KRT - Karat Packaging: A Buy If The Growth Story Continues

2023-10-25 05:06:28 ET

Summary

- Karat Packaging has experienced significant organic revenue growth in the long term.

- The company has scaled its gross margin significantly in the first half of 2023, possibly causing revenue decreases that the company has currently faced.

- I believe the currently quite low valuation represents a good risk-to-reward for the stock.

Karat Packaging ( KRT ) produces food packaging among similar products. The company has had a good history of organic growth. On top, the company has scaled its gross margin significantly in the first half of 2023, growing the company’s bottom line despite currently decreasing revenues. Although the company’s future financials are quite tough to predict, I believe Karat’s current price represents a fairly good risk-to-reward ratio. At the moment, I see a buy-rating as constituted.

The Company & Stock

Karat manufactures disposable food and beverage products. The company’s offering includes products such as cups and lids for drinks, paper food buckets, take out bags, aluminium foil products, utensils, napkins, and gloves. The company offers products through four brands – Karat, Karat Earth, Tea Zone, and Total Clean. Karat’s partners include names such as 1883, Big Train, Caffe D’Vita, DaVinci, and Dole – most of Karat’s serviced brands are quite small in size.

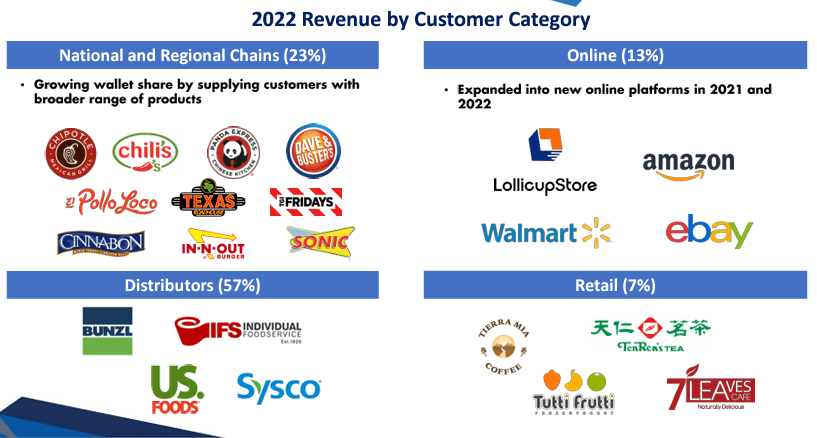

Further, the company’s customers can be divided into four main categories: National and Regional Chains, Online, Distributors, and Retail, of which the Distributors category is clearly largest with the majority of Karat’s revenues:

{kind=link}

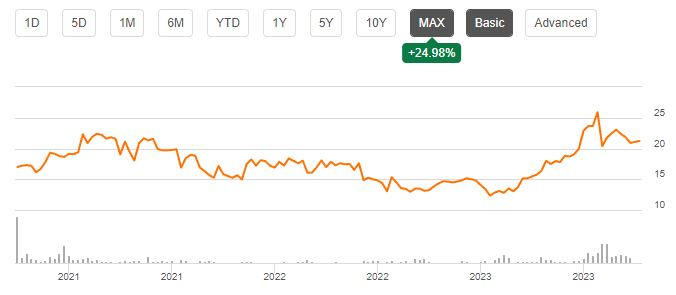

Since Karat’s IPO in April of 2021, the stock has appreciated by 25% as a result of a clear price rally in 2023. The stock price has seen a clear increase year-to-date in 2023 with an appreciation of around 66% as Karat’s bottom line has increased significantly.

{kind=link}

Financials

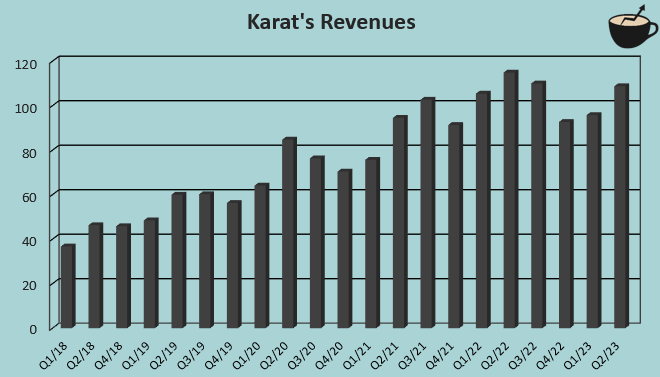

From 2017 to 2022, Karat has had a very good revenue performance. In the period, Karat’s compounded annual growth rate in revenues has been 24.8%. The clear trend in growth can also be seen on a somewhat turbulent, but mainly good quarterly level from 2018:

{kind=link}

I believe that the achieved growth could partly be due to the Covid pandemic from 2020 to 2022 – take out food with delivery services skyrocketed in demand in the period, raising the demand for single-use food and beverage packaging. Although take out with services such as DoorDash and Uber Eats have cemented their place in the culture, the growth could very well be lower than the company achieved during the pandemic. As a recent example, in the first half of 2023, Karat’s revenues decreased by -7.2%, contrary to the company’s historically significant growth.

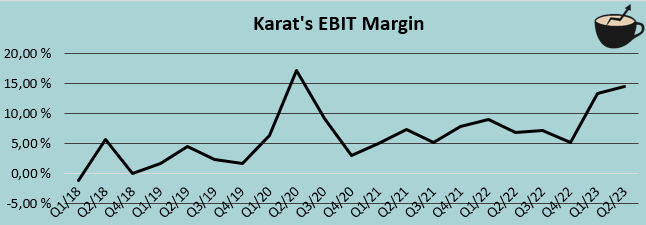

On a quarterly basis, Karat’s EBIT has had some turbulence. From Q1/2018 to Q2/2023, the company has achieved an average EBIT margin of 6.3%. As a result of stronger gross margins in 2023 so far, Karat’s first half of 2023 saw a significant increase in the company’s EBIT margin – in the first half of 2023, Karat’s gross margin grew by 8.1 percentage points year-over-year into a figure of 39.1%. I believe that the increased gross margin is in part due to increased pricing and some cost deflation. The improvement has had a significant impact on Karat’s EBIT margin, which is clearly higher than in the previous year even with revenue decreases in the period:

{kind=link}

The combination of decreasing revenues and an increasing gross margin seems to indicate that Karat has pushed a more aggressive pricing to the company’s products, deterring some of Karat’s customers from the company. An increased pricing could signify a lower level of growth in the medium- to long-term future and decreasing revenues in the short term; I believe that investors should be somewhat cautious in the coming quarters.

Valuation

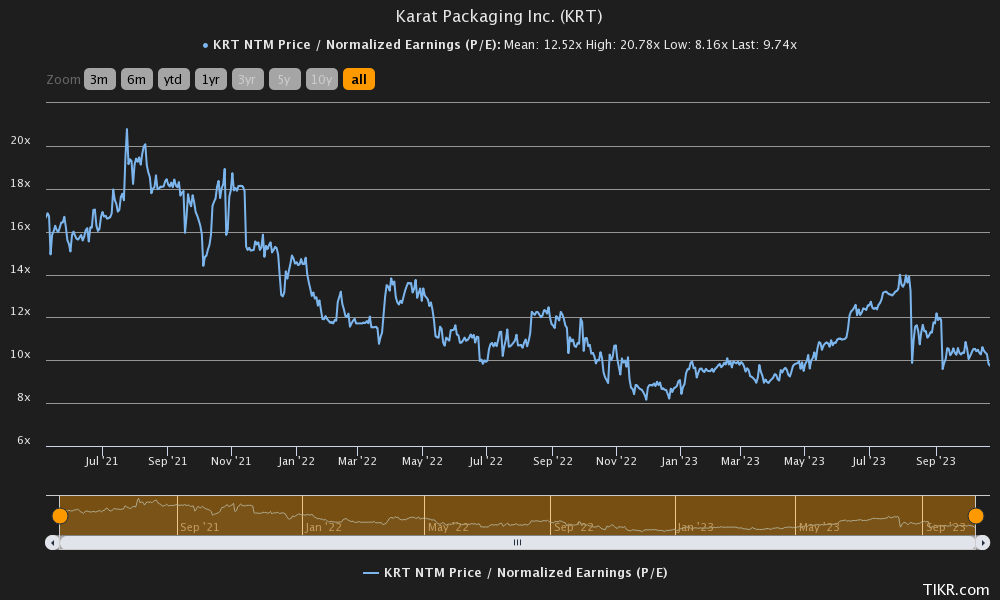

Considering Karat’s significant long-term growth, the stock seems to be priced quite cheaply at a forward P/E of 9.7, significantly below the company’s average of 12.5 since its IPO:

{kind=link}

The decreasing revenues in H1 of 2023 have probably scared investors about Karat’s future topline growth, lowering Karat’s accepted P/E significantly. I still believe that the current price represents a fairly good entry point, as my discounted cash flow model demonstrates.

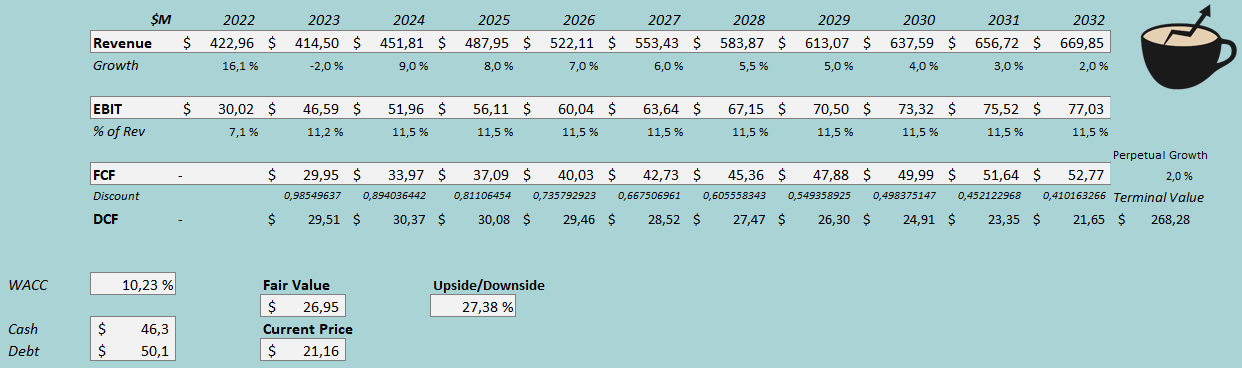

In the DCF model, I estimate Karat’s revenues to decrease by 2% in 2023 as a result of the higher pricing and softer demand. The estimate is also in line with Karat’s current guidance. After 2023, I estimate Karat to turn back into its growth trajectory, although with a significantly lower level than the achieved CAGR of 24.8% from 2017 to 2022 – for 2024, I estimate a growth of 9%. After the year, I estimate Karat’s growth to come down further in steps into an eventual perpetual growth rate of 2%. Altogether, the DCF model estimates have a revenue GAGR of 4.7% from 2022 to 2032.

I estimate Karat’s increased margin to be sustainable in the model. For 2023, I estimate an EBIT margin of 11.2%, clearly above the achieved 2022 level of 7.1%. Furthermore, I estimate Karat’s EBIT margin to scale very slightly in 2024 into a margin of 11.5% that stays stable into perpetuity. The achieved margin implies that Karat can keep up the currently good gross margin. The mentioned estimates along with a cost of capital of 10.23% craft the following DCF model with a fair value estimate of $26.95, around 27% above the stock price at the time of writing:

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Karat had $0.57 million in interest expenses in Q2. With the company’s current interest-bearing debt balance , Karat’s interest rate comes up to 4.55%. Karat uses debt quite moderately, and I estimate the leveraging to stay near the current figure with a long-term debt-to-equity ratio of 10%.

For the risk-free rate on the cost of equity side, I use the United States’ current 10-year bond yield of 4.87% . Professor Aswath Damodaran estimates the United States’ equity risk premium to be 5.91% in his latest estimates . Karat’s beta is estimated at a figure of 0.95 according to Yahoo Finance. Finally, I add a small liquidity premium of half a percent into the cost of equity, crafting the figure at 10.98% and the WACC at 10.23%.

Takeaway

Karat is at an intriguing point in time. The company has scaled its gross margin significantly, leading to an increased bottom line. At the same time, though, the company’s revenues have decreased after a possibly pandemic-boosted market and increased pricing. If Karat can turn back into a growing company even at half the pace of Karat’s history, the stock seems to be priced too low. At the moment, I believe the risk-to-reward is quite good as my DCF model estimates a fair amount of upside for the stock.

For further details see:

Karat Packaging: A Buy If The Growth Story Continues