VICI - Juicy Income With These 2 Hotel REITs

2023-08-22 07:00:00 ET

Summary

- Hotel REITs faced significant challenges during the pandemic but are now showing signs of recovery.

- Apple Hospitality REIT is a top performer with a well-diversified portfolio and strong balance sheet, offering a 6.6% yield.

- VICI Properties stands out with its asset portfolio and offers a 5.2% yield.

This article was coproduced with Leo Nelissen.

I think it’s fair to say that hotel REITs were among the most hated investments during the pandemic years. Occupancy rates were at rock bottom, often as a result of lockdowns. On top of that, global restrictions, like China’s zero-COVID policies, kept a lid on global travel.

To make things worse, the inflation surge after 2021 did a number on discretionary spending, which includes hotels.

Investors were much better off buying industrial real estate, Sunbelt residential real estate, or beaten-down retail REITs, to name a few.

Having said all of this, REITs, in general, are now feeling pressure from elevated rates and fears that the Fed may have to keep rates elevated on a prolonged basis.

Interestingly enough, the hotel space is still recovering.

In this article, we’ll discuss two promising hotel/leisure REITs that not only come with juicy income but also business models that make decent long-term total returns very likely.

So, let’s get to it!

What’s Up With Hotels?

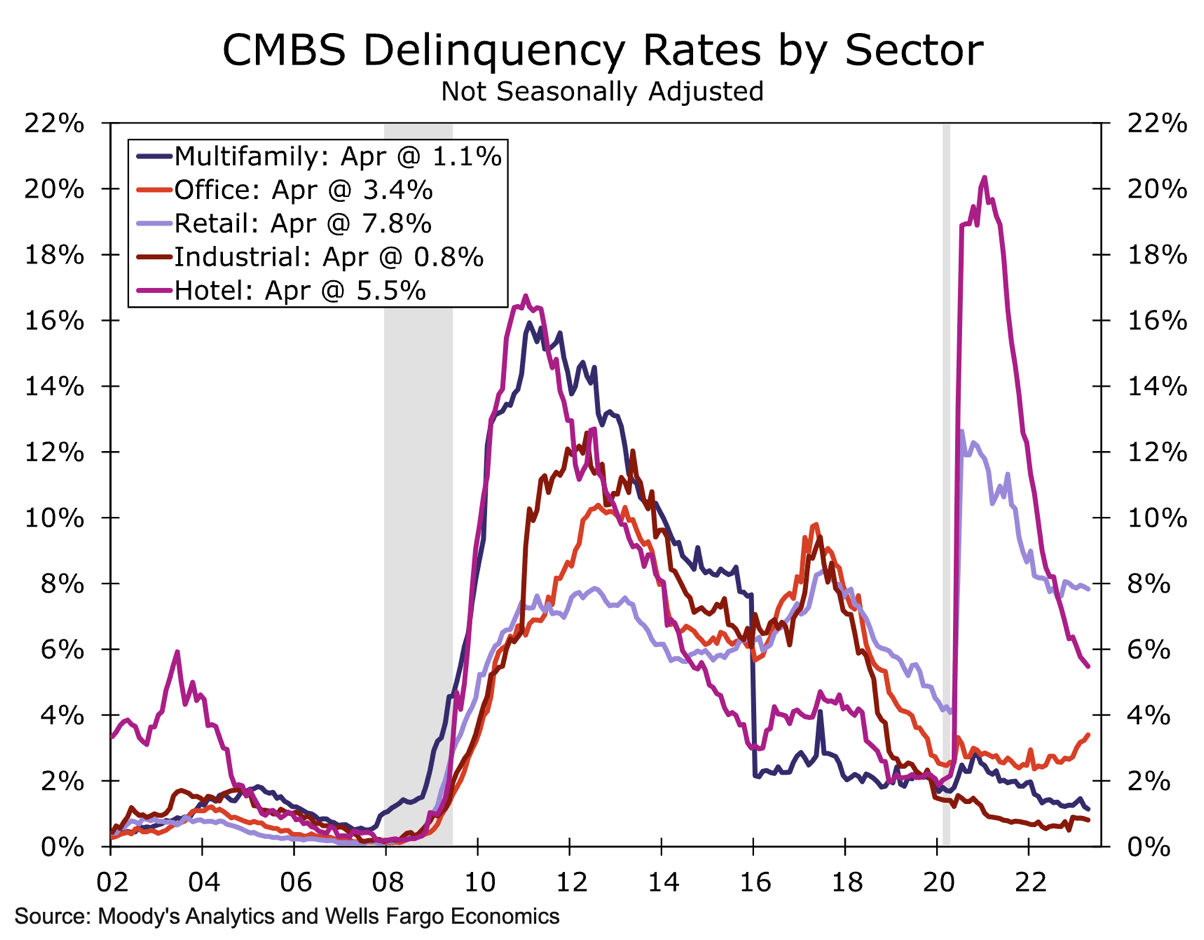

During the pandemic, delinquency rates in the hotel industry exceeded 20%. Now, delinquency rates are falling, while sectors like office real estate are showing increasing weakness.

Going into the summer, delinquency rates in the hotel sector were at 5.5%, below the retail sector and roughly 200 basis points above office delinquency rates.

{kind=link}

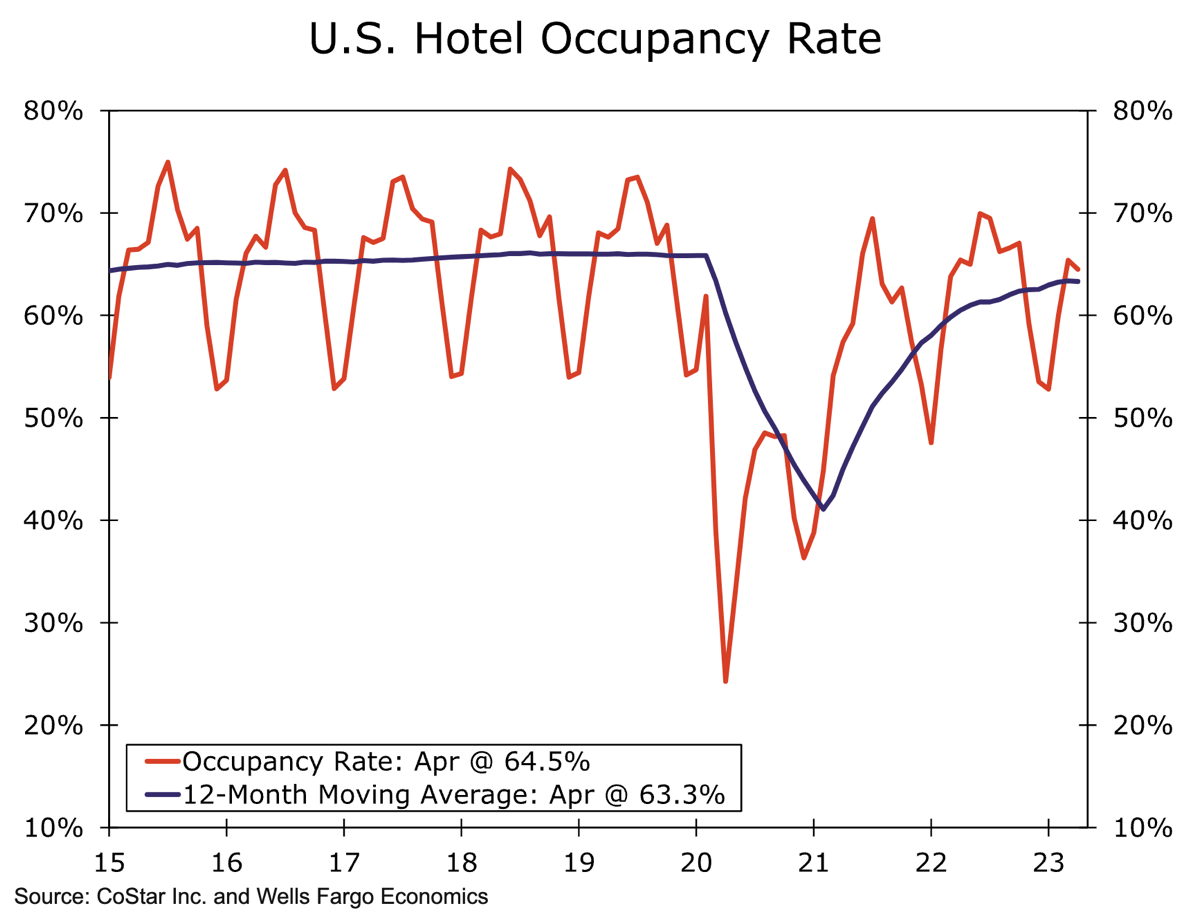

As reported by Wells Fargo’s most recent CRE report, following a seasonal lull during the winter months, the hotel industry has seen a remarkable resurgence in the spring.

In the first quarter, the average hotel occupancy rate reached an impressive 59.4%, marking a substantial increase from the 56.0% recorded during the same period in the previous year.

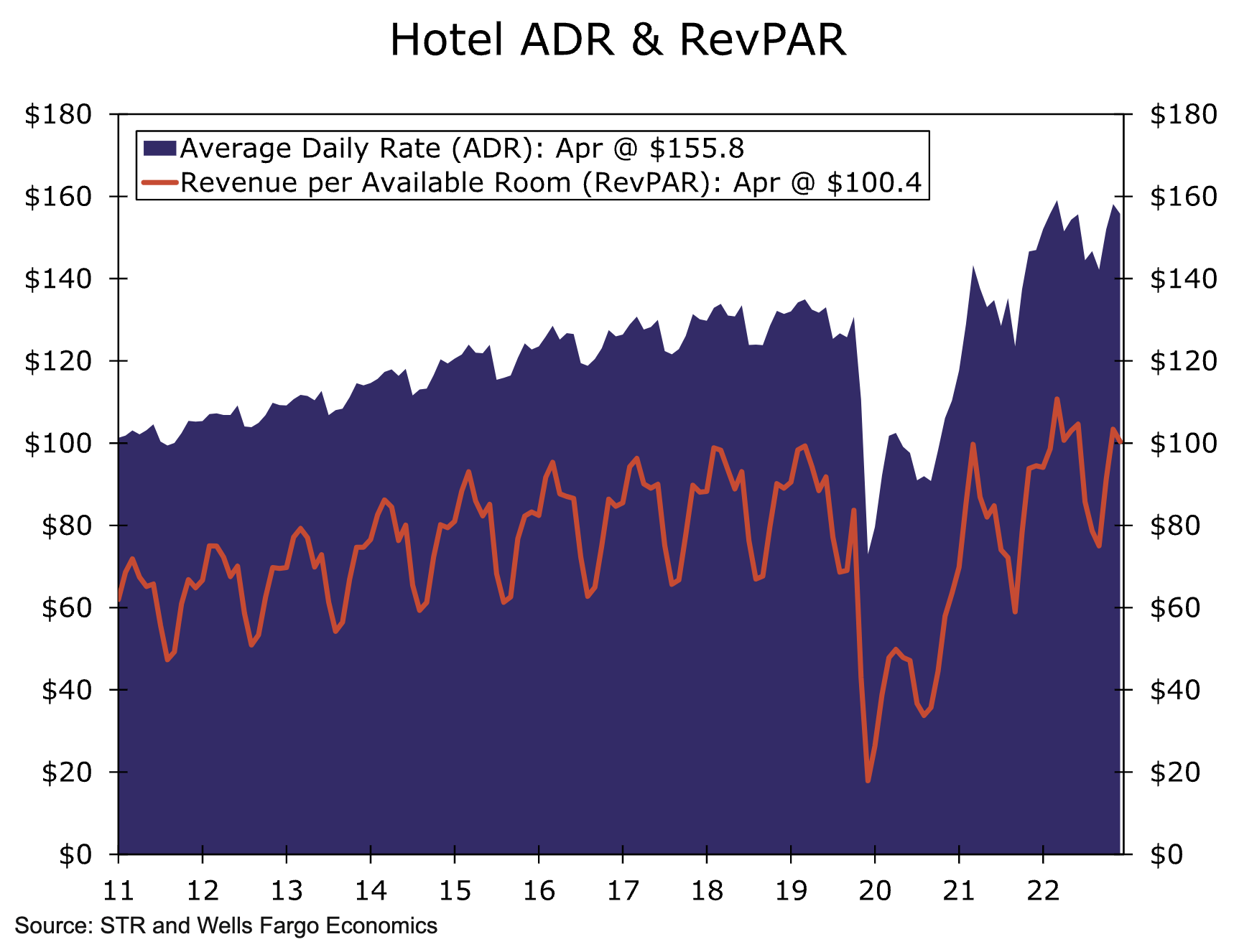

This resurgence was also reflected in the Average Daily Rates (ADR), which showed a robust year-over-year growth rate of 10.9%.

Additionally, the room revenues experienced a notable upswing of 17.1% over the course of the year in the first quarter.

{kind=link}

As the industry transitioned into the second quarter, signs emerged of a modest deceleration. Notably, hotel occupancy during the month of April averaged 64.5%, displaying a marginal decrease from the 65.4% figure observed in the prior-year period.

This decline is the first year-over-year contraction in occupancy since February 2021.

While occupancy rates have shown a slight lag, the sector's revenue stream remains relatively stable. ADR demonstrated resilience, climbing to $155.80 in April, which is a modest 3.4% year-over-year rise.

Growth in Revenue Per Available Room (RevPAR) was more moderate, as it was up 1.9% year-to-date. Looking at the bigger picture, we see that both ADR and RevPAR are close to all-time highs.

{kind=link}

With regard to supply growth, in April, the number of rooms under construction experienced a decline to approximately 150,000 units, down from January's 160,000 units. Notably, this number stands well below the pre-pandemic peak of 210,000 units, which is good news for hotels.

In other words, while hotels aren’t firing on all cylinders, it’s still an industry with steady progress.

These developments come with opportunities.

Pick 1: Apple Hospitality REIT (APLE) – 6.6% Yield

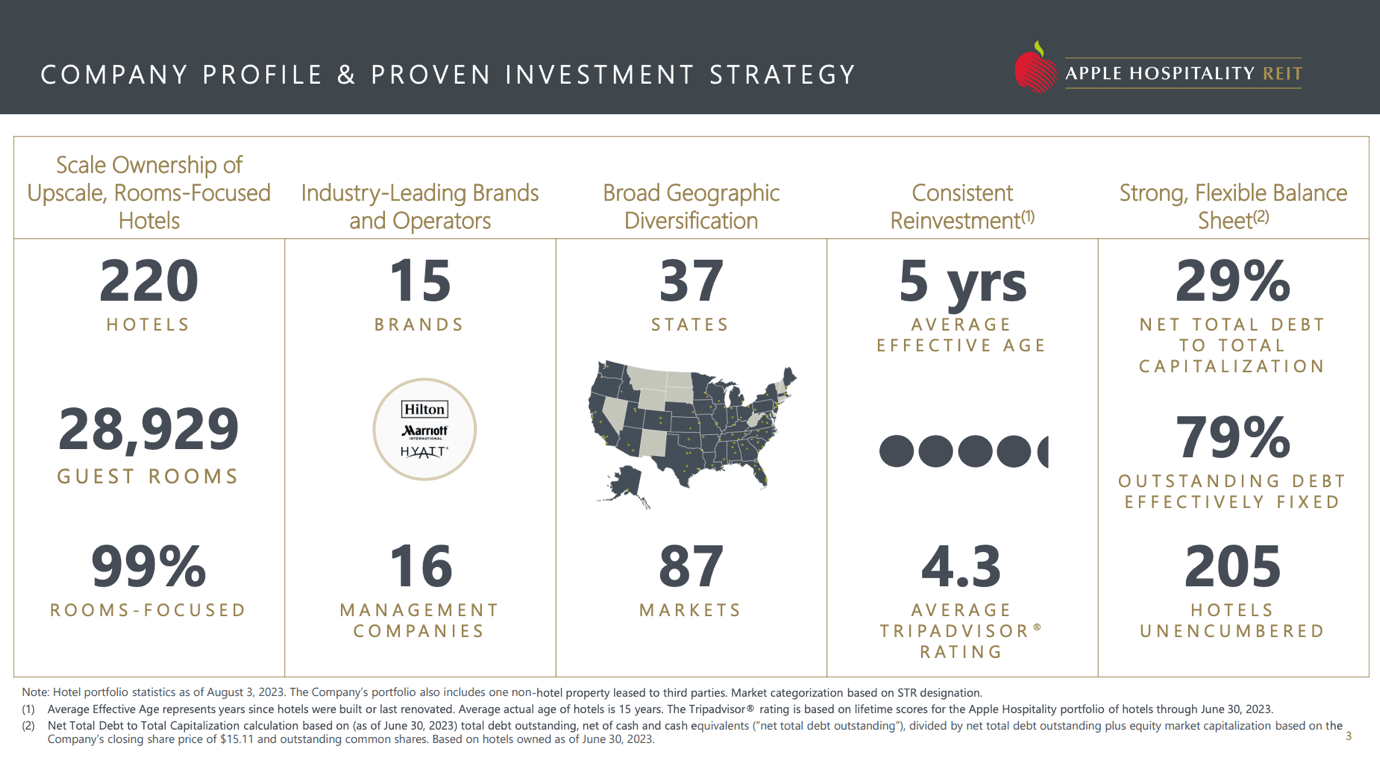

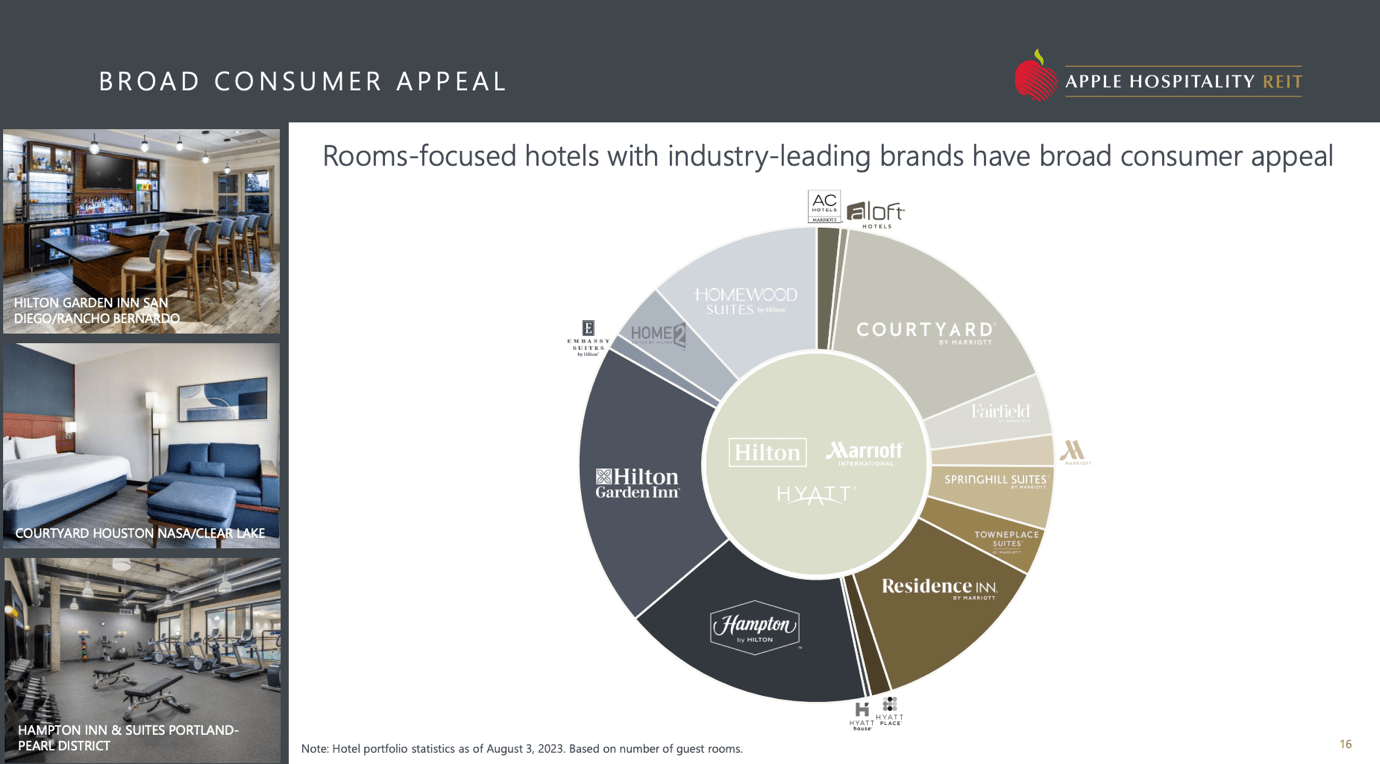

Apple Hospitality is one of the best-managed hotel REITs on the market. With a market cap of roughly $3.3 billion, it focuses on upscale hotels. This room-focused hotel REIT, meaning it has no exposure to conventions and other major events, has hotels in 37 states. Its 220 hotels are managed by 16 management companies.

{kind=link}

Most of its roughly 29,000 hotel rooms are operated under Hilton, Marriott, or Hyatt brand names.

{kind=link}

Its hotels are diversified across 87 markets. Most of its hotels are located in suburban markets. According to the company, suburban markets come with a broad mix of business and leisure demand generators that, in addition to a wide range of amenities and conveniences, help to drive consistent demand.

In addition to my aforementioned supply comments, APLE is in a good position when it comes to new hotel supply. Almost 50% of its hotels do not have any exposure to new projects (within a five-mile radius). Also, national supply growth over the next four quarters is expected to be just 0.9%. That’s more than 30% below the long-run average.

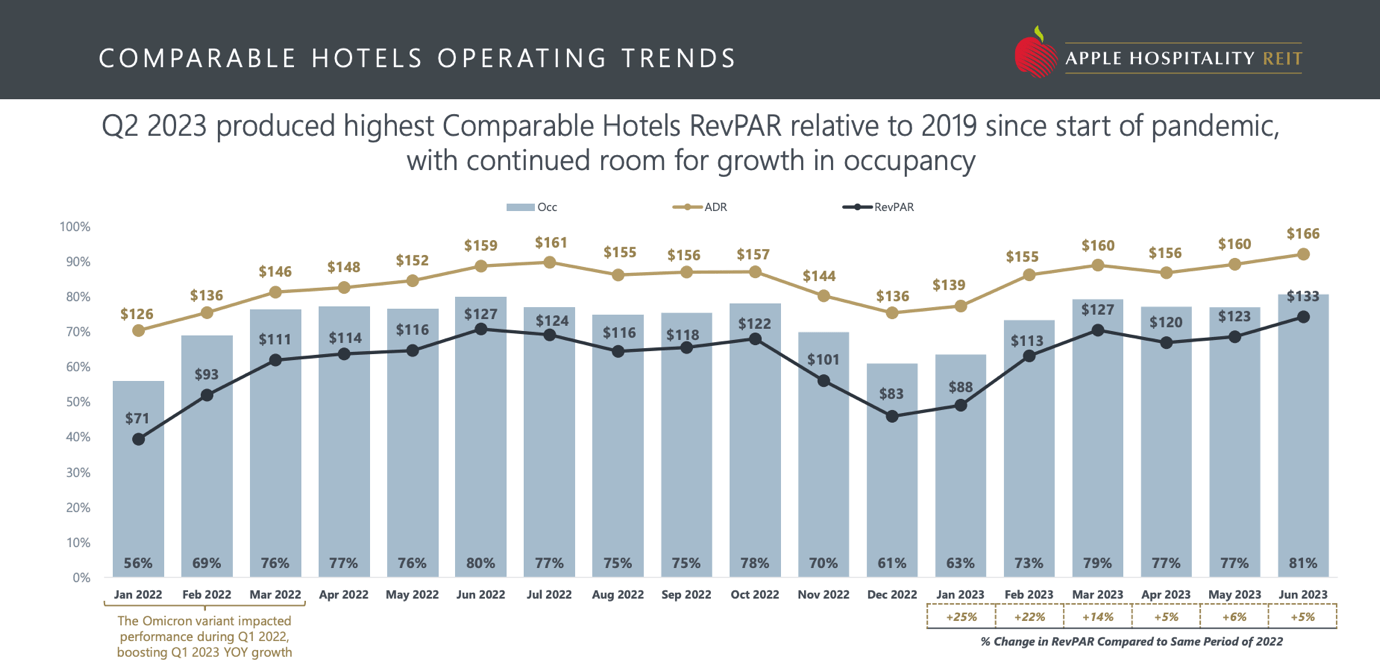

With that in mind, the company is in a great spot. During the second quarter, the company observed continued strength in leisure travel demand. Weekend occupancies for April, May, and June ranged from 82% to 84%, highlighting the elevated interest in leisure stays.

Additionally, business travel demand showed gradual improvement, with year-over-year support for average weekday occupancies of 75% in April, 74% in May, and 79% in June.

{kind=link}

As a result, the comparable hotels' RevPAR experienced a 5% increase over the second quarter of 2022. The Average Daily Rate stood at $161, indicating a 5% increase, and occupancy reached 78%, a nearly 1% rise over the same period in the previous year.

In light of the first part of this article, APLE is clearly outperforming its peers when it comes to occupancy rates. This helps its ability to grow ADR and RevPAR.

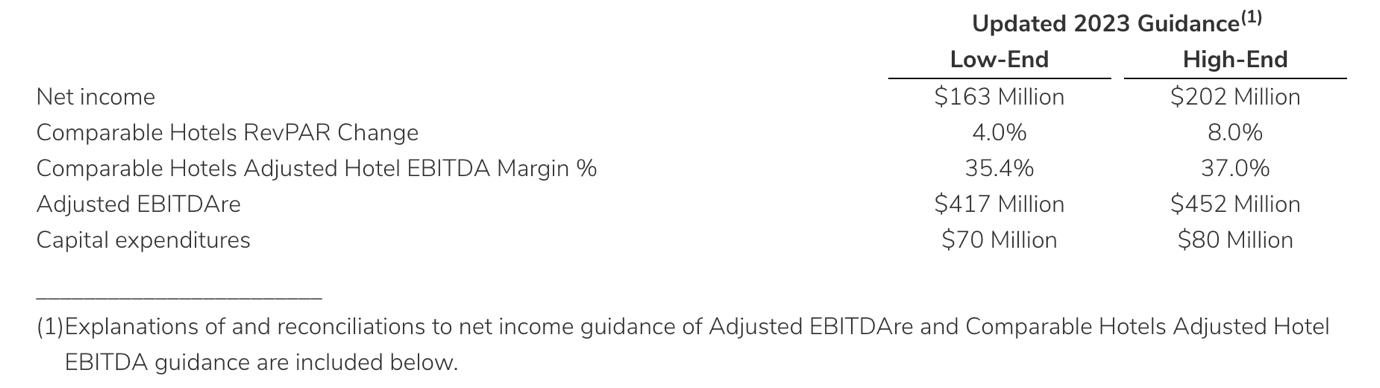

APLE also upgraded its guidance in early August.

Thanks to a strong operating environment, APLE anticipates comparable hotels' RevPAR growth to be between 4% and 8%, a 100 basis points increase on both ends of the range.

- Similarly, the company aims for comparable hotels' adjusted hotel EBITDA margin to be between 35.4% and 37%, reflecting a ten basis point increase on both ends.

- Adjusted EBITDAre is projected to fall within the range of $417 million to $452 million, while net income is expected to be between $163 million and $202 million.

{kind=link}

The company also has a healthy balance sheet.

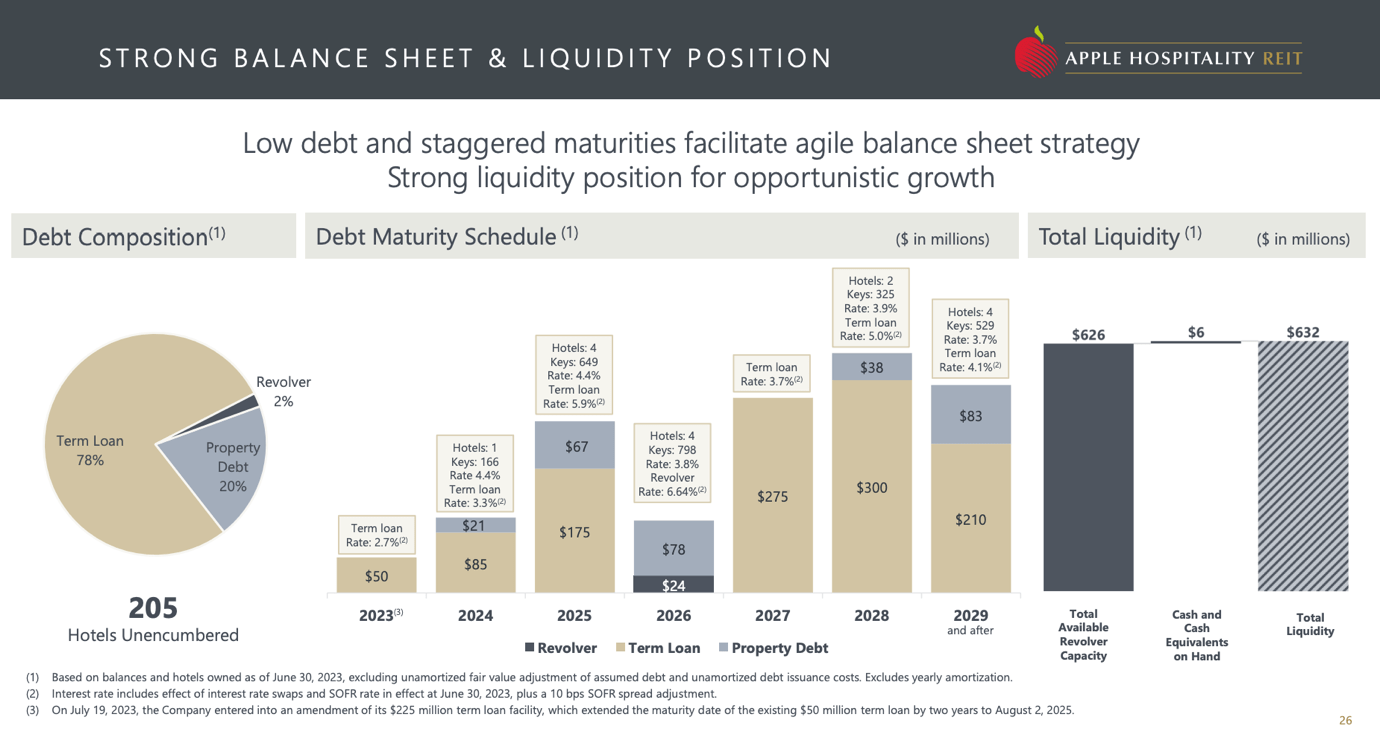

Of its portfolio, 205 hotels are unencumbered, which significantly lowers financial risks for its portfolio – especially in this high-rate environment.

As of June 30, the company had $1.4 billion in outstanding debt, roughly 3.2x its trailing 12 months EBITDA. The weighted average interest rate is just 4.3%.

In July, the company entered into an amendment of its $225 million term loan facility, which extended the maturity of the existing $50 million term loan by two years to Aug. 2, 2025, and aligned the maturity date with the other term loan and the broader $225 million facility.

{kind=link}

In other words, not only does the company own a top-tier portfolio of high-quality brands with above-average occupancy rates, but it also has one of the best balance sheets in the industry.

This has paved the way for a post-pandemic dividend recovery.

APLE has never been a dividend growth stock. It has always been a go-to place for a high yield.

Before the pandemic, it paid $0.10 per share per month. During the pandemic, the dividend was cut to protect the balance sheet. After all, nobody knew how bad things might have gotten back then.

Now, the dividend is back to $0.08 per share. This translates to a 6.6% yield.

Seeking Alpha

This dividend is backed by a 63% forward FFO payout ratio, which is in line with the sector median.

If the company’s recovery continues, a $0.10 monthly dividend is likely, which would translate to an 8.3% yield.

The company is trading at 9.2x forward FFO. That’s below the sector median of 12.2x and caused by the unattractiveness of the hotel REIT industry.

The current consensus price target is $18, which is 24% above the current price.

We have a Speculative Buy rating on APLE.

When looking for juicy income, APLE is one of my favorite spots in the REIT industry.

Pick 2: VICI Properties (VICI) – 5.2% Yield.

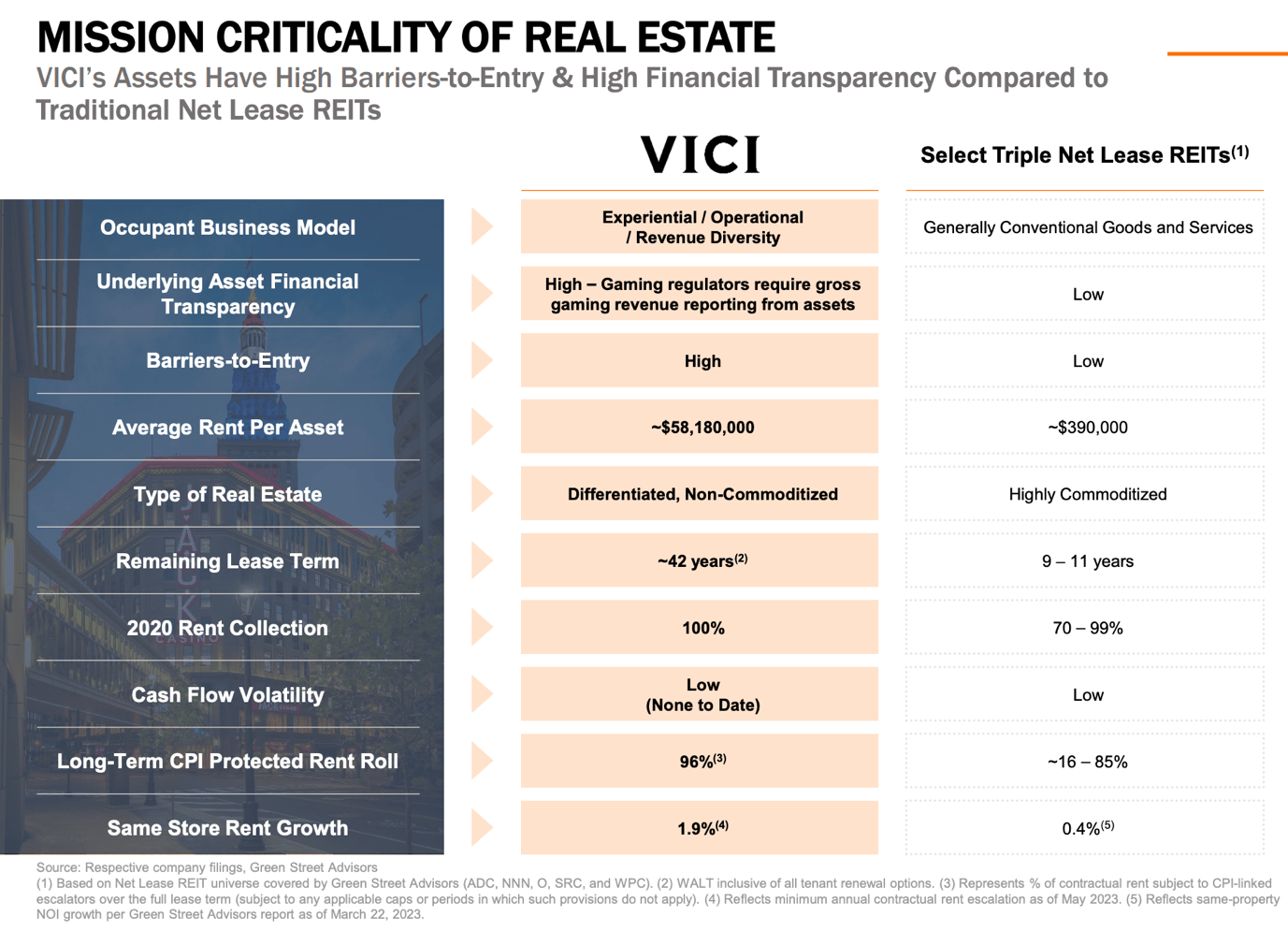

When talking about hotels and leisure, VICI is one of the best investments money can buy.

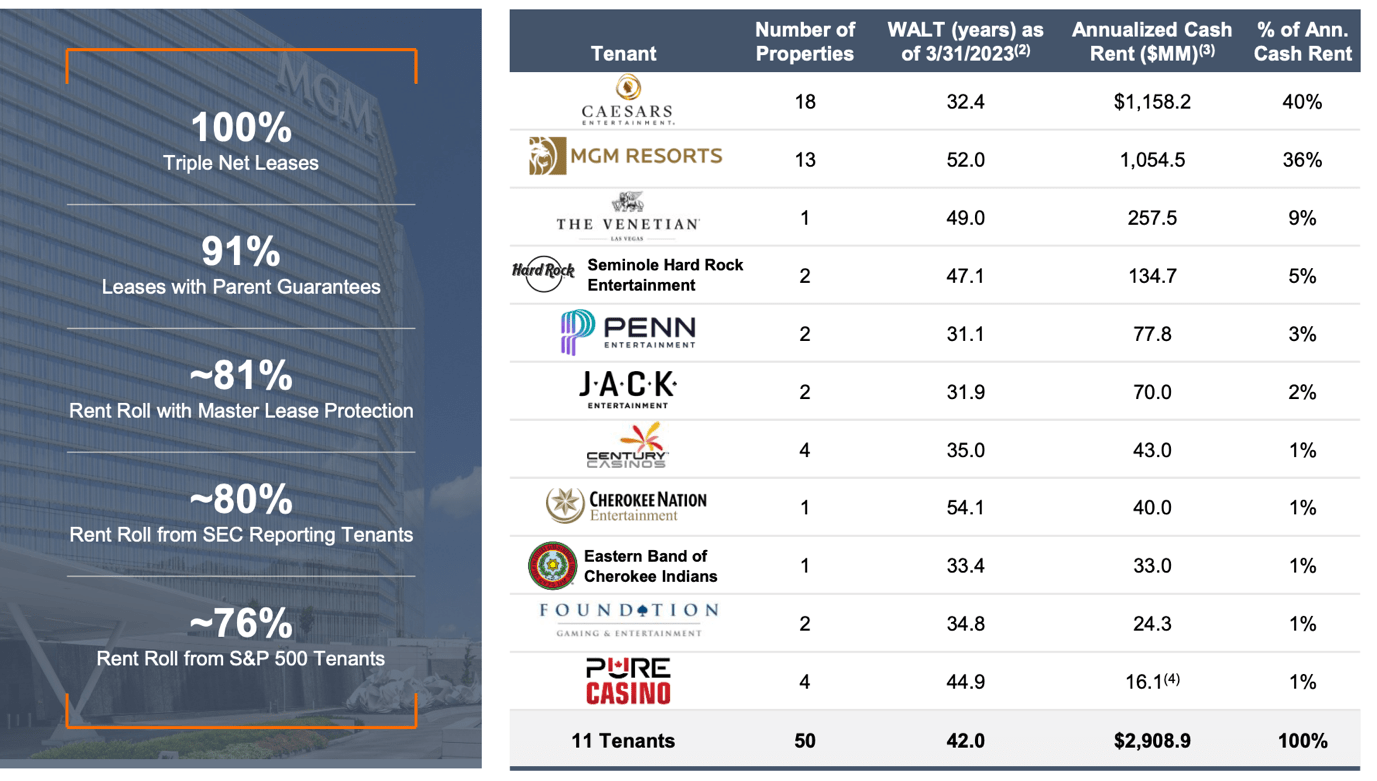

What makes VICI so special is that it owns irreplicable assets in an industry with a high barrier to entry. Roughly half of its rents come from Las Vegas, where it owns some of the greatest assets, including Mandalay Bay, Park MGM, Luxor, MGM Grand, The Venetian, and the Mirage.

{kind=link}

While this means that it has a concentrated tenant base, there’s little to worry about as Caesars and MGM Resorts depend on these buildings. These buildings aren’t just tools to allow them to do business but the reason why people visit their facilities in the first place.

These properties also come with 100% occupancy and multi-decade lease deals that include favorable inflation protection.

{kind=link}

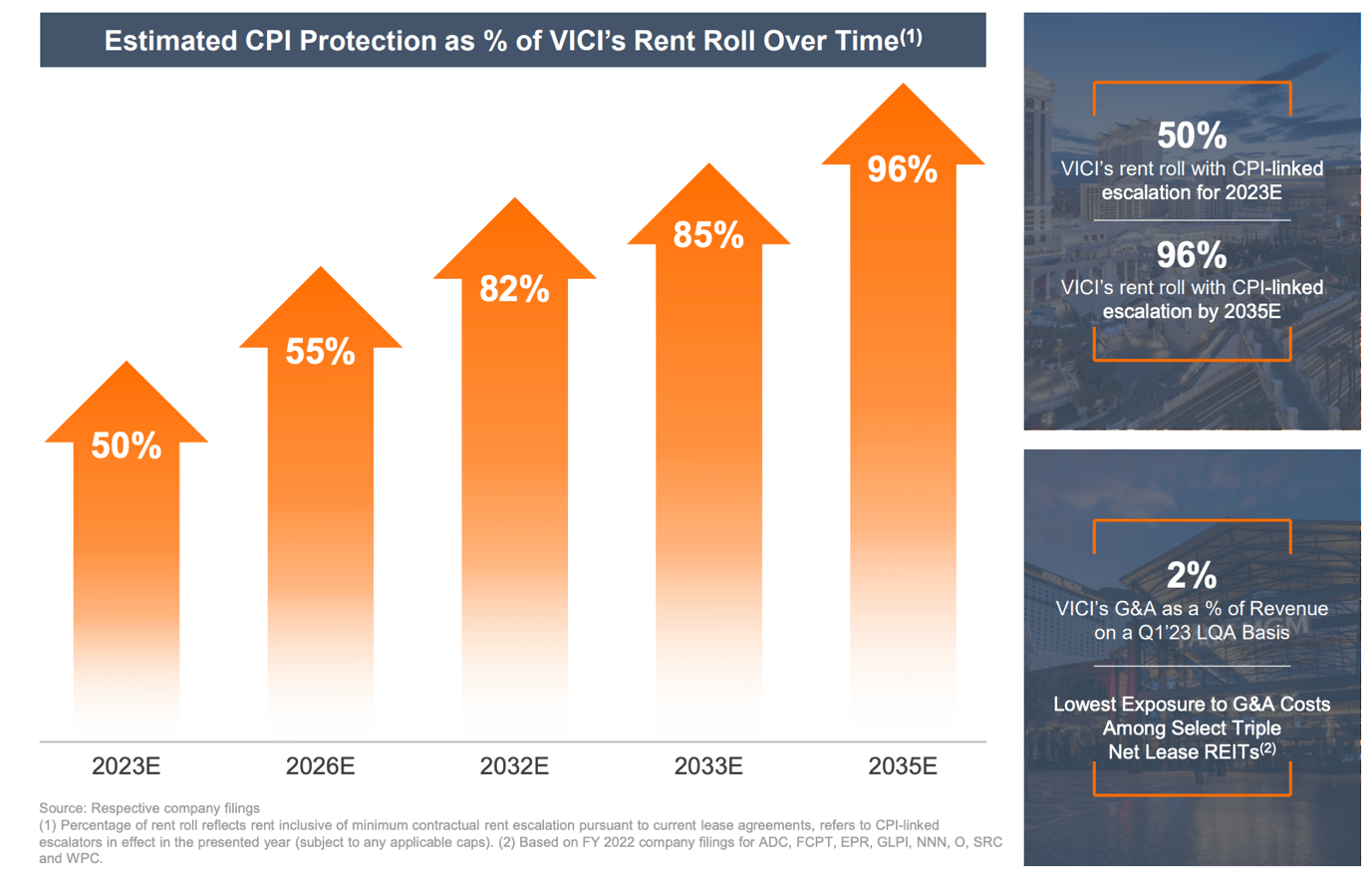

Furthermore, the company’s triple-net lease comes with more benefits. It has extremely low cash flow volatility (so far, none due to 100% rent collection). It also has non-commoditized assets that are irreplaceable. With regard to inflation, VICI has protected almost every penny of rent income against inflation.

{kind=link}

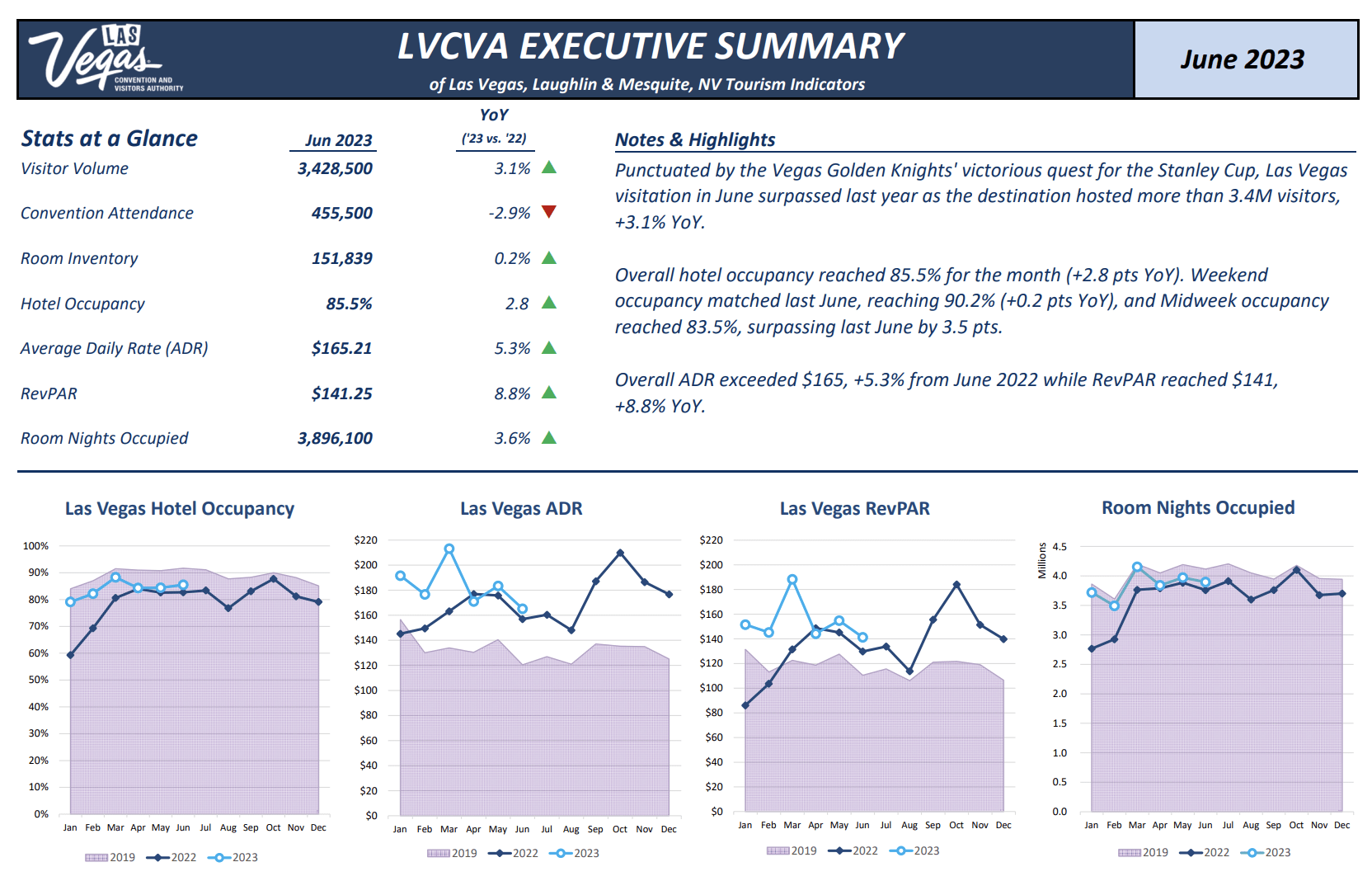

Having said that, Vegas is as strong as ever. In its 2Q23 earnings call, the company noted that Las Vegas reported all-time high margins and results, along with record traffic, which demonstrates the resilience of the sector.

Looking at official Las Vegas numbers, we see that while occupancy rates are slightly lower compared to 2019, ADR and RevPAR are well-above pre-pandemic levels.

{kind=link}

On top of owning gaming assets in Vegas and beyond, the company is expanding into non-gaming areas.

One of the things we recently discussed with the CEO is the Canyon Ranch deal, which adds top-tier wellness assets to its portfolio.

Canyon Ranch, with nearly 45 years of operating history, caters to high-net-worth clients who actively invest in medical and holistic life enhancement experiences. Despite having only two established destination resort locations, the company is well-positioned for significant expansion both domestically and internationally.

{kind=link}

The conversion of conventional resorts into Canyon Ranch Resorts is expected to bring transformative potential due to the unique economic model of maximizing guest experiences and revenue intensity.

During the 2Q23 earnings call, VICI reaffirmed its commitment to provide up to $200 million in development funding for Canyon Ranch Austin. This new resort is set to open between 2025 and 2026, with VICI having a call right to own the real estate upon completion.

In other words, it’s a win-win for both Canyon Ranch and VICI. One gets to expand more rapidly, while the other gets to own the assets, building a more diversified income base for its investors.

Having said that, VICI yields 5.2%. It’s a quarterly payer with a 72% AFFO payout ratio, using 2023 guidance.

Seeking Alpha

The company also enjoys a stellar balance sheet.

At the end of the second quarter, VICI had roughly $4 billion in total liquidity, and efforts were being made to enhance credit ratings and reduce the cost of capital. VICI's leverage stood at 5.6x net debt to annualized adjusted EBITDA. The company has a BBB- credit rating, which I expect to be upgraded to BBB+ within 2-3 years.

VICI also updated its AFFO guidance for 2023, expecting between $2.11 and $2.14 per diluted common share, reflecting a 10% year-over-year increase. The guidance excluded potential impact from unclosed transactions, interest income, acquisitions, dispositions, capital markets activity, and nonrecurring transactions.

{kind=link}

With regard to the valuation, the company is trading at 14x the midpoint of its AFFO guidance range, which is in line with the sector median.

I do not believe that VICI deserves to trade this low as it’s simply a better REIT.

The consensus price target of $38 reflects this. This price target is 28% above the current price.

We maintain a Buy rating.

Takeaway

The hotel REIT landscape has shown remarkable resilience despite the challenges of the pandemic and economic shifts. As the hospitality sector rebounds, two standout choices catch my attention.

Firstly, Apple Hospitality REIT emerges as a top performer. With its well-diversified portfolio, strong balance sheet, and strategic positioning in high-demand suburban markets, APLE displays its potential for outperformance. APLE's post-pandemic dividend recovery, backed by solid fundamentals, offers a 6.6% yield, potentially growing to 8.3% as its recovery continues. This REIT's performance outpaces its peers, and while the industry poses risks, APLE shines with juicy income potential.

Secondly, VICI Properties stands out due to its irreplicable asset portfolio, notably in Las Vegas. The company's foray into non-gaming sectors and its Canyon Ranch expansion adds diversity to its income stream. With a well-maintained balance sheet and a yield of 5.2%, VICI's potential for growth and stability makes it a compelling choice.

In navigating the hotel REIT landscape, these two options present themselves as solid contenders for investors seeking income and long-term returns. While risks persist, the future looks promising for these carefully chosen hospitality investments.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Juicy Income With These 2 Hotel REITs