KALV - KalVista's Sebetralstat: A Pill Worth Swallowing In HAE

2023-10-01 00:05:36 ET

Summary

- KalVista Pharmaceuticals is positioned to disrupt the HAE treatment landscape with its oral therapy, sebetralstat, offering rapid symptom relief and improved patient adherence.

- Financially, KalVista has a cash runway of about 14 months, but rising G&A costs raise concerns about capital efficiency.

- Given the statistically significant Phase 2 results, I speculate that the Phase 3 data, expected in Q4 2023, will likely be positive.

- I recommend a speculative "Buy," based on sebetralstat's efficacy, market-disruptive potential, and KalVista's solid financial footing.

At a Glance

KalVista Pharmaceuticals' ( KALV ) sebetralstat has notable upside potential given the unmet need for oral therapies in hereditary angioedema [HAE] treatment. The drug's strong Phase 2 data indicates a robust efficacy profile, making it a prime candidate for future adoption and market share acquisition. Financially, KalVista has a cash runway sufficient for near-term operations, although increased G&A expenses need to be rationalized, especially ahead of the pivotal Phase 3 readouts. Elevated short interest, although a risk factor, could result in a price surge should the Phase 3 trials yield positive results. From a clinical efficacy and capital allocation standpoint, the firm appears well-poised for medium to long-term growth, justifying a speculative "Buy" rating. However, investors should closely monitor Phase 3 data and potential financing activities as they would substantively influence the stock's risk-return profile.

Earnings Report

To begin my analysis, looking at KalVista Pharmaceuticals' most recent earnings report for the quarter ended July 31, 2023, we observe an increase in both Research and Development (R&D) and General and Administrative (G&A) expenses, to $19.3M and $9.8M respectively, compared to $18.2M and $8.1M in the same quarter last year. Operating loss widened to $29.1M from $26.3M YoY. Notably, there was a marginal boost in interest income to $0.9M and an improvement in foreign currency gains to $0.5M. Share dilution is evident, with the weighted average common shares outstanding increasing from 24.6M to 34.4M.

Financial Health & Liquidity

Turning to KalVista Pharmaceuticals' balance sheet , as of July 31, 2023, the company had cash and cash equivalents of $49.4M and marketable securities valued at $73.8M, summing up to $123.2M in highly liquid assets. The net cash used in operating activities over the last quarter was $26.7M, equating to an approximate monthly burn rate of $8.9M. Given these values, the company has an estimated cash runway of approximately 13.9 months based on the monthly cash burn rate. It's crucial to note that these values and estimates are based on past data and may not accurately reflect future performance.

In terms of liquidity, KalVista appears to be in a relatively comfortable position with minimal current liabilities totaling $14.1M, which are well covered by its current assets. There's no mention of outstanding debt in the balance sheet, suggesting that the company does not bear the financial constraints and risks associated with borrowing. Based on the available data, it appears KalVista would be well-positioned to secure additional financing if needed, given its robust cash position and absence of debt, which make the company a less risky prospect for investors or creditors. These are my personal observations, and other analysts might interpret the data differently.

Capital, Growth, Momentum, & Ownership

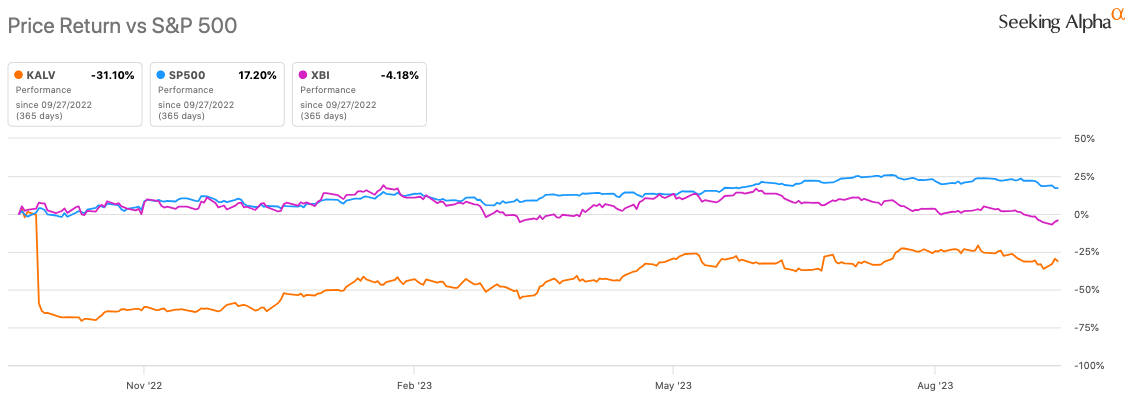

According to Seeking Alpha data, KalVista's capital structure benefits from adequate liquidity with high cash reserves and no significant debt, reducing its financial risk despite a relatively moderate market cap of $339.22M. Its Phase 3 asset sebetralstat aligns with promising growth prospects; analysts project a revenue surge from $3.57M in 2024 to $119.67M in 2026, a signal of market confidence in its disruptive potential. Stock momentum appears mixed; KalVista outperformed SPY in the 3M, 6M, and 9M timeframes but lagged on a 1Y basis (-31.10% vs +17.17%).

{kind=link}

Ownership is diversified but leans toward institutional (58.46%) and PE/VC firms (27.14%), offering stability yet indicating expectations of strategic exits. Insider trading activity shows recent sells without subsequent buys, necessitating cautious interpretation. High short interest at 20.53% implies market skepticism, although the 19.18 days to cover could exaggerate price upswings upon positive catalysts.

Sebetralstat: A Swell Solution for HAE

In the HAE treatment landscape, where prophylactic and on-demand therapies largely rely on injectable solutions, sebetralstat's Phase 2 efficacy offers a compelling alternative. The primary endpoint—time to use of rescue treatment within 12 hours—was achieved with significant statistical rigor. A mere 15.1% of patients on sebetralstat required rescue treatments, compared to 30.2% in the placebo group (p=0.001). This is noteworthy given that rapid symptom relief is of paramount importance in HAE, a condition punctuated by painful and potentially life-threatening swelling episodes.

The primary endpoint's significance is twofold in this context. Firstly, it highlights the drug's rapid action in mitigating acute episodes, a critical factor for patients who often struggle with the speed of symptom progression. Secondly, it demonstrates the drug's potential to reduce dependency on rescue medications, which often come with their own set of challenges, including pain and inconvenience of administration.

Moreover, sebetralstat aims to differentiate itself by its oral administration, a feature that alone could significantly improve patients' quality of life. The existing market leaders like Takhzyro and Firazyr are injectables. This makes them less patient-friendly, as injections can be painful, cumbersome to administer, and may require healthcare professional intervention. Oral therapy would not only simplify administration but also promote better adherence, which is always a concern in chronic conditions requiring consistent prophylactic care.

The Phase 3 KONFIDENT trial , launched in 2022, is set to further scrutinize these promising features. The trial is expansive, covering around 84 patients across 60 global sites and utilizing a double-blind, placebo-controlled, event-driven crossover design. It will assess varying doses of sebetralstat to better understand its efficacy profile. Crucially, its primary endpoint remains focused on the time to symptom relief, a measure assessed by the PGI-C scale, reinforcing the drug's potential advantages in rapid symptom control without the need for injections.

Per the company, anticipated data in Q4 2023 could pave the way for a New Drug Application (NDA) by H1 2024, potentially heralding a new era in HAE treatment that marries efficacy with convenience.

My Analysis & Recommendation

In conclusion, KalVista Pharmaceuticals stands at a pivotal inflection point. The company’s lead asset, sebetralstat, has the potential to significantly disrupt the HAE market by offering an oral therapy option that can effectively replace or reduce the need for injectable rescue medications. This is not merely a quality-of-life improvement; it could transform the very economics of treatment adherence in chronic conditions like HAE. Given the statistically significant Phase 2 results, I speculate that the Phase 3 data, expected in Q4 2023, will likely tilt toward positive efficacy.

From a financial standpoint, KalVista has an adequate runway for the next 13.9 months. Their absence of debt is a positive indicator, though the increased G&A expenses raise questions about management’s capital efficiency. Elevated short interest is a risk factor, but it could also act as a slingshot for share prices if Phase 3 data serves as a strong catalyst. Furthermore, the diversified but institutionally weighted ownership structure suggests a low probability of capricious price movements and implies a longer-term horizon for ROI, possibly aligned with strategic exits.

Investors should keep a close eye on upcoming readouts from the KONFIDENT trial, monitor any updates regarding the company's cash burn rate, and look out for additional equity financing as a sign of institutional confidence. A strategic partnership could also be a significant upside catalyst. These are not mere operational milestones; they will serve as essential validation points for sebetralstat's commercial viability and market positioning.

My investment recommendation here is a speculative "Buy." The rationale rests on sebetralstat’s strong efficacy profile, its potential market-disruptive convenience, and the company's sound financial footing. Should sebetralstat secure FDA approval, it stands to command a sizable share of a market that is not just ready but eager for innovation. This makes KalVista a compelling, though speculative, long-term bet for investors willing to shoulder the inherent biotech risks in search of substantive returns.

Risks to Thesis

While my thesis leans towards a "Buy" recommendation for KalVista, there are several underexplored risks. First, the drug landscape for HAE is competitive; even if sebetralstat gets FDA approval, market adoption is not guaranteed. Failure to differentiate meaningfully from injectables could hinder uptake. Second, the increased G&A expenses with a widening operating loss raise concerns about management's efficiency, particularly as the pivotal Phase 3 data is imminent. Third, the high short interest suggests a bearish sentiment that shouldn't be ignored. Additionally, while ownership is mostly institutional, the recent insider selling is cautionary. Lastly, the company's cash runway of 13.9 months implies it may require financing soon, which could result in further share dilution.

For further details see:

KalVista's Sebetralstat: A Pill Worth Swallowing In HAE