ACVA - KAR Auction Services: Worth Getting Revved Up Over

Summary

- KAR Auction Services has undergone a lot of changes lately, the largest being a sizable assets divestiture.

- The company is now de-risked and looks attractive in most respects, particularly from a debt perspective.

- Add on top of this the fact that shares look cheap, and it's definitely worth serious consideration.

Buying into a company that is undergoing significant changes can always be rather risky. When changes are taking place, it creates uncertainty about what the future holds. Add on top of this the fact that the economy is in a questionable state right now and the fact that said state could impact any one business rather materially, and I understand the trepidation some investors might have when it comes to picking up stock in a firm such as KAR Auction Services ( KAR ). Historically speaking, this enterprise has done pretty well for itself from a revenue and cash flow perspective. Up until recently, the company did have quite a bit of debt. But thanks to a major asset sale, the company has now become significantly de-risked compared to what it once was. In addition to this the fact that shares are now trading at an attractive level, both on an absolute basis and relative to some similar firms, and I would make the case that it provides investors with a solid 'buy' opportunity at this moment.

Going once, going twice… gone

According to the management team at KAR Auction Services, the firm has historically operated as a leading provider of used vehicle auctions and related vehicle remarketing services throughout North America and Europe. Using its own technology, the company has created an efficient marketplace centered around auction services for sellers of used vehicles, largely through its digital marketplaces that are supported by more than 70 vehicle logistics center locations It has across North America. During its 2021 fiscal year, the company facilitated the sale of roughly 2.6 million used vehicles, collecting fees from both vehicle buyers and sellers in the process. In addition to facilitating the transactions, the company also provides other services like transportation, reconditioning, inspection, titling, and other related activities all centered around vehicle sales.

Up until recently, the company was quite a bit larger than it is as of this writing. This is because, in February of 2022, management announced that it was selling its ADESA US physical auction business to Carvana (CVNA) in a deal valued at $2.2 billion. That sale consisted of all auction sales, operations, and staff at the 56 ADESA US vehicle logistics centers the company had, plus the exclusive use of the ADESA.com marketplace throughout the country. Although the company said that it would likely lose around $100 million worth of EBITDA on an annual basis, using data from the 2022 fiscal year, it also mentioned that there were many benefits to the sale. For instance, the company said that it would reduce its headcount by roughly 50% and use the capital to nearly eliminate the debt on its books.

Following the completion of this deal, the company still had many of its other ADESA operations. This includes operations in Canada, Mexico, and throughout parts of Europe. About 15% to the company's revenue in all came from Canada during its 2021 fiscal year. And total foreign revenue amounted to 26.8% of sales. In addition to that, it also had other distinct business activities that it engaged in. The greatest example of this can be seen by looking at AFC. This particular unit, which made up 13% of the company's revenue in 2021, operates as a provider of floor plan financing to independent used vehicle dealers.

Management's plan to completely reinvent the company has so far paid off. As of the end of its latest quarter, the company had debt of $951.6 million and cash and cash equivalents of $832.5 million. Subsequent to the end of the quarter, the company did initiate a tender offer to buy back up to $600 million of its 5.125% senior notes that are supposed to come due in 2025. That tender offer was oversubscribed, allowing the company to buy back the amount they were interested in buying in exchange for a premium of just $4.5 million. Based on my estimates, the company should now have net debt of $123.6 million, with gross debt totaling around $356.1 million.

{kind=link}

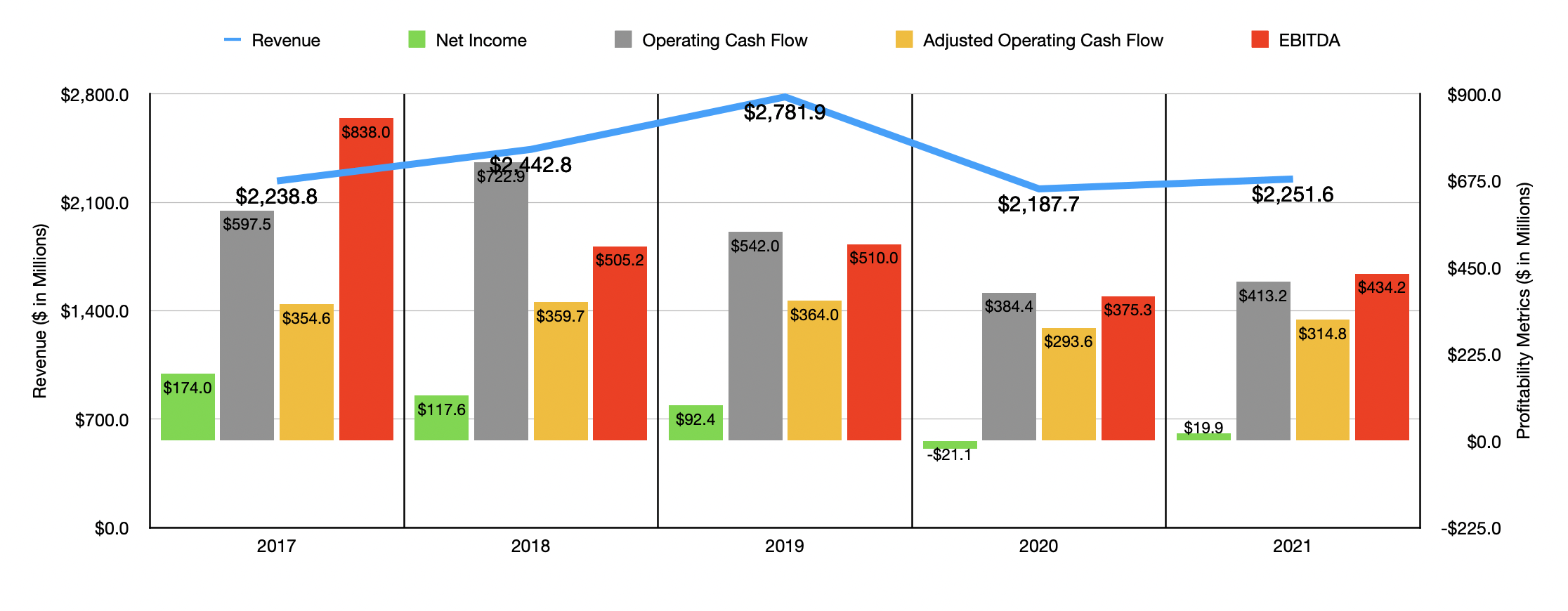

When I perform an analysis of any company, I always like to look at its historical performance. After all, this helps to paint the picture of how high quality the company is. Though it is also true that this significant change in the company's financial condition makes its past less relevant than it otherwise would be. Even so, in the chart above, you can see the five-year financial performance for the enterprise through the 2021 fiscal year. As you can see, revenue rose year after year up until the pandemic. After the pandemic, sales continued to climb once again. The company's bottom line results actually were worsening from an earnings perspective in the four years ending in 2020, only to see a slight recovery in 2021. But if you look at cash flow, you can see that the company was quite healthy. Adjusted operating cash flow (which ignores changes in working capital), for instance, rose from $354.6 million in 2017 to $364 million in 2019. In 2020, it dipped to $293.6 million before popping up to $314.8 million in 2021. And although the 2017 fiscal year was different, you can see a similar trajectory when it comes to EBITDA.

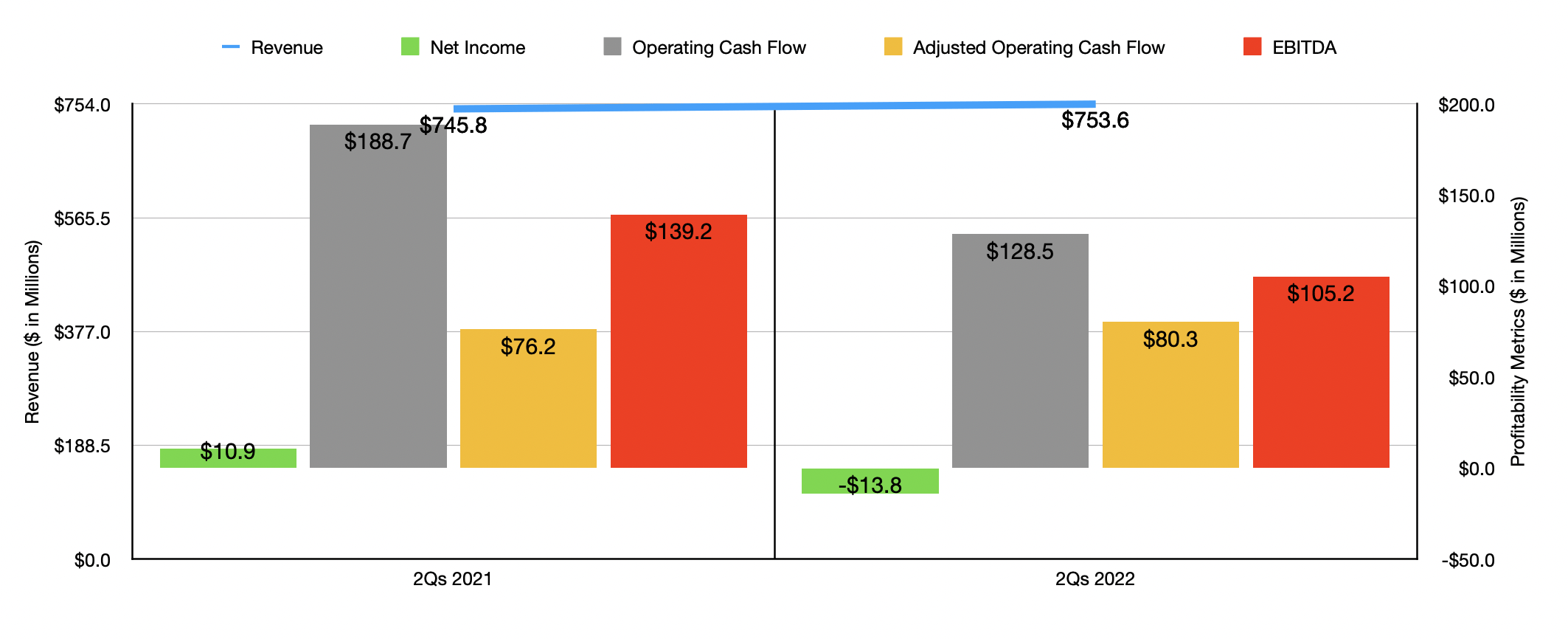

What's more important than how the company fared back then was how the company is performing today. In its most recent financial results , management made sure to classify the assets that it was selling as discontinued. Ignoring these then, you can see that the company generated sales in the first half of the 2022 fiscal year of $753.6 million. That's slightly above the $745.8 million the firm generated the same time one year earlier. Interestingly, the company's revenue actually declined in most categories. Auction fees, for instance, dropped from $208.8 million in the first half of 2021 to $200.6 million the same time this year. Service revenue declined from $287.3 million to $284.8 million, while purchased vehicle sales revenue dropped from $115.3 million to $92.1 million. Management classifies these particular activities its falling under its Marketplace. Collectively, the decline in sales amounted to 6%, largely as a result of a decrease in the number of vehicles sold, but partially offset by a rise in average revenue per vehicle sold. This came even as the company benefited to the tune of $34.6 million from acquisition-related activities.

{kind=link}

The total increase in sales, then, came from finance revenue rising from $134.4 million to $176.1 million. Management attributed this 31% increase to a 23% rise in revenue per loan transaction and a 6% increase in total loan transaction volume. The 23% rise in revenue per loan transaction, meanwhile, benefited from an increase in loan values and a rise in interest yields. On the bottom line, results have been somewhat mixed. Net income went from $10.9 million to negative $13.8 million. Operating cash flow dropped from $188.7 million to $128.5 million. But if we adjust for changes in working capital, it would have risen from $76.2 million to $80.3 million. Meanwhile, EBITDA for the company also declined, dropping from $139.2 million to $105.2 million.

When it comes to the 2022 fiscal year as a whole, management said that EBITDA, which excludes the EBITDA tied to its former ADESA operations, should be between $245 million and $265 million, with the actual results likely coming in near or at the low end of that range. No guidance was given when it came to other profitability metrics. But if we take the remaining debt on the company's books and strip out annual interest from that, combined with removing the $44.4 million in payments required for the company's preferred stock, we should get pro forma adjusted operating cash flow of $177.8 million.

{kind=link}

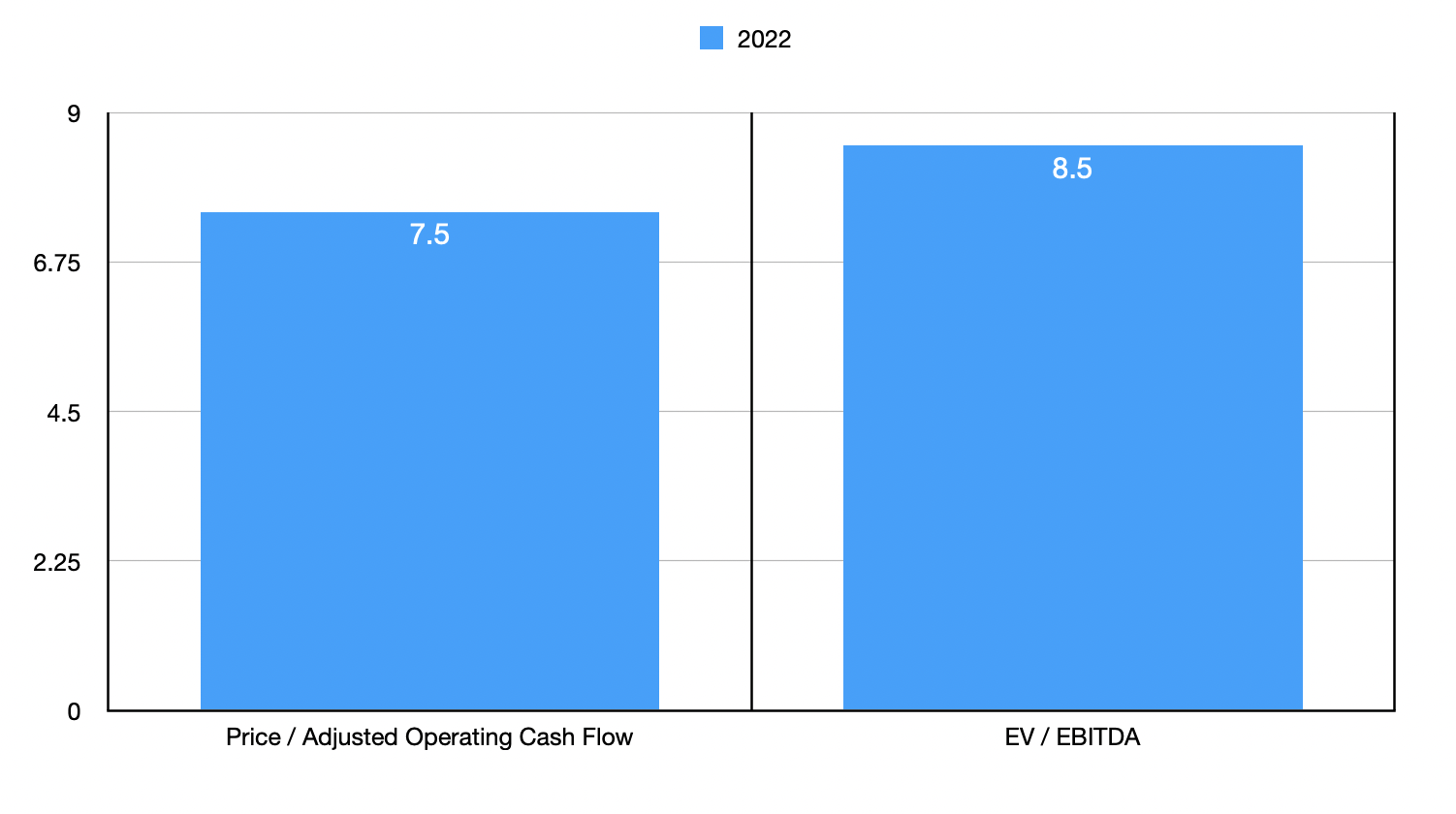

Based on these figures, the company is trading at a pro forma price to adjusted operating cash flow multiple of 7.5 and at a pro forma EV to EBITDA multiple of 8.5. As part of my analysis, I compared the company to three firms that I felt were similar in nature to it. On a price to operating cash flow basis, two of the three companies had positive results, with multiples of 22.9 and 126.2, respectively. And using the EV to EBITDA approach, the range for the two companies with positive results was between 11.9 and 16.4. In both cases, KAR Auction Services was the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| KAR Auction Services |

| 7.5 |

| 8.5 |

| ACV Auctions ( ACVA ) |

| 126.2 |

| N/A |

| Ritchie Bros. Auctioneers ( RBA ) |

| 22.9 |

| 16.4 |

| CarParts.com ( PRTS ) |

| N/A |

| 11.9 |

Takeaway

Based on all the data provided, KAR Auction Services strikes me as a very intriguing company that could very well generate attractive returns for investors moving forward. I would not be surprised to see financial performance worsen should the economy suffer materially from here on out. But with its debt significantly reduced and shares trading as cheap as they are, both on an absolute basis and relative to similar firms, I do believe that the long-term potential of the company warrants a 'buy' rating at this time.

For further details see:

KAR Auction Services: Worth Getting Revved Up Over