ATXS - KalVista Pharmaceuticals: The Share Price Rally Requires An Adjustment Of My Investment Thesis

Summary

- KalVista intends to provide best-in-class therapies, both for acute on-demand and prophylaxis treatment, to fundamentally change the way HAE is treated.

- The backbone of the company is Sebetralstat, which is currently being investigated in a phase 3 trial for the on-demand treatment of HAE attacks - a potentially billion-dollar market opportunity.

- Enrollment is going well and KalVista confirms topline data in the second half of 2023.

- The market for on-demand treatment of HAE is generally underrated by investors, which is also reflected in KalVista's poor valuation.

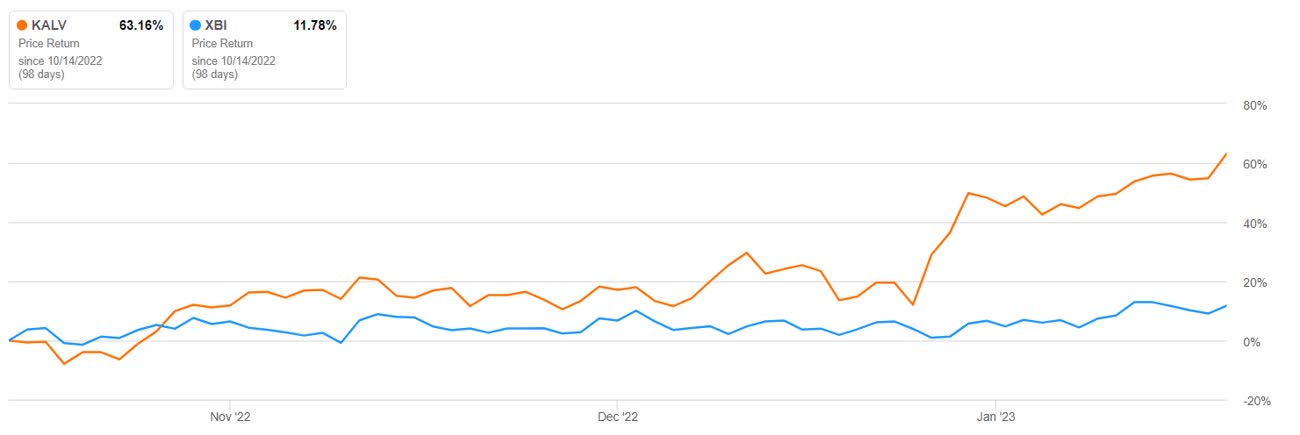

The biotech sector is off to a promising start, and after a challenging 2022, the outlook for 2023 seems promising. KalVista was also fortunate to benefit from this development and has outperformed the market extraordinarily in recent weeks. Since my first article on KalVista in October, in which I addressed the sell-off prices and the negative value of the pipeline, the share price has recovered and risen by almost 60%.

Kalvista's outperformace since my last article (Source: SeekingAlpha)

{kind=link}

However, the strong performance of KalVista has an impact on my investment thesis. The root of my initial investment thesis was the massive undervaluation of KalVista, which was reflected in the peer comparison as well as in the negative pipeline value. Due to the strong price increase, KalVista's pipeline has a positive value and the question arises whether the price increase is justified and what value is attributable to the pipeline. In this article, I would like to address these questions and update my investment thesis. With this in mind, I would like to highlight recent developments and assess the market potential of Sebetralstat from an economic point of view.

Business of KalVista Pharmaceuticals

Logo of KalVista (Source: Company Homepage)

{kind=link}

KalVista ( KALV ) is a clinical-stage pharmaceutical company developing oral therapies to create the next generation of hereditary angioedema ((HAE)) therapeutics. KalVista intends to provide best-in-class therapies, both for acute on-demand and prophylaxis treatment, to fundamentally change the way HAE is treated.

The backbone of the company is Sebetralstat, which is currently being investigated in a phase 3 trial for the on-demand treatment of HAE. KalVista confirms the publication of topline results in the second half of 2023 as enrollment is going very well. Based on positive study results, KalVista plans to submit a NDA in the first half of 2024 and is committed to develop internal sales and marketing capabilities. In addition to Sebetralstat, KalVista is developing an oral Factor XIIa inhibitor for the prophylactic treatment of HAE. KalVista plans to take the compound into a phase 1 trial in humans in 2023. The mechanism of action in HAE was recently validated in a phase 3 study by CSL Behring .

HAE is a rare and potentially life-threatening genetic disease characterised by recurrent, severe and unpredictable swelling in different parts of the body. It occurs in 1 in 10,000 to 1 in 50,000 people, and the first symptoms usually appear by the age of 12. Both the frequency and severity of HAE attacks are highly variable and unpredictable and are not correlated. The attacks can lead to hospitalization and, although rare, airway swellings can lead to death.

Despite having multiple therapies approved, there is a high unmet medical need to improve quality of life and ease of disease control. The standard of care has evolved to both on-demand and prophylactic therapies for HAE. With the exception of ORLADEYO , approved for prophylaxis, all therapies currently on the market are administered by injection. For patients, injections can be challenging despite their effectiveness, as they are painful, time-consuming to administer and difficult to store. For an overview of KalVista's potential to change the treatment paradigm for HAE from a clinical perspective, I would like to refer to my first article .

Corporate Developments and Financials

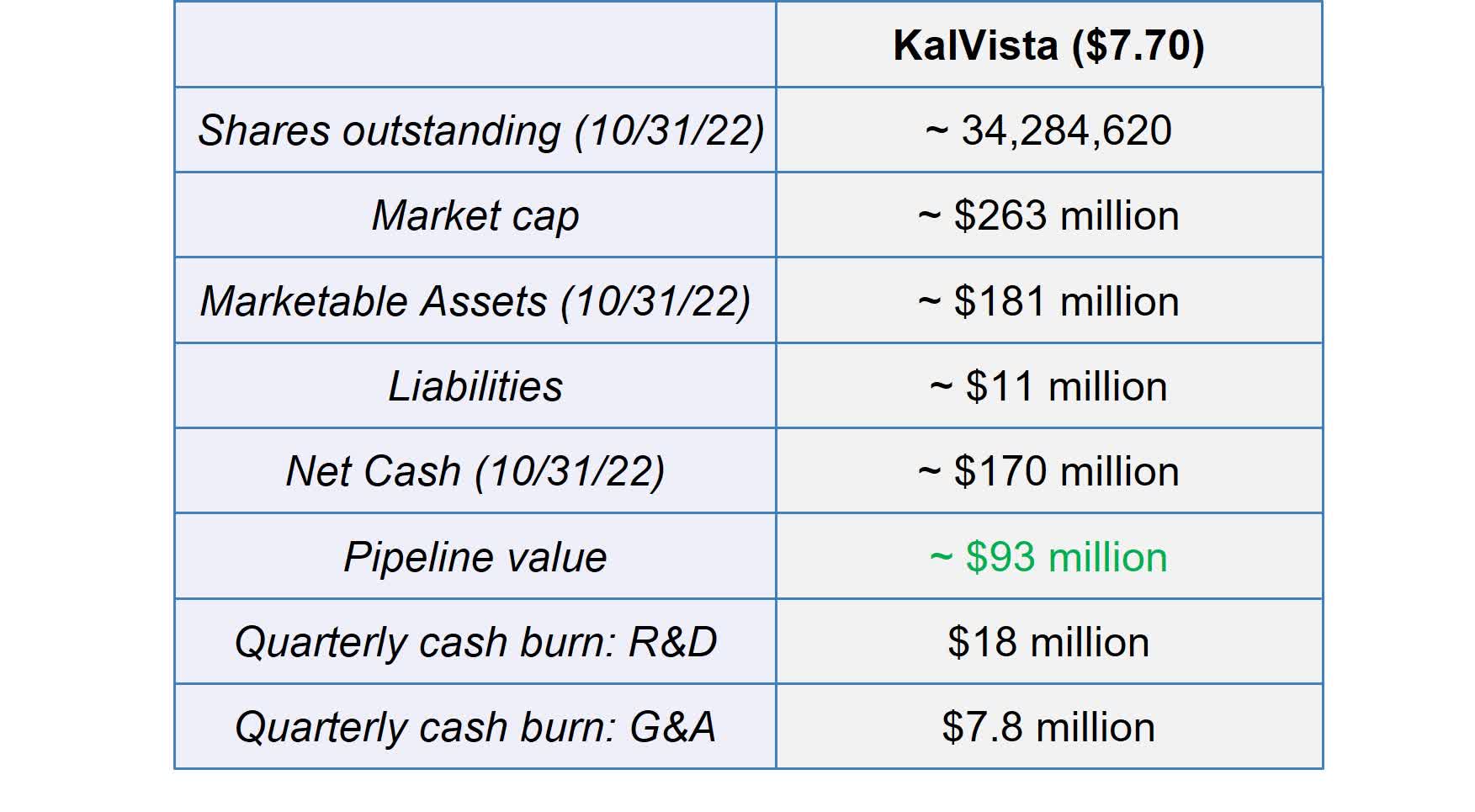

In particular, in the case of biotechnology companies, the financial position is one of the most important fundamental factors. Here KalVista was able to strengthen its financial position earlier than expected. In my opinion, KalVista has given the large institutional investors involved in the last capital increase the opportunity to lower their average price. Although KalVista was able to raise a total of $58 million at a price of $6 , effectively extending its cash runway to 2025 , I expect another financing transaction after the publication of the topline data or FDA approval.

The existing financial strength will not be sufficient to support the sales and marketing activities that will probably start in the second half of 2024. However, KalVista has mentioned the possibility of providing more complex financing structures as a late-stage company . In addition to raising equity, KalVista could enter into international collaborations, debt structures and royalty agreements to provide funding for the start of sales activities.

KalVista's market capitalization at current levels is about $250 million, and their pipeline is valued at about $80 million after deducting available capital. I expect research and development costs to continue to decline in the coming quarters.

KalVista is fully funded beyond major milestones (Source: Author's Chart)

{kind=link}

In addition to strengthening its financial position, KalVista has already started to conduct life-cycle studies to enhance the label of Sebetralstat. For example, KalVista announced positive clinical results for an orally disintegrating tablet (ODT) formulation of Sebetralstat. This dosage form could benefit paediatric patients and patients with difficulties swallowing.

The trial results for KVD824 are still blinded and KalVista will do further analyses. However, it is not yet clear whether the study results will be published.

Commercial Opportunity for Sebetralstat

In my first article, I provided an overview of the currently approved therapies for HAE and highlighted the potential of Sebetralstat to change the treatment paradigm for this disease. For this reason, I would like to go into more detail about the commercial potential and the differentiation from competition. In line with market trends, I believe the market opportunities for on-demand and prophylactic therapies should be assessed separately.

Market opportunities for on-demand therapies

Many investors and big pharma believe the future of HAE treatments lies in the preventive treatment of attacks and are therefore focusing on the development of prophylactic therapies. One indication for this is the declining revenue in the on-demand market in the last 3 years. However, examining the sales volume is not sufficient here. Looking at the quantity of prescriptions, for example, there is no visible trend in recent years; instead, the quantity of prescriptions has remained stable. The declining sales volume can be explained by the fact that Firazyr is no longer patent-protected and can be sold generically at one-third of the branded price since 2019. Moreover, quantity of prescriptions for prophylactic therapies shows that only few patients are willing to switch from on-demand therapies as there is no significant growth.

Currently, on-demand therapy costs around $11,000 per dose on the branded side, while generics are gaining market shares at around $3,500 per dose. Given the superior clinical profile addressing the high unmet medical need, KalVista expects the price of Sebetralstat to be equal to or higher than the price of current branded therapeutics . This assumption has also been confirmed in discussions with payers.

Since the majority of patients are willing to switch to oral drugs, the initial market success is primarily dependent on the availability. Again, the payers have already indicated that they will not put any more roadblocks in front of Sebetralstat . On the one hand, the payers recognise the advantages. For example, patients not only benefit from the more convenient form of administration, but also gain in quality of life. With Sebetralstat, they no longer have to choose between efficacy and simplicity of administration, nor do they have to suffer unnecessarily because they want to avoid the injections. On the other hand, on-demand therapy is cost effective, as the annual therapy cost for preventive treatment of HAE exceeds half a million dollars.

The biggest opportunity, which is currently completely ignored by the market, is the potential to move patients away from prophylaxis and towards on-demand treatment. Even though prophylactic treatment of HAE reduces the frequency of attacks, breakthroughs attacks can still occur. For this reason, these patients should also carry on-demand therapies as a backup.

Prophylaxis can be terrific for many patients but it does not completely prevent breakthrough attacks for most patients, so there is certainly a meaningful opportunity to address that market.

- Source: Andy Crockett , CEO of KalVista

Another advantage in the on-demand market is the competitive situation. In case of approval, Sebetralstat can already strongly differentiate itself from the competition due to the oral form of administration. Currently, there is only one other oral drug in clinical development for the on-demand treatment of HAE: PHVS416 from Pharvaris ( PHVS ). Although Pharvaris was able to present positive phase 2 study results , the situation in the US is difficult. They first need to conduct a 26-week rodent toxicology study to address clinical concerns before the FDA lifts their (partial) clinical hold. KalVista expects to enter the market first with Sebetralstat and to achieve a dominant position in the market by the time PHVS416 is potentially approved.

In summary, Sebetralstat offers real market potential and both the value and the number of patients is certainly underappreciated. With the potential to change the treatment paradigm and prevent attacks as soon as they occur, rather than limiting the severity and symptoms of attacks, Sebetralstat also has the potential to change the entire on-demand market. Sebetralstat definitely has the potential to reach blockbuster status, after all, the total HAE market is estimated to exceed $4 billion by 2026 .

Market opportunities for prophylactic therapies

Since KalVista is also developing a Factor XIIa inhibitor for prophylactic treatment of HAE, I would also like to briefly discuss the market opportunity for prophylactic treatment. Clearly, this is the focus of big pharma and investors. While on-demand drugs treat the symptoms, i.e. the attacks, patients have an even greater benefit if attacks can be prevented in the first place. Furthermore, prophylactic treatments can cannibalise on-demand therapies.

The mechanism of action of factor XII inhibitors in HAE was recently validated by CSL Behring in a phase 3 study . KalVista plans to advance a potent selective orally available factor XII inhibitor into a phase 1 trial in humans in 2023. However, it is still a long way to approval and the market is very competitive. However, investors are willing to invest a lot of money in early stage compounds. Astria Therapeutics ( ATXS ), for example, raised a further $115 million in cash following positive phase 1 results and currently has a market capitalisation of over $400 million. Other competitors include CSL Behring, who will file a NDA in the coming weeks, Ionis Pharmaceuticals ( IONS ), who expect full patient enrollment in their Phase 3 trial in 2023, Pharvaris as well as Attune Pharmaceuticals, who also recently published positive Phase 1 trial results. Intellia Therapeutics ( NTLA ) also plans to initiate a phase 2 trial in 2023, using a single dose to prevent future attacks. In my opinion, the efficiency and safety profile of these compounds will be key in determining how the HAE market will be divided in the future.

Summary

In my opinion, the positive momentum should continue in the coming months. While shareholders can already look back on significant and easy gains since my last article, I believe that there is more upside potential. The current valuation does not yet reflect the full potential of Sebetralstat. I expect even higher prices by the time of the topline publication in the second half of 2023 and expect Sebetralstat to be valued at around 200 million, which corresponds to prices of around $10.

The risk profile of the share remains unaffected, for more information see my last article .

I personally see great potential in Sebetralstat. A novel and the only oral drug in a multi-billion market with a high unmet medical need that is superior to the competition. For this reason, I will use lower prices to buy more shares. However, since the publication of study results is always a binary event, I will also reduce the risk well in advance.

For further details see:

KalVista Pharmaceuticals: The Share Price Rally Requires An Adjustment Of My Investment Thesis