TKAYF - Just Eat Takeaway: Valuation Is Too Cheap To Ignore

2024-01-22 03:00:05 ET

Summary

- Just Eat Takeaway has a strong marketplace food delivery business with high profitability and a strong moat.

- The food delivery industry is growing, driven by the convenience and variety of options available.

- Even with conservative assumptions, the upside is very attractive.

Investment overview

I give a buy rating to Just Eat Takeaway ( TKAYF ), as I believe the valuation is too cheap to ignore. TKAYF has a very strong marketplace food delivery business that is highly profitable with a strong moat. Even if we make very conservative assumptions, the stock is still worth a lot more than it is today because of its ability to continue growing margins.

Business description

TKAYF operates a very simple business - food delivery, and they operate it under two models: Marketplace and Logistics. A marketplace is basically an online platform where customers can place delivery orders from different restaurants. Logistics is similar to a marketplace, only that the delivery is done by TKAYF own riders. Since TKAYF needs to pay the wages of these riders, the margin is naturally lower and the cost to restaurants and/or consumers will be higher too (somebody has to pay the cost of the riders unless TKAYF decides to subsidize by swallowing the cost via its own P&L). Unlike most peers that are mostly focused on the logistic model, TKAYF has both, which allows it to use the cash flow from marketplace model to fund its logistic model expansion. TKAYF has successfully grown its business by more than 20x to a total revenue size of EUR5.5 billion (from FY13 to FY23) and gross transactional value has reached size of more than EUR26 billion (as of FY23). This growth was driven through organic means and also a series of acquisitions.

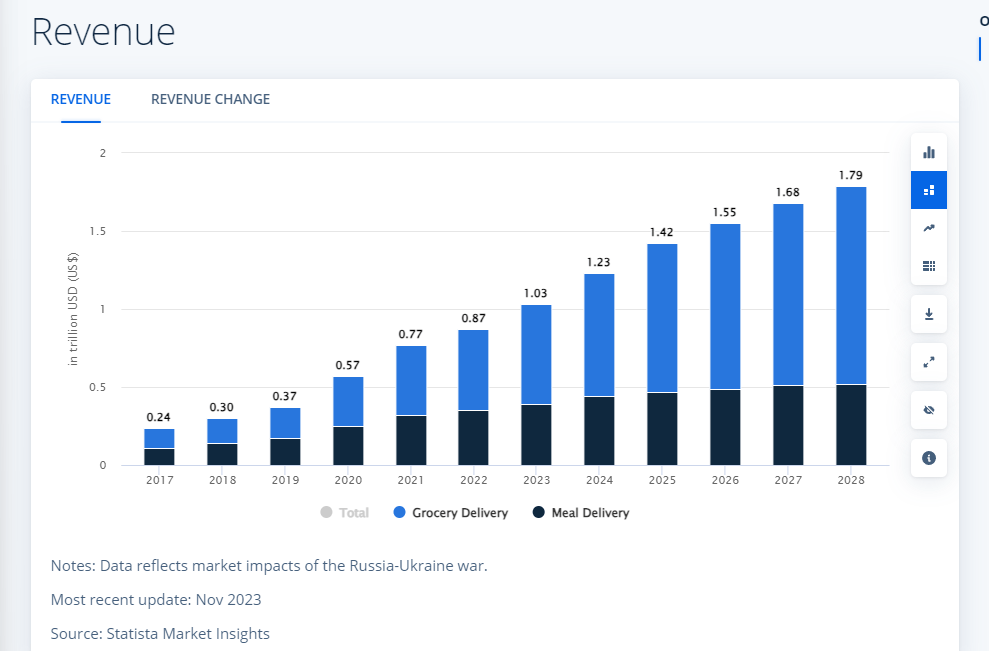

A growing industry

The online food delivery industry has grown at a staggering pace in recent history, mainly due to the increasing need for convenience and also accelerated by the pandemic.

{kind=link}

I believe food delivery is a growing industry that will only get larger over time as the upcoming demographics increasingly become a larger part of the working adult population. Unlike in the past, food delivery has gotten a lot simpler, and there is a lot more variety of food available. With a few taps on the mobile phone, hot food can be delivered within 30 minutes. This convenience is something that the younger generation values and wants to have, which I think is due to the environment that they grew up in. The current batch of young generations is known to have a shorter attention span , which means they want things fast and are willing to pay more to save time . As such, when this group of consumers becomes working adults, they will have more spending power to spend on things like food delivery. I would also note that younger generations are cooking less often , which is also a growth tailwind for the food delivery industry.

Marketplace model has strong moat

In the entire food delivery space, TKAYF has one of the leading marketplace operations because of its roots in Netherlands, Germany, and UK (all marketplace business models. Please refer to TKAYF historical financials for more information). TKAYF competitors like Doordash, Deliveroo, and Uber have their core food delivery business based on a logistic model (source: companies filing. Please refer to their 10K). My opinion is that the marketplace model has the strongest moat and is also the most profitable model to operate.

A food delivery marketplace, as I touched on briefly up top, is an online platform where customers can place delivery orders from a variety of restaurants. The revenue model is akin to e-commerce sites, where TKWY charges the restaurant a commission, which is a percentage of the order value. Similar to large e-commerce sites like Amazon, the sellers are typically independents or small chains. These FNB merchants have historically received delivery orders by phone, which naturally has a smaller market size as there is a lack of discovery element. For instance, if you wanted to order food today without using an app or website, how would you go about doing it? Naturally, you would start googling, and Google would spit out a list of restaurants. You will then need to look through each menu and call the restaurants to see if they are delivering and how much that service will cost. This is a lot of trouble. Here comes a food delivery marketplace operator like TKAYF, whose key value proposition is to solve the discovery element and enlarge the total profit pool for restaurants as it lowers the adoption friction for food delivery. Since the deliveries are fulfilled by the restaurants, this is an extremely asset-light business that has high-profit margins if one achieves scale.

So how does TKAYF exactly win? I believe it boils down to 2 aspects:

- Selection: having all the restaurants

- Brand/habit: being top of mind

For selection, firstly, while it seems easy for people to adopt an additional tablet, it creates operational complexity. This is what people call tablet hell (for readers that think it is just another tablet, that is not true. Ask any front of house staff how annoying and complex it is to deal with 3 or 4 different tablets). Secondly, it costs a lot to acquire marketplace restaurants as a subscale/new player, not only because you have to acquire the restaurants one by one, but because these restaurants churn at a relatively higher pace than large chains (because of weaker balance sheet, lesser marketing power, etc.). Remember that these restaurants are typically independent or small chains, so the sales team on the ground needs to look for each of them individually. TKAYF already has the scale to continuously fund this restaurant acquisition cost (this is the total cost to sign the restaurants up - for instance, the cost of hiring ground staff to knock on each independent restaurant to convince restaurants to be listed on the platform). while being profitable (Netherlands, Germany, and UK [see Just Eats financials before the logistics business unit started]). For a newcomer, the cost to acquire these restaurants is very high.

We can see this in the Netherlands where TKAYF is the largest player. Deliveroo failed to do any damage and exited, Uber has been there for multiple years but has done no damage to TKAYF yet (TKAYF continues to hold the largest market share and remained profitable with >4% EBITDA margin as a percentage of GTV). Uber has not been able to build any level of selection that matters because they only had chain restaurants (McDonald's mostly) and while they do have some independent restaurants, the over selection remains weak relative to TKWY. Take for example, from the latest data available, Uber had >1,200 restaurants in 2019 but TKAYF had more than 24,000 restaurants and added more than 3,000 restaurants between FY19 and FY20 (source: company filings ). Also, because TKAYF has built up such as strong brand, its other moat it's a high share of consumer mindshare (discussed below).

For brand/habit, most consumers are habitual in nature as well which creates a fair bit of stickiness. This is where being top of mind matters. Once the platform reaches a significant scale, it begins to reap the benefits of network effects. This is because customers are more likely to use a marketplace that has a large number of restaurants listed on it. Restaurants are more likely to want to be in a marketplace if there are a lot of people using it. Once the habit is formed, naturally they will keep going back to the same platform to order. I would note here that this is also the reason why TKAYF has had a hard time penetrating London which is Deliveroo's stronghold (where Deliveroo started its food delivery business) because of the habit that consumers' have built up over time. Once the platform has reached that level of scale, so long as it does not give a reason for consumers to churn to another platform (like having a lesser selection), consumers generally stick to the same platform. You may argue that platforms can continuously provide vouchers and discounts to attract consumers. This may work for the near term, but without selection, these consumers won't stay for long (look at Uber and Deliveroo's failure to displace TKAYF as the leader in the Netherlands is a good example).

Grubhub is profitable without the fee caps

Regarding Grubhub, I think what is done is done. This is a bad acquisition that has significantly altered the stock's narrative. Ever since TKAYF acquired Grubhub, the stock has gone in only one direction: downward. However, at this point, I think there is only an upside from here. My main focus on this aspect is that Grubhub is a profitable business without the fee caps. Based on the FY22 disclosure in the call, fee caps were a EUR130 million headwind to the business. This EUR 130 million is literally 6x FY22 EBITDA, for reference. I believe the fee caps are unconstitutional , and they should go away eventually. My take is that these fee caps were put in place to help restaurants tide through the pandemic. Now that the pandemic is over, there is no reason for this to be permanent.

North America, we turned to positive adjusted EBITDA of EUR65 million in 2022, despite more than EUR130 million negative impact from remaining fee caps. Company FY22 earnings

Valuation too cheap to ignore

{kind=link}

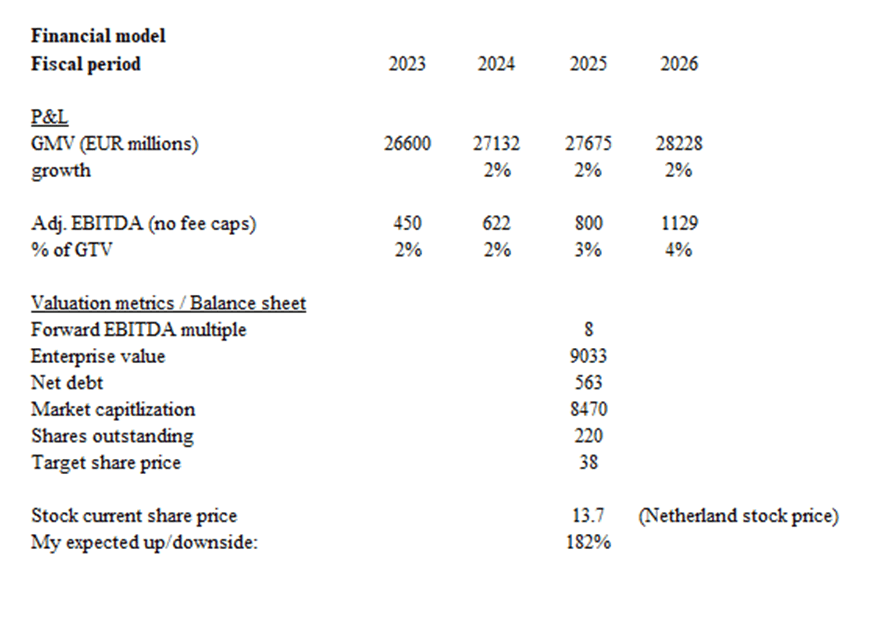

Lastly, I simply think that the TKAYF valuation is too cheap to ignore. Even if we assume that the business has reached growth maturity and is going to simply grow with inflation (2% growth), the upside is still tremendous because it is now on track to continue expanding its margins. My model suggests that TKAYF will reach EUR28 billion in GMV, and assuming that fee caps are removed and the EBITDA margin expands to 4%, TKAYF should be able to generate EUR1.1 billion in adj EBITDA. I remind readers that TKAYF has a very profitable marketplace model, and its logistics model (mainly in Canada) is profitable as well. Its marketplace model, at maturity (using northern Europe as a benchmark), has an EBITDA margin (percentage of GTV) of >4%, and its Canada logistic business has an EBITDA margin of >4% as well. Suppose TKAYF and the rest of the country grow by a similar margin over time (which is possible given that they can now cut back on growth expenditure since my assumption is that growth has matured), the business can easily achieve >EUR1 billion in adj. EBITDA. Even if we assume valuation stays at the current level of 8x forward EBITDA, I still get a target share price of EUR38, which is almost triple the current share price.

Risk

TKAYF stock sentiment is very negative because of the Grubhub acquisition, where many investors believe that management is not competent. Moreover, Doordash has been executing very well and capturing share in the US, which has made the sentiment even worse. If TKAYF does not show growth, the bearish narrative will continue to take over the stock, putting huge pressure on the share price. Macro is also a risk because food delivery is deemed as discretionary spending. When a recession hits, more people are likely to cut on such spending (and dine at home for example). One more risk is that the fee caps might not go away as soon as I expect, or they might not go away forever. In this case, TKAYF will lose $130 million of EBITDA permanently, which will impact its valuation.

Conclusion

I give TKAYF a buy rating as it has a robust marketplace food delivery business, marked by strong profitability and a formidable moat. Despite concerns arising from the Grubhub acquisition, the fact is Grubhub is a very profitable business without the fee caps. Even assuming a conservative growth scenario, the current valuation appears markedly undervalued. The path to expanding margins, coupled with the profitability of both the marketplace and logistics models, could easily push TKAYF's adjusted EBITDA to over EUR1 billion.

For further details see:

Just Eat Takeaway: Valuation Is Too Cheap To Ignore