KNTNF - K92 Mining: Too Cheap To Ignore

2023-12-14 08:37:41 ET

Summary

- K92 Mining's resource estimate for its Kora and Judd deposits exceeded my expectations, reaching ~7.1 million gold-equivalent ounces.

- Importantly, the company achieved this resource growth with minimal share dilution, increasing its GEOs per share, yet the stock has barely moved since the news.

- With this being an exploration story sector-wide, a top-3 growth story & with K92 set to be the lowest-cost producer sector-wide, the stock is dirt-cheap at ~0.40x P/NAV.

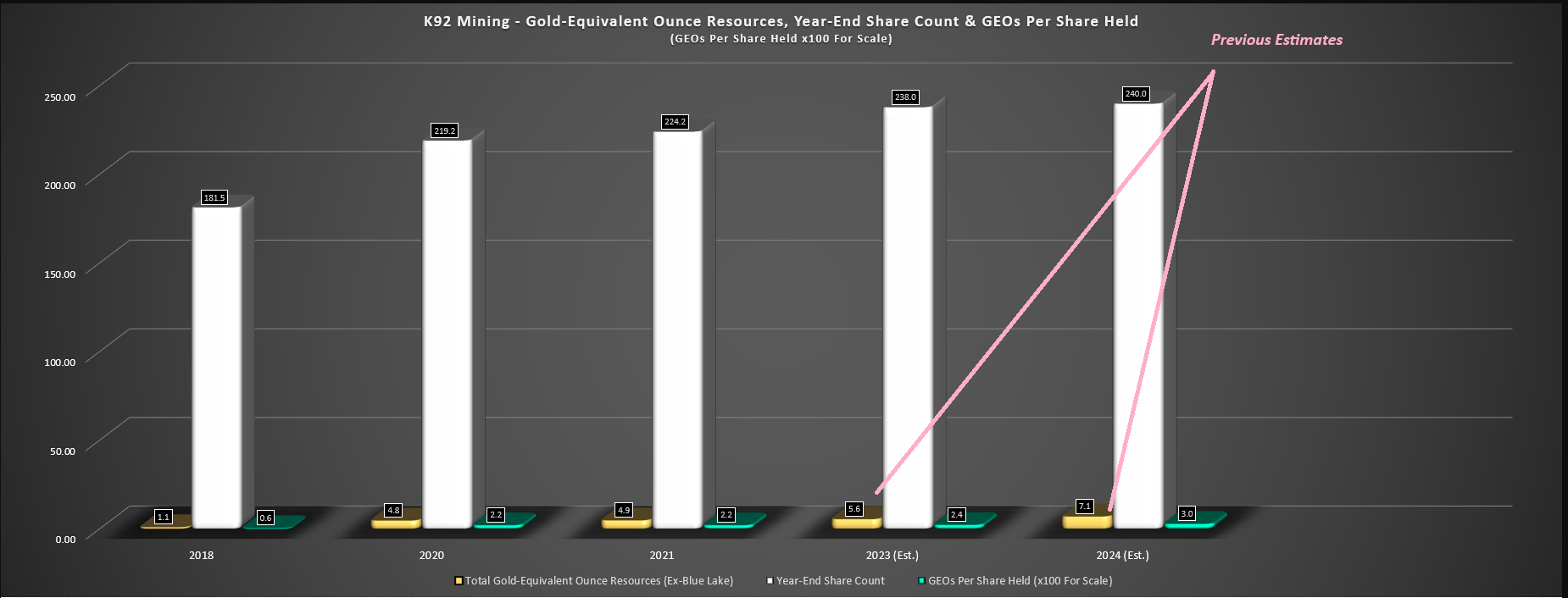

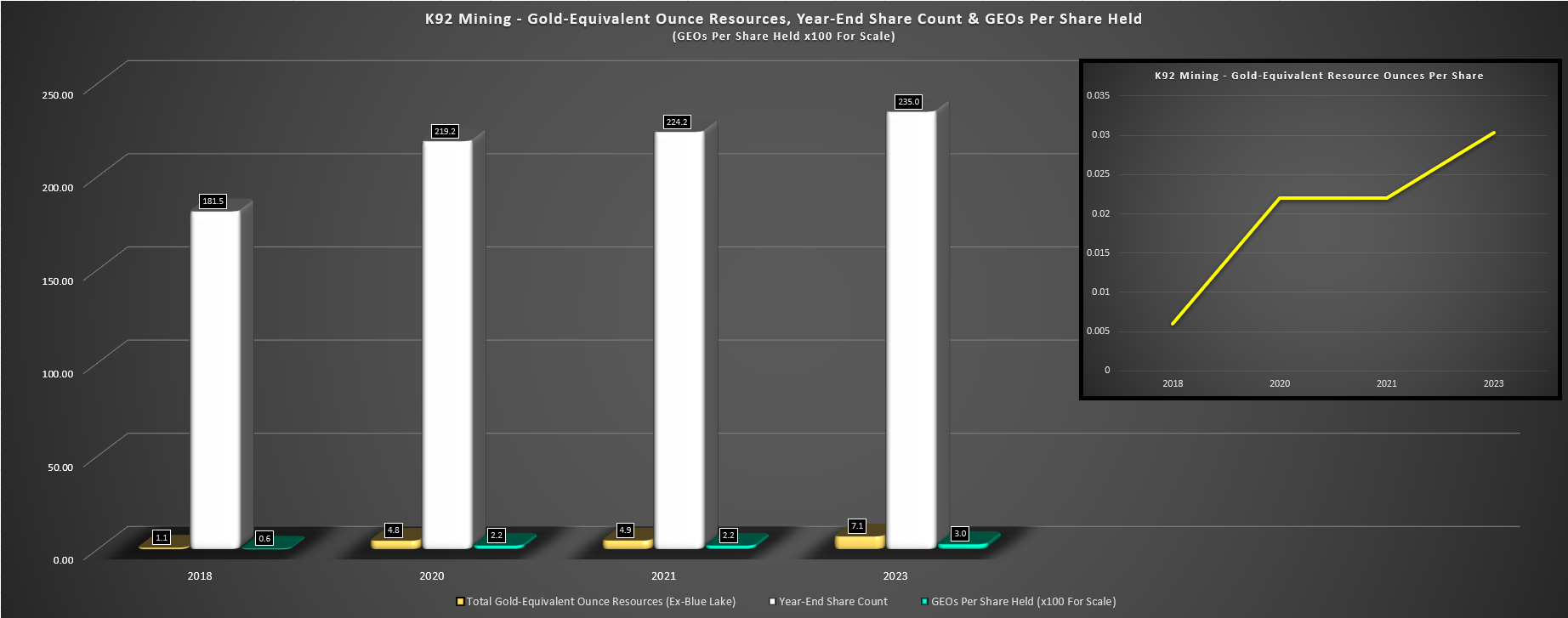

K92 Mining (KNTNF) released an update resource estimate for its Kora and Judd deposits at its Kainantu Mine (effective date September 12th, 2023), and the results exceeded my expectations. As noted in a previous update in June 2023, I expected to see resource growth to 5.6 million GEOs in 2023 as I wasn't sure about the company's ability to get enough infill drilling completed in time to see the full benefit of resource growth this year, but that I expected 6.3 - 7.1 million GEOs to be proven up by year-end 2024. And as the below charts highlight, the company's new resource hit the top end of my estimate a year early, with ~7.1 million gold-equivalent ounces across all categories.

"If we combine these two resources, I see the potential for 6.3 - 7.1 million gold-equivalent ounces to be proven up in the resource category at Kainanatu (Judd + Kora) by year-end 2024 (Q1 2025) and I think there's upside to this figure longer-term once better definition drilling is complete. "

- June 2023 Update

Judd Underground Development & Drill Core - Kainantu Mine - Company Website K92 Mining - Gold-Equivalent Ounce Resources, Estimated Year-End Share Count & GEOs Per Share Held - Company Filings, Author's Chart & Estimates K92 Mining Current GEOs, Year-End Share Count & GEOs Per Share Held - Company Filings, Author's Chart

{kind=link}

{kind=link}

{kind=link}

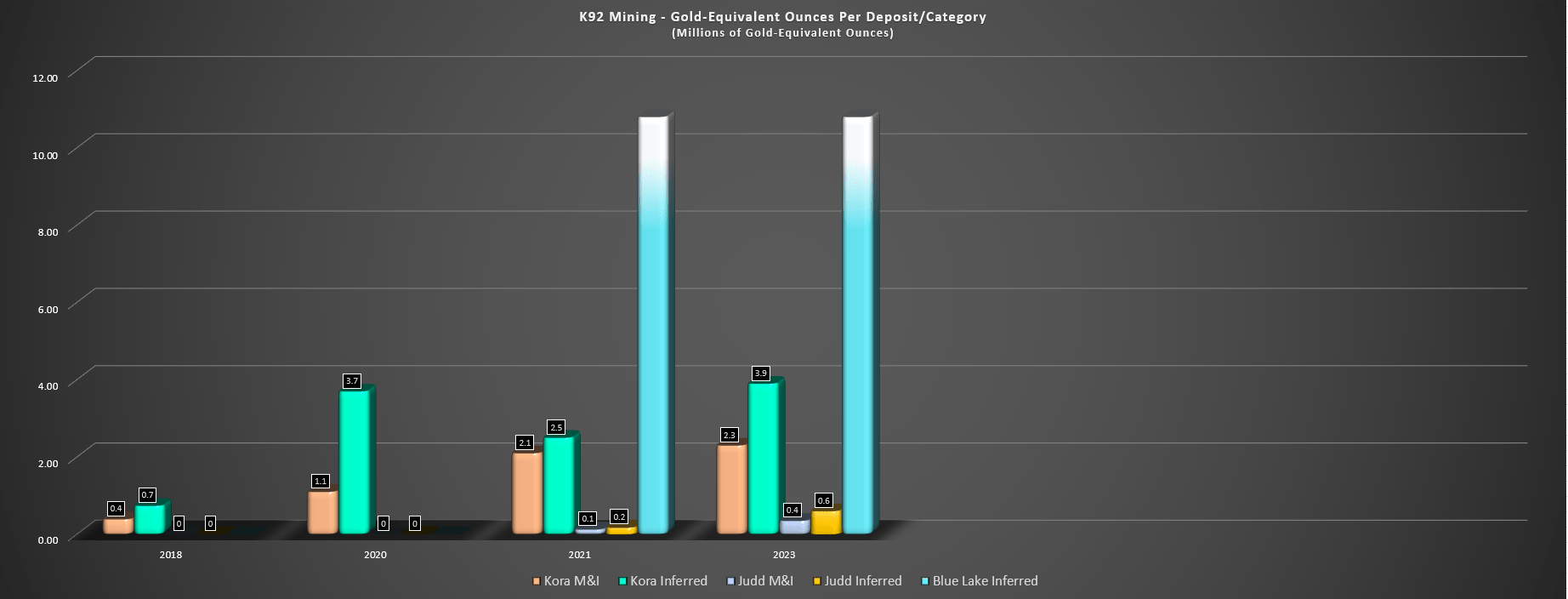

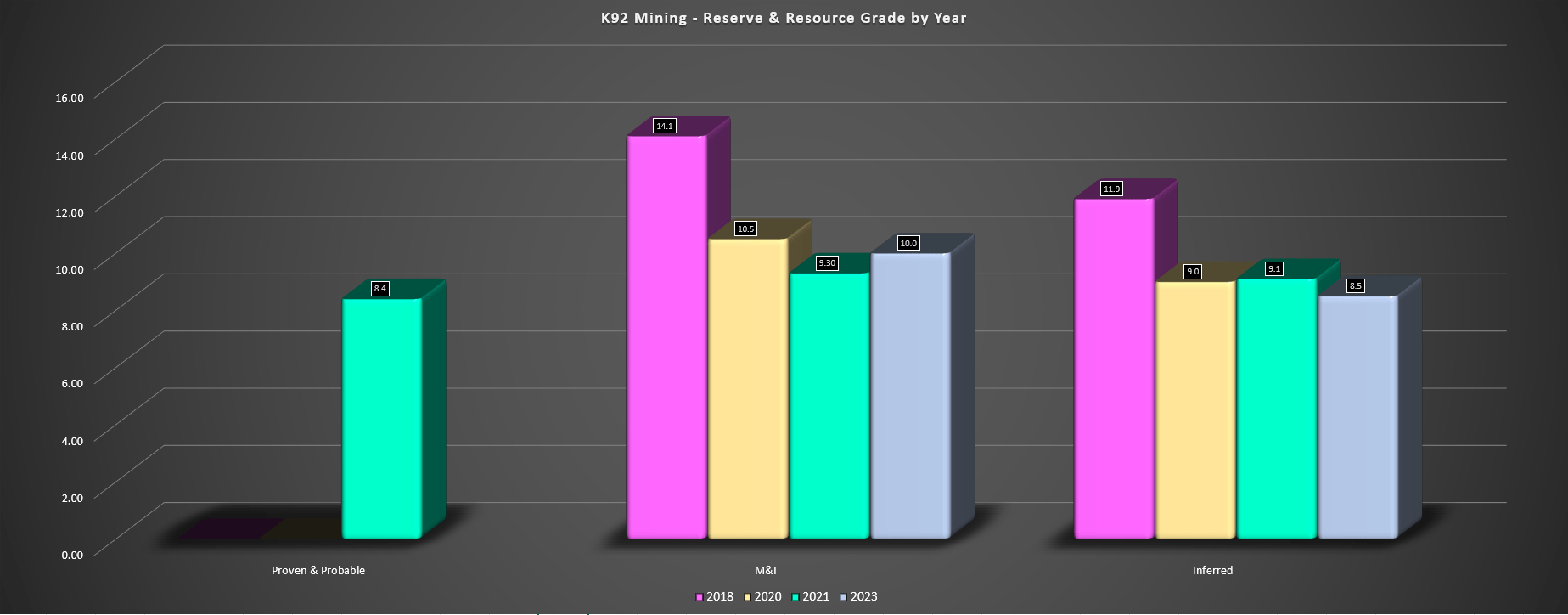

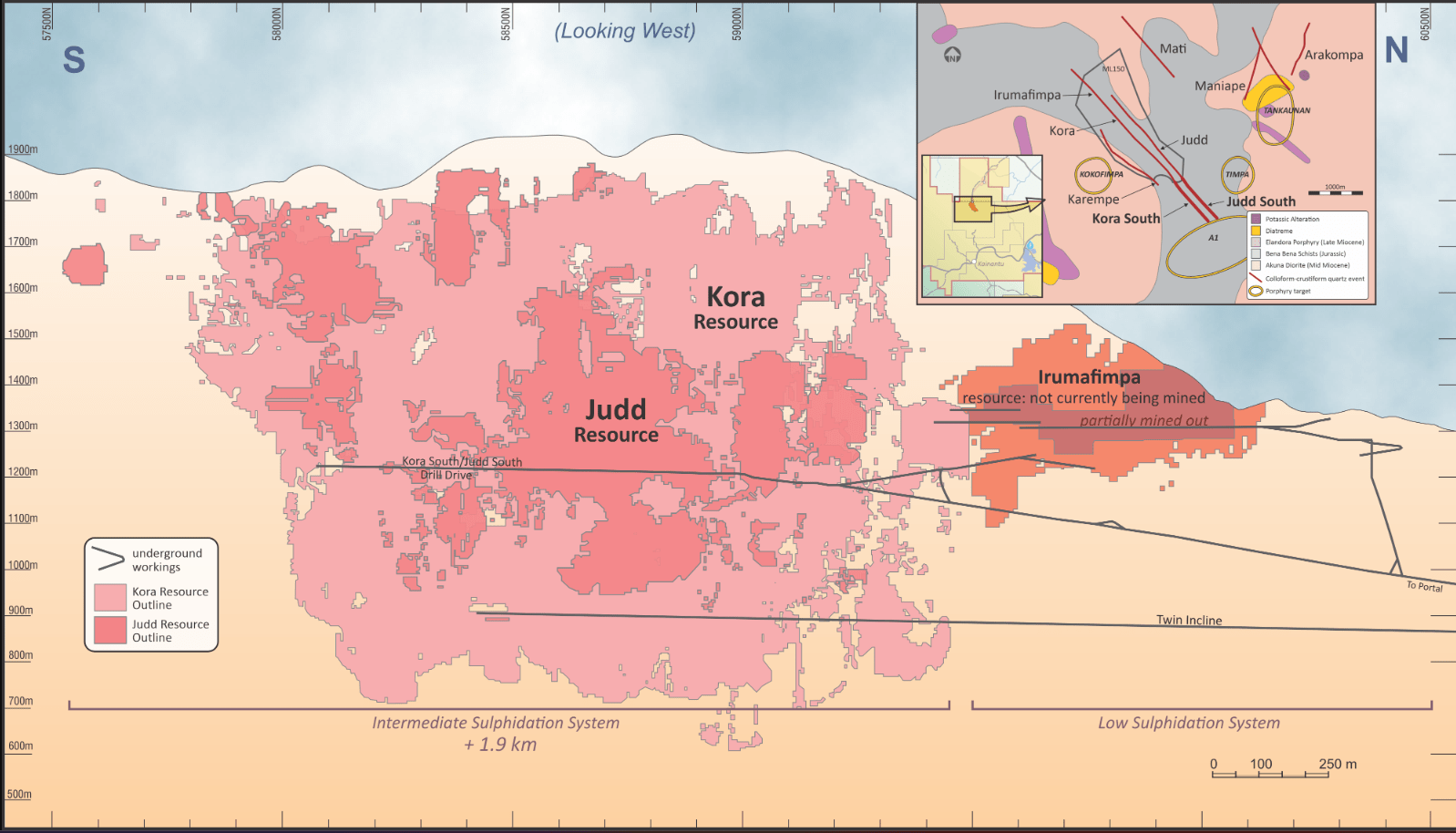

Looking at the above/below charts, we can see that Kora's (main deposit) measured & indicated resource increased to ~2.3 million GEOs at 10.24 grams per tonne gold-equivalent which is net of roughly two years of mining depletion or ~300,000 high-grade ounces at 10.4 grams per tonne of gold, an ~8% increase from ~2.1 million GEOs previously. In addition, Kora's inferred resource soared 58% to ~3.9 million GEOs at 8.60 grams per tonne gold-equivalent, giving the Kora only deposit a total resource of ~6.0 million GEOs (~21.2 million tonnes) at ~9.1 grams per tonne gold-equivalent. Meanwhile, the company's relatively new Judd discovery (small deposit) has grown to critical mass, with its resource increasing from a mere ~130,000 M&I resources and ~180,000 inferred ounces (~0.31 million GEOs total) to ~350,000 M&I resources and ~560,000 inferred resources or 810,000 ounces. The result is that K92's property-wide resource (excluding Blue Lake porphyry) has grown to an impressive ~7.1 million GEOs.

More important than the resource growth and one reason why K92 Mining stands out among its peers is that the company has achieved this growth with minimal share dilution, evidenced by GEOs per share held increasing from ~0.022 to ~0.03 after the updated resource given the minimal share dilution since year-end 2021. This is highlighted on the above chart, showing a steep uptrend in GEOs per share held and cash flow per share, and production per share growth is soon to follow. It's also worth noting that K92 added these ounces at a discovery cost of less than US$7.50, a very attractive figure when this is a mine that should be pulling ounces out at a ~$1,200/oz AISC margin assuming a $1,975/oz gold price. This is even better than Endeavour Mining's ~$25/oz figure and similar to its ~$10/oz figure at Tanda-Iguela.

K92 Mining Current Resource by Category - Company Filings, Author's Chart

{kind=link}

Putting this resource in perspective, this is a massive resource when it comes to high-grade deposits not fully held by majors, comparing favorably to Osisko Mining's main Lynx deposit which holds ~12.1 million tonnes at ~12.1 grams per tonne of gold or ~4.7 million ounces of gold and where a major (Gold Fields) recently came in for half ownership, and Windfall's total resource base of ~7.4 million ounces of gold. It also compares very favorably to Alamos' ~5.3 million ounces of gold at Island Gold at ~12.0 grams per tonne of gold and Lundin Gold's ~8.5 million ounces at 8.2 grams per tonne of gold. The major difference is that all of these companies have billion dollar market caps (and even Osisko with 1/2 ownership of Windfall), yet K92 Mining trades at the lowest market cap of the group yet should be the highest-margin producer sector-wide in 2026 with all-in sustaining costs [AISC] below $700/oz and a production profile closer to ~360,000 GEOs (increasing to 400,000+ GEOs in 2027).

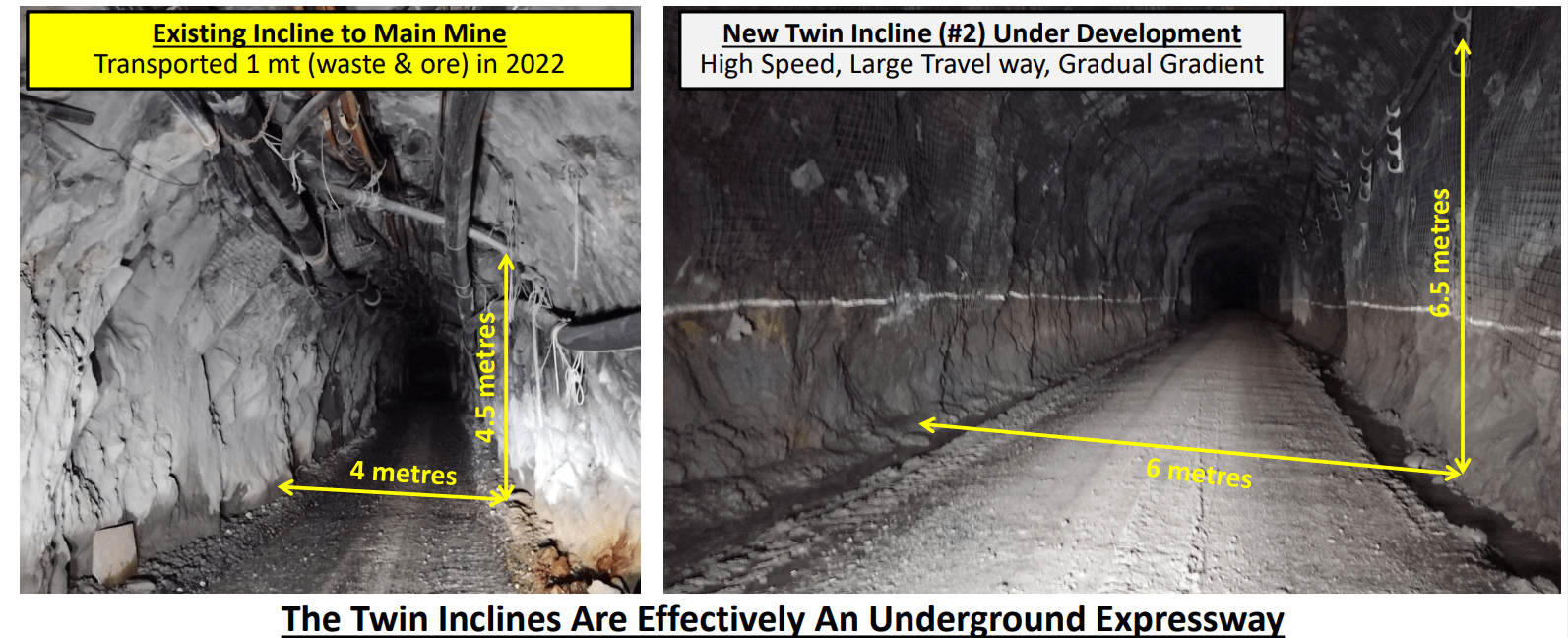

New Twin Incline For Ore Transport - Company Website

{kind=link}

Moving over to grades, we saw grades hold up relatively well with average M&I grades up year-over-year to ~10.0 grams per tonne gold-equivalent, while inferred resource grades dipped slightly to 8.5 grams per tonne gold-equivalent. This can be partially attributed to mining out some of the higher-grade material in the previous resource (~300,000 ounces at 10.4+ grams per tonne of gold) and the addition of the new dilatant zones which are significant from a tonnage standpoint but slightly lower grade. Still, with conservative operating costs of ~$130/tonne and ~$158/tonne with sustaining capital which I have modeled ( K92's 2022 study assumes ~$107 tonne or ~$125/tonne with sustaining capital ) and an average rock value of ~$530/tonne at a $1,950/oz gold-equivalent price, even the inferred resources are extremely attractive and high margin (M&I resources carry a rock value of ~$630/tonne). Finally, it's encouraging to here that reconciliation continues to be in line with expectations, with a 1% difference in gold ounces between mill feed and the updated resource model.

K92 Mining - Reserve & Resource Grade by Year - Company Filings, Author's Chart Kainantu Updated Resource - Company Website

{kind=link}

{kind=link}

While all of this news is very positive, there's a few points worth making:

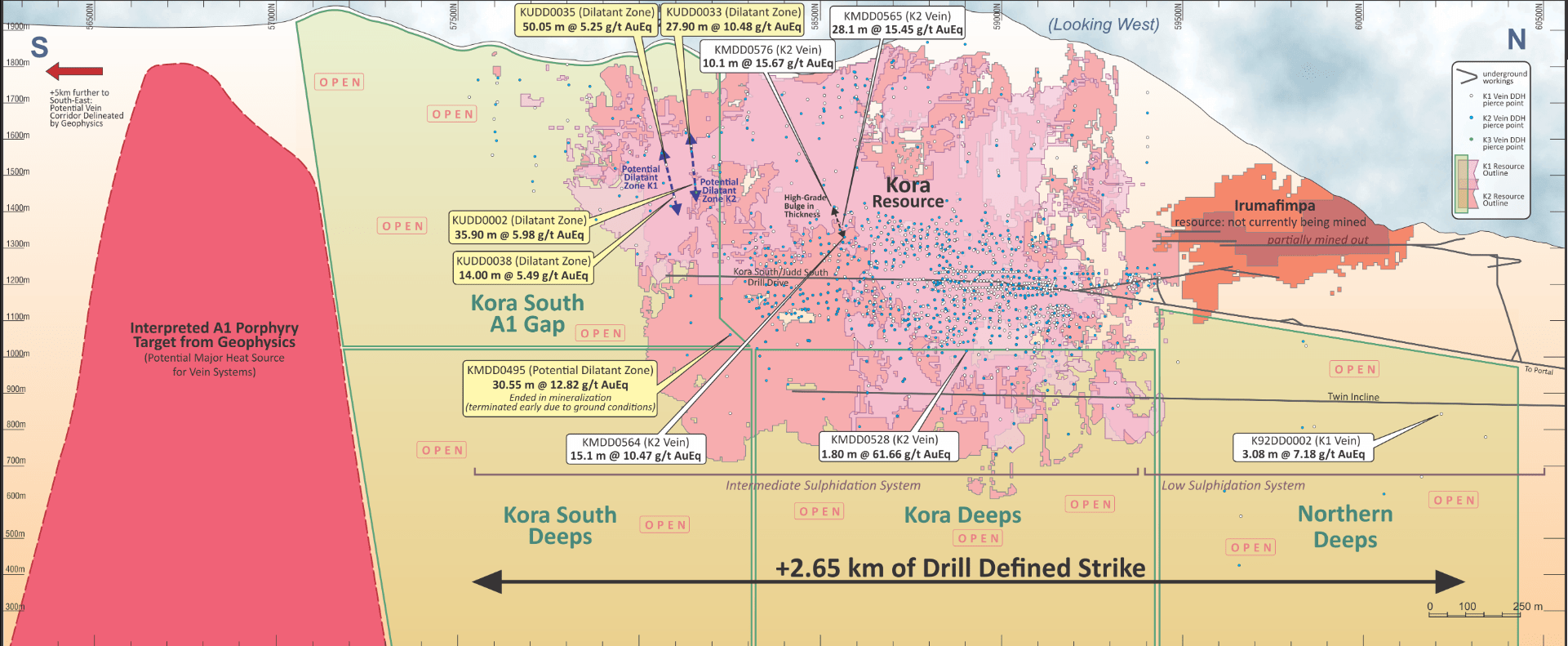

1. Drilling is expected to ramp up at Kora South Deeps and Judd South Deeps next year, and we've already seen multiple high-grade intercepts including 5.05 meters at 12.51 grams per tonne gold-equivalent, 1.47 meters at 11.70 grams per tonne gold-equivalent, and 2.0 meters at 6.94 grams per tonne gold-equivalent. This potential high-grade zone sits just 50 meters from the near fully constructed twin incline, and we can see there are no resources present in this area to date. And with similar grades being intersected at depth and an impressive hit rate for mineralization, I certainly wouldn't rule out the potential for additional 500,000+ GEOs to be added at depth, pushing total resources closer to 8.0 million GEOs with just deeper targets alone.

K92 also noted that channel sampling from an area previously believed to be waste hit 4.6 meters at 14.89 grams per tonne gold-equivalent and 6.8 meters at 11.77 grams per tonne gold-equivalent.

K92 - Resource Upside At Kora Deeps, Northern Deeps & Kora South Deeps - Company Website

{kind=link}

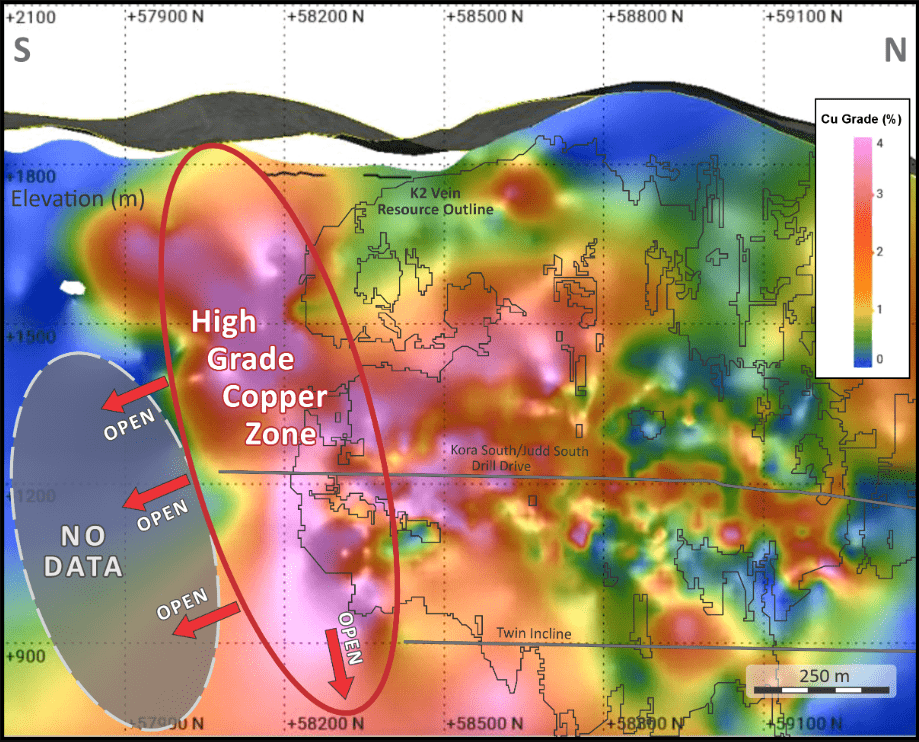

2. The company still has an opportunity to increase resources to the south of its current resources towards what it believes could be a higher-grade porphyry than Blue Lake (Blue Lake already hosts ~10.8 million GEOs at lower grades. In addition, the company remains confident that it could have a mid-grade porphyry on its hands that's higher-grade than Blue Lake, and drill results closer to this area certainly support this with a high-grade hit of 8.50 meters at 6.43% copper, 4 ounces per tonne of silver and 0.60 grams per tonne of gold and another highlight intercept of 10.80 meters of 3.8% copper, 1.85 grams per tonne of gold and 5 ounces per tonne of silver. I am not modeling upside from a mid-grade or high-grade porphyry and the real story here is the high-grade gold, but this is certainly a nice kicker to an already very undervalued company.

Improving Copper Grades South Of Kora Main - Company Website

{kind=link}

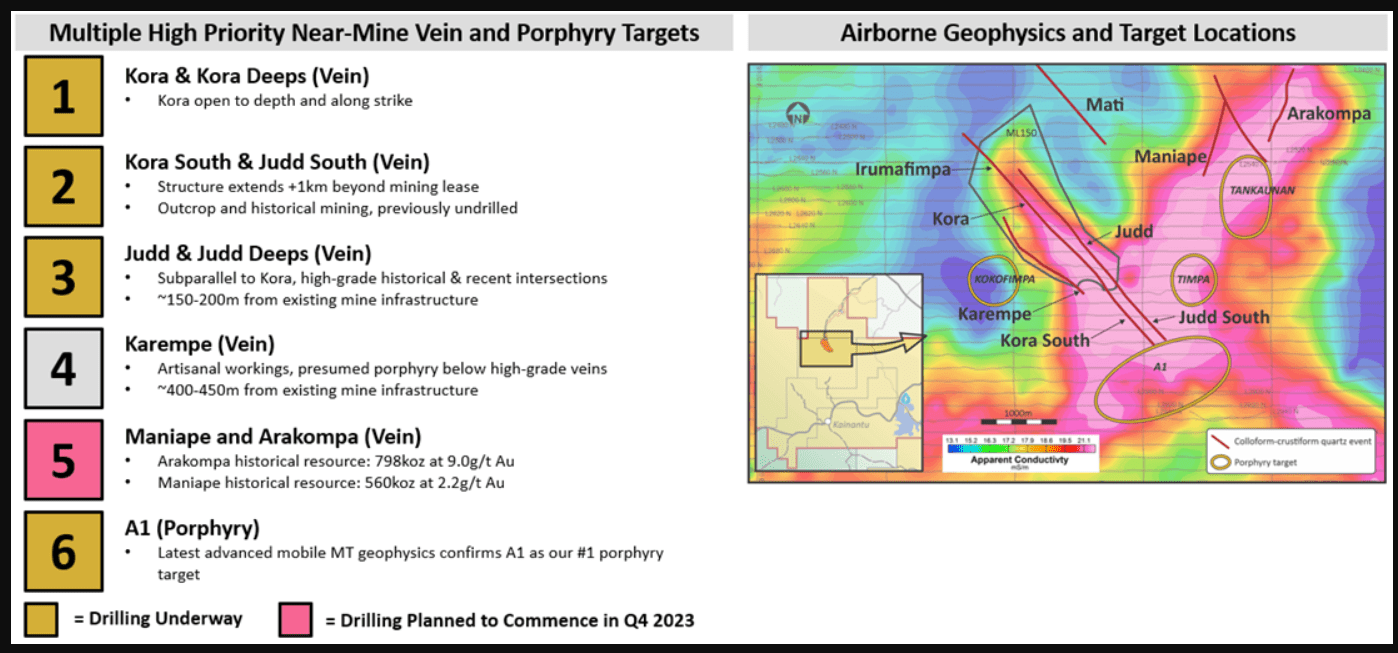

3. There are multiple other gold targets that include Maniape and Arakompa just northeast of its mining lease, with the former being a high-grade open-pit target (560,000 ounces at 2.2 grams per tonne of gold), and the latter having a historical resource of ~798,000 ounces at an average grade of 9.0 grams per tonne gold. Meanwhile, the Karempa Vein is another gold target that sits less than 500 meters from existing infrastructure running parallel to Judd and Kora with a 2.0 kilometer strike length (five known veins that are steeply dipping with a north-south trend). Karempe is believed to be a intrusive related gold-copper-silver epithermal vein system similar to Kora and highlight intercepts include 2.45 meters at 40.18 grams per tonne gold-equivalent and 3.20 meters at 18.28 grams per tonne gold-equivalent from the KA1 vein .

K92 Mining Airborne Geophysics - Company Website

{kind=link}

Last but not least, we can see that geophysic surveys completed have shown a strong correlation between known mineral deposits and conductivity, with the areas of high conductivity (red/pink) yielding deposits of impressive size and grades to date. However, the resistivity zone that lines up with Kora and Judd continues well past the A1 porphyry target to the southeast for over a kilometer, and this resistivity signature is just as significant to the east at Arakompa and Maniape. Hence, if K92 Mining has been able to prove up over 7.0 million GEOs in just a small area of focus near its mining lease and there's already known mineralization at Karempe, known historical resources at Maniape/Arakompa, but with no real drilling done by the company given that it's been busy with Kora/Judd, this project could ultimately host closer to 10.0+ million GEOs, making it one of the largest high-grade deposits globally, even among those held by majors.

To summarize, I remain comfortable with my view that K92 Mining can prove up a ~4.0+ million GEO reserve base, which translates to an After-Tax NPV (6% discount rate) of ~$2.4 billion at a $1,925/oz gold-equivalent price assumption and uses slightly higher mining/processing and G&A costs than K92 Mining has assumed in its study to be more conservative.

Q3 Results Takeaways

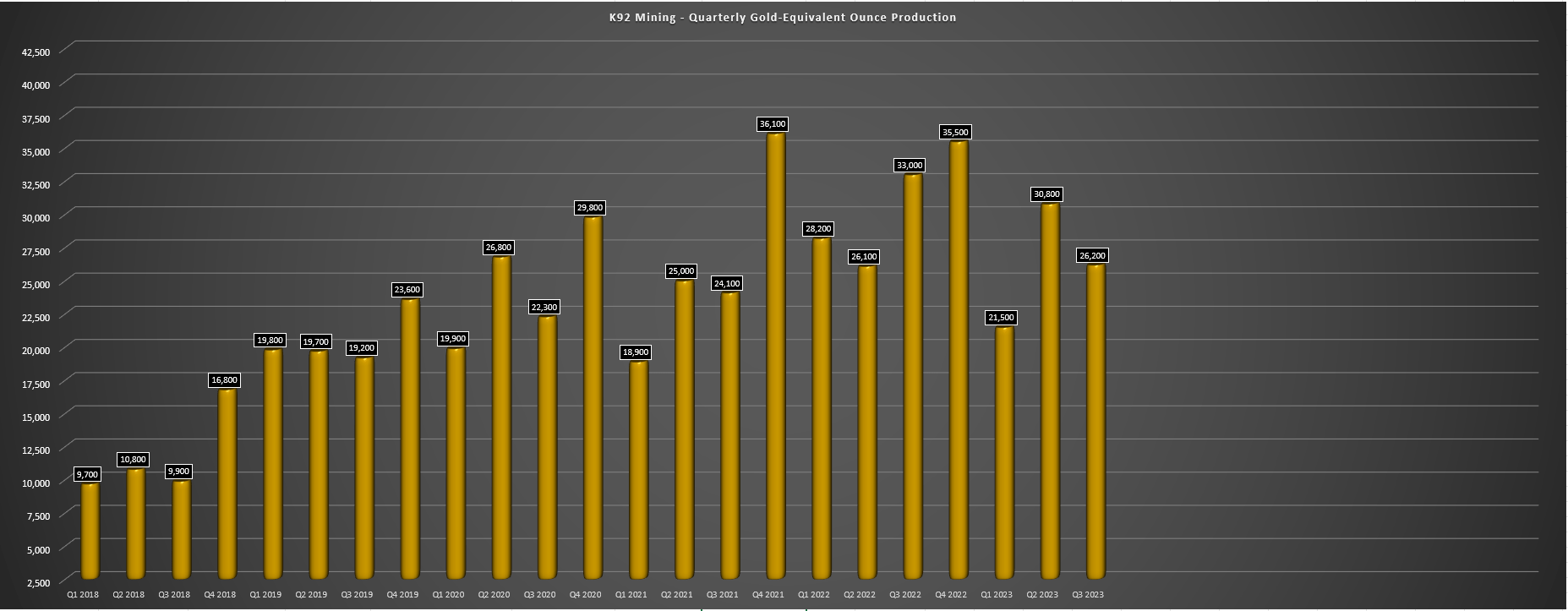

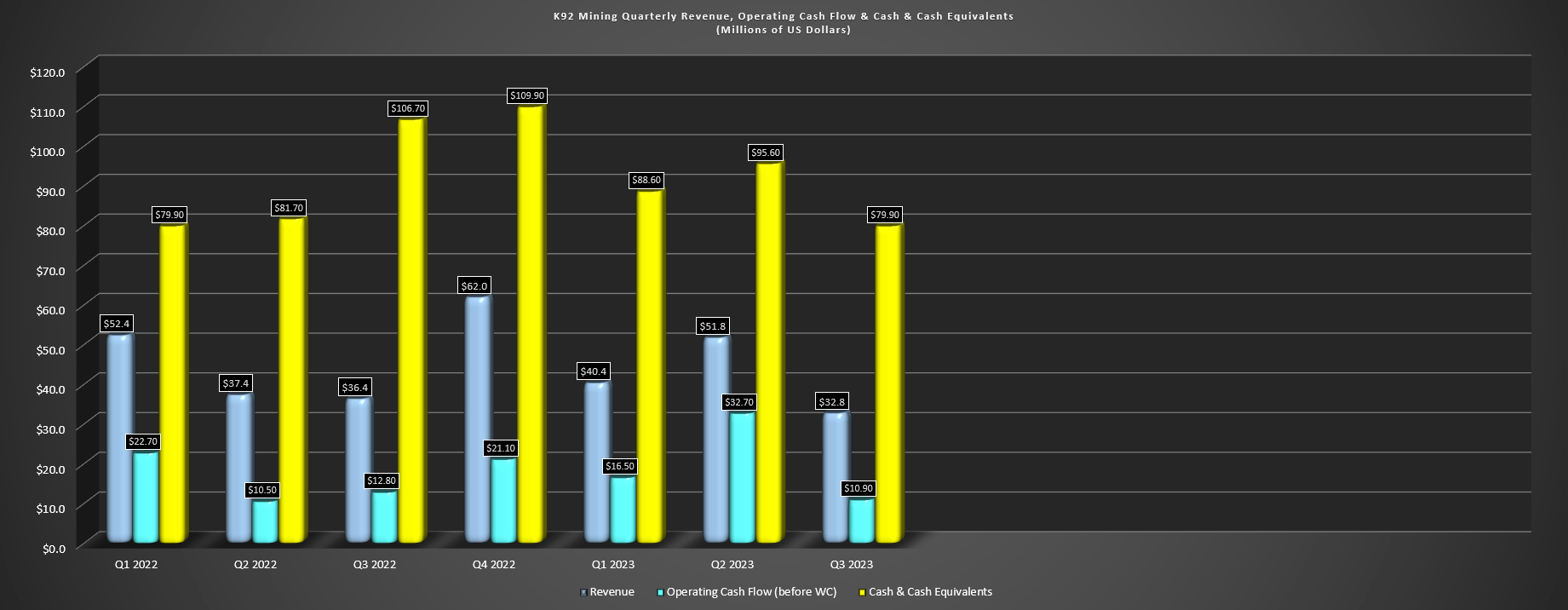

In the results, lower production and sales obviously translated to weaker results, with $32.8 million in revenue (Q3 2022: $36.4 million), $10.9 million in operating cash flow, and AISC margins of $548/oz vs. $754/oz last year. However, it's important to note that the rise in costs ($1,300/oz vs. $909/oz) was mostly related to the lower denominator (much fewer ounces produced than sold) and higher sustaining capital year-over-year. These ounces that didn't get sold ($7.4 million in dore inventory) will benefit the Q4 results and Q4 is shaping up to be a great quarter it looks like, with the CEO noting "we're pretty happy with where we so far in Q4" , and sharing that gold grades are likely to be at or above 8.0 grams per tonne of gold in Q4, and gold-equivalent grades are expected to be above 9.0 grams per tonne gold-equivalent it seems, a significant step up from 6.2 grams per tonne of gold in Q3 due to reliance on stockpiles.

Plus, it's important to note that this mine is capable of sub $800/oz AISC once expanded, so there's zero reason to be worried about costs following one of the company's weakest quarters with much fewer ounces sold vs. produced.

K92 Mining Quarterly Production - Company Filings, Author's Chart

{kind=link}

On the cash balance, despite significant spending year-to-date (~$69 million) to work towards its Stage 3 Expansion (expected to be completed in Q1 2025, and will push production to 300,000 GEOs), K92 has one of the stronger cash balances sector-wide with ~$80 million in net cash, allowing it to self-fund its massive growth (~120k GEOs to 400k+ GEOs) with no share dilution. This is also during a period of aggressive exploration to grow reserves, with 11 rigs on site and the exploration budget increased to $20 million from $14.5 million (over $15 million spent year- to-date).

K92 Mining - Operating Cash Flow & Cash/Cash Equivalents - Company Filings, Author's Chart

{kind=link}

There were also several other positive takeaways:

1. The company reiterated that 1.2 million tonnes per annum for Stage 3 plant looks conservative and that 600,000 tonnes per annum looks possible for Stage 2A plant (designed for ~500k tonnes per annum), suggesting that 1.8 - 2.0 million tonnes per annum once in Stage 4 is a possibility vs. the 1.7 million tonne per annum plans. Importantly, every 100,000 tonnes at 8.0 grams per tonne gold-equivalent is worth ~24,000 GEOs per year and will drive unit costs even lower than sub $800/oz assumptions.

"Optimization efforts are ongoing, including to increase throughput that we believe has the potential to be materially greater than its nameplate design."

- K92 Mining CEO, John Lewins, Q3 2023 Conference Call

2. The CEO stated that the resource is due for this quarter and that the Judd deposit (much smaller deposit) will "increase by multiples", suggesting the potential for considerable resource growth in this parallel mining area to the main Kora deposit. This is significant because it is parallel to existing infrastructure, providing greater operational flexibility next to areas already developed. In addition, the company is already drilling a potential mid to high grade porphyry to the south (A1 was Barrick's favorite prospective target before it sold the project), and K92 also plans to start drilling the high-grade Arakompa deposit before year-end, with ~800,000 ounces at ~9.0 grams per tonne gold in historical resource, suggesting a busy few months for drilling results in new areas.

2. Annual production has the potential to come in at the top end of guidance with costs at the low end.

Assuming ~1,550 tonnes per day processed in Q4 and a grade of 9.0 grams per tonne gold- equivalent with 92.5% recoveries, K92 Mining should produce at least 38,000 GEOs in Q4, which on top of 78,500 places K92 Mining just above the top end of guidance (116,000 GEOs). Meanwhile, AISC year-to-date is sitting in the bottom third of guidance ($1,214/oz) despite the strongest Q on deck, suggesting a beat on the guidance mid-point is highly likely even if sustaining capital remains elevated at $10+ million in Q4.

1,550 tonnes per day might be a stretch (implies annualized rate of 565,000 tonnes), but with multiple days above 1,800 tonnes per day in October and a record above 2,000 in October and September averaging 1,584 tonnes per day, I think 1,550 is quite doable in Q4 so it will be all about grades. A grade of 9.0 grams per tonne of gold looks doable, with the potential for a slight beat there, so K92 Mining is set up to come in at the top or above the top of its revised guidance.

3. Exploration

"We are progressing on multiple fronts, with a total of 11 drills operating at the Kora-Kora South, Judd-Judd South vein systems and the A1 porphyry. We expect to provide another extensive exploration update shortly."

- K92 Mining CEO, John Lewins, Q3 2023 Conference Call

This increase to the exploration budget ($10.1 million year-to-date vs. $6.7 million in H2 2022) is quite encouraging given that this is an asset that continues to give, it boasts a high hit rate, and I would compare the situation somewhat to Osisko Mining (OBNNF). The similarity between the two companies is that both have aimed to step out in the past regionally given the potential but the high-grade intercepts near-mine have been so significant that it's tough to justify taking drills off of the main area. However, with a strong balance sheet and a larger production profile to finally support this exploration, we are seeing drilling ramp up, with confirmation that drills are present at multiple targets, suggesting a newsflow packed next few quarters.

This leads me into one important aspect of the story that might be overlooked, but that truly makes K92 Mining special, which is the exploration upside here. History There's no shortage of management teams that will tell you that they have significant exploration upside in this sector, and while many are telling the truth, the key is focusing on those deposits that have the most upside, the cash position to surface that value, and the infrastructure to take advantage of that upside.

Exploration Upside

The most recent point on exploration leads me into one important aspect of the story that might be overlooked, but that truly makes K92 Mining special, which is the exploration upside here. And while there's no shortage of management teams that will tell you that they have significant exploration upside in this sector, and while many are telling the truth, the key is focusing on those deposits that have the most upside, the cash position to surface that value, and the infrastructure to take advantage of that upside. And in the case of K92 Mining, I don't know that all investors are aware of how significant this opportunity is, which in my opinion is what makes the current valuation (~$930 million enterprise value) so attractive.

When considering the exploration upside here (~800+ square kilometer land package), it's important to look back at this asset's history, which is quite extensive. As for gold discoveries, these began in 1928 in alluvial gold areas, but modern exploration didn't begin until the 1980s. This resulted in the discovery of the Irumafimpa deposit (just north of current Kora/Judd mining areas), with Highlands Pacific Limited beginning production in 2005. The property was purchased shortly after by Barrick Gold (GOLD) in 2007, who at the time was a ~8.6-million-ounce gold producer with ~123 million ounces of gold reserves, so the company was certainly not fishing for 100,000 to 150,000 ounce gold mines and instead hunting down monster deposits globally. This is why it moved the ~100,000 tonne per annum operation into care and maintenance shortly after it acquired it, given that it acquired the asset for the exploration potential, not the small operation in place at the time.

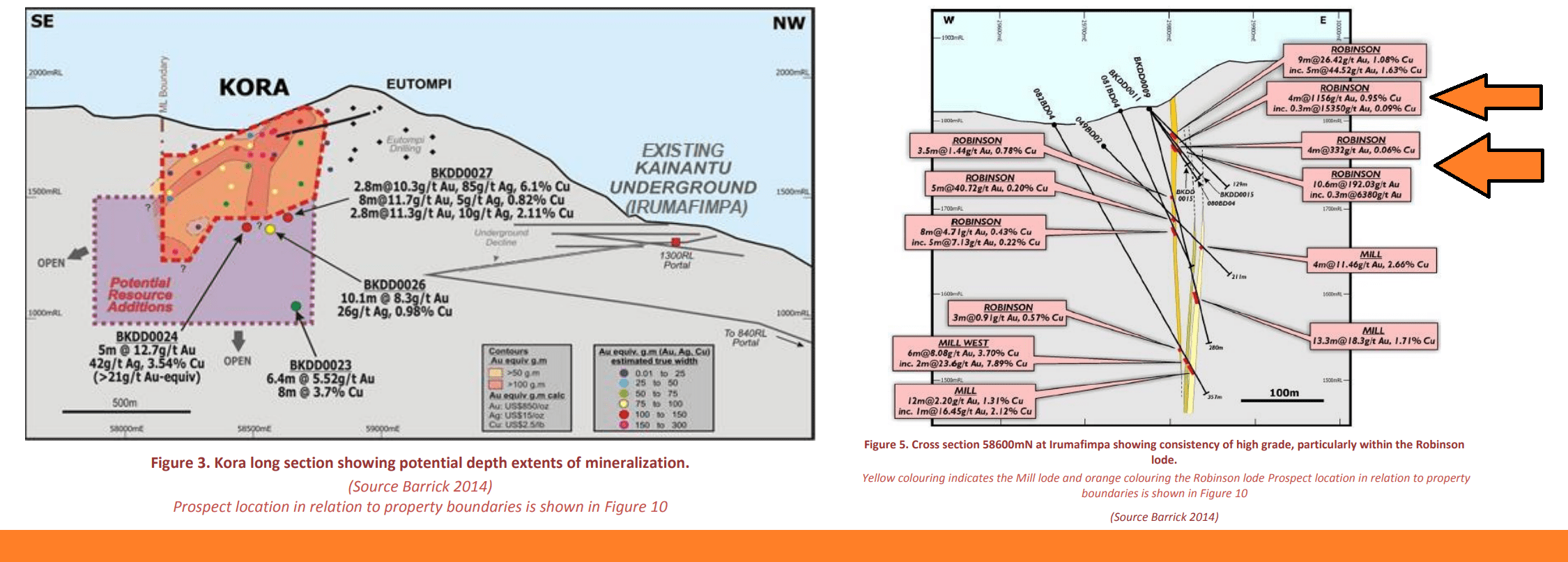

Looking at the below image, Barrick certainly had high hopes for Kainantu (shown with Porgera), with the company referring to Porgera and Kainanatu as "supergiant" targets, in the same class as 20+ million ounce mines like the Golden Mile (Western Australia), Reko Diq (Pakistan) which is one of the world's largest undeveloped copper-gold projects, Goldstrike and Cortez (two of the largest mining complexes globally), Donlin (~40 million ounces of gold resources), and several others. Barrick's stated was focus was on growing the resource base at Irumafimpa-Kora and testing the property for large copper-gold porphyries, and it undertook exploration from 2008 to 2012 (24 holes drilled at Kora). On the gold side, the results were quite solid, confirming the vertical extent of Kora to over 800 meters, and also testing Judd, the high-grade deposit that K92 Mining has since delineated 200 meters east of Kora.

Barrick Gold Supergiant Targets (Including Porgera/Kainantu) - Barrick Presentation

{kind=link}

As shown below, some of the historical intercepts here were spectacular, and even in a decade where high-grade discoveries were more frequent (Fruta Del Norte, Cerro Negro, La Bodega, Goldrush/Red Hill), these intercepts still stood out as some of the best sector-wide. Highlight intercepts from the Robinson Lode at Irumafimpa hit 4 meters at 1156 grams per tonne of gold and ~1.0% copper which are Swan Zone-like results (Fosterville), while two other nearby intercepts hit 10.6 meters at 192 grams per tonne of gold and 4 meters at 332 grams per tonne of gold and 0.06% copper. Meanwhile, highlight intercepts at Judd hit 3 meters at 278 grams per tonne of gold and 0.20%copper.

Barrick Gold Drilling at Kainantu - Company Presentation

{kind=link}

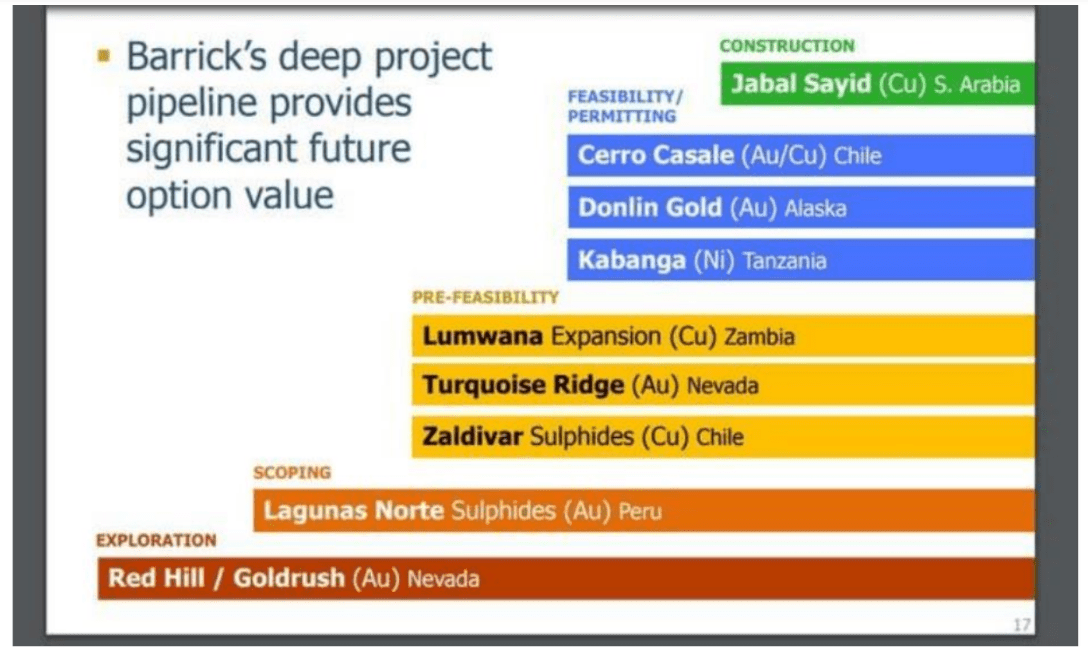

As shown above, Barrick's definition of its deep project pipeline was arguably an understatement at the time following its massive bid for Equinox Minerals (Lumwana & Jabal Sayid). This is because it had Jabal Sayid in construction, Cerro Casale, Donlin, and Kabanga bringing up the rear, and it had just made a significant discovery at the Cortez Complex with Red Hill/GoldRush. Additionally, the massive Pueblo Viejo Mine was in the process of ramping up. And it already had assets like Reko Diq also in the exploration phase. Hence, the company had an abundance of massive development projects that would keep it busy for over a decade if it moved them all through to development and picking where to invest exploration dollars and move assets up its development pyramid was not easy. In the end, Barrick ended up halting exploration at Kainantu, subsequently taking an impairment, and divesting the asset in 2015.

Barrick Gold Historical Pipeline - Company Presentation

{kind=link}

And while a top gold miner letting go of this asset might seem like it discounts the potential here, there are some important points to make:

1. Barrick was looking for monster assets capable of producing at least 300,000 ounces of gold per annum with its production profile at the time (8.0+ million ounces), so even high-grade gold at 10.0+ grams per tonne wasn't going to cut it unless Barrick planned to construct a 1.5+ million tonne per annum plant. And as Barrick stated at the time, it acquired the Kainantu Property, a large part of its focus here was on copper-gold porphyry potential, with the high-grade gold opportunity likely coming in second.

"Barrick has conducted diligence on the properties and plans to embark on a comprehensive exploration program on identified high grade gold vein targets and indicated copper-gold porphyry potential in the district. The Company will also have a fresh look at opportunities at the Kainantu mine".

October, 2007 News Release, Barrick Gold

2. Land access issues at the time were an impediment to exploration activities, and its internal reports ranked the A1 Porphyry Target as its top target on the property. And importantly, access to the A1 target was only available for the six months prior to Barrick stopping exploration and ultimately choosing to divest the project at the bottom of the gold market in 2015. So, Barrick may have potentially given away this project without testing one of the best targets, and leaving behind a very solid gold asset that might have just been a little too small for it at the time. This is corroborated by the following quote at the time of the divestment which stated that "Barrick originally purchased the Kainantu Project for the porphyry Cu-Au potential and internal reports rank the project very highly on a global scale. The decision to divest the project was made for corporate rationalisation reasons based on global competition for exploration expenditure rather than geological reasons."

So, why is this relevant today?

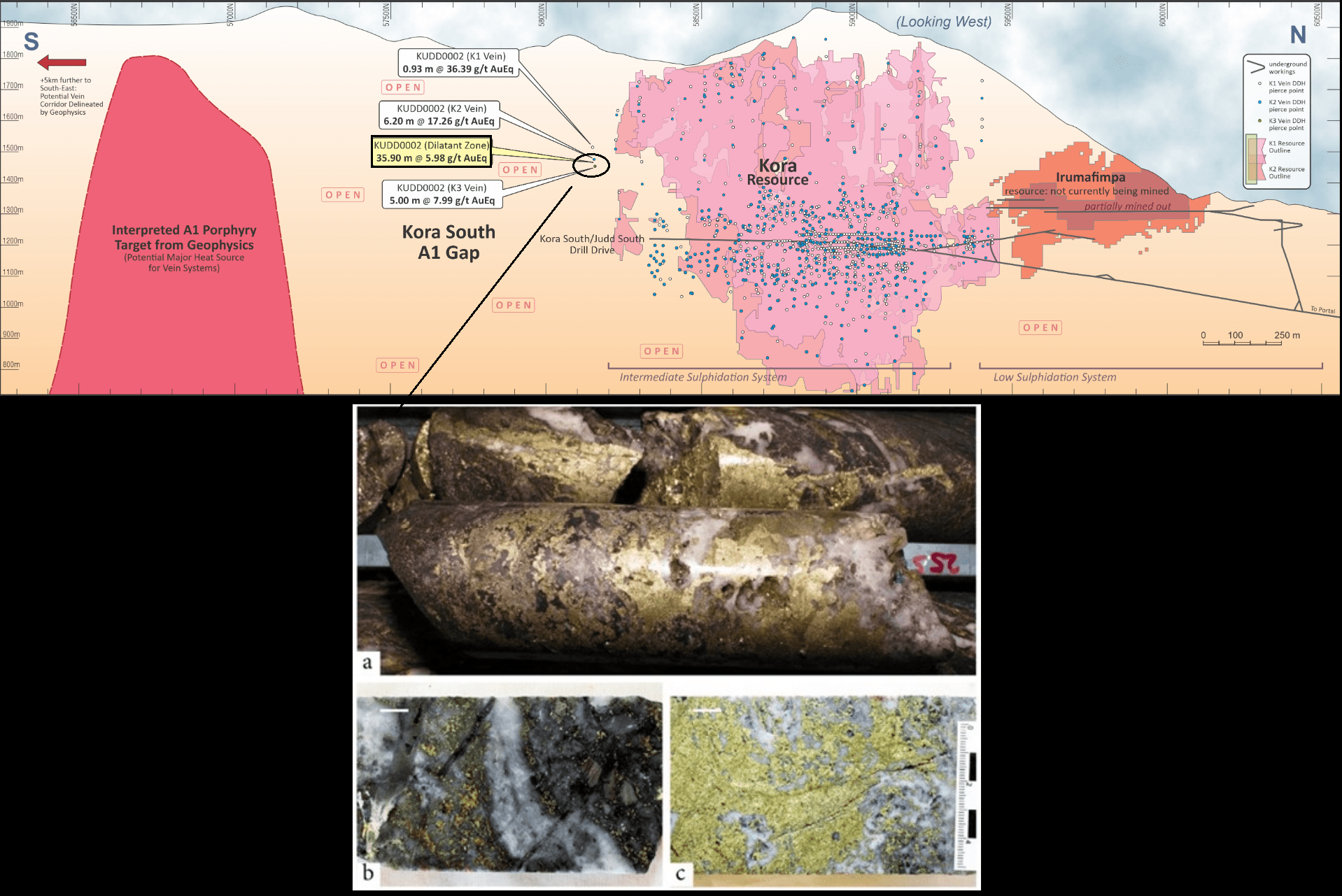

K92 Mining is now finally testing the A1 target just south of its Kora and Judd mining areas, and consultants for Barrick (Corbett and Tosdale) concluded that a Barrick moly in-soil anomaly southeast of the Kora Vein could be a key target, which was referred to the A1 or Billmoia prospect. Corbett concluded that it may represent an intrusion related upflow zone for the Kora/Irumafimpa low sulphidation deep epithermal copper-gold mineralization. And as we've seen from drilling by K92 Mining and mineralization (shown below), copper grades are elevated in this area, suggesting that the A1 porphyry target (also shown below in red) could be a monster.

A1 Porphyry Target - K92 Mining Website

{kind=link}

Plus, given the vicinity to a top-5 gold mine globally by reserve grade, one could certainly make an argument that this could be a mid-grade to high-grade poprhyry, like the monster asset elsewhere in Papua New Guinea: Wafi-Golpu (~160,000 ounces of gold at negative $2,000/oz AISC with by-product credits based on most recent economic study). Image "C" in the aboveimage highlights massive chalcopyrite in cryptocrystalline quartz in drill-hole KUDD-0002 as the company steps out further to the south towards the interpreted A1 porphyry target, with KUDD-0002 hitting 0.61 meters of 4.6 grams per tonne of gold and 19.2% copper. Image "A" highlights massive chalcopyrite and bornite. To summarize, this is a bonus kicker to an alreadyvery attractive investment thesis based on the gold/copper vein systems only at Kora/Judd.

Valuation

Based on ~235 million shares outstanding and a share price of US$4.27, K92 Mining trades at a market cap of ~$1.0 billion (enterprise value of ~$930 million), which leaves it trading at ~0.42x P/NAV based on an estimated NPV (6%) of ~$2.4 billion. This compares quite favorably to other producers like Lundin Gold at over 1.0x P/NAV despite the fact that K92 Mining is likely to be a similarly profitable producer than Lundin Gold in the 2026-2028 period (even after Lundin's planned throughput expansion) with K92 Mining set to produce an average of ~415,000 GEOs at ~$700/oz AISC (2026-2028) while Lundin Gold will produce closer to ~460,000 ounces of gold at ~$850/oz AISC.

The major difference today is that Lundin Gold has the free cash flow to support its valuation and K92 Mining does not, given that K92 Mining still has 18-30 months left before it fully completes its Stage 3/Stage 4 expansions and is spending on growth. However, with ~$265 million in free cash flow in 2026 and this growth being fully-funded by ~$70 million in net cash and consistent cash flow generation during the build, I expect K92 Mining to exit 2026 with net cash despite outlays for capital expenditures ($250+ million) and I expect free cash flow to improve to ~$350 million in 2027 ($2,000/oz gold-equivalent price assumption), growing to $400+ million in 2028. So, with this significant ramp in free cash flow, I expect the re-rating to be fast and furious, especially if the gold price cooperates.

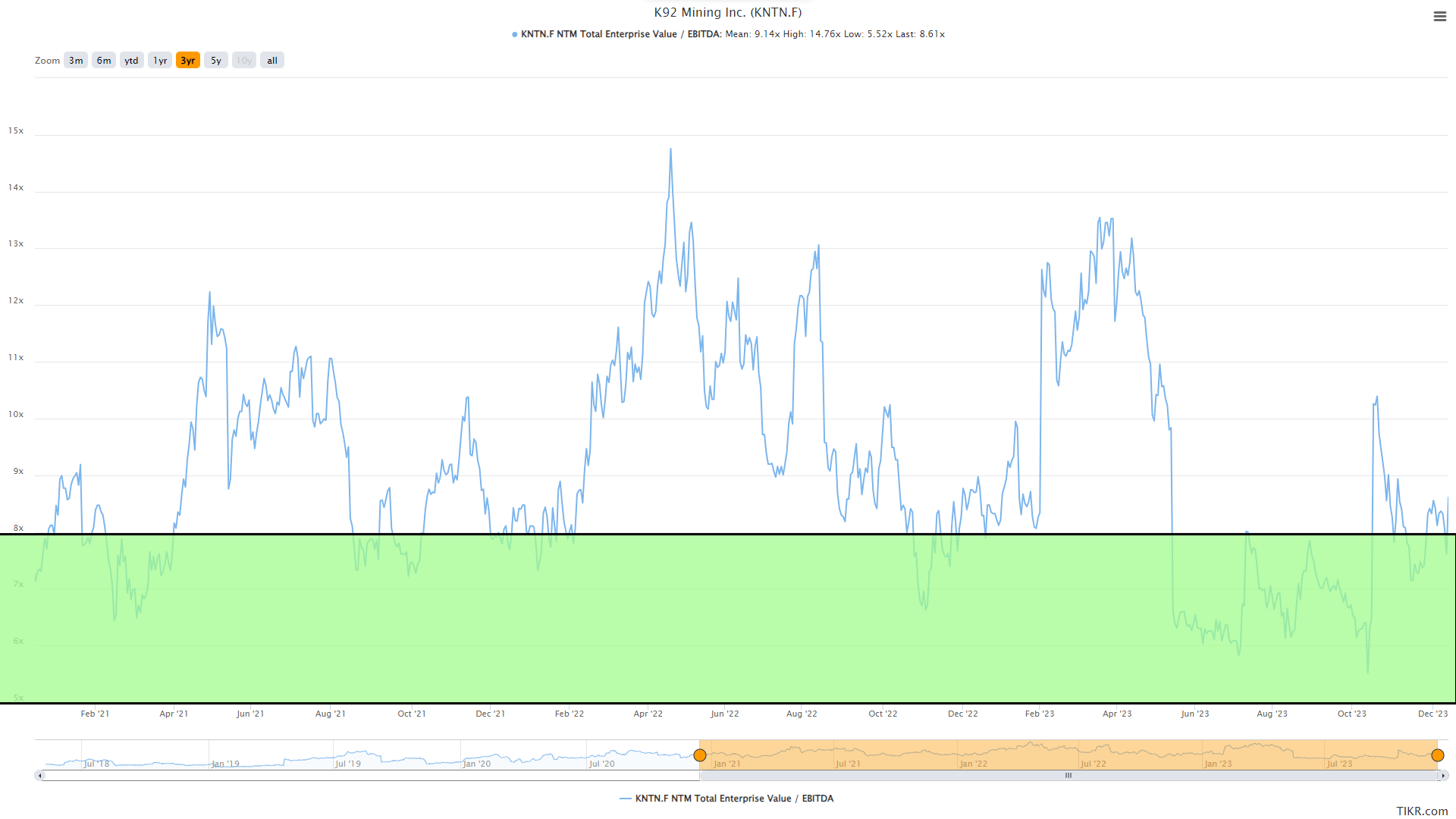

K92 Mining - EV/EBITDA Multiple - TIKR.com

{kind=link}

Even using a very conservative free cash flow multiple of 7.5x for a gold producer with ~65% AISC margins and what will be the sector's lowest-cost producer if it executes successfully [Lundin Gold (LUGDF) traded at 11x EV/FCF at its recent peak], this would translate to a fair value for K92 Mining of ~$1.98 billion in 2026 or US$8.25 on ~238 million shares. At what I believe to be a more fair multiple of 8.5x especially if sentiment returns to the sector, fair value increases to ~$2.25 billion [US$9.40]. Importantly, this would still leave K92 Mining trading at a discount to P/NAV (Lundin Gold has consistently traded at 1.0x to 1.2x), and these targets assume zero upside in the gold price as these free cash flow estimates are based on a $2,000/oz gold-equivalent price.

Summary

With gold looking like a breakout is inevitable, K92 Mining arguably being a top-5 exploration story, a consistent per share grower and a mini-Lundin Gold (~400k ounce producer at industry-leading costs with a high-grade asset). Notably, K92 Mining's growth does not require taking on any meaningful debt to complete its growth plans (at current metals I would expect minimal draws on its credit facility), and I would expect a story like this to come in vogue and trade at a premium valuation if sentiment returns to the sector, especially when there are far worse stories trading at double-digit free cash flow multiples. In summary, K92 Mining continues to be one my favorite ideas with a sub $1.0 billion market cap in the gold space.

Given the combination of a bullish gold price setup and industry-leading growth with unrivaled margins I would not be surprised to see the stock trade above US$8.50 in the next two years and above US$10.00 long-term. Plus, the kicker is the possibility of a takeover as I'm not sure how long larger producers comfy with non-Tier operating jurisdictions can ignore this level of free cash flow and margin improvement that comes with an operation capable of ~400,000+ GEOs at sub $700/oz AISC but at a steal of a valuation (vs. Lundin Gold which is also very attractive price, but is arguably fairly priced at triple K92 Mining's market cap). In summary, I see two paths to a potential re-rating, and I see this pullback in K92 Mining below US$4.30 as a buying opportunity.

For further details see:

K92 Mining: Too Cheap To Ignore