TKAYF - Just Eat Takeaway.com: European Segments Flourish But U.S. Remains A Drag

2023-10-25 07:56:37 ET

Summary

- Northern Europe and UK&IE return to positive GTV growth and provide strong adj. EBITDA generation.

- Grubhub remains an anchor on the stock and valuation with poor growth.

- Just Eat Takeaway.com is undervalued relative to European peers despite strong adj. EBITDA generation.

- JET FCF breakeven point accelerated to Q4 '23 compared to mid '24.

- Target Price of €22 based on terminal growth rate of 2% and WACC of 8.34%.

Editor's note: Seeking Alpha is proud to welcome Matthijs Kok as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Just Eat Takeaway (JTKWY) (TKAYF) is a mix of the good and the bad. A dragging Northern American segment is paired with the strong earnings potential of the Northern Europe and UK&IE segments. Whilst the past year results do not make for fantastic reading, there is plenty to be positive about. I have used conservative estimates. Were Just Eat Takeaway [JET] to underperform, then there is still a buffer offering some protection.

The opportunity for investors lies in the strong EBITDA generation at this current valuation. At €10.88 ($2.25 in OTC) a share implying a market cap of €2.4 billion, the current cash position and the EBITDA generation will repay that investment quickly. Investors searching for a growth company must look elsewhere, as the double digit growth seen during the pandemic is not likely to return any time soon.

The EBITDA generation is underpinned by the significant strides being made so that all segments are at a minimum FCF breakeven. Cost cutting via order pooling delivers consistent higher margins giving credibility to sustainable higher profitability. EBITDA generation is relatively secure as it occurs in markets where JET is the market leader making increased competition less of a factor. Food delivery markets are a winner takes all game. This can be highlighted by one quick look at the German market.

I rate Just Eat Takeaway a buy for its earnings potential in Northern Europe and UK&IE segments which covers the company's shortcomings in other areas. Target price set at €22.00 ($4.56 in OTC).

About Just Eat Takeaway

Just Eat Takeaway.com is a leading online food delivery marketplace in Europe, the USA, Canada, Australia and New Zealand. The company offers a mobile application for ordering and delivering of food, beverages, groceries and in future potentially tech products. As with other food delivery businesses, it profited from tailwinds due to the corona-pandemic, which significantly increased order volumes. A key distinction between JET and some of its peers which is often overlooked is that JET is not a pure play food logistics company. Whilst JET could do a better job communicating this fact, marketplace orders (orders on the platform but not delivered by JET) is a key profitable source for the company. At the turn of the decade JET had been aggressively expanding with ventures into Germany, UK&IE (successful) and the US (unsuccessful). Especially the latter has become an issue, with it being a drag on results. At the end of last year (2022), JET sold its iFood stake for €1.5 billion with a consideration of up to €300 million. This was a great price as it valued iFood at 4.5x-4.8x EV/Sales. For comparison it was the highest multiple in the sector beating out the profitable DoorDash at 3.98x at the time. This has been the only recent divestment thus far.

Business Model

JET business model can be divided up into two type of orders. Marketplace and logistic orders. Marketplace orders are far more profitable as no human capital is involved. JET naturally wants to increase the amount of restaurants/participants on their platform as this makes its proposition more attractive to customers. At the time of writing JET has 6 platforms , already down from 13 after the merger with Just Eat. The end goal is to have 1, which is almost the case in European segments.

What makes this business sector so enticing is the operational leverage that is possible. This operational leverage is due to a hard limit on marketing spend. A hypothetical example: if you could reach every Englishman 15 times a week on a budget of €100 million, there is very little gain to increase the budget to reach them 16 times. This creates a natural hard cap / saturation on marketing spend.

Initially growth comes from getting people onto your platform (market penetration), but in the long term, growth lies in an increase in order frequency from existing customers. Herein lies the leverage. The extra order frequency also results in further revenue and Gross Transactional Value (GTV) from which 80-90% profit can be garnered.

Most of the growth in revenue is generated by existing customers. This is the reason why we keep adding more restaurants and partners. This is what creates a moat compared to new competitors - Jitse Groen

In the future JET is looking to deliver more groceries but also tech products . Groen had initially said groceries on their own would not be profitable, but if they could be added to an order pool it could be. However, the margin on food items remains low. This is not the case for tech products. For example: an iPad being delivered to your house that has a €5 delivery fee represents a far lower percentage cost compared to groceries with such a fee. JET is currently exploring this GTV/revenue growth opportunity, but it is still in the pipeline as insurance and other risks need to be evaluated.

I think adding a higher cost items to the potential order pool is a good idea. It creates a strong revenue opportunity in a segment that is less price sensitive than food. JET can leverage its logistic network and if such high margin products can be added in, it is a no brainer. Furthermore it adds another source of customers. The only risk I foresee is that perhaps return order frequency may be very sporadic unlike with food. If it comes to fruition I will see it as another positive catalyst.

Industry

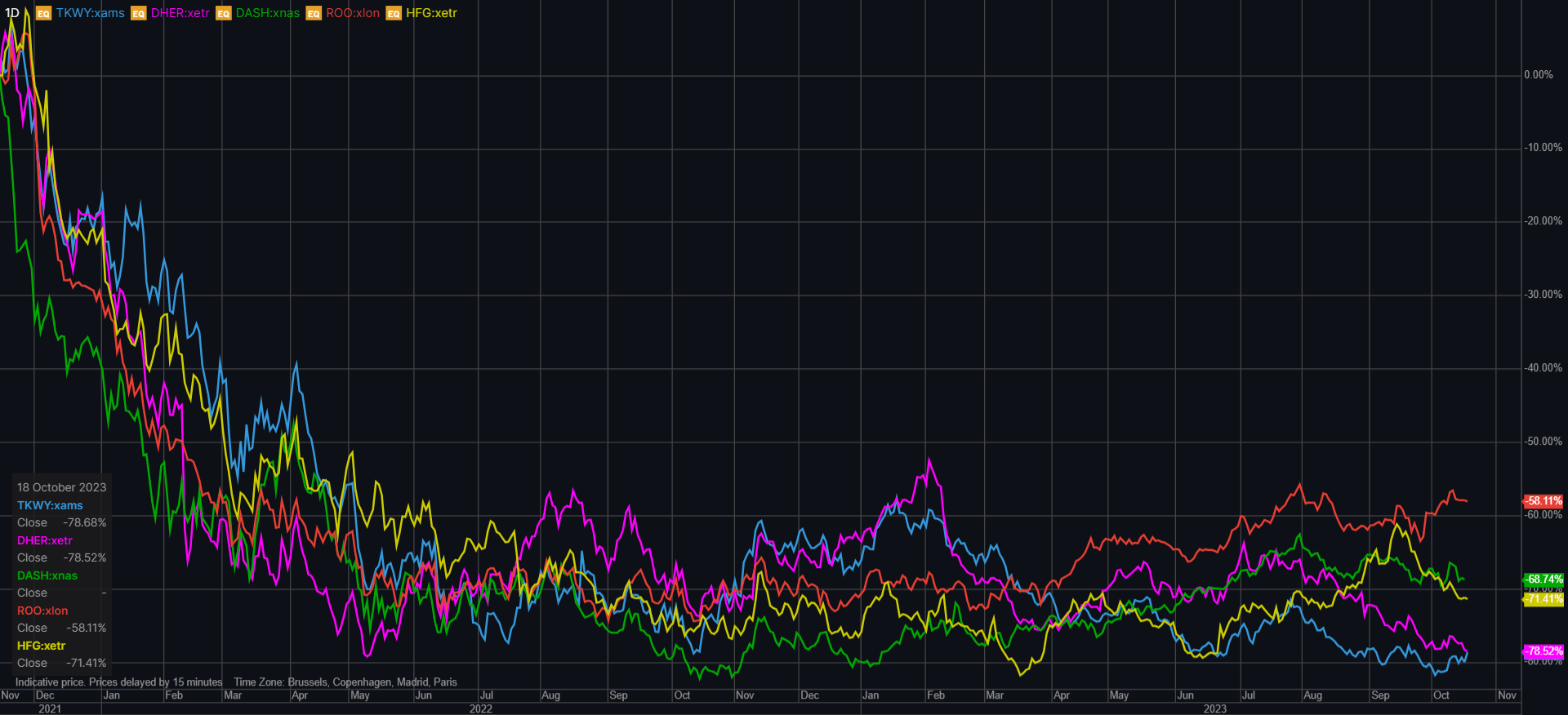

At the end of 2021 and start of 2022 concerns were starting to be raised over the profitability of the sector and if it would be viable without corona tailwinds. The increase in interest rates further enhanced the scrutiny on "growth at all costs" companies and valuations of these companies plummeted as shown below.

Devaluation of food delivery sector since Nov. '21 (Saxobank)

{kind=link}

US food delivery companies have shown to be able to make a profit, as has JET, but some other European players are struggling more. Laws in Europe have become a thorn in the side for many players. Freelancing/gig work has come under extra scrutiny with new laws and fines in Spain and Italy for example. This was not an issue for JET and hence it remains active in these markets where others have pulled out.

I believe the fall in valuation was justified. The pandemic may have given a far too optimistic view in terms of growth figures which were then extrapolated. The future promise of profits, which at the time seemed distant for most companies seemed an empty promise. I think companies will now be rewarded if they can show that their business model can be profitable. This can definitely be aided by further expected growth of the sector.

Globally the food delivery space is expected to grow at 12.78% CAGR through to 2027 according to Statista with the European market growing slightly slower at 12.31%. The US will grow even faster reaching a CAGR of 15.02%. Whilst growth in Europe is not slow, missing out on the faster growth in the US with a troubled Grubhub represents a missed opportunity.

Peers

The largest critique of JET is that the slowed/negative growth, especially this year, is not sector wide. Where JET has shown negative constant currency growth peers like Uber Eats and DoorDash show double digit growth (see below).

Uber Eats Q2 Results (Uber Q2 earnings release) DoorDash Q2 Results (DoorDash Q2 earnings release)

{kind=link}

Whilst performance in Europe seems in line with fellow European focussed food delivery companies Delivery Hero (DLVHF) and Deliveroo (DROOF), the discrepancy on the other side of the Atlantic is startling. Grubhub has lost 8% market share in two years and with the latest figures is not showing an uptick in form. Q3 '23 order growth was -13% compared to previous year compared to DoorDash's +25%. As an investor such figures usually point to an incredibly flawed product where it is being fully outcompeted.

Herein lies a key risk for JET. North America, which is mostly Grubhub, encompassed 46% of last year's revenue and 41% of GTV . A question that needs to be asked how much more investment would be required for Grubhub to shift the tide? And if JET just wants to sell Grubhub, are such negative growth figures going to make it all appealing despite the fact it could become profitable.

After the announcement of the acquisition I was enthusiastic about the venture, however the price was questionable. I had not foreseen the market share loss that has occurred. I would have expected it to remain more stable. My current view of Grubhub, is far more negative. As my title implies, it has become a large blemish on a successful company but due to its size completely overshadows such accomplishments. I believe it will require sizeable investment to regain such market share and I am a firm believer that the market leader will win in the long run. Hence I believe a sale would be the best option but who will buy it and at what price?

Third Quarter Trading Update

Just Eat Takeaway presented its third quarter trading update on the 18th of October 2023 along with an updated guidance. This is the second raised guidance of the year, which the company hopes will spark positive momentum. The raised guidance was expected as it was possible to be extrapolated from the H1 '23 figures. Based on historical figures Q3 is usually the worst quarter of the year as it encompasses most of summer in the Northern Hemisphere. Q4 is usually the best performing quarter for JET.

Key takeaways

- Free cash flow breakeven point pulled forward to H2-23 from mid-24

- Guidance for FY23 adj. EBITDA increased to €310 million from €275 million

- GTV growth returned in Northern Europe and UK&IE

- Constant currency GTV growth for FY23 between -3.5% and -4.5%

- New share buyback of €150 million (explained below)

Q3 Trading Update (Just Eat Takeaway)

I believe the raised guidance will not generate significant positive momentum. What makes me positive is the return of GTV growth in Northern Europe and the UK&IE. I explain why in the outlook and valuation section. The negative growth in orders in North America was larger than I expected and makes me worry about sales prospects. In Q4 it really needs to stop the decline to make it attractive at all to a potential investor.

Share Buybacks

JET has completed its first share buyback as of the 20th of September. In total 10.78 million shares were repurchased and in the conference call of the 18th of October, Groen said these would remain in treasury for now and have not been used in remuneration.

Just Eat Takeaway Buyback I (Just Eat Takeaway)

{kind=link}

Along with the third quarter trading update, a second share buyback was announced. In total €150 million in shares will be repurchased starting on the 18th of October. Based on the last close stock price on the 17th of October (€11.92) it would approximately be 5.7% of the issued shares. JET will hope to complete it by the 30th of September 2024.

I believe share buybacks are an attempt to give some return to shareholders. I understand the reasoning of using excess cash but I do not think there will be any positive momentum gained from it. The stock has fallen far too far to be seen as any compensation for long term shareholders.

Outlook & Valuation

The sale of iFood was well executed and brought some needed cash into the company. JET had gotten financing through convertible loans, with the expectation of share dilution rather than having to pay the principal back. Hence, additional cash was required and with the offer of 4.5x EV/sales for iFood, it was too good an opportunity to pass up. JET is now well capitalised for the future. While it may not have the financing powers of its American peers, it does not suffer from a capital shortfall for Europe due to the successful Northern Europe and UK&IE segments.

Catalysts

Now you should have a decent overview of the company and it is time to look at why this is an investment opportunity. As I mentioned previously, the focus is on Northern Europe and UK&IE. Below is the trajectory of the adjusted EBITDA per segment.

| Total |

| 419 |

| 528 |

| -141 |

| 240 |

| 509 |

| 716 |

| Adj. EBITDA in € millions |

| 2019A |

| 2020A |

| 2021A |

| 2022A |

| 2023E |

| 2024E |

| Northern Europe |

| 96 |

| 217 |

| 256 |

| 313 |

| 402 |

| 457 |

| UK & IE |

| 226 |

| 237 |

| -107 |

| 23 |

| 121 |

| 224 |

| North America |

| 106 |

| 166 |

| -28 |

| 65 |

| 101 |

| 140 |

| Southern Europe and ANZ |

| -9 |

| -92 |

| -262 |

| -161 |

| -115 |

| -52 |

Financial Estimates (Author)

Northern Europe

Northern Europe requires no additional investment to maintain its current market position. Market share is trending towards 40%, with the Netherlands (58%) and Germany (77%) particular strongholds . Hence there will be no drag down on the adj. EBITDA. For further growth in adj. EBITDA, penetration is the next step. The expected growth of the food delivery market will assist this. Furthermore, the improvements in order pooling have made this segment more lean. Despite orders falling 7% year on year, revenue looks to increase by 6.5% according to my estimates.

I expect adj. EBITDA to cross the €400 million mark this year growing further to €457 million in 2024 profiting from these gains in penetration.

Penetration of JET (FY 2022 Presentation JET)

{kind=link}

UK&IE

Where Northern Europe is looking for increased penetration, adj. EBITDA will be generated in the UK&IE segment through cost cutting. This segment was created from the merger of Just Eat and Takeaway.com in 2020. Then the pandemic arrived which dramatically increased order numbers from 190 million in 2020 to 277.1 million in 2022 . At the time because growth accelerated so rapidly, JET had three different logistics models to be able to capture this growth. This concluded the heavy investment phase in 2021 (reflected in the adj. EBITDA) and then started the path to profitability.

Herein lies the opportunity. The UK&IE has the hallmarks to become JET's strongest market. With strong penetration and market share, the basic fundamentals have been set and cost cutting will allow adj. EBITDA growth to be even quicker. This is reflected in my estimates with higher increases in adj. EBITDA for the UK&IE compared to the Northern Europe.

The three logistics models have been reduced to two and now JET will decrease the cost per order. Order pooling once again lies at the heart of this and will further reduce logistic costs.

North America

I have highlighted the issues with Grubhub but there is also potentially positive news. A gain of between $100-120 million in adj. EBITDA is possible due to fee caps being scrapped. Even without the fee caps Grubhub is approaching FCF breakeven.

The main positive catalyst would be if JET manage to sell Grubhub, but the fact it does not negatively affect adj. EBITDA can be seen as a small victory.

Overall

I believe that JET has the ability to generate €1.225 billion in adj. EBITDA in total during 2023 and 2024. €1.204 billion will be generated by the two most important segments mentioned above. This alone equates to half the current market cap. To achieve these numbers, JET does not even need to perform spectacularly. It is a cost cutting exercise, which they have proven to do well in the last couple of years. Furthermore growth has returned to Northern Europe and UK&IE giving a further boost to possible adj. EBITDA.

Valuation

With Northern Europe and UK&IE being FCF positive, I find that at its current valuation JET is undervalued. It currently trades at 0.59x EV/Sales compared to DoorDash (3.11x), Delivery Hero (1.04x), HelloFresh (0.51x) and Deliveroo (0.71x). I accept that Grubhub being a drag plays into it, but I feel the strong profitability is being slightly overlooked especially compared to Deliveroo and Delivery Hero.

Whilst growth can be important, strong profitability should not be overlooked. That is why profitability should be the headline for this company rather than growth in GTV and revenue. Let us not forget however, that Northern Europe and UK&IE are growing!

In line with my low growth expectations I have set revenue growth at 2% a year from 2024 onwards with an expected drop of 8.2% in FY23. Where JET will make its gain is from costing cutting in delivery and staffing. This is done by for example further pooling of logistics orders and lowering the cost per delivery.

Financial Estimates JET (Author)

{kind=link}

Below I have added a table that reflects other terminal growth rates and various WACCs.

Sensitivity Analysis (Author)

I am setting my price target at €22.00 ($4.56) based on a terminal growth rate of 2% and a WACC of 8.34%. Even though my model calculates that the WACC is 7.34%, I am applying a 100bps risk premium due to the uncertain nature that lies ahead. I rather be a bit more conservative with such a volatile stock than preach unbridled optimism. This offers an upside of 84.5% to yesterday's close and would reflect an EV/sales of 1.08x which better on the company's standing in my view.

Conclusion

I would consider JET a buy due to its strength in Northern Europe and UK&IE segments. With FCF breakeven accelerating to the end of this year and adj. EBITDA improving, its current valuation of 0.59x EV/Sales does not reflect its performance in my opinion. Whilst the performances of Grubhub are very poor compared to peers, the faintest glimmer of positivity is that it too is approaching FCF positivity with fee caps being removed. This investment case mostly relies on the adj. EBITDA generation of Northern Europe and UK&IE, so deterioration of those segments would result in a lower valuation.

For further details see:

Just Eat Takeaway.com: European Segments Flourish But U.S. Remains A Drag