JBAXY - Julius Baer: Benefiting From Credit Suisse Turmoil But Fairly Valued

2023-08-14 10:42:28 ET

Summary

- Julius Baer Group is known for its discretion and lack of scandal compared to its peers in the Swiss financial industry.

- By catering to ultra-wealthy clients, Julius Baer has seen steady growth in AUM and profits.

- Looking ahead, Julius Baer may gain market share as Credit Suisse / UBS may see client attrition through their merger.

- I would look to add shares of Julius Baer on any market pullbacks.

Within the ranks of Swiss financial institutions, I believe the Julius Bär Gruppe AG ( JBAXY ) - referred to as Julius Baer Group in the rest of this article - stands out for its discretion and relative lack of scandal compared to its peers.

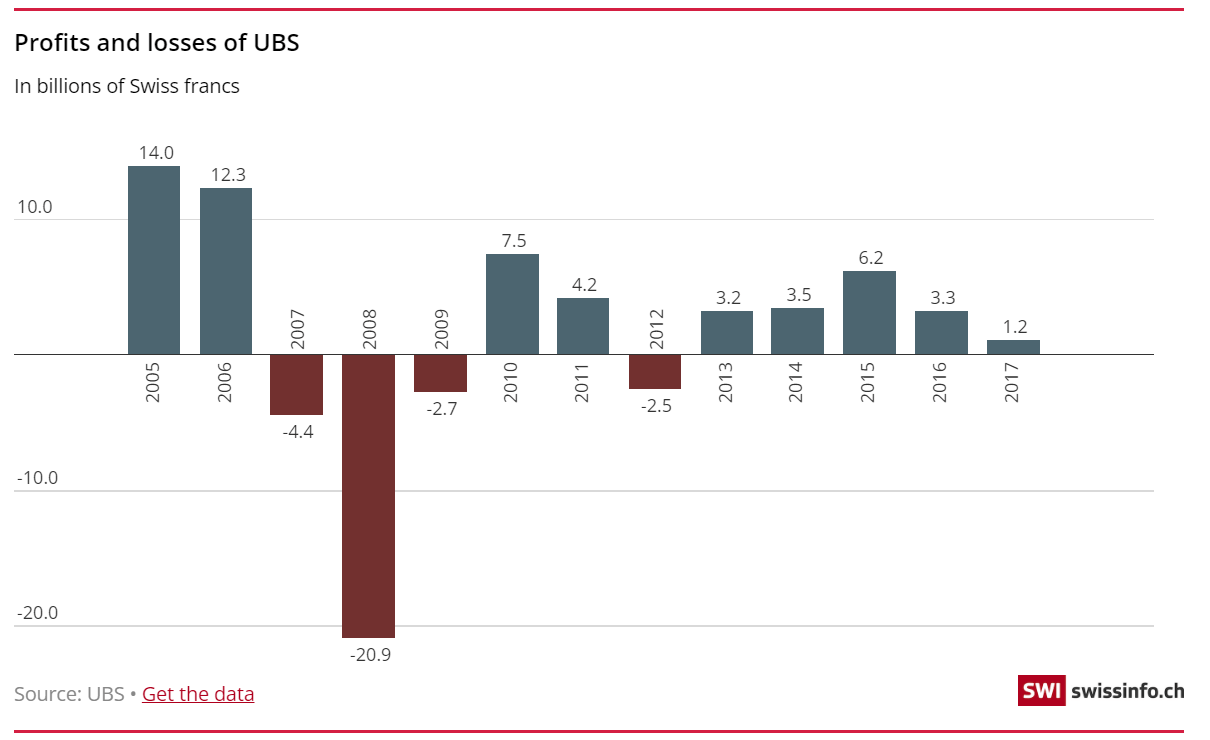

For example, UBS Group AG ( UBS ), its largest Swiss competitor, expanded heavily in the U.S. in the early 2000s and almost faced insolvency during the Great Financial Crisis, recording a record 20.9 billion CHF loss in 2008 on sub-prime mortgages and related losses (Figure 1).

Figure 1 - UBS suffered large losses during GFC (swissinfo.ch)

{kind=link}

If the Swiss government and the Swiss National Bank ("SNB") had not stepped in to create a 'bad bank' for UBS transfer illiquid securities to, UBS would surely have failed in my opinion.

UBS followed the near death experience with a tax-evasion scandal in 2009 that resulted in a $780 million fine, as well as a rogue trader scandal in 2011 that lost the bank $2.3 billion.

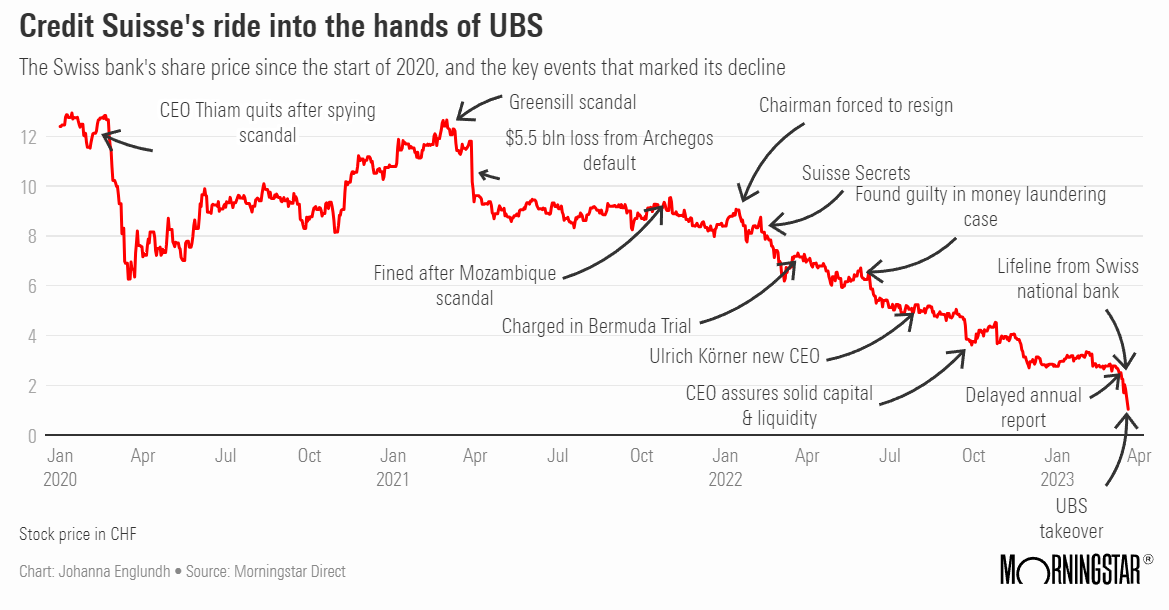

Similarly, Credit Suisse ( CS ), the other Swiss banking giant, was involved in its own string of scandals including former CEO Thiam allegedly spying on his former employees, the Greensill scandal in 2021, a $5.5 billion loss from Archegos, and most recently, near insolvency and a forced marriage with UBS (Figure 2).

Figure 2 - Timeline of Credit Suisse scandals (morningstar.hk)

{kind=link}

In contrast, a google search of 'Julius Baer scandal' returns few results, with the most prominent being a $36 million FIFA money laundering scandal in 2021. Julius Baer was also involved in a 2015 tax-evasion scandal in the U.S. for which the bank paid a fairly significant settlement without admitting guilt.

With a history spanning over a century, Julius Baer has carved a distinct niche for itself in the world of private banking and wealth management for the ultra-wealthy.

Company Overview

Julius Baer's business model is relatively simple. It is a pure wealth manager serving ultra-wealthy clients (to open an account with Julius Baer, clients must have a minimum account balance of $1.2 million USD). The absence of potentially conflicting lines of business like investment banking and trading reinforces Julius Baer's focus on providing top-tier wealth management services.

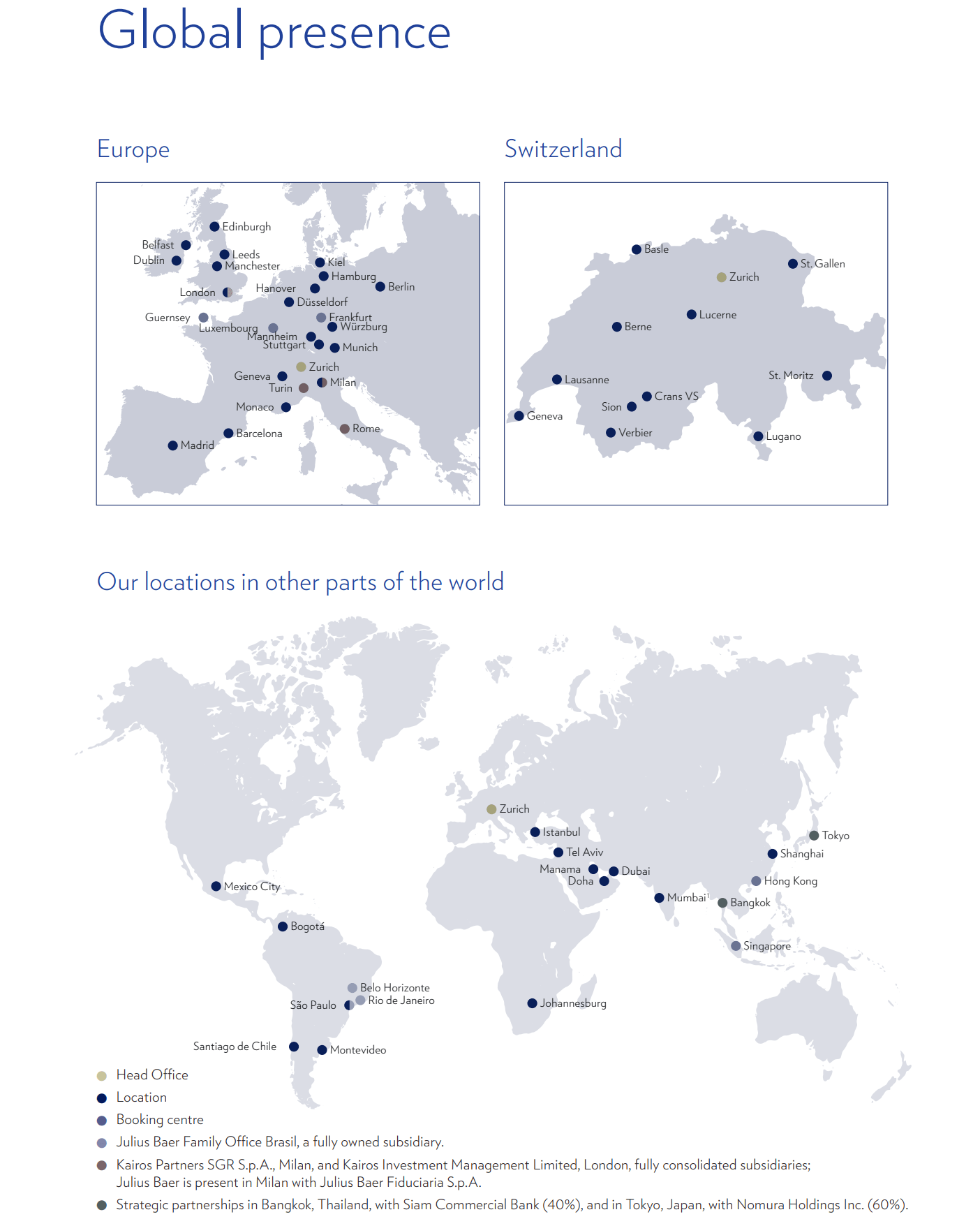

With a presence in over 25 countries and a network of offices spanning Europe, Asia, and South America (Julius Baer is notably absent from North America, having exited in 2004), the bank has positioned itself as an international player in wealth management (Figure 3).

Figure 3 - Julius Baer has offices in 25 countries (Julius Baer annual report)

{kind=link}

Julius Baer's geographical diversification not only enables the bank to tap into the ultra-wealthy in various regional markets, but it also provides the bank a hedge against local economic downturns.

Wealth Focus Drives Steady Performance

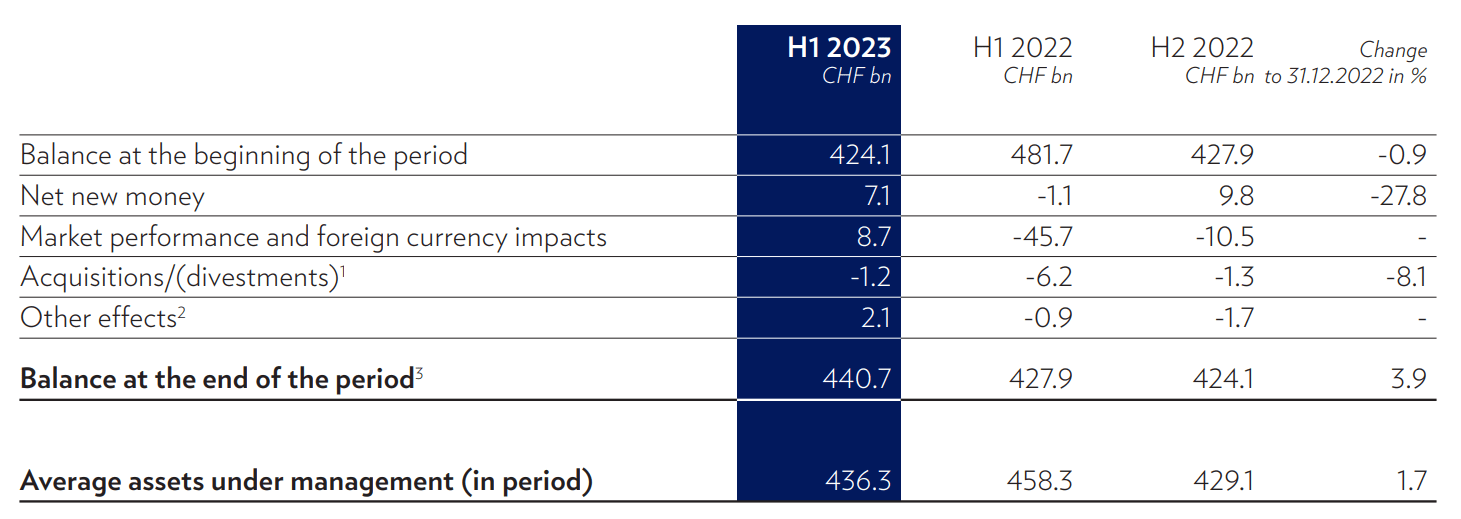

As of June 30, 2023, Julius Baer had 441 billion CHF in assets under management ("AUM"), a 3.9% increase YoY despite challenging market conditions in 2022 (Figure 4).

Figure 4 - Julius Baer AUM (Julius Baer investor presentation)

{kind=link}

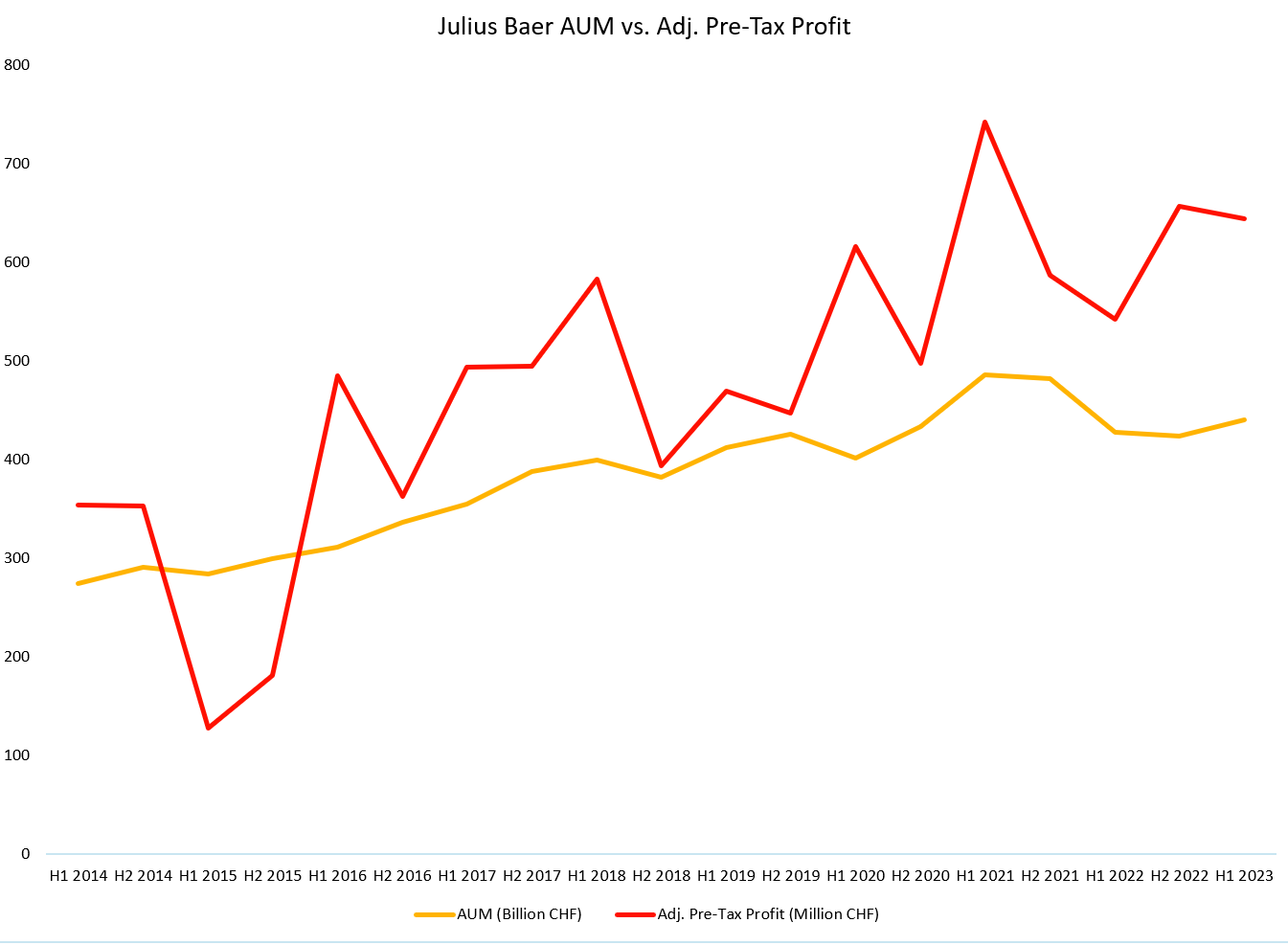

In fact, since 2014, Julius Baer's AUM has grown at a 5.4% CAGR from 274 to 441 Billion CHF (Figure 5). This steady increase in AUM has allowed to bank to increase adj. pre-tax profits from 354 Million CHF in H1/2014 to 644 Million CHF in H1/2023, a 6.9% CAGR.

Figure 5 - Julius Baer AUM and adj. pre-tax profits (Author created with data from company reports)

{kind=link}

Julius Baer currently employs 1,305 client-facing relationship managers ("RM") to manage the 441 billion CHF in AUM, or an average of 338 million CHF per RM. Assets per RM have also grown, from 225 million CHF in 2014 to 338 million currently, indicating the bank's growth has been mostly organic, with RMs either gaining new clients or deepening relationships with existing clients to manage more of their wealth.

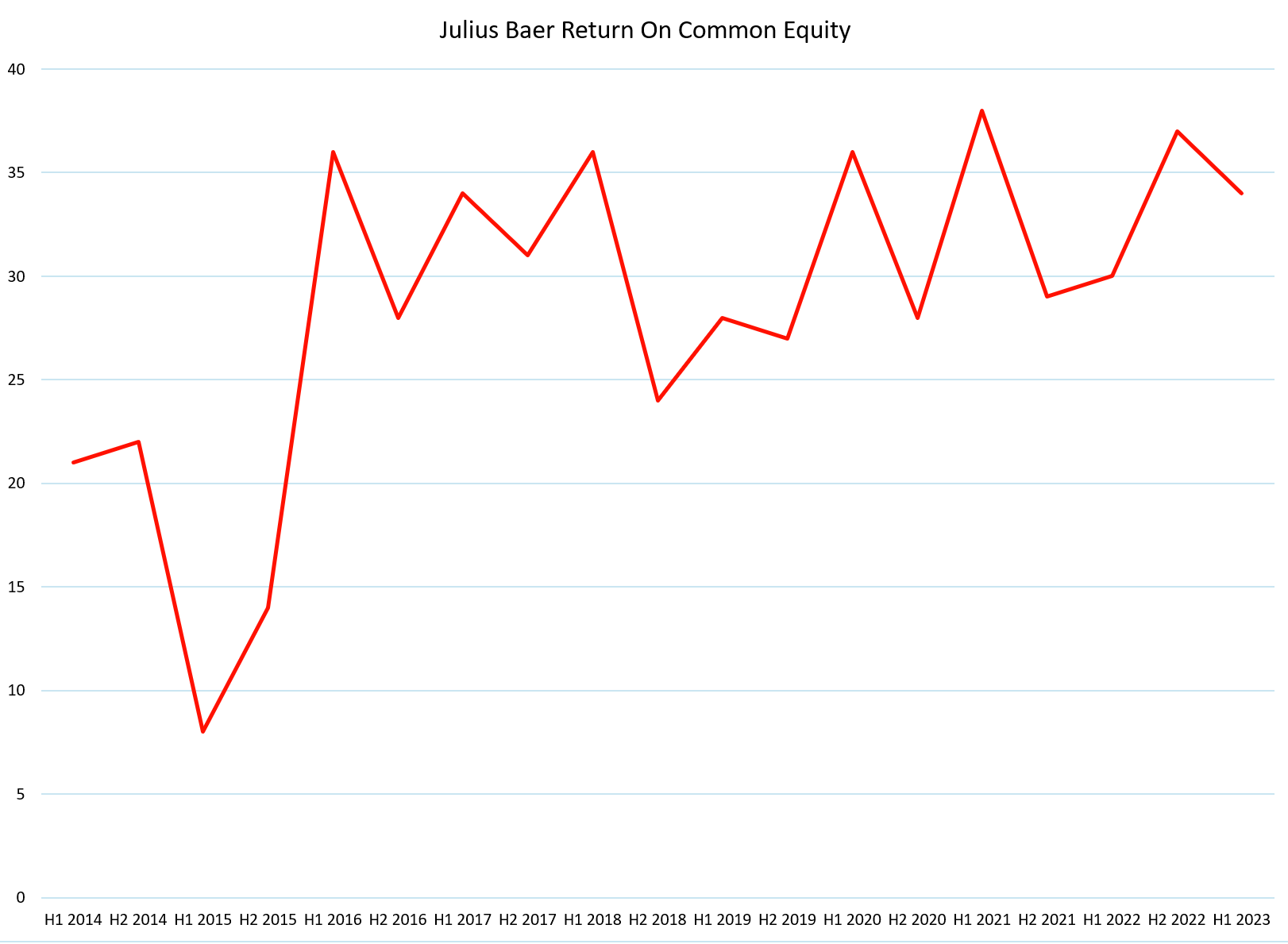

Aside from a brief period in 2015 when the bank booked charges due to the settlement of a U.S. tax-evasion probe mentioned above, Julius Baer has been delivering exceptional returns on common equity for shareholders, ranging from 20 to 35% (Figure 6).

Figure 6 - Julius Baer has been delivering strong ROE (Author created with data from company reports)

{kind=link}

Catering To The Rich Is Good Business

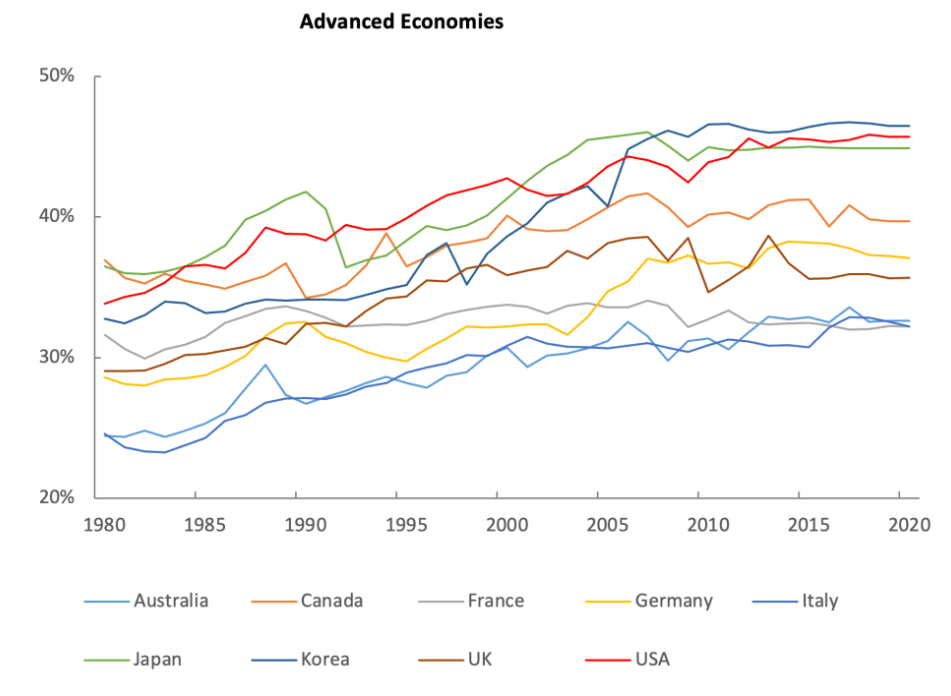

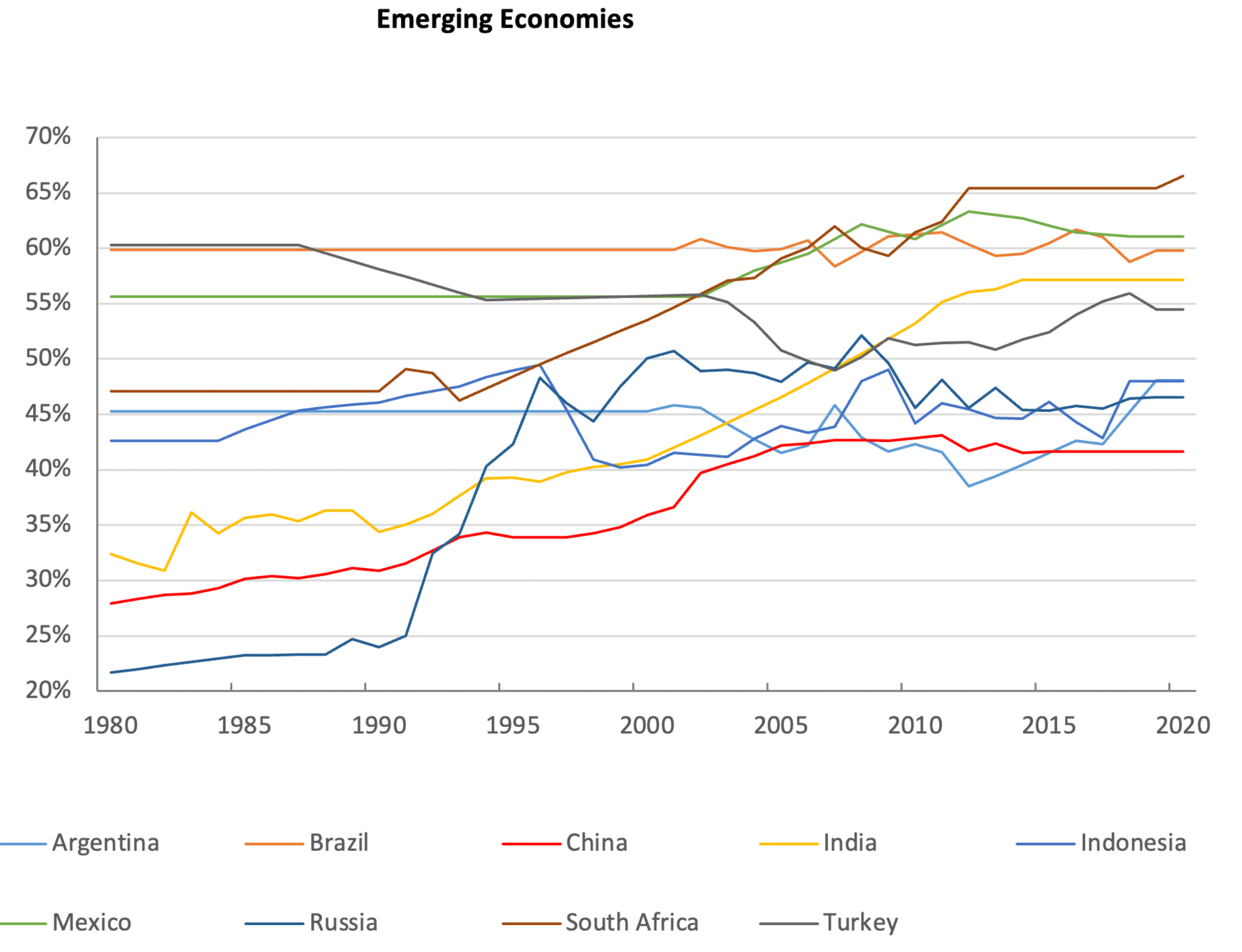

Given the continued growth in the income share of the world's wealthy, businesses like Julius Baer that cater to the ultra-wealthy should continue to enjoy favorable tailwinds. According to the Brookings Institute , the richest 10% have seen their share of income increase across both advanced economies (Figure 7) and emerging economies (Figure 8) in the past four decades .

Figure 7 - Richest 10% have seen rising income share in advanced economies... (Brookings Institute)

{kind=link}

{kind=link}

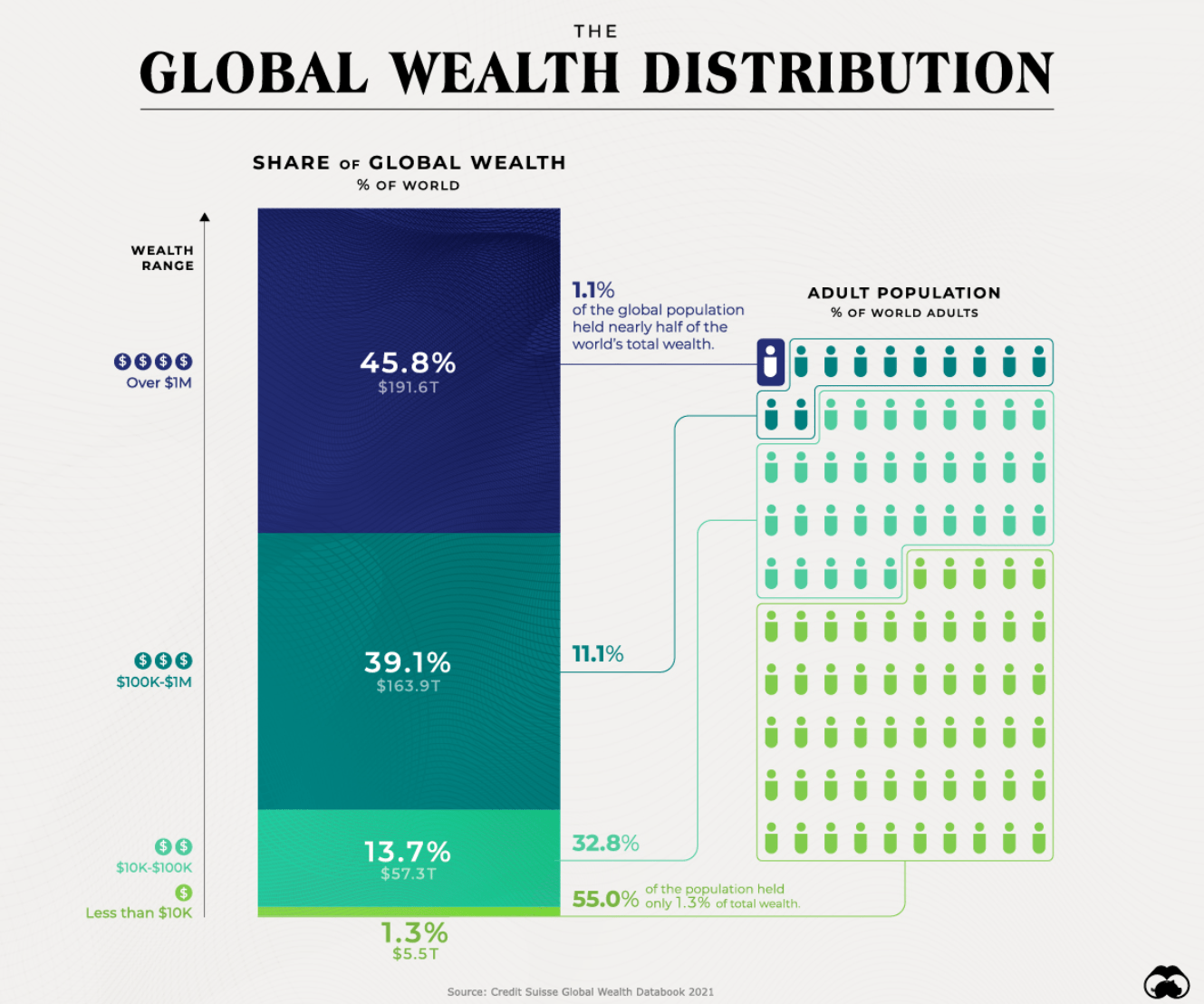

According to Credit Suisse's research, 1.1% of the global population controlled nearly half of the world's wealth (Figure 9).

Figure 9 - 1.1% of the world's population control nearly half of the world's wealth (visual capitalist)

{kind=link}

Credit Suisse / UBS Merger Creates Opportunity For Julius Baer

As mentioned above, in recent months, the global wealth management industry has been thrown into a bit of a flux following the near collapse of Credit Suisse and its subsequent shotgun marriage to UBS. For context, UBS and Credit Suisse are widely considered as the #1 and #2 players in the wealth management industry globally, so any reputational damage opens the door for more nimble players like Julius Baer to take market share.

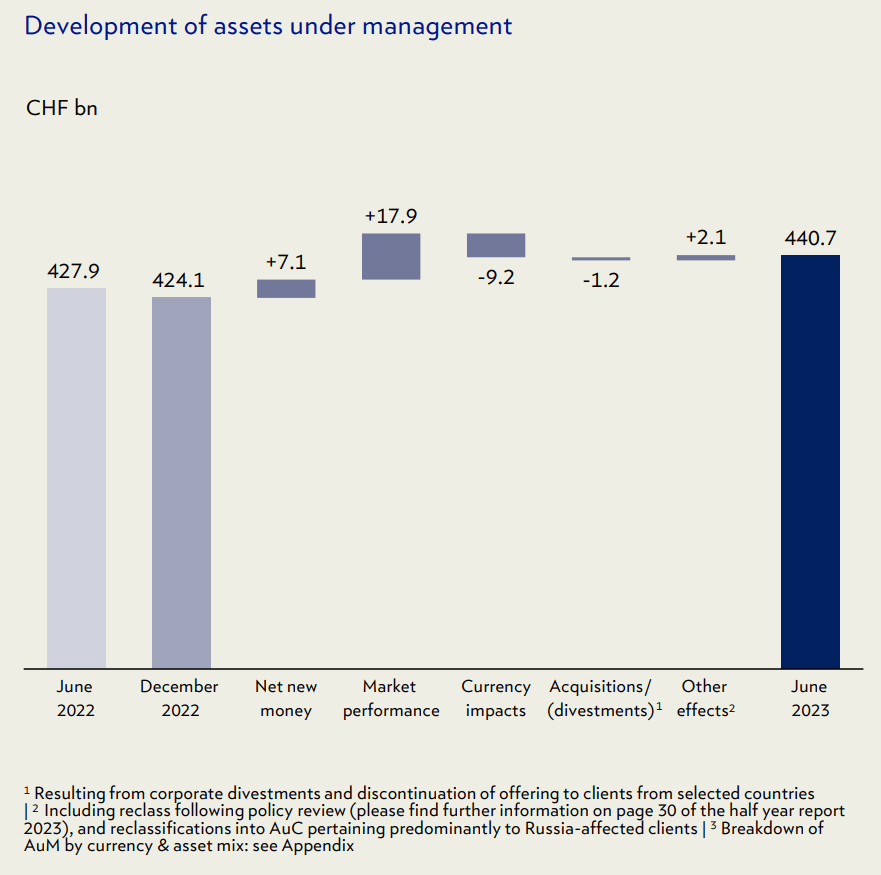

In the most recent semi-annual report, Julius Baer reported that the bank has seen 7.1 billion CHF in net new money from clients as Julius Baer added 57 RMs, many of whom come from rivals UBS and Credit Suisse (Figure 10).

Figure 10 - Julius Baer saw net inflows in AUM (Company reports)

{kind=link}

The CEO of Julius Baer expects the knock-on effects of the Credit Suisse crisis to continue for the next few years, as there is typically a time-lag between RM hires and assets under management.

Fairly Valued Low-Risk Business Model

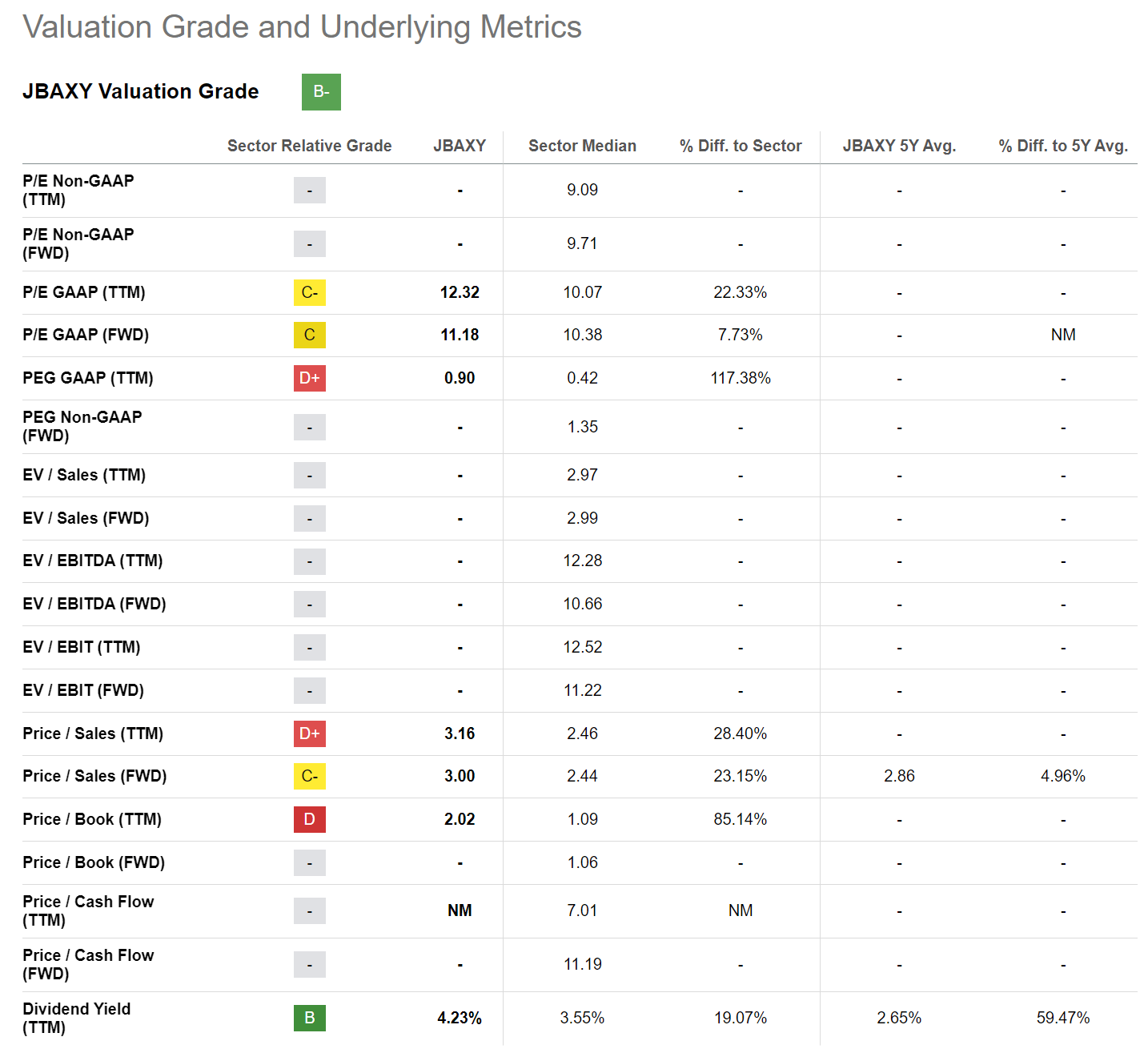

Julius Baer currently trades at a 11.2x Fwd GAAP P/E ratio, a slight premium compared to 10.4x for the Financials sector (Figure 11). Julius Baer stock also pays a 4.2% dividend yield compared to 3.6% for the sector median.

{kind=link}

Unlike traditional banking that has cyclical exposure from loan losses, providing wealth management services is more defensive and should command a premium multiple.

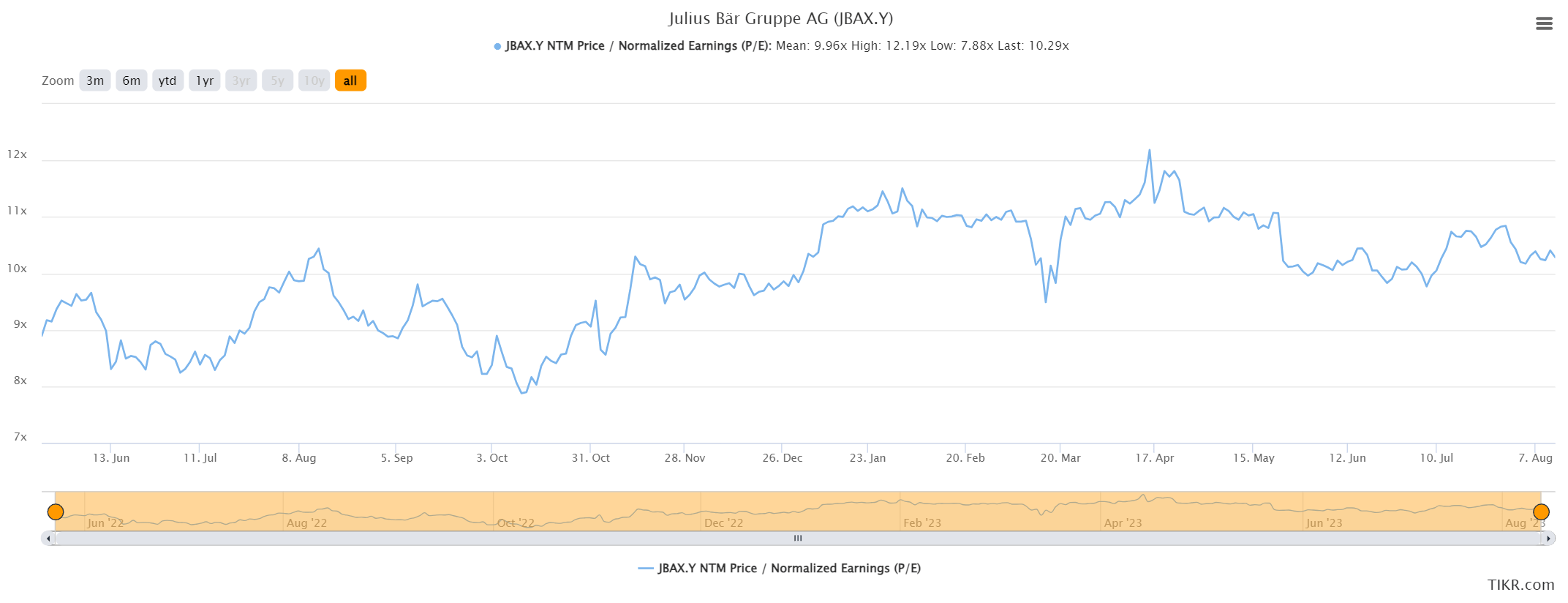

Overall, I believe Julius Baer is fairly valued currently and would look to accumulate shares if it trades towards the low-end of the historical 8 to 12x Fwd P/E range (Figure 12).

Figure 12 - Julius Baer historical Fwd P/E multiple range (tikr.com)

{kind=link}

Risks To Julius Baer

The biggest risk to a wealth manager like Julius Baer is a market crash that reduces the market value of its clients' assets and thus the fees that can be earned on those assets. For example, the market swoon in H1/2022 reduced AUM for Julius Baer by 9.5% (Figure 4 above). However, over the long-run, assets tend to appreciate, providing long-term tailwinds for wealth managers like Julius Baer.

Private banks like Julius Baer also have reputational risk from major scandals as wealthy clients do not want to be associated with scandal-ridden banks. Luckily, Julius Baer seems to be able to keep its name out of the headlines most of the time, unlike its Swiss competitors Credit Suisse and UBS.

Conclusion

Julius Baer is a high quality wealth management company solely focused on providing top-tier service to its ultra-wealthy clients. The bank has enjoyed steady growth and performance in the past decade by catering to the ultra-wealthy as they continue to gain income share. Looking ahead, Julius Baer may gain market share as its scandal ridden competitors may see client and asset attrition through their government mandated merger.

Julius Baer's stock is currently fairly valued, trading at 11.2x Fwd P/E with a 4.2% dividend yield. I would look to accumulate shares if it trades towards the low end of its 8-12x Fwd P/E range.

For further details see:

Julius Baer: Benefiting From Credit Suisse Turmoil But Fairly Valued