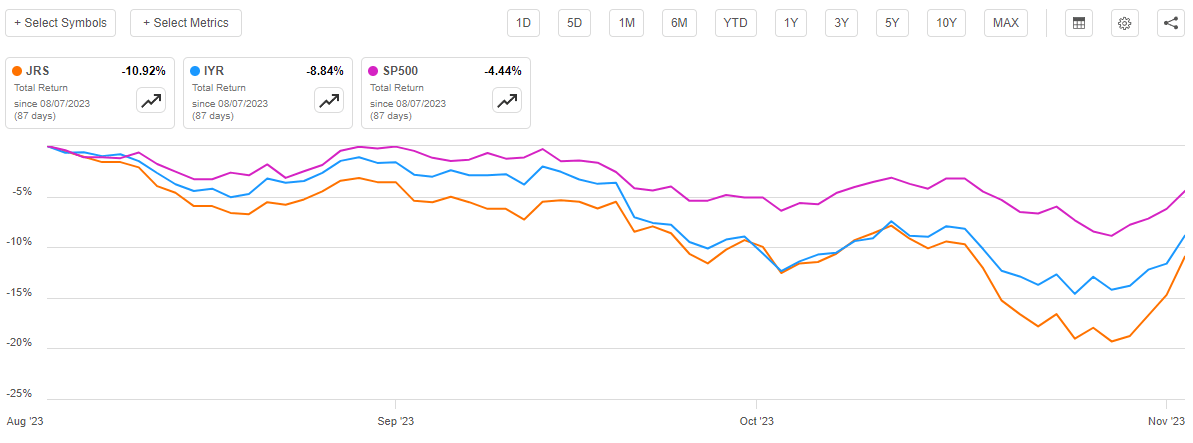

As regular readers may remember, we last discussed the Nuveen Real Estate Income Fund back in August 2023. The fund's performance since that time has been rather disappointing. Investors who purchased the fund when that previous article was published have now lost 10.92% of their investment after we take the fund's distribution into account. This is worse than either the S&P 500 Index ( SP500 ) or the iShares U.S. Real Estate ETF ( IYR ):

{kind=link}

If we look simply at the fund's price performance, it has done even worse as the large distribution provides an offsetting effect to some of the fund's share price decline. This alone is not necessarily the end of the world though, as there are still a few reasons to consider including real estate or a real estate fund like this one in your portfolio. In particular, real estate can serve as a store of wealth that helps to protect you against inflation. In addition, as we have already seen, it can be quite reasonable as a source of income.

Let us investigate this fund and attempt to determine if it might still make sense to include it in your portfolio today.

About The Fund

According to the fund's website , the Nuveen Real Estate Income Fund has the primary objective of providing its shareholders with a high level of current income and capital appreciation. As the name of the fund suggests, it aims to achieve this objective by investing in a portfolio of securities issued by real estate investment trusts and similar entities. The webpage describes the strategy thusly:

The Fund's investment objective is high current income and capital appreciation.

The Fund invests primarily in income-producing common stocks, preferred stocks, convertible preferred stocks and debt securities issued by real estate companies. At least 75% of the Fund's managed assets will be in securities rated investment grade. The fund uses leverage.

Thus, we can see that the fund includes mostly common stocks and various types of preferred stocks. However, it is currently somewhat more weighted to common stock than preferred securities:

CEF Connect

This actually makes a good deal of sense given the fund's objective. This is true despite the statements that I have made in past articles about common stocks not being especially good income vehicles. One of the reasons for this is that common stocks issued by real estate investment trusts tend to be quite reasonable in terms of yield. The iShares U.S. Real Estate ETF, which tracks the Dow Jones U.S. Real Estate Capped Index, has a current yield of 3.38%. That is, admittedly, not especially high when compared to fixed-income securities but it is still quite a bit better than the S&P 500 Index.

The fact that the fund also includes preferred stock and debt issued by real estate investment trusts improves its income credentials. These securities tend to boast much higher yields than common stock because the dividends and distributions are the primary ways in which these securities provide a return to the investors. As such, these securities will generally always yield a premium over the risk-free rate. Here are the current yields offered by a few different Treasury offerings:

| Security |

| Current Yield |

| U.S. Treasury - 1 Mo. |

| 5.398% |

| U.S. Treasury - 3 Mo. |

| 5.427% |

| U.S. Treasury - 6 Mo. |

| 5.496% |

| U.S. Treasury - 1 Yr. |

| 5.326% |

| U.S. Treasury - 2 Yr. |

| 4.882% |

| U.S. Treasury - 5 Yr. |

| 4.512% |

| U.S. Treasury - 10 Yr. |

| 4.556% |

The iShares Preferred and Income Securities ETF ( PFF ), which tracks the ICE Exchange-Listed Preferred & Hybrid Securities Index, currently yields 6.81%. That is clearly a premium to U.S. Treasury securities, which is exactly what we would expect. It is fair to assume that the preferred stock held by the Nuveen Real Estate Income Fund has a similar yield to that of the index. Thus, it clearly beats most other options available in the market today.

The fact that the Nuveen Real Estate Income Fund is more heavily weighted towards common stock than preferred stock does mean that its income will probably be lower than if it was primarily weighted towards preferred stock. However, the common stock favoritism does work well for the thesis that I outlined in my previous article on this fund. In short, I pointed out that real estate by its very nature can serve as a hedge against inflation. This comes from the fact that real estate cannot just be printed into existence as fiat currency can. The root cause of inflation is the money supply increasing faster than the actual productive output of an economy, so anything that is in limited supply and can only experience a supply increase through actual human or mechanical effort should increase in value along with everything else during inflationary periods. This is one of the biggest reasons why house prices have been increasing rapidly since the pandemic, and it should affect all other forms of real estate as well. Thus, this fund should be able to serve as protection against inflation. However, only the common equity issued by real estate investment trusts will accomplish that goal. The preferred equity will not because it has no link to any appreciation of the underlying property.

This comes from the fact that when a property is sold, the debt holders are completely paid off first. After that, the preferred equity holders receive their initial investment back. Whatever is left is distributed among the common equity holders. Thus, the debt holders and the preferred equity holders basically are stuck only receiving their money back plus any dividends or distributions that their securities paid in the interim. The common equity holders end up receiving all of the property's appreciation. Investors who want to bet on real estate values going up, which is what you want if you are looking for an inflation hedge, will want to hold the common equity. This fund is doing that, although it is balancing its common equity position with a preferred stock position for income. That is a very reasonable balance to be holding right now.

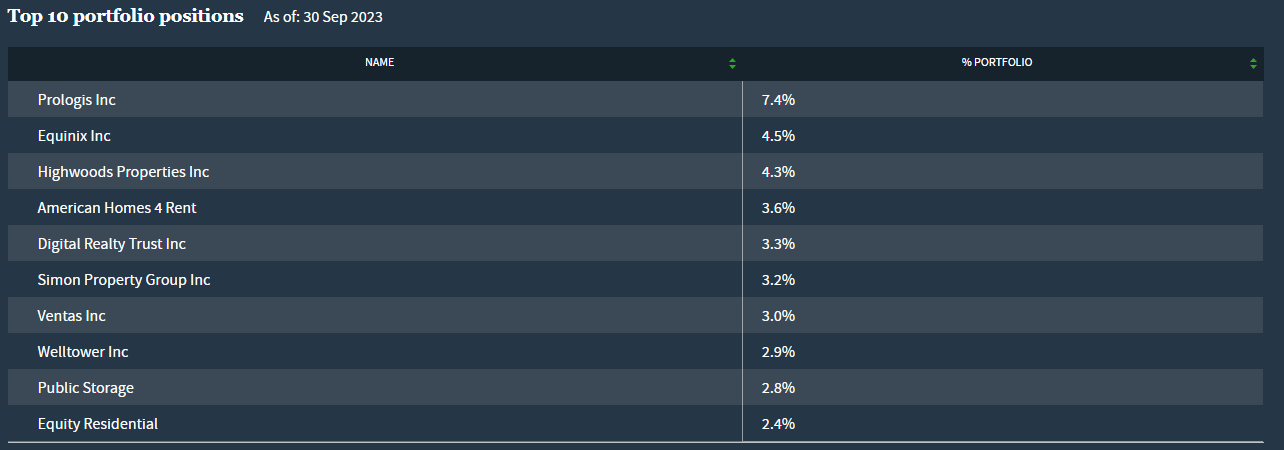

Many of the fund's largest positions are the same as the last time that we discussed it. Here are the current largest positions in the fund's portfolio:

{kind=link}

While most of the companies listed here were on the fund's largest positions list the last time that we discussed it, there have certainly been a few changes. In particular, CubeSmart ( CUBE ), Alexandria Real Estate Equities, Inc. ( ARE ), and Kite Realty Group Trust ( KRG ) have all been removed from the list. In their place, we have Ventas, Inc. ( VTR ), Public Storage ( PSA ), and Equity Residential ( EQR ). Interestingly, Public Storage and Equity Residential were both included among the fund's largest positions back in November of last year and were removed from the largest positions list mid-year. They are now back on the list, which could imply that the fund never fully sold out of its positions, but simply temporarily reduced them during the early to middle part of 2023.

In addition to those three major changes, a number of the fund's largest positions have seen their weightings change since the date of the last publication. This could be caused by the fund actively buying and selling stocks to change their weightings in the fund, but it might also be caused simply by one asset outperforming another in the market. The fund has a 58.00% annual turnover, which suggests that both possibilities are occurring. That turnover certainly seems high, especially when compared to a typical index fund, but it is actually pretty much in line with most equity closed-end funds.

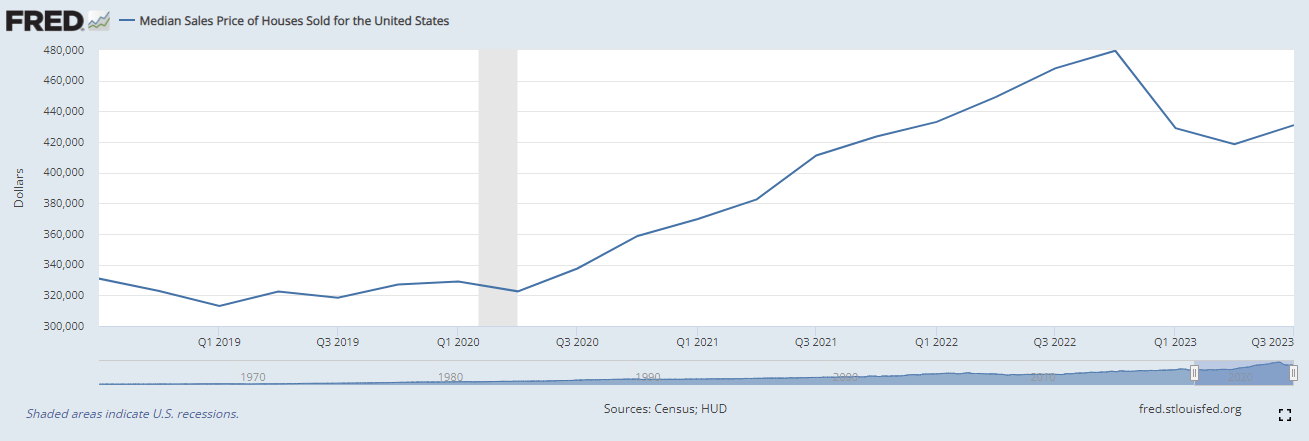

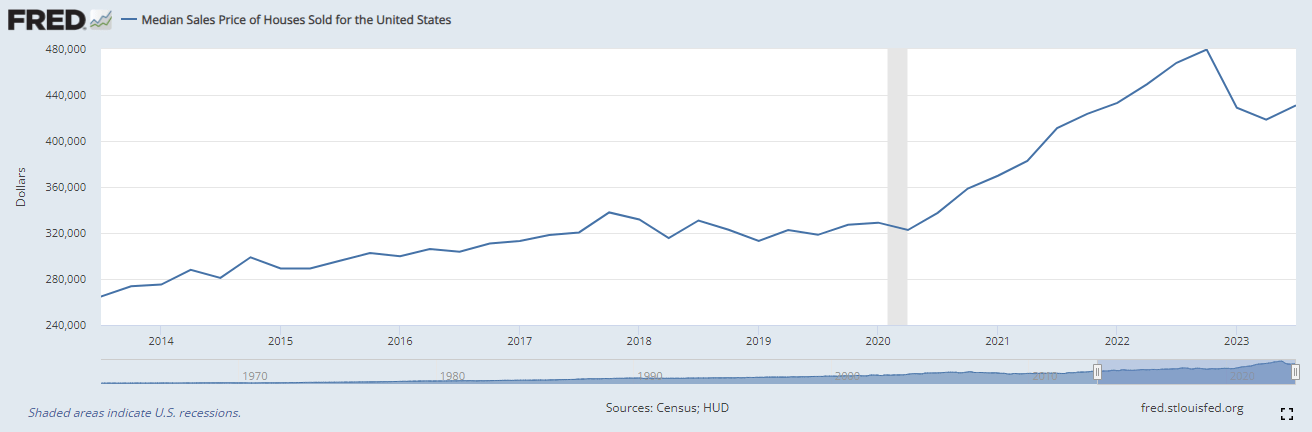

The real estate sector has not been a favorite among many investors as higher mortgage rates have caused a lot of fear among investors that property values will be coming down. However, thus far that has not really happened to the degree suggested by the market. In the third quarter of 2023, the median sales price of a home in the United States was $431,000. That is lower than the peak in the fourth quarter of 2022, but it is an increase over both the first and the second quarter of 2023. It is also higher than at any time prior to the first quarter of 2022:

{kind=link}

Here is the same chart extended over a longer period:

{kind=link}

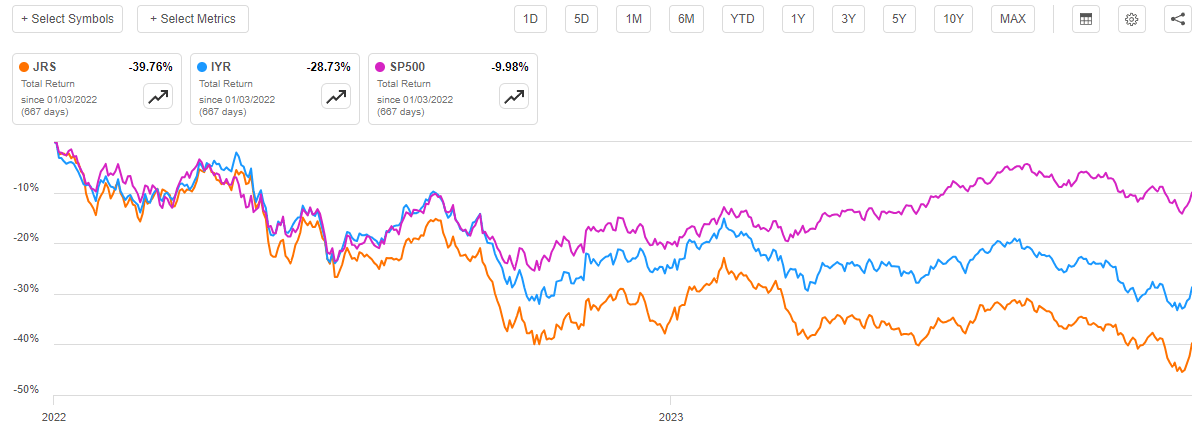

Thus, we can see that while there has been a decline in home prices versus the median level in 2022, prices have not declined nearly as steeply as the market seems to be expecting. Since the start of 2022, the U.S. Real Estate Index has delivered a -28.73% total return. The Nuveen Real Estate Income Fund has done even worse, handing its investors a 39.76% loss even after we include the effects of the distribution:

{kind=link}

That is much more than the actual decline in real estate prices, which could indicate an opportunity.

With that said, there is one area of real estate in which poor market performance is warranted. This is in commercial office space. The COVID-19 pandemic caused many companies to switch to a remote work environment, where employees are simply able to remain at their homes to work as opposed to commuting to the office. It is questionable whether or not there are benefits to such a work structure, as some companies suggest that in-office work is strongly preferable while others suggest that the flexibility that working at home provides their employees is worthwhile. Employees seem to prefer working at home, however. When we combine this with rising crime rates in various cities that have generally encouraged employees and employers to stay away, many companies have found that it makes more sense just to cancel their leases for office space and put the money elsewhere.

This has caused a substantial number of vacancies in certain areas. A recent article suggests that 33.9% of office space in San Francisco, California is vacant. The article goes on to suggest that even higher vacancy rates could arise in the near future as some tenants have stated their intention not to renew their leases. This has obviously pushed down commercial office space valuations in those areas. After all, real estate is, at its core, worth what someone will pay for it, and nobody is going to buy a vacant office building that is not generating income and that they do not need for their own business.

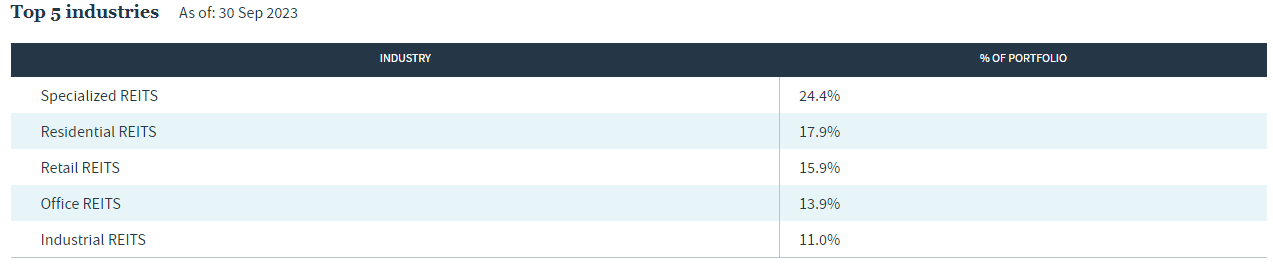

Fortunately, the Nuveen Real Estate Income Fund has only limited exposure to commercial office space. As we can see here, only 13.9% of the fund's assets are invested in real estate investment trusts that specialize in commercial office space:

{kind=link}

Thus, this fund is focusing its attention on those sectors that still own desirable properties that are holding their value. After all, in the case of rental real estate, as long as you can avoid vacancies and raise the rent sufficiently to cover rising expenses due to inflation then the property should hold its value and protect the property owner against inflation. Thus, a fund like this might still make sense for someone seeking to protect their assets against the ravages of inflation.

Leverage

As mentioned in the fund website's description of its strategy, the Nuveen Real Estate Income Fund employs leverage as a method of boosting its yield beyond that of any of the actual assets in the fund. This is something that is commonly done by closed-end funds to allow them to deliver some of the highest yields available in the market. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase common and preferred equity issued by real estate investment trusts. As long as the purchased securities have a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, this strategy is not as effective today with borrowing rates at 6% as it was two years ago when borrowing rates were essentially nothing. This is because most real estate common equities have yields of less than 6%, meaning that the fund has to depend on sufficient capital appreciation to offset the money that it pays in interest on the borrowed money as it can no longer rely on dividends alone.

The use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an outsized amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Nuveen Real Estate Income Fund has levered assets comprising 30.23% of its portfolio. That is a reasonable balance between the risks and rewards caused by leverage, so it is probably okay.

However, the fund's leverage is higher than the 27.91% ratio that it had the last time that we discussed this fund. That is somewhat concerning, as it would be preferable to see this ratio moving in the opposite direction. That is especially true if rates continue to rise, which is a distinct possibility. I discussed that in previous articles. This is because leverage costs pressure the fund's net investment income down and may ultimately force it to cut its distribution. We already saw this with other equity closed-end funds (see here ). As such, we should keep a close eye on the fund in order to ensure that its leverage remains at a reasonable level and does not increase too much from the present point.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Nuveen Real Estate Income Fund is to provide a high level of current income to its shareholders. In order to achieve this objective, the fund invests in a portfolio of common and preferred equity issued by real estate investment trusts. These securities tend to have higher yields than many other sectors, although not all of them are competitive with fixed-income securities in today's environment. The fund seeks to offset this both through realizing capital gains as real estate prices appreciate and by using leverage to boost its effective yield and capital gains. The fund collects all of the money that it earns through this strategy and pays it out to the investors, net of its own expenses. In the past, this strategy worked very well to allow the fund to boast a very high yield. It is, unfortunately, somewhat less effective today but the fund still does a reasonable job of providing its investors with a high level of current income.

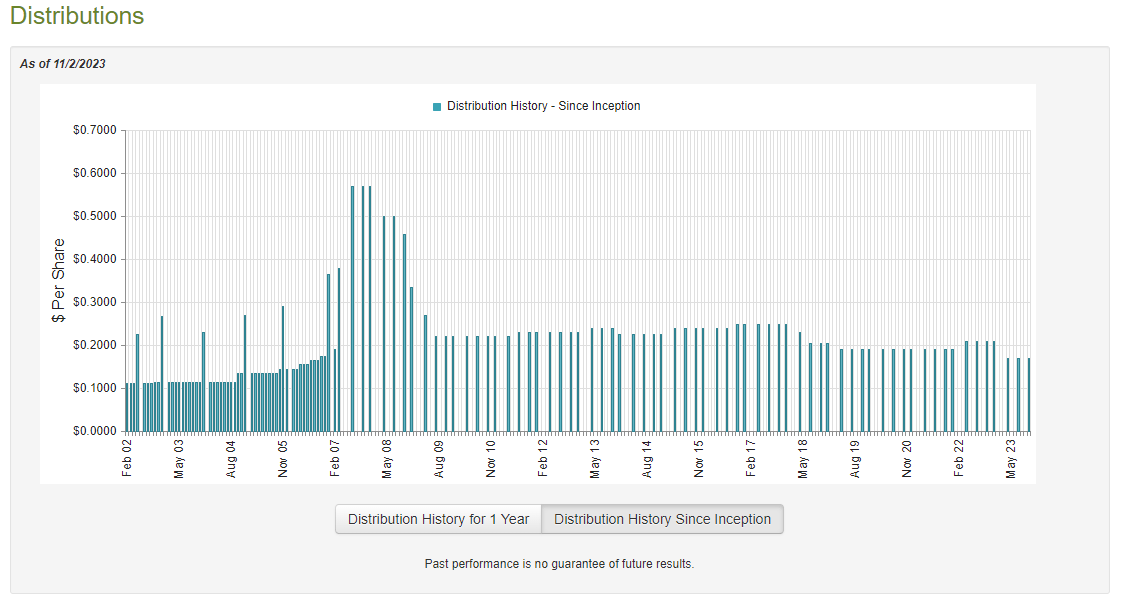

The Nuveen Real Estate Income Fund currently pays a quarterly distribution of $0.17 per share ($0.68 per share annually), which gives it a 10.33% yield at the current price. That is obviously quite a bit higher than the S&P 500 Index or just about any real estate index fund on the market, although it is only in line with other real estate-focused closed-end funds. Unfortunately, the fund has not been especially consistent with respect to its distribution. In fact, it has varied quite a lot:

{kind=link}

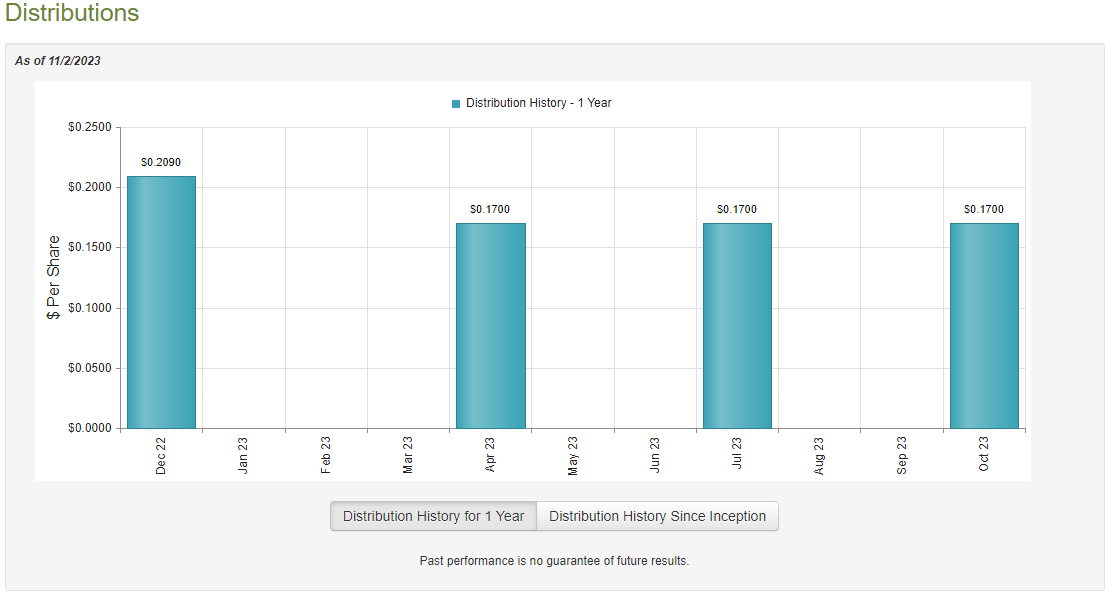

As we can see, the fund has varied its distribution significantly from quarter to quarter and year to year over its lifetime. This will almost certainly reduce the appeal of this fund in the eyes of those investors who are seeking to earn a safe and consistent income from their assets that can be used to pay their bills or finance their regular expenses. The fact that this fund cut its distribution this year will further reduce its appeal:

{kind=link}

There are other funds out there, such as the CBRE Global Real Estate Income Fund ( IGR ), that have managed to keep their distribution steady even in the current environment. The fact that this one has not could thus make some of those competing funds more attractive for investors who are focused on the generation of income.

As is always the case though, the fund's history is not necessarily the most important thing to consider when we are evaluating a fund as an income investment. This is because anyone who purchases the fund's shares today will receive the current distribution at the current yield and will not be affected by events that have occurred in the past. Thus, the most important thing is how well the fund can sustain its current distribution going forward.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a newer report than the one that we had the last time that we discussed this fund, which is nice. This is because the first half of 2023 was characterized by optimism among market participants that the Federal Reserve will rapidly abandon its monetary tightening policy and begin to cut rates. As a result, investors bid up the prices of most common stocks, bonds, and other assets. While this optimism has ultimately proven to be unfounded, it still could have given the fund an opportunity to earn some capital gains on the assets in its portfolio. That will be reflected in these results but obviously would not have been reflected in the fund's annual report for 2022, which was the most recent document that was available the last time that we discussed this fund.

During the six-month period, the Nuveen Real Estate Income Fund received $7,598,930 in dividends along with $114,318 in interest from the assets in its portfolio. This gives the fund a total investment income of $7,713,248 during the period. It paid its expenses out of this amount, which left it with $3,458,708 available to shareholders. That was, unfortunately, not nearly enough to cover the distribution that the fund paid out. During the six-month period, the Nuveen Real Estate Income Fund paid out distributions totaling $9,823,440. At first glance, this is likely to be concerning as the fund clearly failed to cover its distribution out of net investment income.

However, there are other methods through which the fund can obtain the money that it needs to cover its distribution. For example, it might have been able to generate some capital gains that could be paid out to investors. The fund had mixed results in this task, however. It reported net realized losses of $2,172,341 but these were more than offset by $18,607,342 net unrealized gains. Overall, the fund's net assets increased by $10,070,269 over the period after accounting for all inflows and outflows.

The fund's net assets increased during the period even after considering the distribution that was paid out so overall it did manage to cover the payment. However, we can clearly see that it had to rely on net unrealized capital gains to accomplish that task. This is concerning, as unrealized gains do not result in an inflow of money into the fund until these assets are sold, and the gains realized. Thus, these gains could very easily be erased if the market turns sour, which it did following the end of the period that is reflected in this report. The fund's net asset value is down 7.14% year-to-date, so this suggests that it is the case that its unrealized gains have since been wiped out. Thus, the fund may not have covered its distribution as well as this report suggests.

Valuation

As of November 2, 2023 (the most recent date for which data is currently available), the Nuveen Real Estate Income Fund has a net asset value of $7.54 per share but the shares currently trade for $6.78 each. That gives the shares a 10.08% discount on net asset value at the current price. This is a reasonable discount, although it is nowhere near as attractive as the 12.99% discount that the shares have had on average over the past month. Thus, investors may be able to obtain a better price by waiting for a short period of time. However, a double-digit discount generally represents a good entry point for any fund, so it is not necessarily a bad time to get into this fund right now if you want the shares.

Conclusion

In conclusion, real estate can offer a lot of potential for an investor who is seeking to protect their wealth against the ravages of inflation. This comes from the fact that it should be able to hold its value due to the fact that it is in limited supply and requires real effort to improve. However, there are certain sectors of the real estate market that have fallen off a cliff due to a lack of demand. Nuveen Real Estate Income Fund appears to be limiting its exposure to those sectors and focusing on in-favor sectors.

The valuation is also quite attractive right now. The big issue here is that the distribution may not be sustainable right now as the fund had to rely on net unrealized losses during the first half of the year to sustain its payout, and it is possible that these unrealized gains have since been wiped out.

For further details see:

JRS: Limited Exposure To Troubled Real Estate Sectors And A Very Attractive Yield