VTI - July CPI Report: Where Prices Are Rising What It Means For Fed Rate Policy

2023-08-10 09:50:19 ET

Summary

- The consumer price index rose 0.2% in July and was up 3.2% from one year ago, in line with expectations.

- Excluding food and energy, core CPI increased 4.7% YOY, a slight cooling from June and lower than expected.

- The shelter component remains sticky, but the softening in the index is likely to further accelerate through the remaining months of the year.

- Though the report largely met expectations, key categories are still running higher than desired. This increases the likelihood of at least one more Fed rate hike in September.

The July CPI report met expectations. This may raise the confidence level of those that see no further rate hikes from the Federal Reserve ("Fed"). The details of the report, however, suggest it's still too early to get overly comfortable.

July CPI Headline Inflation Rate

The consumer price index climbed 3.2% in July from a year earlier, the Labor Department said Thursday. While this was up from last month's 3% rise, June's drop largely reflected favorable YOY comparisons. Since June 2022's inflation rate of 9.1% marked a peak, the comparisons in the second half of 2023 should invariably turn less favorable. July's reading was indicative of this.

For the month, CPI rose 0.2%, in line with expectations. Core CPI, which excludes volatile food and energy prices, was up 4.7% YOY in July, down from 4.8% reported in June and lower than the 4.8% expected . The three-month annualized core rate is now about 3.1%, which is the lowest reading since March 2021.

Market Reaction To July CPI Report

Stocks rose in the pre-market hours immediately following the release. Both the Dow (DJI) and the Nasdaq (NDX) climbed over 100 points, while the S&P 500 (SP500) was up to a lesser extent. Bond yields moved lower, with the 10-YR note (US10Y) falling to 3.993% from 4.011% the day prior.

Drivers Of Inflation In July

Following a notable decline in May, energy prices began to climb in June, rising 0.6% on the month. Since then, benchmark crude prices have increased nearly 20%. Little surprise, then, that energy was up again in July. But its muted rise of just 0.1% may not have been expected.

But given that the index is an average over the course of the month, it's likely the full effect of the recent increases will be felt next month in August. Even with the recent increases, however, prices are still down 12.5% over the last twelve months.

The YOY declines in the energy component are continuing to have a favorable impact on ancillary categories, such as airfare. In July, airfares were again down 8.1% after declining by the same percentage in June. The category continues to be down double-digits on a YOY basis. Prices for car and truck rentals are also down in the upper single-digit percentage range, certainly good news for travelers.

But continuing to offset this benefit in the transportation category are vehicle ownership-related costs, such as maintenance/repairs and insurance. The two, together, were up 3% on the month and are up 12.7% and 17.8%, respectively, YOY. The increases here are the primary reason the overall transportation services line item remains stickier than other categories.

Food prices have also resumed an upward march in July. Both the food at home and away indexes increased by 0.2% in July. Among the six major grocery store categories, increases were seen in four, with prices for beef leading the way, up 2.4%.

Another slow-moving category is shelter. In July, the index was up 7.7% YOY. It was also the largest contributor to the monthly overall increase, accounting for 90% of the increase. Despite the increase, the trend in the index is promising. July's increase, for example, marked the fourth straight month of deceleration in the index.

One can also utilize Zillow's ( Z ) observed asking rents report as a leading indicator and can reasonably infer that the index will be significantly lower toward the end of 2023. In fact, research from the Federal Reserve Bank of San Francisco also noted that the YOY headline shelter rate could even turn negative by mid-2024. This should bode well for the overall inflation rate, given shelter's outsized contribution to the index.

The continuing pullback in the shelter component should favorably supplement declines seen elsewhere. The price of both used and new vehicles, for example, declined in July, with a more notable drop in used prices of 1.3% in the month. Over the last twelve months, used prices are now down 5.6%.

What Does The July Inflation Report Mean For The Economy?

Inflationary pressures are receding in many categories. But they either remain too high or are increasing in key line items. This week, Fed governor, Michelle Bowman, cited job growth and continued economic expansion as two factors justifying further increases in the federal funds rate. The rise in the energy component in July may validate this viewpoint.

Others feel differently. On Tuesday, Fed President of Philadelphia, Patrick Harker, stated that current policy appears to be at a point where they can hold on rates to allow for their past actions to work their way through the economy. This statement also assumed that there would be no "alarming new data" prior to their meeting in mid-September. The current reading may reinforce his current line of thinking. While certain categories, such as energy, are increasing, the overall index appears tame, especially given the continued strength in the U.S. economy.

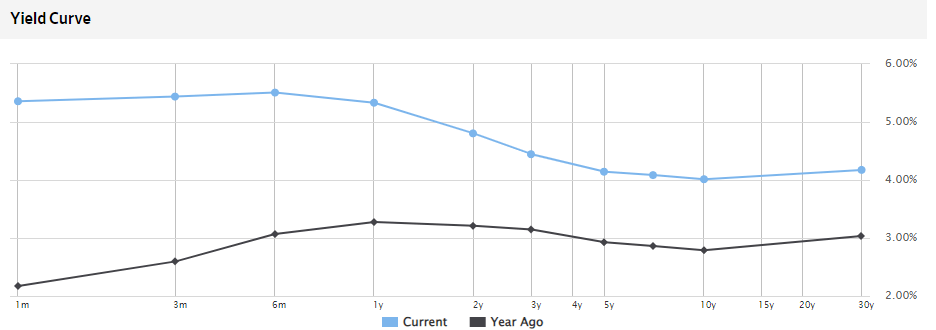

Bondholders appear to be placing more weight on Harker's views. The yield on the 10-year U.S. Treasury note, for example, fell following the July CPI release. But the yield is still hovering at elevated levels, near their 14-year high of 4.231% attained in October. With movement in shorter-term yields essentially unchanged, this indicates investors are betting that the Federal Reserve is nearly complete in their rate campaign. It also indicates investor confidence in a "soft landing."

WSJ - Current Yield Curve To Highlight Relationship Between Short & Long-Term Yields

{kind=link}

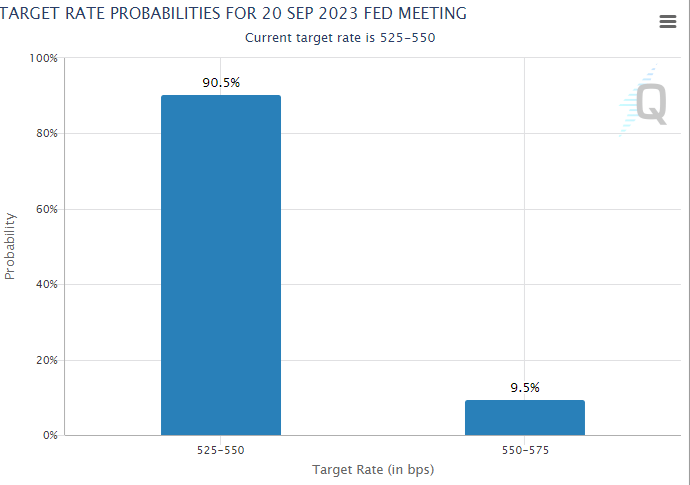

Overall, markets are now pricing in a 90% chance that the Fed will hold steady in September. Interest rate traders, too, are betting that the Fed holds still. And according to the CME FedWatch tool, there's a high likelihood that the federal funds rate will stay at 5.25% to 5.50% for the rest of the year.

CME FedWatch Tool - Target Rate Probabilities For Fed Rate Policy At September Meeting

{kind=link}

My Prediction

The Fed wants to reduce inflation to their 2% target without triggering a recession. A moderating rate of growth in most categories provides some degree of confidence that they can do so. But their efforts are contradicted by energy prices, which are on the rise in part because of investor optimism about the strength of the U.S. economy. This may lend support to at least one more rate increase in September.

Policymakers do have the luxury of additional economic data, including another CPI reading, before their decision is due for release. But I view any material change in the economic indicators between now and then as unlikely. If anything, additional data is more likely to come out in support of at least one more increase. Expectations are high that the Fed will hold steady. Overconfidence, however, may prove ill-fated.

For further details see:

July CPI Report: Where Prices Are Rising, What It Means For Fed Rate Policy