KNTNF - K92 Mining: Excellent Miner With Huge Potential

2023-12-13 23:39:17 ET

Summary

- K92 is a gold miner with one producing mine in Papua New Guinea, Kainantu. The mine has ore grade 9.1 g/t and a 7.6 M oz AuEq reserve base.

- In the next three years, the annual production is expected to quadruple from 111 k AuEq to 470 k oz AuEq.

- K92 has a robust balance sheet with a 12.1 cash-to-total debt ratio and enough liquidity to fund Stage 3 and 4 expansions.

- K92 management has proven itself to be a capable capital allocator. Over the years, they avoided significant share dilution, kept debt to equity ratio below 12%, and consistently realized positive returns.

- Despite being more expensive than its peers, K92 is undervalued compared to its past 5Y average multiples and offers excellent value for its price.

Introduction

K92 Mining ( KNTNF ) (KNT:CA) is an enticing gold miner with significant upside potential. The company has one operational mine, Kainantu, in the Eastern Highlands Province of Papua New Guinea. Kainantu is an underground mine with a top ore grade of 9.1 g/t and a 3.0 cutoff grade. The reserve base is 7.6 M oz Au. These figures put Kainantu among Tier 1 mines like Obuasi, Brucejack, and Fruta del Norte.

Mine output is 111 k oz Au per year, but it is planned to expand to 470 k oz Au in the next three years. K92 has a robust balance sheet with low leverage and adequate liquidity to finance the Kainantu mine expansion. K92 management has proven itself to be a capable capital allocator, too. Over the years, they avoided significant share dilution, kept debt to equity ratio below 12%, and consistently realized positive returns. K92 trades at higher multiples compared to its peers. On the other hand, its EV/Sales, EV/EBITDA, and Price to Book are well below 5Y average and 5Y peak figures.

K92 overview

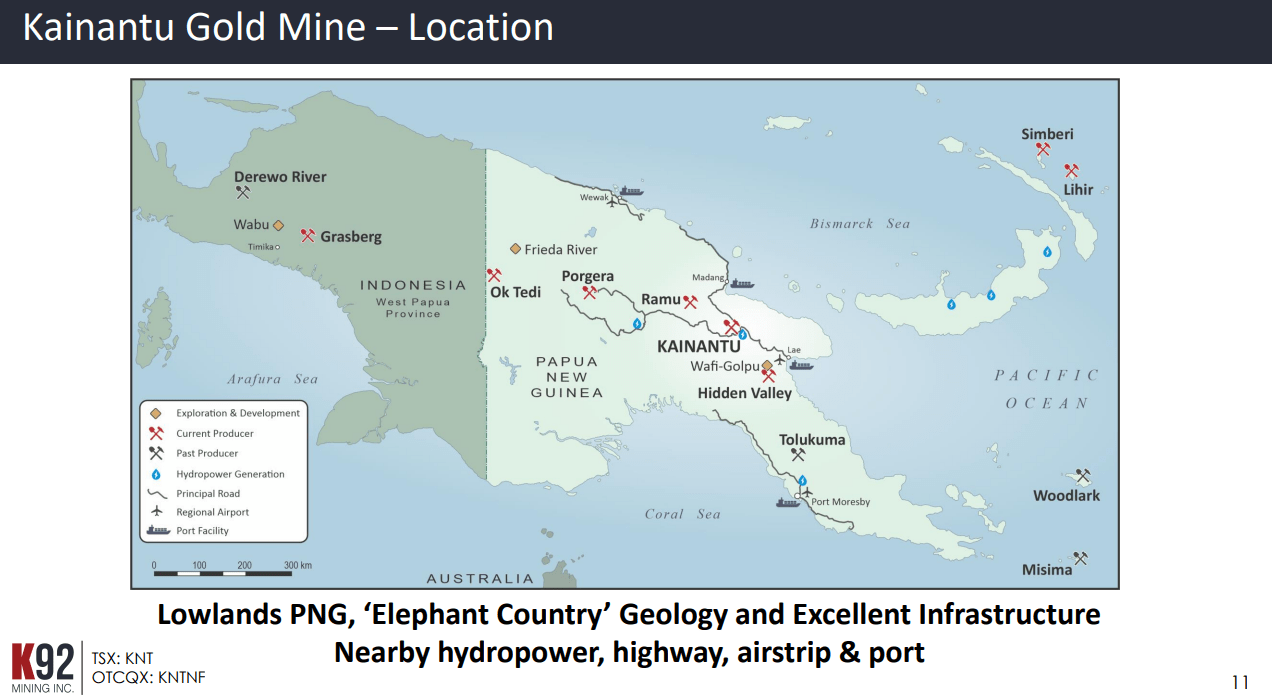

Papua Island (Indonesian province of West Papua and Papua New Guinea as an independent state) is home to large gold and copper deposits. Grasberg Mine, one of the largest gold and copper discoveries ever, is in the Indonesian part of the island. K92 mine is in Papua New Guinea. Other notable mines are Lihir owned by Newcrest/Newmont ( NEM ) and Porgera owned by Barrick ( GOLD ).

The map below from the last K92 presentation shows Papua's major mine sites.

{kind=link}

Kainantu mine is a polymetallic deposit with gold, copper, and silver reserves, although gold represents over 90% of mine output. The mine has an annual output of 150 k oz AuEq, LOM until 2029, cash cost $900/oz, and AISC $1300/oz.

{kind=link}

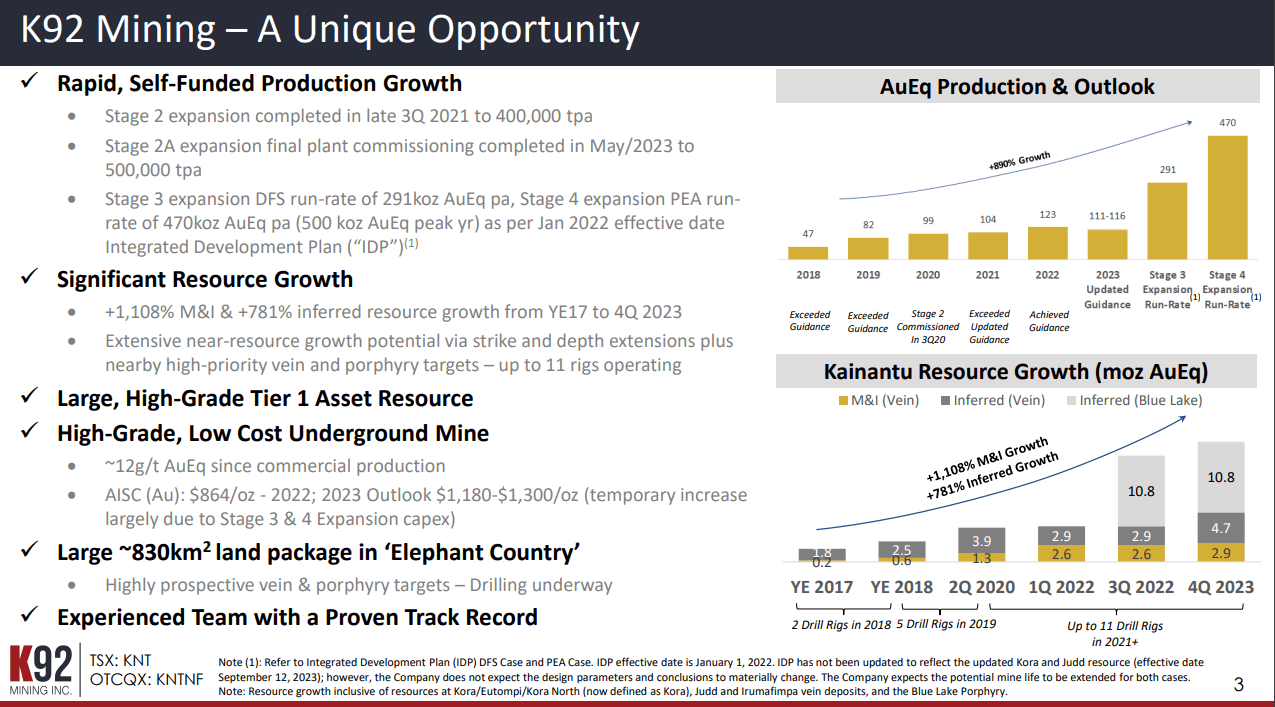

In 2018, the annual production was a mere 47 k oz AuEq, reaching 111 k oz AuEq in 2023. The total production growth for five years is 890%. The company’s resource base grew significantly, too. M&I reserves grew by 1,108% for five years.

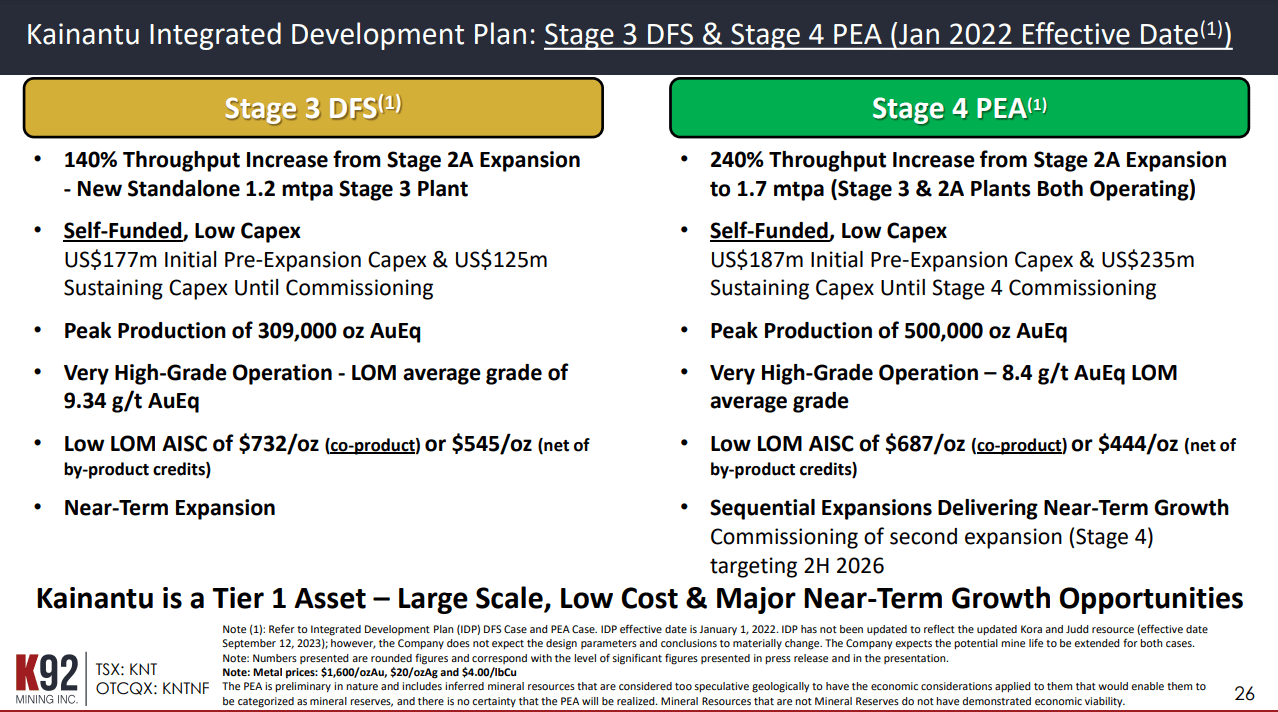

K92 management gradually expanded Kainantu production, following a multiple-stage plan. The subsequent phases are shown in the table below.

{kind=link}

The next phase is Stage 3, planned for 1Q25, increasing throughput by 140% and production to 291 k oz AuEq for LOM. The peak production is expected to reach 309 k oz AuEq with an average LOM grade of 9.34 g/t. AISC is projected to be $732/oz. The total investment is $302 million: $177 million for initial CAPEX and $125 million for sustaining CAPEX. The completion of stage 3 is planned for 1Q25.

Stage 4 will increase mine output further—the thought to 1.7 mtpa and peak production to 500 k oz AuEq. LOM's average grade is 8.4 g/t. LOM AISC will drop further to $687/oz. The total investment required to complete stage 4 is $422 million, $187 million for initial CAPEX, and $235 million for sustaining CAPEX. Stage 4 commissioning is planned for 2H26.

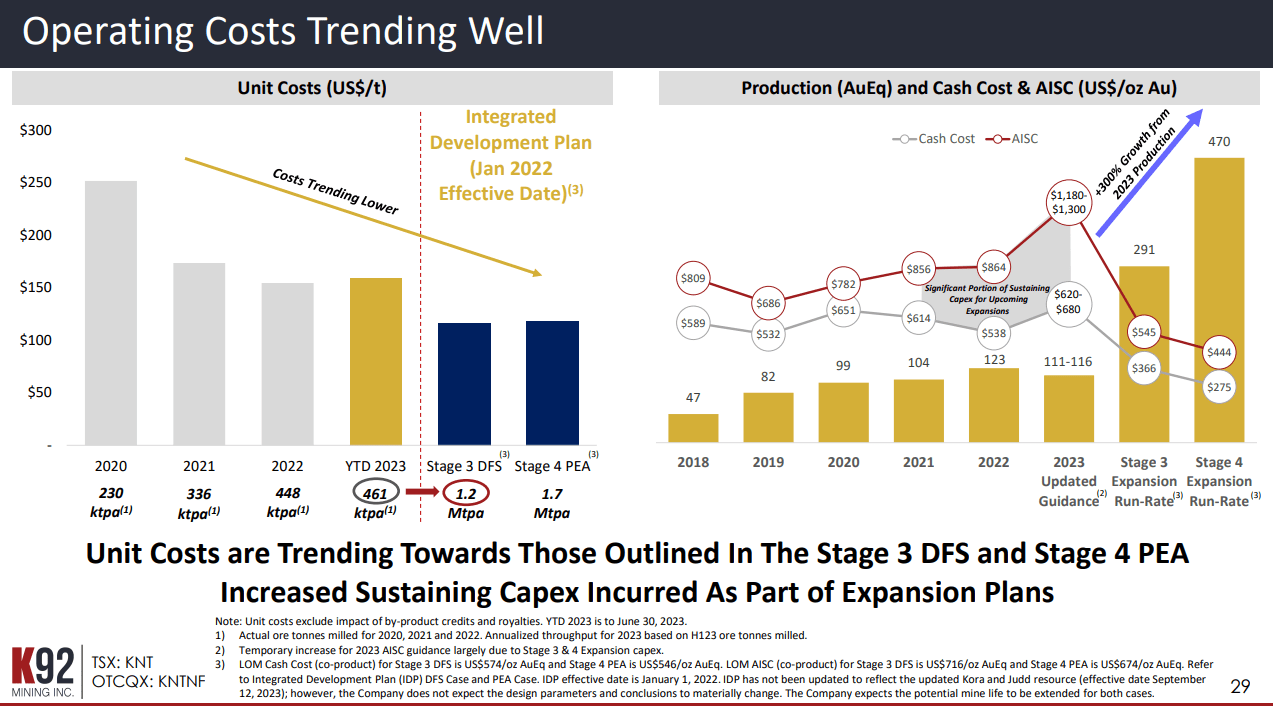

K92 has a competitive cost profile even at the $1300/oz AISC ( 3Q23 ). The completion of the expansion phases will significantly reduce cash costs and AISC.

{kind=link}

The company`s managers have proven their ability to improve mine operations efficiency. The unit cost has declined following the throughput increase, resulting in lower-than-average cash AISC. In the last two years, cash costs and AISC have increased due to capital investments, although they remain below the global average of $1,358/oz.

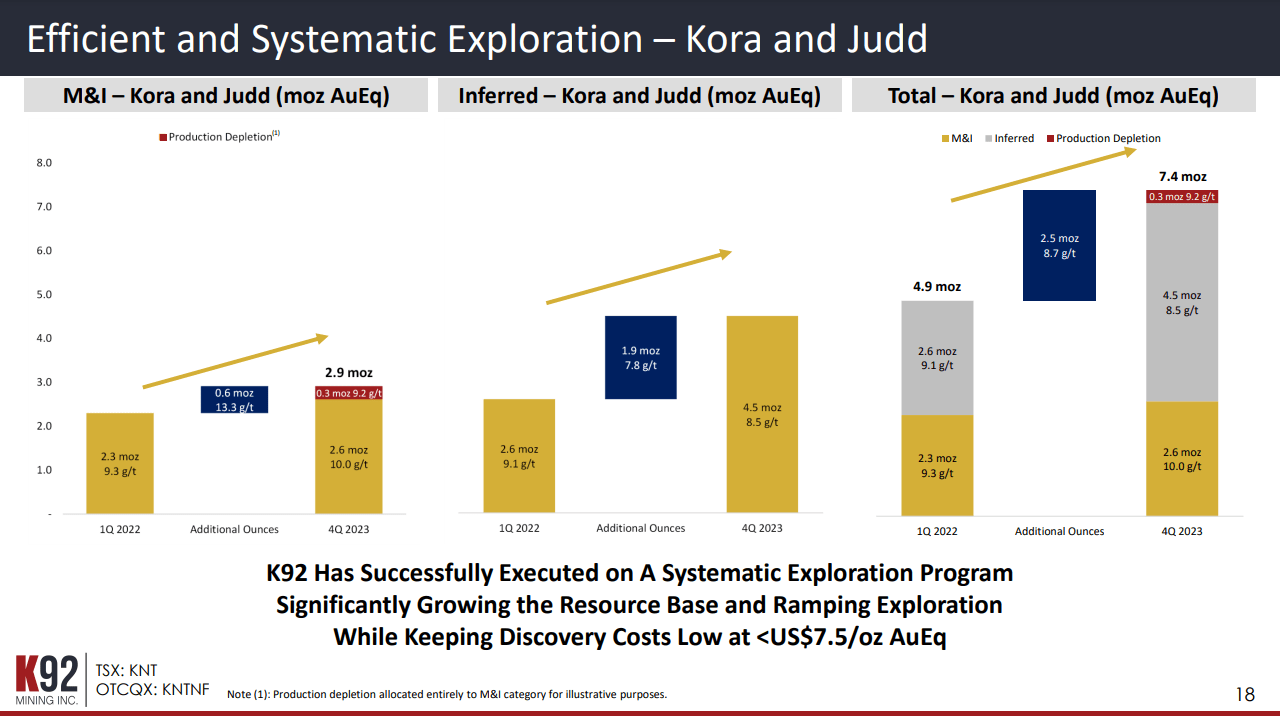

K92 follows a systematic approach to exploration.

{kind=link}

The table above shows that the resource base is growing faster than depletion. K90 team sticks to rule number one in mining: the reserves renewal rate must exceed the reserves depletion rate. The company continues with exploration, targeting unexplored Judd and Kora South veins. The results are encouraging, with grade 8 g/t and recovery of 92%.

K92 Financials

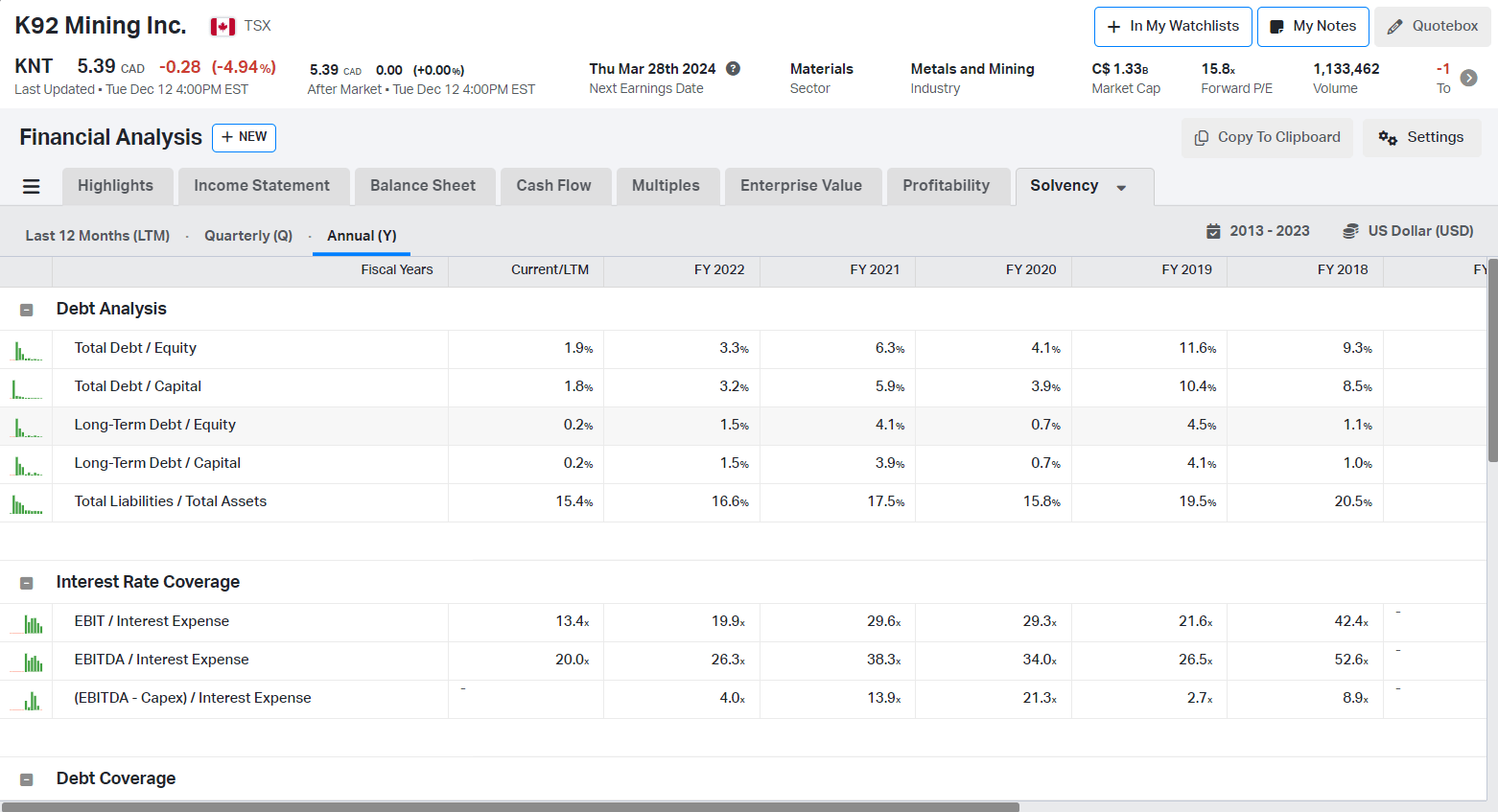

K92 has a robust balance sheet to cover its company expansion projects: the chart company`s capital structure and interest coverage.

{kind=link}

K92 excels on all debt-to-equity metrics. Total debt/equity is 1.9%, long-term debt/capital is 0.2%, and total liabilities/total assets are 15.4%. Interest coverage figures are impressive, too. EBITDA/Interest expenses have not been lower than 20 for five years.

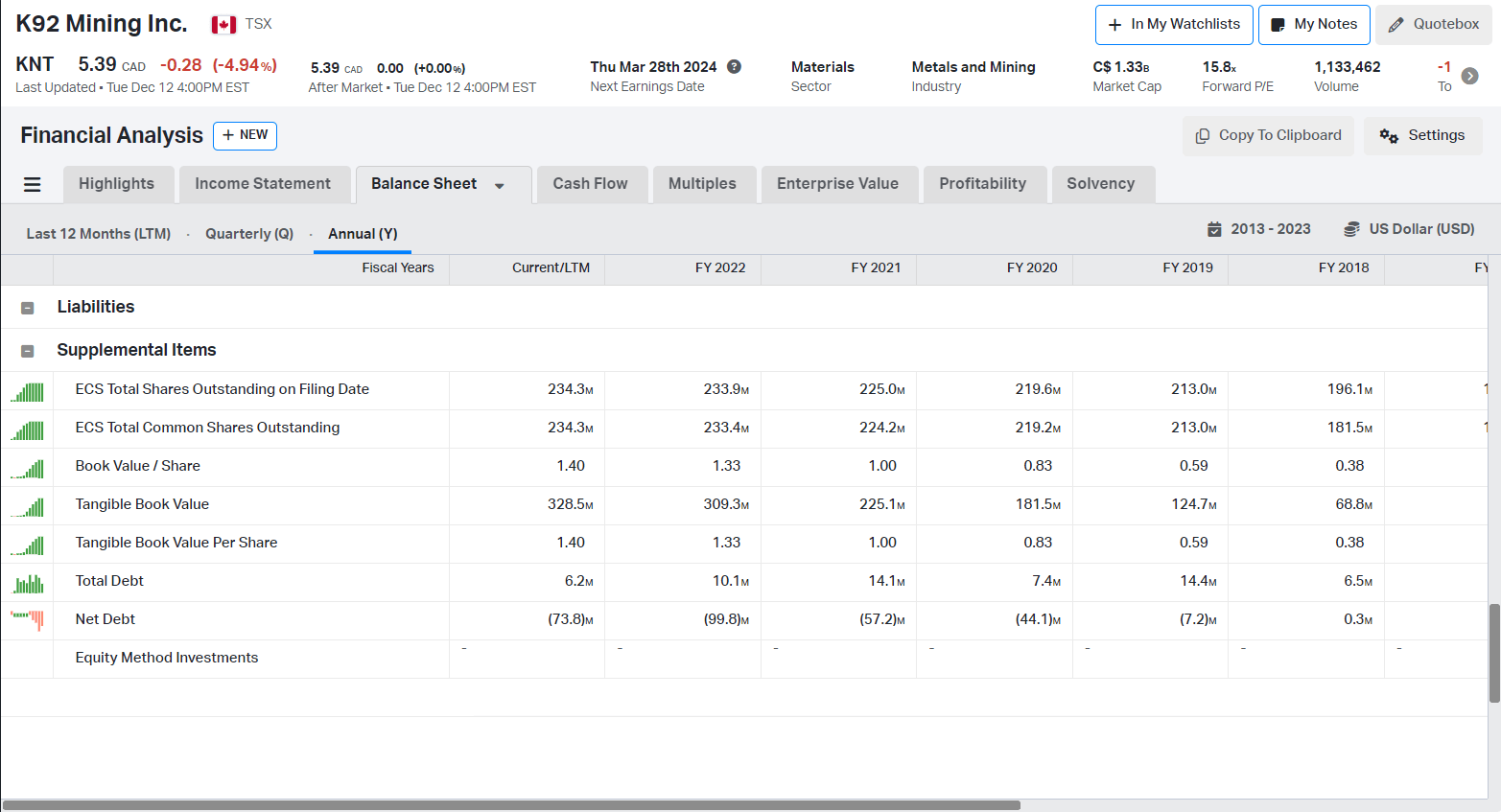

The company’s management has done an excellent job maintaining the company`s leverage low and avoiding significant share dilution. The table below shows the K92 share count for the last five years.

{kind=link}

Share count increased 22% over a year, while the company reserve base and annual production grew 890% and 1108%, respectively.

K92 has $79.9 million cash and $6.6 million total debt, resulting in a 12.1 cash-to-total debt ratio. For reference, similar-sized miners like Seabridge ( SA ) have 0.26; New Gold ( NGD ) 0.46; Centerra Gold ( CGAU ) 97; and Coeur Mining ( CDE ) 0.11. K92 and Centerra have the higher cash-to-total debt multiples among the sample group.

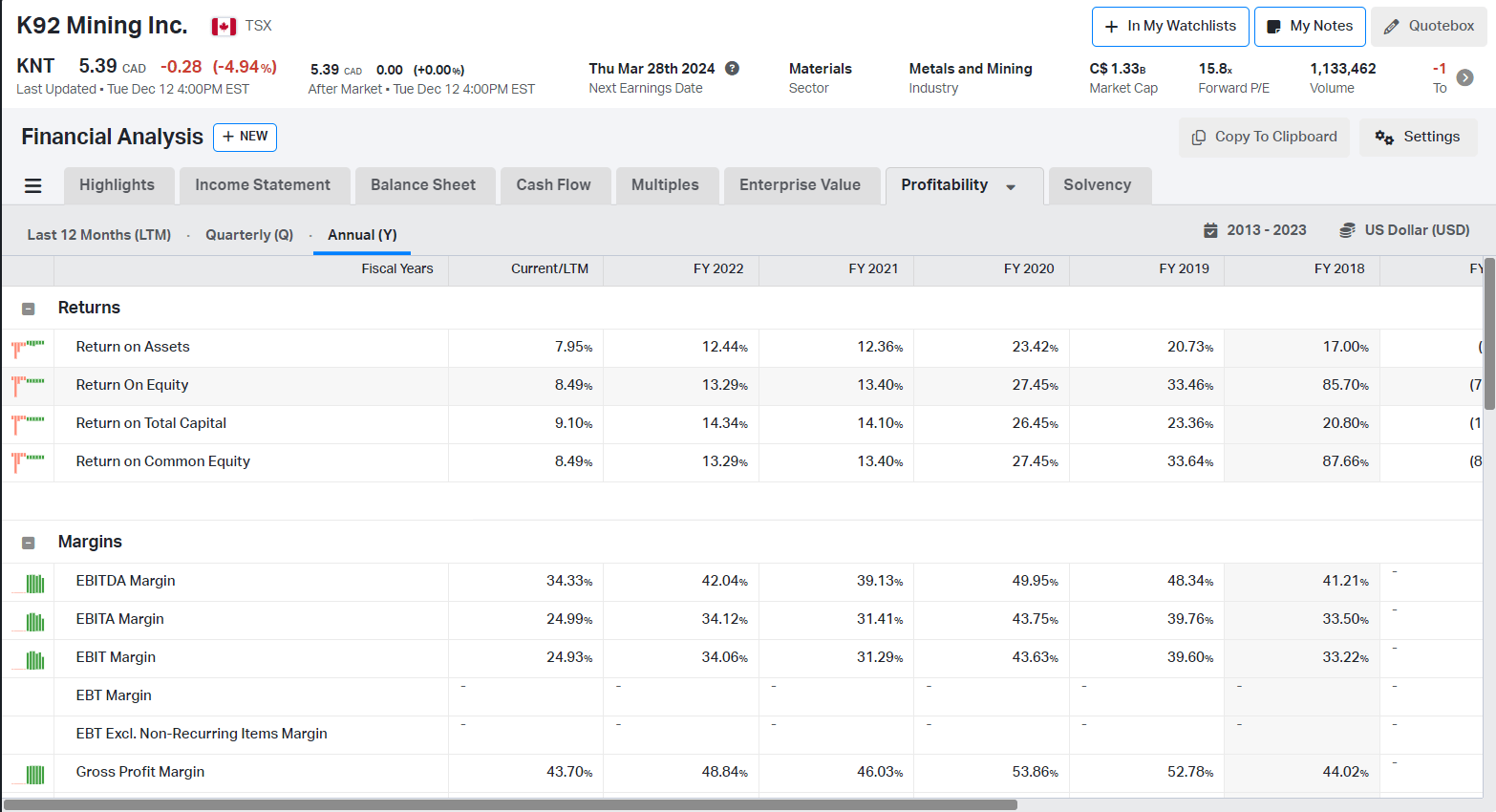

Let's see how efficient and profitable the K92 business is.

{kind=link}

The returns and margins are great for gold miners with one producing mine. Apart from that, the margins and returns have been positive over the years. The mining business is tough due to its pronounced cyclicality; hence, going underwater is not difficult.

Let`s compare K92's profitability with similarly sized peers:

- KNTNF: 43.7% Gross Margin, 34.3% EBITDA Margin, 8.5% ROE, and 9.1% ROTC

- SA: - % Gross Margin, - % EBITDA Margin, (4)% ROE, and (1)% ROTC

- NGD: 41.6% Gross Margin, 34.9% EBITDA Margin, (5.6)% ROE, and 2.2% ROTC

- CGAU: 23.7% Gross Margin, 10.2% EBITDA Margin, (9.9)% ROE, and (2.2)% ROTC

- CDE: 16.7% Gross Margin, 9.7% EBITDA Margin, (3.1)% ROE, and (1.4)% ROTC

K92 and NGD score the highest margins. However, the former has solid returns, too.

The resources are scarce and limited, though our desires are not. Despite the size of the account, it is not infinite. That said, investing is a game of funds allocation. The same applies to business operations.

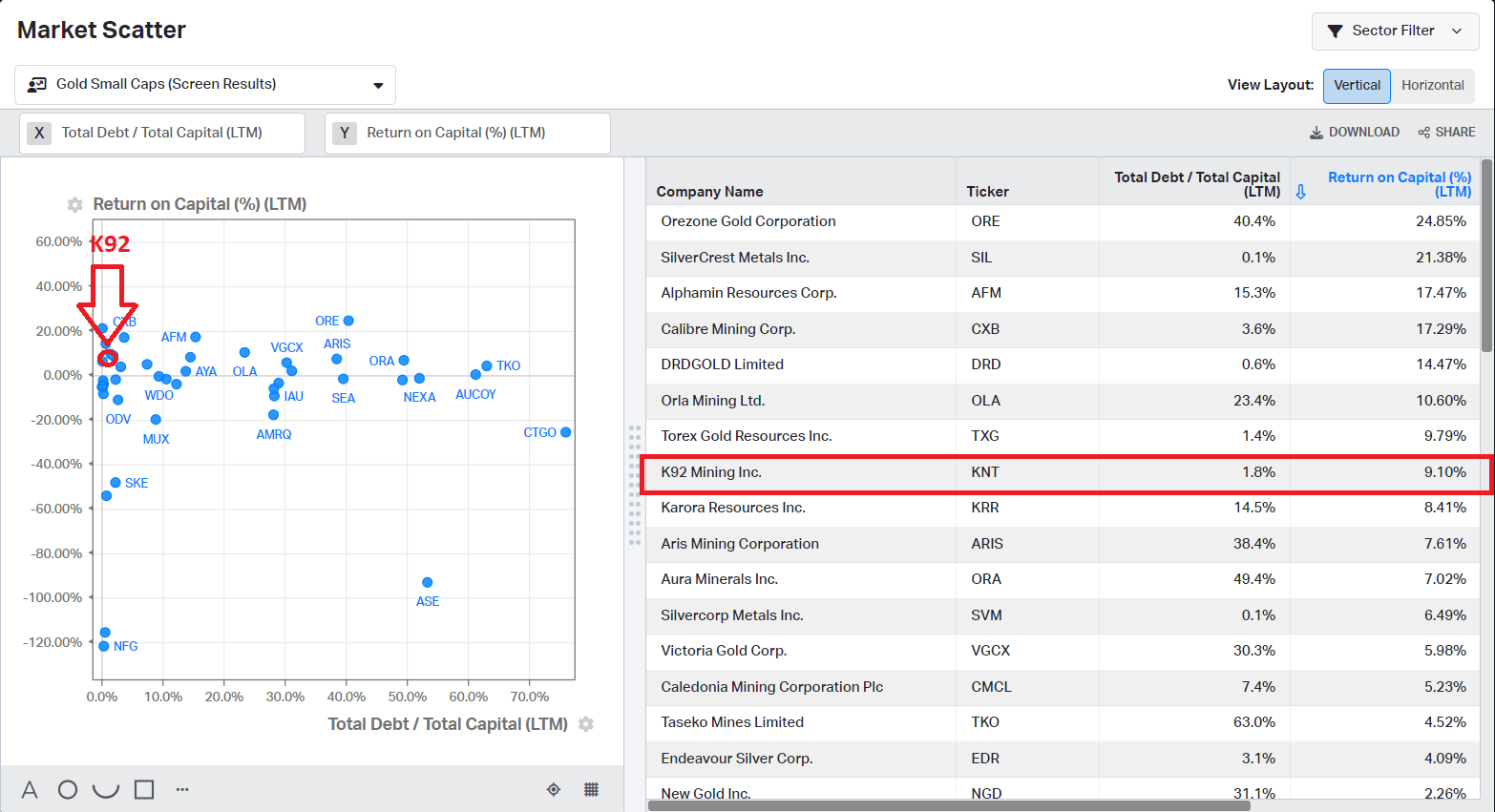

{kind=link}

K92 is one of the best in that game. The table above compares gold miners with a market cap of $200-$1000 million by Total Debt/Total Capital (TD/TC) and ROTC. K92 is among the top five companies in the list measured by ROTC divided by TD/TC.

Valuation

Despite its low price, IAUX is still overvalued compared to its peers. For comparison:

- KNT trades at 4.8 EV/Sales, 14.12 EV/EBITDA, and 2.98 Price/Book

- SA trades at - EV/Sales, - EV/EBITDA, and 1.7 Price/Book

- NGD trades at 1.53 EV/Sales, 4.38 EV/EBITDA, and 1.06 Price/Book

- CGAU trades at 0.71 EV/Sales, 7.01 EV/EBITDA, and 0.69 Price/Book

- CDE trades at 2.15 EV/Sales, 21.95 EV/EBITDA, and 1.14 Price/Book

K92 trades at the highest multiples among its peers. Let's see how the company fairs compared to its historical figures.

{kind=link}

K92 trades at lower than 5Y average multiples (6.52 EV/Sales, 15.01 EV/EBITDA, and 3.01 Price/Book). Besides that, its multiples are well below the previous peaks (11.3 EV/Sales, 25.1 EV/EBITDA, and 8.3 Price/Book).

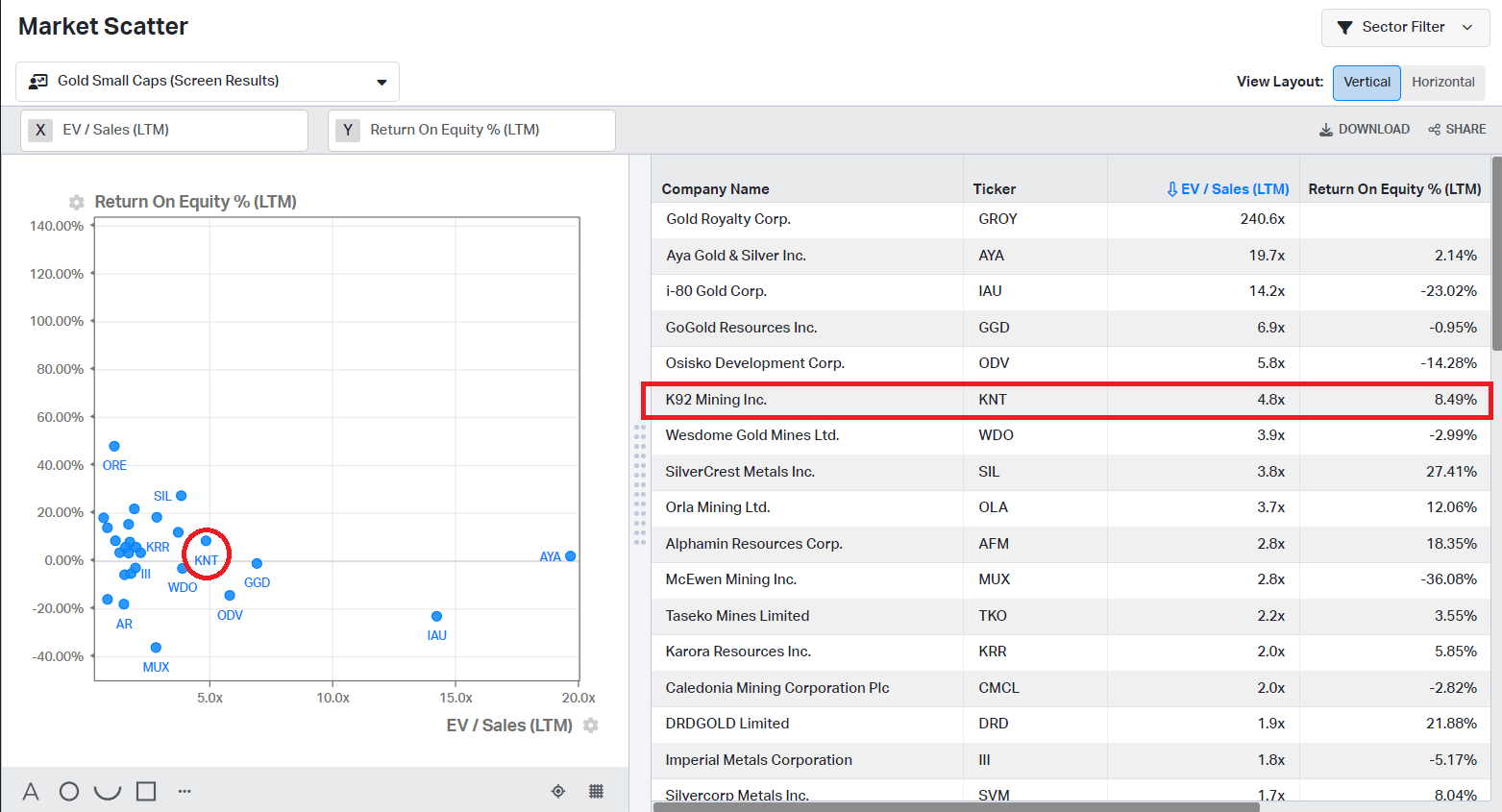

The chart below represents ROE ((LTM)) on the Y axis and EV/Sales ((LTM)) on the X axis for gold miners with a $200-$1000 market cap.

{kind=link}

To get 8.49% ROE, I must pay 4.8 EV/Sales. K92 is among the companies offering the most value for what we deliver. Despite being more expensive than its peers, K92 is undervalued compared to its past 5Y average multiples and offers excellent value for its price.

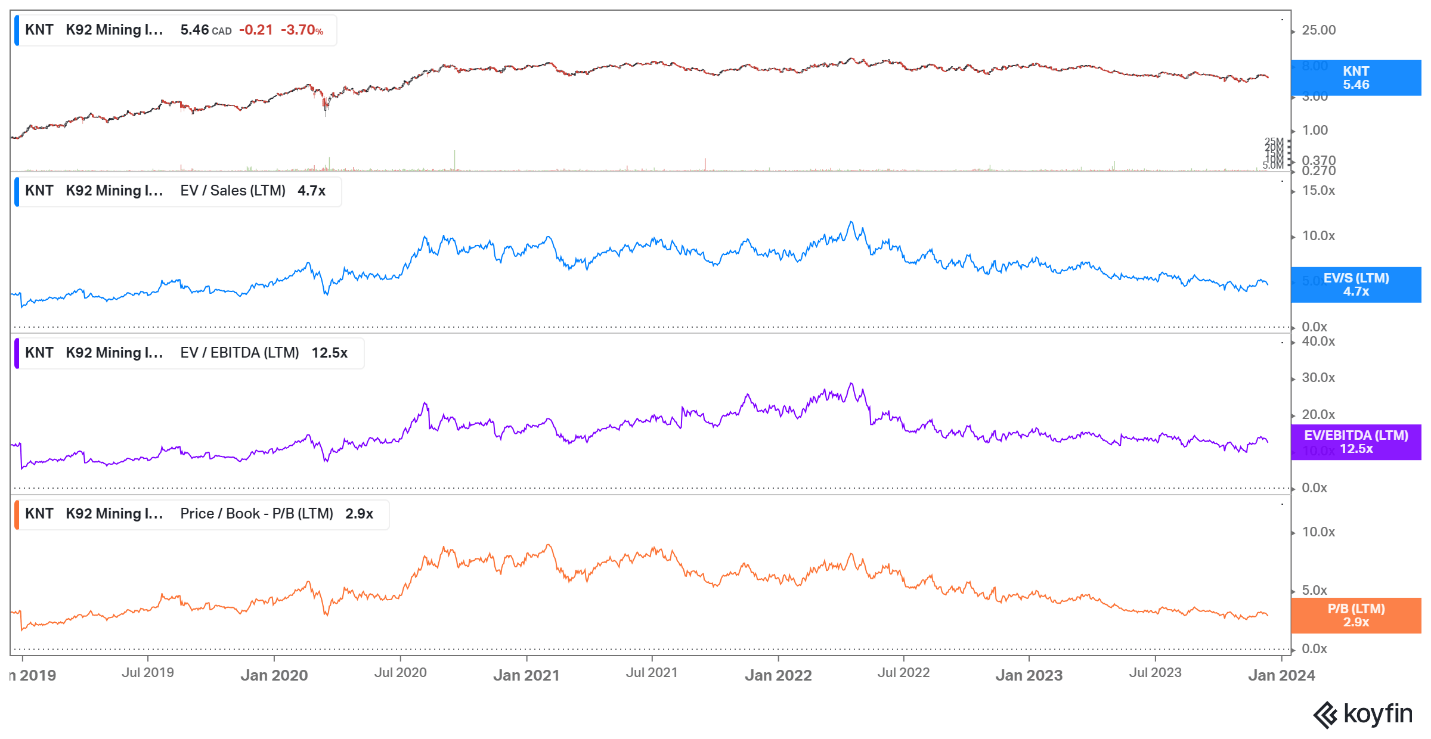

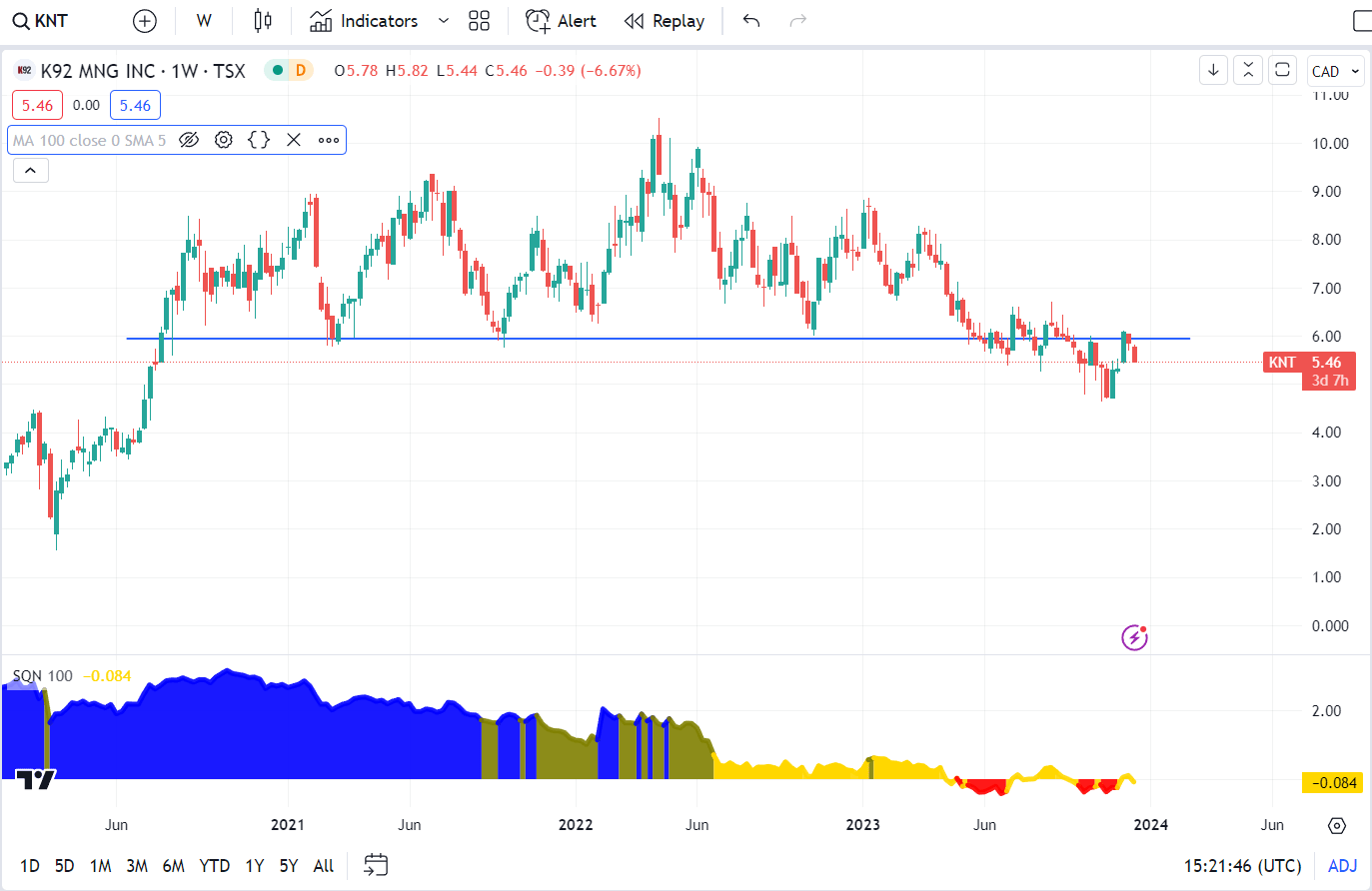

Price Action

K92 trades at a significant price level. A confirmed breakout above would offer an excellent entry opportunity.

{kind=link}

If the price closes above the $6.0-$6.2 zone with a strong bull candle, I will consider it an entry signal. SQN indicator shifts between bear quiet (red) and neutral (yellow) regime. In such a situation, I prefer to wait before I add a considerable size to K92. However, I will start building a position with a fraction of the planned size.

Risks

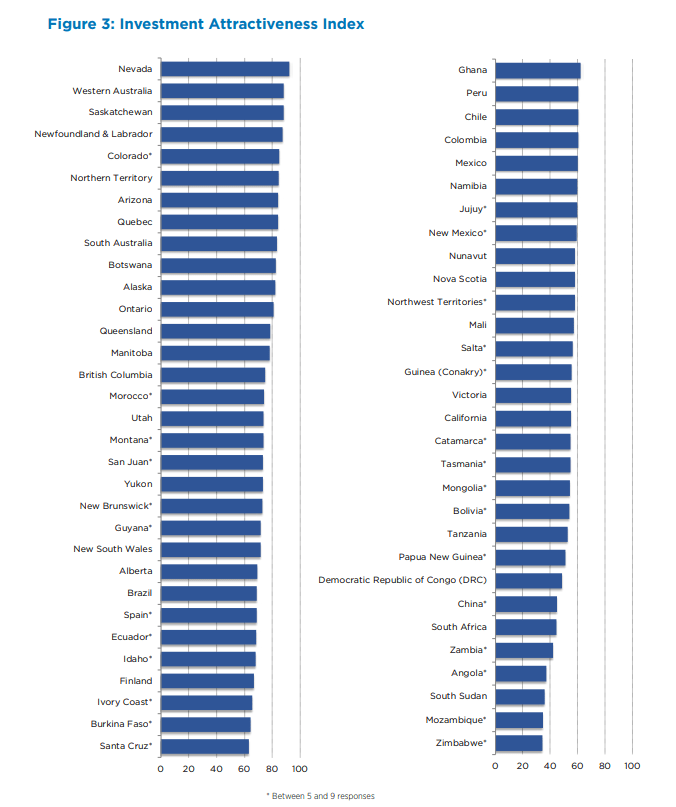

Financial risk is not nonexistent in K92. The company has ample funds to run its operations and invest in CAPEX. K92's most pronounced risk is the country's risk of doing business in Papua New Guinea ((PNG)). The Fraser Institute ranks PNG in the lowest percentile in the Investment Attractiveness Index.

Fraser Institute Annual Survey

{kind=link}

The primary drag in PNG is the uncertainty concerning disputed land claims, taxation regimes, and infrastructure quality. Despite the challenges, the K92 management team has proven their ability to navigate country uncertainties. As my I-80 gold article said, I prefer to invest in an efficient business in a questionable country instead of in a loser in a top jurisdiction. K92 falls into the first category.

The usual risk for all miners is the price of the extracted ore. The gold price has struggled in the last two years to break the significant resistance at $2000/oz. I believe sooner than later, the gold price will eventually run through the 2k level and remain permanently there.

Investors Takeaway

K92 is enticing gold miners with the potential to quadruple production in the next three years. The company owns Kainantu underground mine in Papua New Guinea. The mine has excellent ore grade and reserve base comparable to Tier 1 assets owned by the majors. K92 has a robust balance sheet with a 12.1 cash-to-total debt ratio and enough liquidity to fund Stage 3 and 4 expansions. The company`s management has been very prudent with share dilution, too. K92 margins and returns have been positive over the years.

Despite being more expensive than its peers, K92 is undervalued compared to its past 5Y average multiples and offers excellent value for its price. The reason for not giving a strong buy rating is the price action—the price hovers below a significant resistance. I prefer to wait for the confirmed breakout above the resistance to put full-sized positions. However, I will start building a position with a fraction of the planned size.

For further details see:

K92 Mining: Excellent Miner With Huge Potential