KLR - Kaleyra: More Clarity Needed (Rating Downgrade)

Summary

- Kaleyra is down nearly 90% in the past year.

- The CPaaS industry is still a compelling market that continues to expand rapidly as companies shift to digital channels.

- Its latest earnings result showed deteriorating growth and profitability as macro headwinds weigh.

- The current valuation is cheap but execution and the macro environment are also two huge risks and uncertainties.

- I rate KLR stock a hold.

Investment Thesis

Since my last coverage on Kaleyra ( KLR ), the company got absolutely decimated with the stock price down nearly 80% in just 10 months. The company's fundamentals remain intact and the valuation is cheap, but there are also macro headwinds to be cautious about. The adoption of CPaaS (communications platform as a service) is still in the early stages and should continue to grow over time. The acquisition of mGage and Bandyer also provided significant assets for the company.

However, the macroeconomy has weakened significantly which impacted my buy thesis and the company's performance. It recently reported its fourth-quarter earnings and the results are pretty soft, with revenue growth being weak and the bottom line worsening. The current valuation is very compelling as it is trading at a significant discount compared to peers, but execution risks remain. There are too many uncertainties right now, therefore I am downgrading the company to hold and will wait for more clarity.

Background

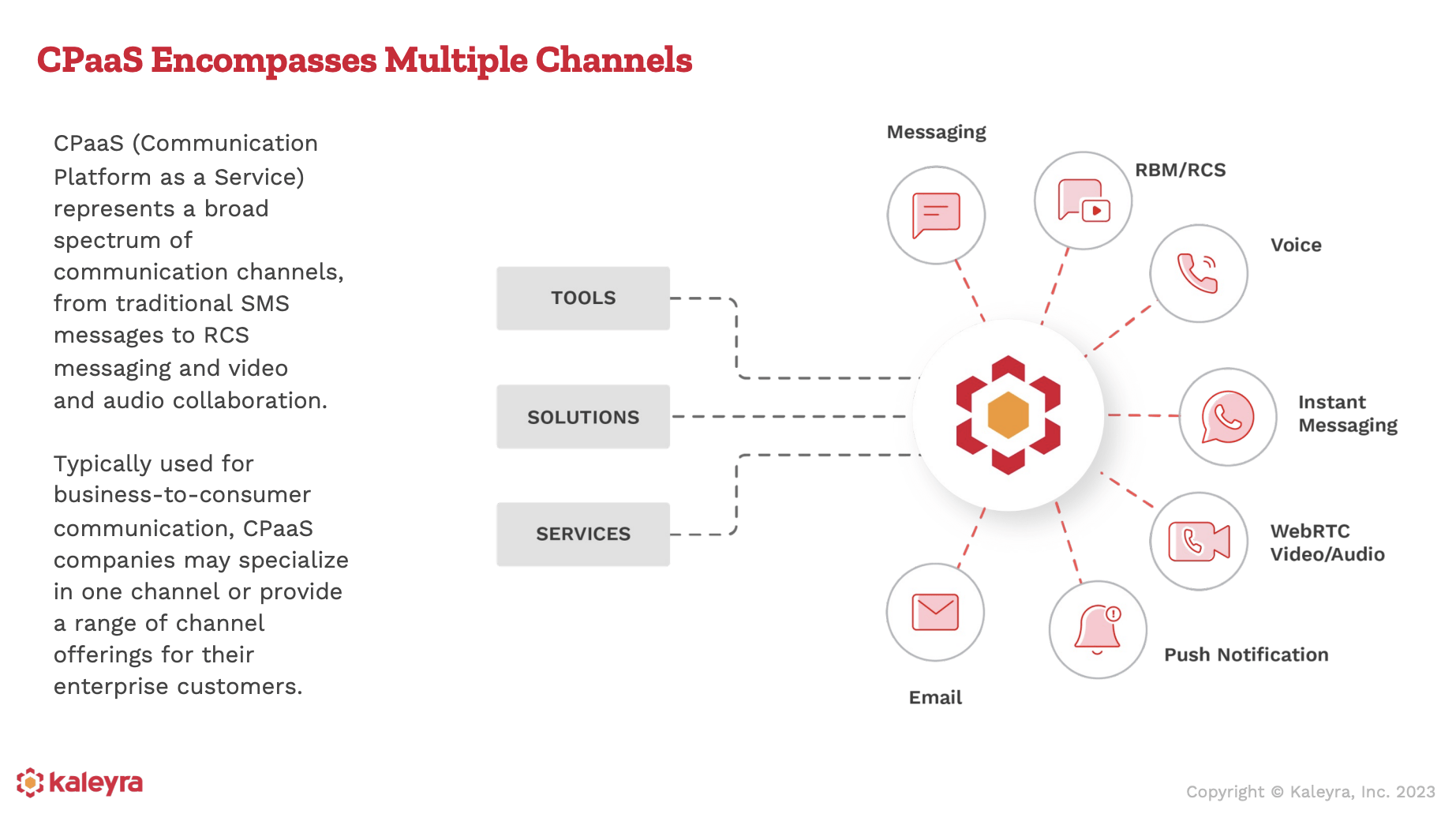

For those unfamiliar with the company, Kaleyra is an Italy-based CPaaS company that provides integrated omnichannel communication services for businesses. It allows companies to communicate and engage with customers through different channels such as video, messaging, RCS, programmable voice services, virtual numbers, push notifications, etc. The company has a strong presence in Europe, India, and Brazil and mainly focuses on the banking, travel, retail, and e-commerce industry. It currently serves customers like Visa ( V ), Mastercard ( MA ), Uber ( UBER ), Flipkart, and more.

Early last year, Kaleyra acquired mGage , an enterprise messaging provider, and Bandyer , a cloud-based audio/video communications service provider. These two acquisitions significantly improved the company's scale and product capabilities. The CPaaS industry is also growing rapidly. According to Markets and Markets , its TAM (total addressable market) is forecasted to grow from $12.5 billion in 2022 to $45.3 billion in 2027, representing a strong CAGR (compounded annual growth rate) of 29.4%. The growth is largely driven by digital transformation as more companies are leveraging digital channels to interact with their users and audiences. This should provide a strong tailwind for the company in the long run.

{kind=link}

Financials and Valuation

Kaleyra reported its fourth-quarter earnings earlier this week and the results continue to deteriorate as macro impact hits.

Revenue growth slowed and profitability contracted. The company reported revenue of $93.7 million, up 4.1% YoY (year over year) from $90 million. On a constant currency basis, growth was 8.6%. Dollar-based net expansion rate for the quarter was 98.1%. The figure was much higher for its top 30 customers at 139% with zero churns. The drop in customer spending is expected as Kaleyra's products are billed based on usage, therefore it is much more responsive to the slowdown in the economy.

Gross profit was down 19.4% from 21.1 million to $17.0 million, due to increasing onboarding costs and a higher revenue mix from low-margin segments. This also resulted in the gross profit margin dropping from 23.5% to 18.2%. Net loss was $(57.8) million or $1.28 per share compared to $(7.3) million, or $0.17 per share. The decline was largely cost by an impairment loss on intangible assets of $49.4 million. This also weighed on the adjusted EBITDA which decreased from $9.6 million to $2.5 million, representing an adjusted EBITDA margin of 2.6%.

The company ended the quarter with $78.1 million in cash and $221 million in debt, which was incurred from its acquisition of mGage and Bandyer. $190 million are long-term debts therefore they are in no rush to pay it back. While the company did not give out explicit guidance for FY23, the management team mentioned that they are expecting adjusted EBITDA growth to be over 20% and also increase its operating cash flow.

After the massive drop, Kaleyra is now trading at an fwd EV/EBITDA ratio of 8.8x (I am using the EV/EBITDA ratio as it takes the company's debt into account), which is pretty low for a company with a large addressable market. From the chart below, you can see that its valuation is significantly lower than other CPaaS companies such as Twilio ( TWLO ), Bandwidth ( BAND ), and 8x8 ( EGHT ). The average EV/EBITDA ratio of the three companies is 19.7x, which represents a 124% premium compared to Kaleyra. The company expects adjusted EBITDA growth for FY23 to be over 20%and if it can achieve it, there should be meaningful potential upsides as multiples get re-rated.

Investors Takeaway

Kaleyra has sold off significantly but I do not think now is the time to catch the falling knife. I believe the company's fundamental is still fine but execution and the macro environment is creating many uncertainties.

The CPaaS industry continues to grow rapidly as digital transformation accelerates, which should provide solid tailwinds for the company in the long run. However, due to the economy weakening and its usage-based model, the company is showing a substantial deceleration in growth.

While the management team expects adjusted EBITDA to grow in the coming year, their execution has not been great in the past year and I'm taking their words with a grain of salt. The economy is also still very volatile and it is likely we will see a recession in the second half of the year.

The current valuation is no doubt attractive but it also incurs a bunch of risks. I believe the upside potential lies in whether the management can deliver what it said, and whether the macro environment will continue to deteriorate. I would like to see some re-acceleration in growth before adding or buying, therefore I rate the company as a hold

For further details see:

Kaleyra: More Clarity Needed (Rating Downgrade)