RYLD - Juan's Top High Yield ETFs For 2023

Summary

- I mostly write about dividend-paying equity and bond ETFs, perfect for income investors and retirees.

- Some of these are offering particularly high yields right now, and seem well-positioned for 2023.

- A look at some of the best of these.

Author's note: This article was released to CEF/ETF Income Laboratory members on January 10th.

Investment markets had a tumultuous 2022, with most asset classes and investment funds down for the year. Although losses were detrimental for investors in the past, they present something of an opportunity for investors in the future. Several asset classes and investments are offering much more compelling dividends and value propositions now than in the past and could see outstanding results moving forward. Thought an article summarizing some of the strongest of these might interest readers and subscribers.

Three funds stand out.

The Invesco CEF Income Composite Portfolio ETF ( PCEF ), which holds a diversified portfolio of CEFs, and offers investors a strong, growing, fully covered 8.5% dividend yield. PCEF's dividends could see further growth if interest rates continue to increase, which seems very likely. Risks are high, and the fund would likely cut its dividends and post sizable losses during any future recession or downturn.

The VanEck Vectors BDC Income ETF ( BIZD ), which holds a diversified portfolio of BDCs, and offers a strong, growing, fully covered 10.5% dividend yield. As with PCEF, BIZD's dividends could see further growth if interest rates continue to increase, but the fund is quite risky, and should see dividend cuts and sizable losses during future recessions.

The Global X Russell 2000 Covered Call ETF ( RYLD ), which invests in small-cap Russell 1000 components, and sells covered calls on its holdings. RYLD boasts a 13.1% yield, and tends to outperform when markets move sideways or drift downwards. Although RYLD's dividends are covered by option premiums, these are incredibly volatile, and at risk of being cut. RYLD's small-cap holdings are riskier than average, and so is the fund.

In my opinion, the three funds above are strong investment opportunities, and the best high-yield ETFs for 2023. At the same time, all three are relatively risky funds, and generally only appropriate for more aggressive investors and retirees.

As a final point, I wrote a similar article to this one last year. My picks all outperformed last year, and by reasonably good margins. Here's hoping for good results this year too.

PCEF - Diversified Fund of CEFs

PCEF is an index ETF investing in a diversified portfolio of investment-grade bonds, high-yield bonds, and equity option income / call options CEFs. PCEF invests in the three major income-producing asset classes or fund classifications, which makes it a perfect choice for income investors and retirees desiring broad-based exposure to CEFs.

PCEF - Benefits

Diversification

PCEF is an incredibly diversified fund, with exposure to most important income-producing asset classes, over 100 CEFs, and thousands of underlying securities. Diversification reduces risk, volatility, and the potential for losses and underperformance due to subpar results in any one specific fund. No single investment decision or investment fund can cause significant losses or underperformance for PCEF, as the fund invests in many funds, with many holdings each.

Strong, Growing 8.5% Dividend Yield

PCEF's underlying holdings and asset classes tend to generate significant income, which results in a strong 8.5% yield for the fund. It is a very strong yield on an absolute basis, and higher than that of most asset classes, although average relative to most CEFs.

PCEF invests quite heavily in bond CEFs, which tend to see higher income and distributions when interest rates are rising , as they currently are. PCEF distributes said income to shareholders as dividends, so fund dividends should see healthy growth due to past and future (expected) interest rate increases. PCEF's dividends grew around 4.6% in 2022, as expected.

PCEF's dividends should continue to grow in 2023, although much will depend on how interest rates move from here on out.

PCEF's strong, growing 8.5% dividend yield is a significant benefit for the fund and its shareholders, and its core investment thesis.

Discount to NAV

PCEF is an ETF, so tends to trade at NAV. PCEF invests in CEFs, which tend to trade with discounts. Currently, PCEF's underlying holdings trade with an average discount to NAV of 5.1%. It is a good discount, very slightly higher than the funds historical average, although nothing outstanding.

PCEF

PCEF's discount increases its dividend yield, and could lead to capital gains in the future, contingent on discounts narrowing. As the fund's discount is not that large, these are relatively minor benefits, but benefits nonetheless.

Good Performance Track-Record

PCEF's performance track-record is reasonably good, with the fund generally outperforming relative to its closest peers.

PCEF generally performs reasonably well relative to indexes covering its underlying holdings. It underperforms relevant covered call equity indexes, as equities are one of the best-performing asset classes of the past few years, but outperforms relevant bond indexes.

On a more negative note, as the fund focuses on bonds, it tends to underperform most relevant equity indexes long-term, including the S&P 500.

As a final point, and as per my calculations , the fund does tend to outperform relative to an average of its underlying asset classes.

PCEF - Drawbacks

Risky Holdings

PCEF invests quite heavily in high-yield and equity CEFs, two relatively risky asset classes. PCEF's underlying holdings are generally leveraged, which increases risks further. PCEF invests in CEFs, which tend to trade with discounts, which tend to widen during downturns and recessions.

These characteristics combine to create a relatively risky investment, and one which should underperform during downturns, bear markets, and the like. As an example, PCEF underperformed relative to bonds and equities during 1Q2020, the onset of the coronavirus pandemic.

PCEF is a relatively risky investment and, in my opinion, only appropriate for more aggressive investors and retirees.

Relative Low Potential for Alpha

PCEF invests in over 100 CEFs, using relative lax / broad inclusion criteria. Although there is nothing inherently wrong with the fund's approach, it does somewhat limit the potential for particularly strong, market-beating returns. A concentrated fund or portfolio might, potentially, focus on the best-performing CEFs, leading to outstanding returns. A diversified fund, like PCEF, simply invests in too many funds and securities for significant outperformance. Leverage, management alpha, and discounts might lead to some outperformance, as they generally have in the past, but don't expect outstanding results from PCEF.

Some investors might prefer to create their own personalized portfolio of CEFs. Investors could use stricter criteria, focusing on CEFs with particularly strong yields, performance track-records, or discounts. Doing so might, potentially, result in stronger yields and total returns. Although doing so is difficult and outperformance is far from certain, I do believe that most investors are up to the task.

PCEF can never match the potential yields and returns of a more targeted CEF portfolio, a negative for the fund and its shareholders.

I last covered PCEF here .

BIZD - BDC Index ETF

BIZD is a U.S. BDC index ETF. BDCs are financial institutions which provide funds, usually loans, to small and medium sized U.S. enterprises. Said loans are almost always relatively risky, and so tend to sport high interest rates. BDCs are generally leveraged, as are most financial institutions. One could think of BIZD as a leveraged high-yield bond play, with all the benefits and risks that entails.

BIZD- Benefits

Strong, Growing 10.5% Dividend Yield

BIZD's underlying holdings generate a lot of income, due to the high interest rate on their underlying loan portfolios and use of leverage. Said income is distributed to fund shareholders as dividends, resulting in a 10.5% dividend yield for the fund. It is an incredibly strong yield on an absolute basis, and significantly higher than that of most asset classes.

BDCs make loans, and their interest rate is partly determined by Federal Reserve rates. All else equal, higher Fed rates mean higher rates on these loans, which means higher BDC earnings and dividends, which ultimately results in higher BIZD dividends. Rates have risen these past twelve months, during which BIZD's dividends have seen strong growth, as expected.

BIZD's dividends should continue to grow in 2023, although much will depend on how interest rates move from here on out.

BIZD's strong, growing 10.5% dividend yield is a significant benefit for the fund and its shareholders, and its core investment thesis.

Cheap Valuation

BIZD currently trades with a relatively cheap valuation, with a PE ratio of 13.1x, and a PB ratio of 0.9x.

BIZD

BIZD's cheap valuation could lead to capital gains moving forward, contingent on valuations normalizing. These are far from certain, and are unlikely to be all that large, as the fund's valuation is not that cheap. Still, some moderate capital gains are possible, and a prospective benefit for the fund's investors.

BIZD - Drawbacks

Concentration / Lack of Diversification

BIZD invests in a relatively niche asset class, BDCs. BIZD's underlying holdings have very similar business models and areas of operation, which exposes investors to idiosyncratic risk, and the possibility of substantial underperformance from the underperformance of any one specific holding or industry.

A fund like PCEF holds investment-grade bonds, which would perform reasonably well during a downturn. An index like the S&P 500 includes non-financial corporations, which would be less affected by a downturn centered on financials, as the past financial crisis. BIZD is concentrated on a very specific niche, is incredibly exposed to conditions in said niche, and would see significant losses and underperformance if said niche underperforms.

Risky Holdings

BIZD's underlying holdings are quite risky, due to focusing on loans to relatively risky issuers, and due to their use of leverage. BIZD's underlying holdings are particularly exposed to economic and credit conditions, and should see increased default rates during downturns and recessions. Dividend cuts and capital losses are likely to follow suit. This was the case during 1Q2020, the onset of the coronavirus pandemic, and the most recent downturn.

BIZD is a relatively risky investment and, in my opinion, only appropriate for more aggressive investors and retirees.

I last covered BIZD here .

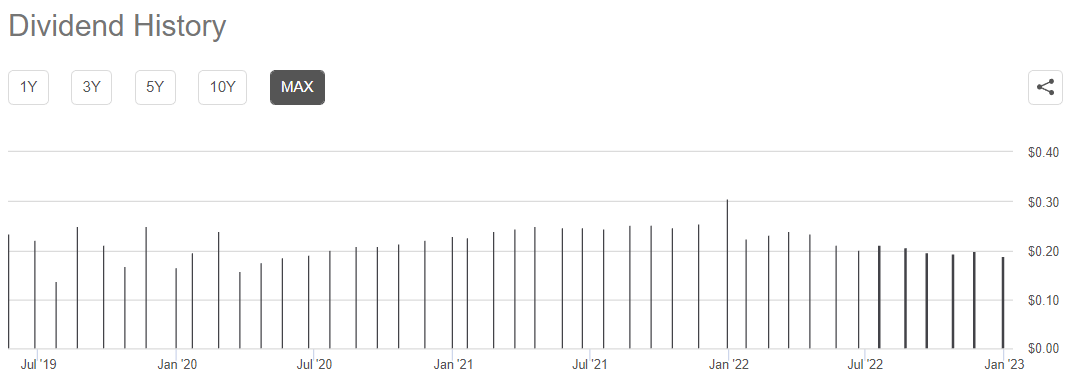

RYLD - Small-Cap Covered Call ETF

RYLD is a small-cap covered call index ETF. The fund invests in the components of the Russell 2000, a U.S. small-cap equity index, and sells covered calls on the entirety of its holdings. Selling covered calls effectively trades away most potential capital gains for an increased 13.1% yield. Downside potential remains the same.

RYLD - Benefits

Strong 13.1% Yield

RYLD's covered call strategy generates significant premiums for the fund, most of which are distributed to shareholders as dividends. RYLD itself yields 13.1%, an incredibly strong yield on an absolute basis, and significantly higher than that of most asset classes.

RYLD's strong yield is a significant benefit for the fund and its shareholders, and its core investment thesis.

Although RYLD's dividends are fully covered by underlying generation of option premiums, these are incredibly volatile, and could, potentially, decline moving forward. Expect significant dividend volatility, and above-average risk of significant dividend cuts.

RYLD's dividends are capped to around 12.0% yield, with the fund retaining any option premiums above and beyond that to invest in the Russell 2000. Under current conditions, investors should expect dividends of around 12.0% moving forward.

High Option Prices

RYLD sells (covered) call options. Call option prices are dependent on many factors, including volatility. All else equal, higher volatility equals higher option prices. Volatility has increased since early 2021, leading to higher option prices.

As RYLD sells options, the fund directly benefits from higher option prices. Said benefit is partly realized through higher dividends, as the fund distributes some of the premiums generated to shareholders. Said benefit is also partly realized through higher capital gains / lower capital losses, as the fund is currently retaining a sizable portion of premiums generated. Both increase total shareholder returns, a benefit for the fund and its shareholders.

Higher option prices were instrumental in RYLD's outperformance during 2022.

RYLD - Drawbacks

Low Potential Capital Gains

RYLD sells covered calls, which severely limits potential capital gains. As an example, the fund's share price increased by 16.9% during 2H2020, compared to 36.9% for the Russell 2000. RYLD's covered call strategy reduced the fund's capital gains by over half during said semester, to the detriment of its investors.

RYLD's downside potential remains unchanged, but upside is quite limited. So, RYLD's share price should go down long-term, as has been the case since the fund's inception.

RYLD should see long-term capital losses / lower share prices, a significant negative for the fund and its shareholders.

Expected Long-Term Dividend Cuts

RYLD's dividends should see long-term declines, due to the fund's declining share price / assets per share (can't have growing income as capital gets depleted, at least not for very long). This has mostly not been the case since inception, as higher option prices have more than made up for lower share prices / assets per share. Dividend volatility, normal for an ETF, makes this somewhat difficult to analyze or measure, but looking through the fund's dividends and dividend growth metrics, I'm not really seeing any long-term trend.

{kind=link}

Seeking Alpha

Expected Long-Term Underperformance

RYLD has significantly reduced potential capital gains. Equities tend to post strong capital gains, so foregoing these should lead to long-term underperformance. This has been the case since inception, as expected.

RYLD's expected long-term underperformance is a significant negative for the fund and its shareholders.

On a more positive note, RYLD is not certain to underperform long-term. The fund could outperform if option prices remain high and equity capital gains low. In my opinion, slight underperformance is the likeliest scenario, and I consider this to be an important negative, but underperformance is not certain.

Conclusion

High yield ETFs offer investors strong dividends, compelling value propositions, and are generally enticing investments for more aggressive income investors and retirees. PCEF, BIZD, and RYLD are three strong high yield ETFs, and my top buys for 2023.

For further details see:

Juan's Top High Yield ETFs For 2023