DIA - July Labor Report Preview: The Soft-Landing Narrative In Limbo

2023-08-01 09:13:52 ET

Summary

- Fed Chair Powell revealed a possible path to the soft-landing scenario at the July FOMC press conference.

- However, the soft-landing scenario contradicts the Phillips curve theory, and the Fed still projects an increase in unemployment despite a worker shortage.

- The stock market is priced for above average growth, not just a soft landing, it's completely disconnected from reality.

- July labor report expected to paint the goldilocks, but even this is likely to cause the Fed to hike in September.

The soft-landing narrative

The Fed Chair Powell said during the post FOMC press conference that: 1) the Fed staff does not predict a recession anymore; and 2) the Fed could start cutting interest rates before core inflation returns to the 2% target. These statements support the soft-landing scenario, whereby the Fed starts cutting interest rates before a recession, which actually avoids a recession.

The key assumption of the soft-landing scenario is that inflation would continue falling, while the labor market remains resilient. This contradicts a well-established theory called the Phillips curve, which predicts a tradeoff between unemployment rate and inflation. According to the Phillips curve, the unemployment rate must increase to cause lower inflation.

In fact, the Fed has been projecting an increase in the unemployment rate to 4.5% this year, which has been downgraded to 4.1% for 2023 and still kept at 4.5% for 2024. That means that over the next months, the Fed is projecting the job losses required to boost the unemployment rate from the current level of 3.6% to 4.1%.

But the U.S. economy is also facing a worker shortage, with nearly 10M job openings. Thus, given the low unemployment rate and severe workers shortage, the main upside risk to inflation is the wage-price spiral.

The soft-landing scenario assumes that the wage inflation would fall by simply reducing the number of job openings, without the need to increase the unemployment rate. In this situation, the Fed would be able to cut interest rates, despite the full employment.

Based on Powell's statements, it seems like the Fed sees a path towards the soft-landing, while still projecting an increase in the unemployment rate to 4.1% by the end of 2023.

The hard landing scenario is consistent with the Phillips curve - there needs to be a significant increase in the unemployment rate to put the inflation on track to reach the 2% target over time.

The July labor market data

JOLT Job Openings

The most important data point for the soft-landing narrative is thus the level of job openings. The chart below shows that job openings have been decreasing, but still remain well above the pre-pandemic levels.

JOLT Job Openings (Trading Economics)

{kind=link}

The expectations are that job openings would fall from 9.8M to 9.6M in July. At this pace, it would take about 15 months until the job openings drop to the pre-pandemic levels - which were still historically high.

Does this mean the Fed will need to keep the monetary policy tight for 15 months more (end of 2024) until the job openings return to the pre-pandemic levels, while the economy remains at full employment (no recession)?

If yes, is it reasonable to assume that the labor market would continue to be resilient for another 15 months of tight monetary policy? Very unlikely. The unemployment rate is likely to spike together with the decrease in the job openings, which makes the soft-landing scenario very unlikely.

This is especially true given the fact that over 40% of job openings are in the health and education sectors, and these will remain high due to structural demographic trends.

Initial Claims

Initial claims for unemployment are considered a leading indicator for the labor market. After spiking in late spring, the initial claims fell sharply during the summer, pointing to a strengthening labor market.

Few still talk about this, but we are currently at the peak Covid reopening. Last summer many were still wearing masks, and there were travel restrictions - remember Djokovic was not allowed to play the U.S. Open in 2022.

The consumer still has some covid-stimulus funds, and this summer everybody is freely traveling and consuming particularly on services. This is reflected in a strong labor market, particularly in the initial claims. My expectation is that the claims will spike in September after the summer vacations are finished.

{kind=link}

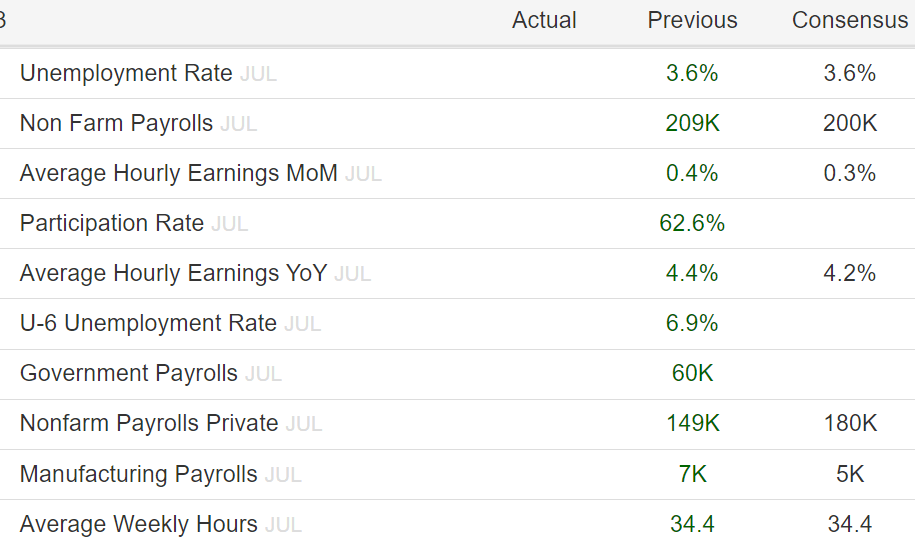

The Friday's Payrolls data for July

The payrolls data on Friday is expected to paint the goldilocks scenario. The headline payrolls number is expected to slightly dip to 200K, which is still a decent number, while the wage growth is also expected to dip to 4.2% YOY and 0.3% MOM. So, still solid jobs number, with falling inflation.

{kind=link}

To put it all together, the July labor market data is expected to show that the U.S. economy is still at full employment, with decent job creation, and falling wage growth. Goldilocks.

But the stakes are getting higher

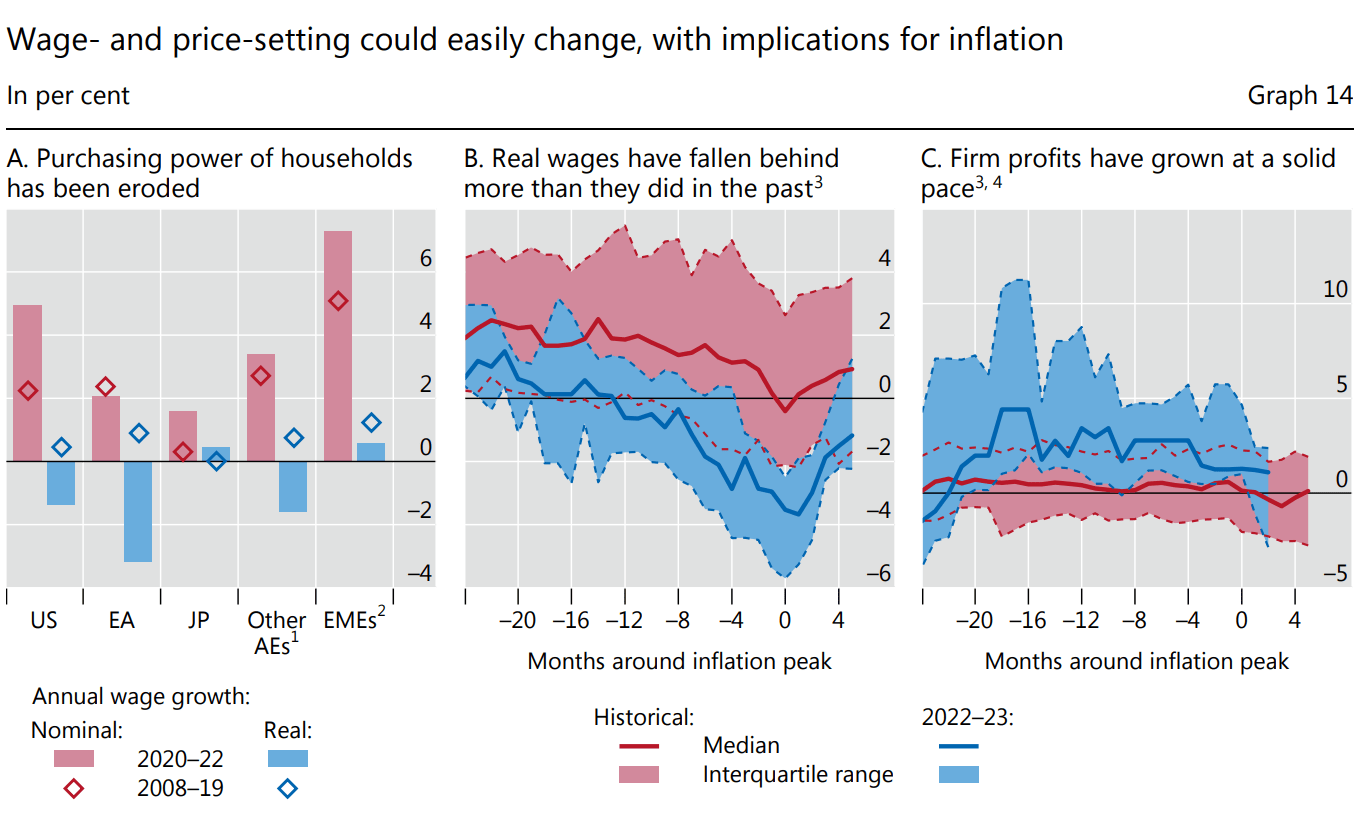

But unfortunately, these conditions do not favor the return to the 2% target over time - the job openings are still very high. Further, the wage growth data does not reflect the recent developments with labor strikes and union-negotiated wage increases.

Powell refused to address the question about the labor strikes at the FOMC press conference, but the BIS Report clearly points to the labor strikes as the main risk for the inflationary wage-price spiral, given that "real wages have fallen behind more than they did in the past."

{kind=link}

Thus, the Fed will not find comfort in these expected labor market numbers to stop the interest rate hikes, which makes it likely that the Fed will hike in September. Given that the Federal Funds rate at 5.36% is above the core inflation, every additional hike will carry much more weight on the markets, and significantly more tighten the monetary conditions.

Market implications

The labor market is strong, but we could be in a full-employment recession already. The recent data shows that Redbook retail sales have been negative in July YOY, and this happens only in recessions. Further, industrial production is negative YOY.

The stock market ( SP500 ) is fully embracing the soft-landing scenario, and analysts are very optimistic about the Q4 2023 earnings and especially the 2024 earnings. In fact, given the forward P/E ratio of 21, the S&P 500 is priced for the above trend growth, not just a soft-landing with a below trend growth.

The soft-landing narrative is flawed and very unlikely, the unemployment rate will likely have to spike, along with a drop in job openings. Further, the key consumer (weekly retail sales) and business data (industrial production) are already pointing to a recession. Yet, the conditions for the Fed to stop hiking are not there yet. That's a very bearish macro environment for stocks, especially given the valuations.

The labor shortage is not a reflection of a sustainable economic strength, it's a reflection of: 1) demographic trends (retiring baby boomers); 2) de-globalization (on-shoring, and tight immigration policy); and 3) the post-pandemic demand for services facilitated with the last drops of stimulus. Thus, the recent labor market strength does not reflect the economic reality, and neither does the stock market.

For further details see:

July Labor Report Preview: The Soft-Landing Narrative In Limbo