KAI - Kadant: Slightly Overvalued Despite Favorable Trends

2023-07-10 04:22:24 ET

Summary

- Kadant is well-positioned to exploit macro trends from global infrastructure development spending to the need for sustainable packaging.

- The industrial machinery company has an impressive record of growth, but the near-term picture is flattening and the long-term forecast is cloudy.

- In the end, the global favorable market trends cannot rescue KAI stock's valuation.

Investment Thesis

Kadant Inc. (KAI) is well-positioned to exploit a number of favorable long-term macroeconomic trends that will increase demand for their products across all three business segments: flow control, industrial processing, and material handling. However, the near-term growth forecast is flat, and the longer-term picture too uncertain when it comes to both the top-line and operating margins. At the end of the day, the stock looks overvalued from both relative and intrinsic perspectives, which is why I give it a hold rating.

Growth Slowdown

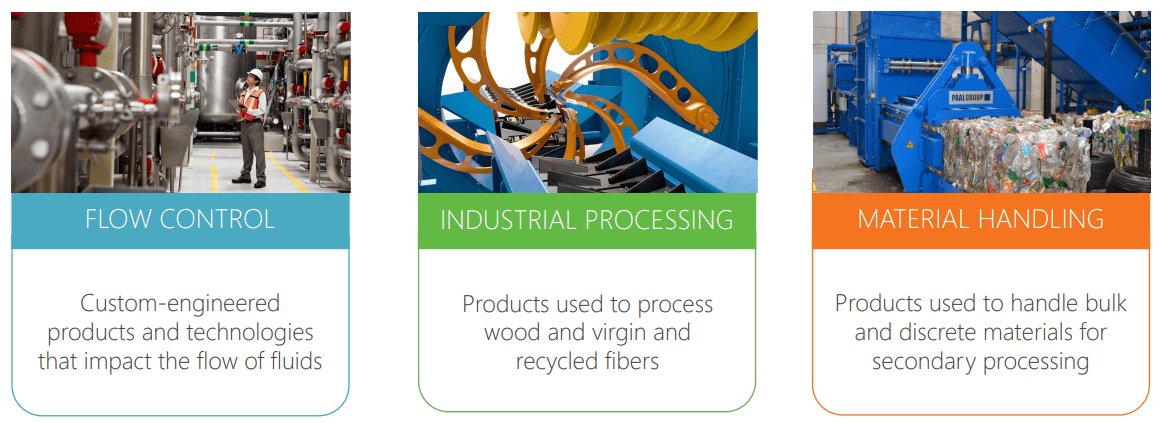

Kadant has three business segments: (1) Flow Control, (2) Industrial Processing and (3) Material Handling. Flow Control accounted for almost 40% of sales in Q123, Industrial Processing 36%, and Material Handling 25%.

Kadant Business Segments (Company Investor Presentation May, 2023)

{kind=link}

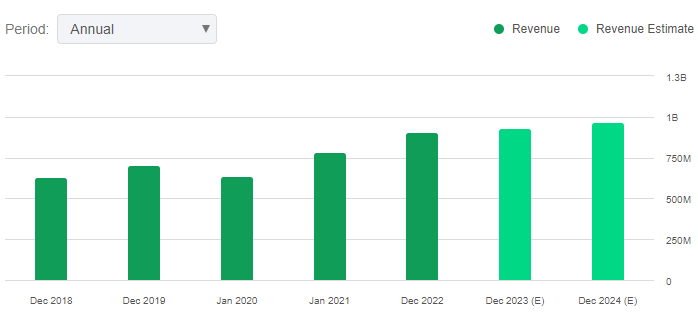

It has almost 20 manufacturing facilities worldwide that combined achieved $905 million in revenue last year. Geographically, the company derived 56% of its revenue from North America, 26% from Europe, 13% from Asia, and 5% from countries in other regions.

Kadant in its May investor presentation has pointed out favorable market trends that could boost the company's long-term revenue.

- For example, U.S. e-commerce sales are expected to grow 16% annually through 2026, which will drive demand for containerboard to produce boxes amid the drive to sustainability. Kadant is number one in global market share for recycled packaging, tissue, debarkers, and stranders.

- Global spending on infrastructure development and critical mineral initiatives are expected to rise substantially, which will boost demand for Kadant's products that increase efficiency in mining and material processing. The company is the market share leader globally for feeders in aggregates and horizontal balers.

- Demand for wood-based buildings, which offer a low-carbon footprint versus concrete or steel, is expected to grow. Housing construction in Europe is starting to transition to wood, a trend that will increase demand for the company's wood processing products.

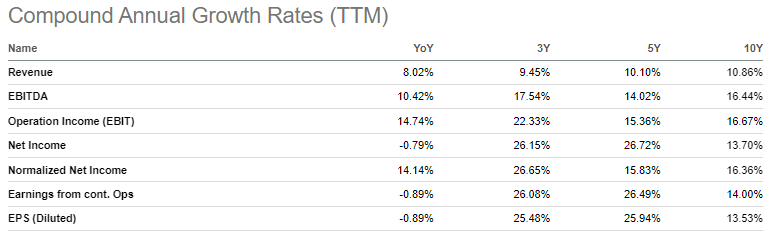

Kadant has an impressive track record of growth across the board, with its sales CAGR at 10.1% over the past five years and EBIT at 15.36%. Meanwhile, revenue is up 8.02% year-over-year in the trailing 12 months and EBIT 14.74%.

{kind=link}

{kind=link}

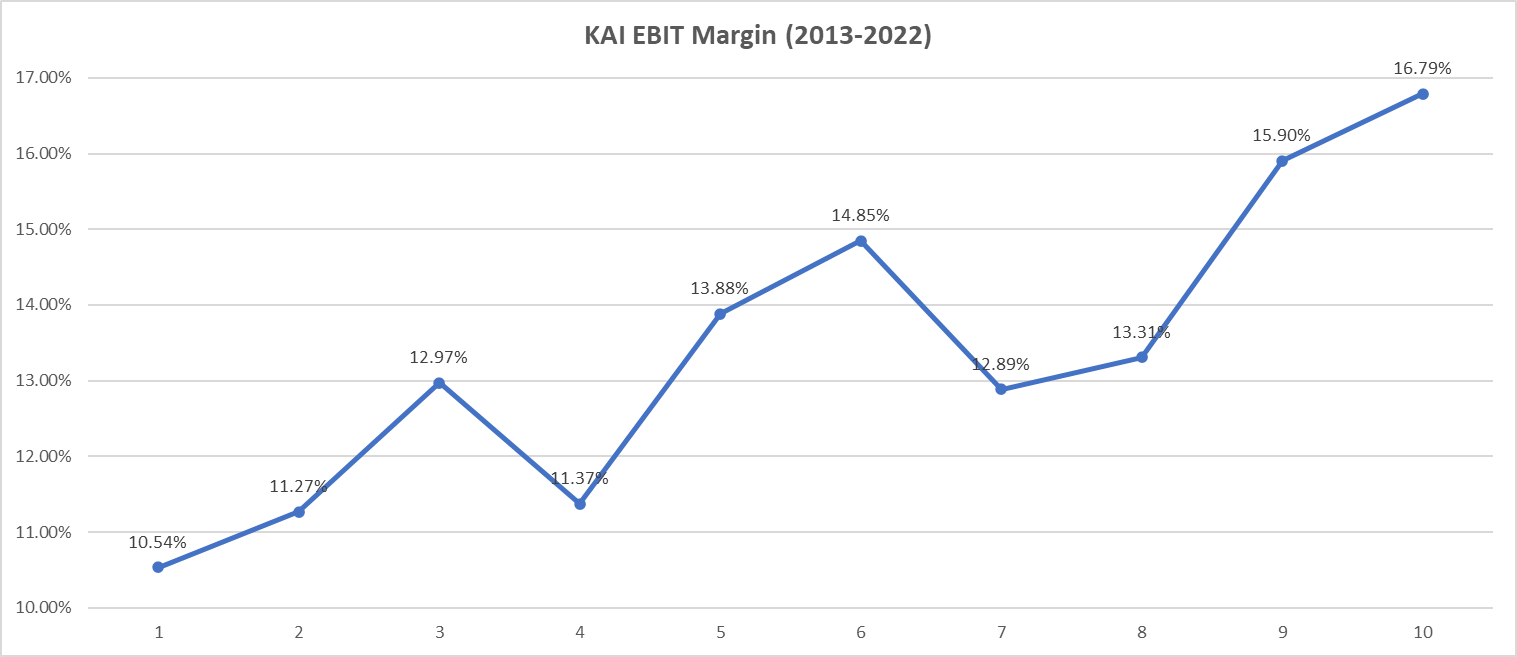

In 2022, the operating margin reached 16.8%, the highest on an annualized basis since at least 2013. The EBIT margin over the trailing twelve months is now at 17.2%.

{kind=link}

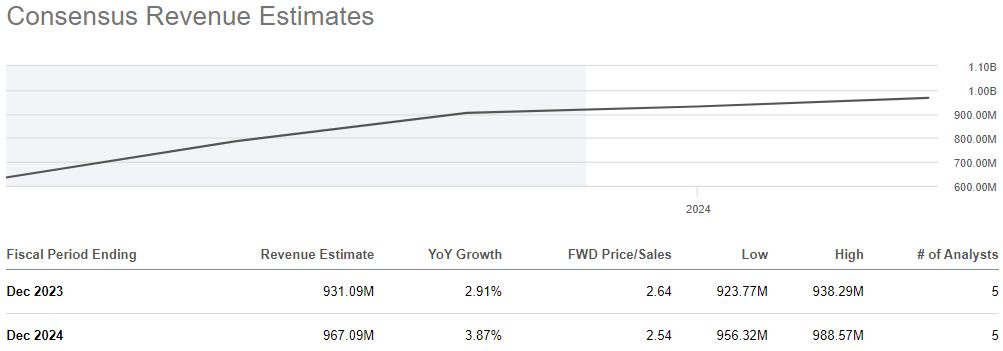

The company however, citing weakening demand in the industrial processing segment, expects the sales growth rate in 2023 to be, at most, 3%, according to company guidance provided in the first quarter. And, five analysts covering the company are also estimating flat growth in 2024 as well.

{kind=link}

Valuation

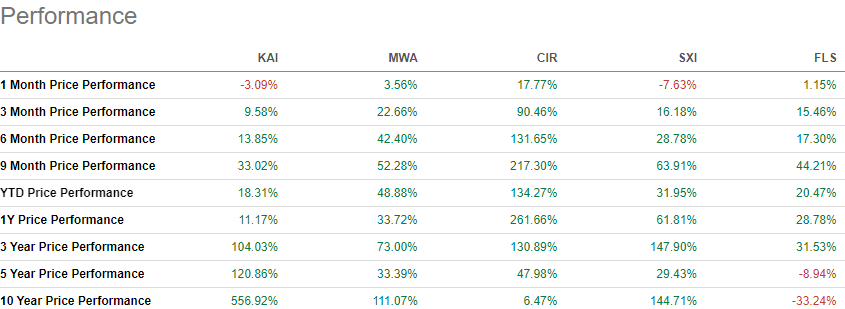

The stock in terms of total returns is up 128% over the past five years, blowing its top rivals in the industrial machinery industry away. However, although Kadant's stock price is up 11% in the past twelve months, it is slightly underperforming the S&P500 average and well below top rivals.

{kind=link}

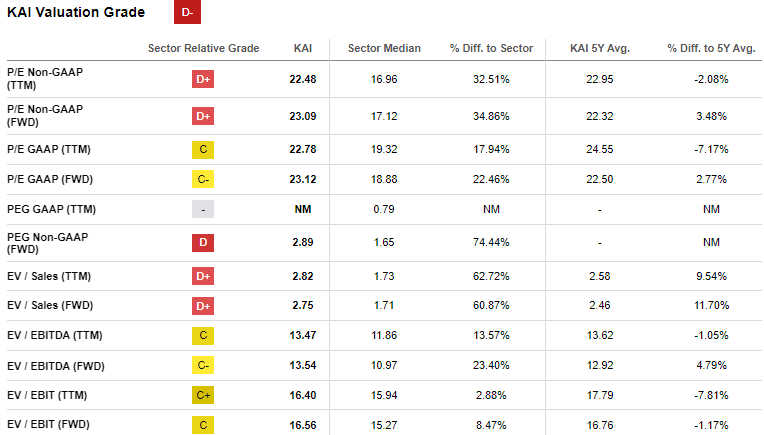

In any event, it appears to have outkicked its coverage, so to speak. From a relative standpoint, KAI looks quite expensive, trading at 22x earnings versus a sector median of about 17. It is also significantly above its industrial peers in EV/EBITDA, EV/EBIT, and PEG ratios, among others.

{kind=link}

Regarding the assumptions behind the key inputs of the intrinsic valuation, I relied on a combination of analyst estimates, historical averages, and industry medians.

Sales Growth - Analysts covering the company forecasted a 3% top line growth rate in 2023 and 4% in 2024, but the projections stop there. Taking into account the macroeconomic trends that could drive demand for their products, including infrastructure and critical mineral spending, e-commerce, and wood buildings, I assumed sales growth would at a minimum reach the 5Y historical average of 10%. In the latter years, I gradually lower the top line growth rate in the direction of the long-term growth rate of the economy.

EBIT Margin - I continued the upward trend and pushed the EBIT margin gradually from 17% to 20%.

Capex - I kept capex at about 3% of revenue, which was slightly offset by D&A, like it has been every year since 2013.

Discount Rate - Finally, the discount rate is based on the 30-year average annual return of the S&P 500, including dividends, rounded up to 10 percent.

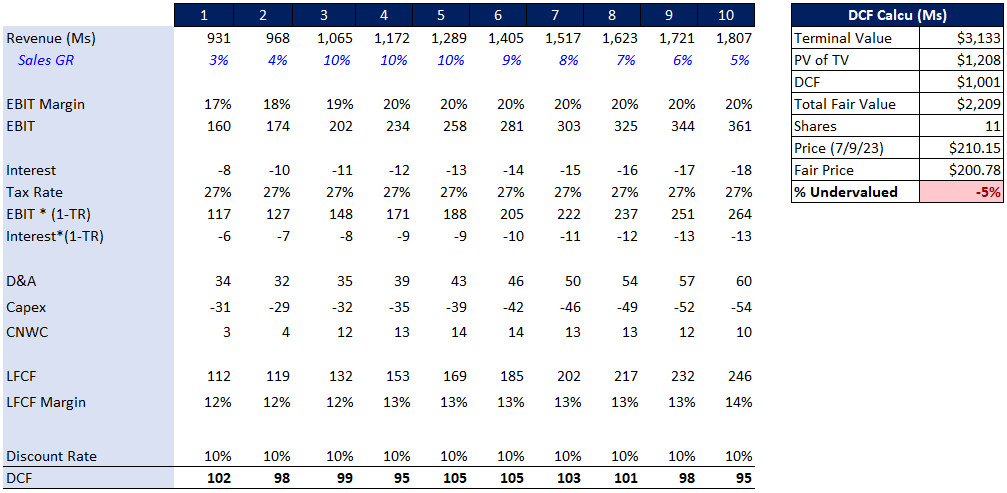

According to the below DCF analysis the stock appears overvalued by 5%.

{kind=link}

EBIT Sensitivity:

- If you plugged in 18% for EBIT for years 5-10, the stock would be overvalued by 15%.

- If you used 22% for years 5-10, the stock would be undervalued by 2%.

Risks

I see risks in two directions vis-à-vis my analysis. On the one hand, I may have underestimated the long-term growth rate and the stock is not overvalued, which would lead to opportunity costs.

However, I believe the risks of holding onto the stock should be weighed even more heavily. A large portion of the company's revenue relies on customers buying large capital equipment, investments that are hard to predict and at more risk amid economic uncertainties. Macro demand drivers may not materialize, including with respect to e-commerce, critical mineral projects, and infrastructure development. As a result, long-term sales growth may be flatter than anticipated.

Conclusion

Kadant is well-positioned to exploit a number of favorable long-term macroeconomic trends that will increase demand for their products across all three business segments: flow control, industrial processing, and material handling. However, the near-term growth forecast is flat, and the longer-term picture too uncertain. As a result, the stock as priced today looks intrinsically overvalued by about 5%, which is why I rate it a hold.

For further details see:

Kadant: Slightly Overvalued Despite Favorable Trends