KRT - Karat Packaging: More Karat Less Stick

2023-12-18 12:14:33 ET

Summary

- Karat Packaging offers industry-leading margins, solid growth opportunities and a bias towards returning value to shareholders via regular and special dividends.

- Management has held the reins for over 20 years developing a robust supplier network offering a range of eco-friendly, bespoke, and branded products for the single-use foodservice industry.

- Regulatory and secular tailwinds favor Karat into 2024 and beyond, and these are independent of an improving cost structure and low-hanging growth opportunities.

Editor's note: Seeking Alpha is proud to welcome Proinsias Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Karat Packaging ((KRT)) is a differentiated small-cap distributor and manufacturer that operates in a highly fragmented market providing eco-friendly products to a diversified customer base. Karat is favorably positioned to benefit from regulatory and secular tailwinds coupled with company-specific growth and margin improving opportunities we discuss below that the market has not fully appreciated. With a mid-single-digit dividend yield return our $27 price target implies a total return of over 20%.

More Karat, Less Stick

With 2023 moving deeper in the rearview mirror, attention is squarely on 2024 and initial guides. Manufacturers and distributors like industry leading Karat Packaging ( KRT ) are expected to draw their first line in the sand at their 4Q23 conference call. We suspect both internal and sell-side models have been sensitized for upside and downside scenarios. Sensitivities include but are not limited to deflation (inflation?) of labor and raw materials, ocean and trucking rates, port fluidity, and political uncertainty - and yes, the overall health of the consumer, an afterthought behind execution - the fan favorite execution toggle is an advanced Wall Street Prep add-in. The stated levers in a supplier model create for a challenging backdrop in a grind higher market, but in the face of an election year and consumer headwinds that Karat has yet to manage as a public company, we thought best to forecast what we hold true (empirically and anecdotally) while applying a high degree of prudence towards what we consider uncertain.

Regulatory and Secular Tailwinds: What We Hold True

State and city governing bodies have proposed and implemented legislature aimed at prohibiting the use of single-use plastic bags and select Food Contact Materials such as styrofoam (polystyrene) containers and plastic straws. These actions were taken by individual states and cities with no existing ban at the federal level. The bans enacted are intended to prevent additional plastic and styrofoam products clogging landfills given their inability to break down. Irrespective of the political echo chamber you call home, which is a harder box than any escape room experience to break, this change makes sense on both a societal and environmental level. However, the downstream impact to distributors, restaurants and stores who rely on existing suppliers for branded / unbranded products with bespoke finishes that infringe on this legislature are left in a precarious position - looking elsewhere - enter Karat.

Karat co-founders Alan Yu and Marvin Cheng showcased their commitment to environmental sustainability beginning in 2008 at the founding of Karat Earth, a plant-based line of compostable products that align with renewable and ethically sourced initiatives. Karat Earth products are certified compostable. Higher margin Eco-friendly products are a key pillar underpinning the margin story Karat has executed, with Management doubling down on the importance of this segment expecting Eco-friendly Net Sales as a % of total sales to edge closer to 35% up from 27% in 2022. Karat is a pioneer and leader in the supply of Eco-friendly disposable foodservice products, a testament to Management's sustainability commitment and ability to recognize where the market is moving before competitors. Net sales of Karat Earth products increased by 36% YoY in 2022 with over 400 SKUs offered. Looking at 2024 and beyond, the team is focused on expanding SKUs plus adding higher-end finishes and customization of products. While the regulatory tailwind is selectively regional for now, and no clear timeline for a national / federal ban , we do expect this to be a "when" not an "if" leaving Karat auspiciously positioned on the back of increasing government regulation irrespective of who's in office.

Legendary value investor and co-founder of Oaktree Capital Management Howard Marks speaks at length on the topic of Sea Change which is the fundamental shift or change in a market or industry. While the secular shift to at-home dining, pulled forward by the pandemic, is certainly not grounds for a sea change title, it is however a respectable tributary / medium-sized river change for a company so levered to consumer habits. From the perspective of Karat's services, there's a zero-sum game between at-home and on-premises dining, and from the numbers, it appears takeout is taking a bite out of brick and mortar - the U.S. Online Food Delivery Market is forecasted to grow to $96 billion in 2026 , up from $31 billion in 2019, the final full-year before the pandemic.

Karat('s) bread and butter is the sale and distribution of single-use disposable foodservice products to distributors, national + regional chains, retail establishments and online. One of the many upsides covering Karat today versus on the back of the IPO is the benefit of seeing how post-pandemic retail trends have panned out. Two polar schools of thought were circulating - on premises dining would never return to its former glory with consumers trading experience for the safety and comfort of their home opting for delivery apps. While the other dogma, perhaps more accurate (helped by consumers flush with cash), a mass exodus from stuffy apartments and homes back into social restaurant settings. While the impact of the pandemic has abated, albeit brief spikes in new variants, takeout dining, and the players within the space (i.e., Uber (UBER), DoorDash (DASH), both > +100% YTD) have shown they are here to stay. With this "medium-sized river" change keeping more restaurant patrons home versus pre-pandemic, establishments recognize the critical role quality packaging and take-out containers play. Karat stands to benefit from this shift with custom-branded and custom-designed products capable of fast turnaround times at competitive prices.

Growth Opportunities Underpinned by Industry-Leading Margins: Take With a Grain of Salt

The single-use disposable foodservice products industry is extremely competitive and highly fragmented. Karat, with just a $440M market cap, has room to run. The global market for foodservice disposables is estimated to reach ~$75 billion by 2026 . Irrespective of a favorable U.S. regulatory environment and secular shifts to at-home dining, we believe the potential for growth within the current addressable market by taking share vis-à-vis price (industry leading margins) and service (reliable supplier network) has created a setup uniquely favoring Karat. The below four bullets describe in detail the potential for Karat that lives outside of regulatory and secular tailwinds:

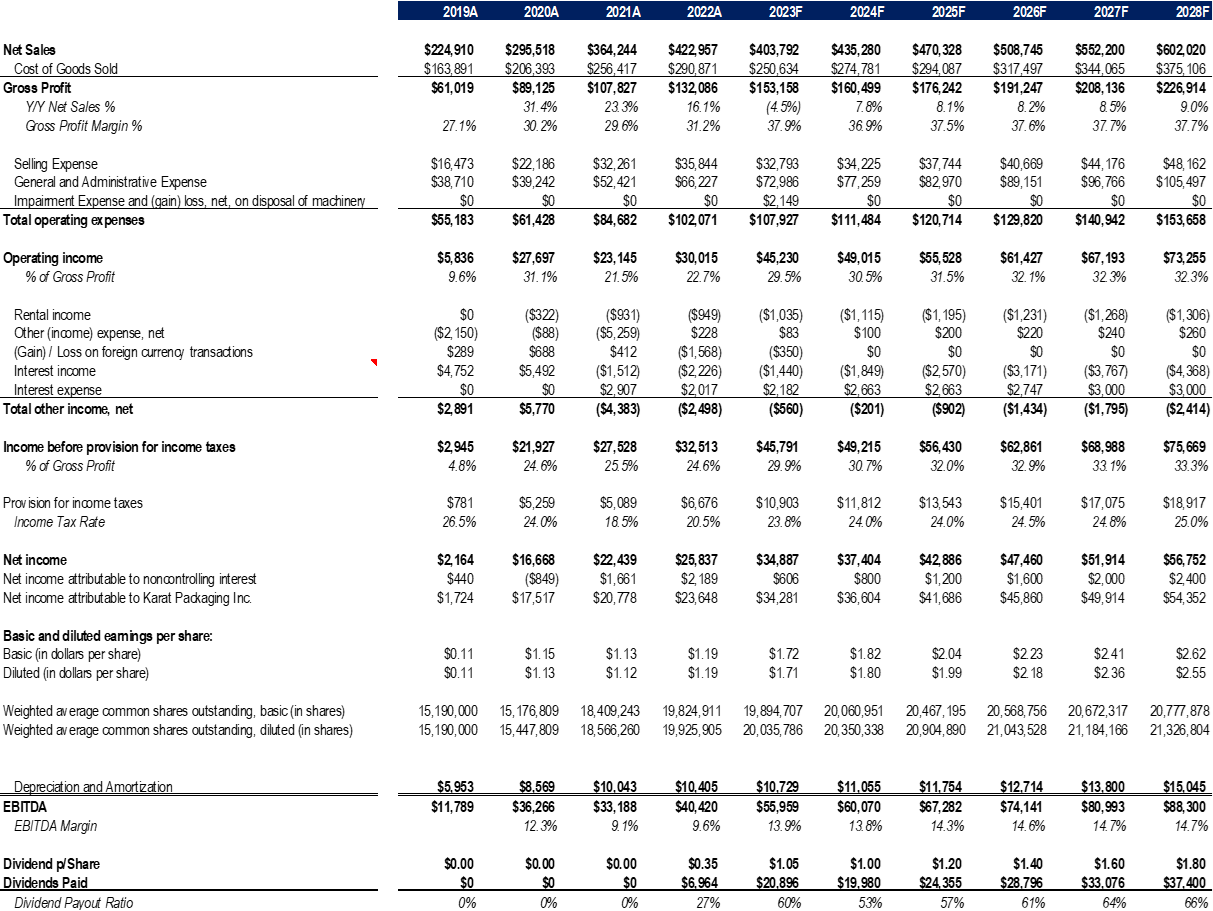

Karat serves a diverse and growing blue-chip customer base, a variety of national and regional distributors, restaurant chains along with retail establishments and online customers. Karat has guided and continues to deliver on new capabilities, products and expanded footprint that has unlocked volume growth with no single customer representing more than 10% of revenue. Despite a modestly down year in 2023E on the back of a deflationary pricing environment, Karat's Net Sales has grown at a 16% annual CAGR since 2019. Easing comps driven by an expected stabilization in pricing coupled with volume growth on the back of warehouse expansion that came online across 2023 creates for a favorable setup heading into the new year where we expect Net Sales to grow high single-digits. Our 2024 growth expectations and longer-term outlook is supported by three pillars of Karat's strategic focus:

The first pillar is premised on expanding distribution network through new products and geographies. The newest sales hires are explicitly targeting expansion into underpenetrated East Coast and Mid-West markets. With headwinds out of California (30% of the total business), geographic expansion is welcomed as Karat looks to create a more balanced model capable of serving customers nationwide. In addition to existing channels, Karat intends to expand its customer base into non-traditional foodservice channels such as airlines, sports and entertainment venues.

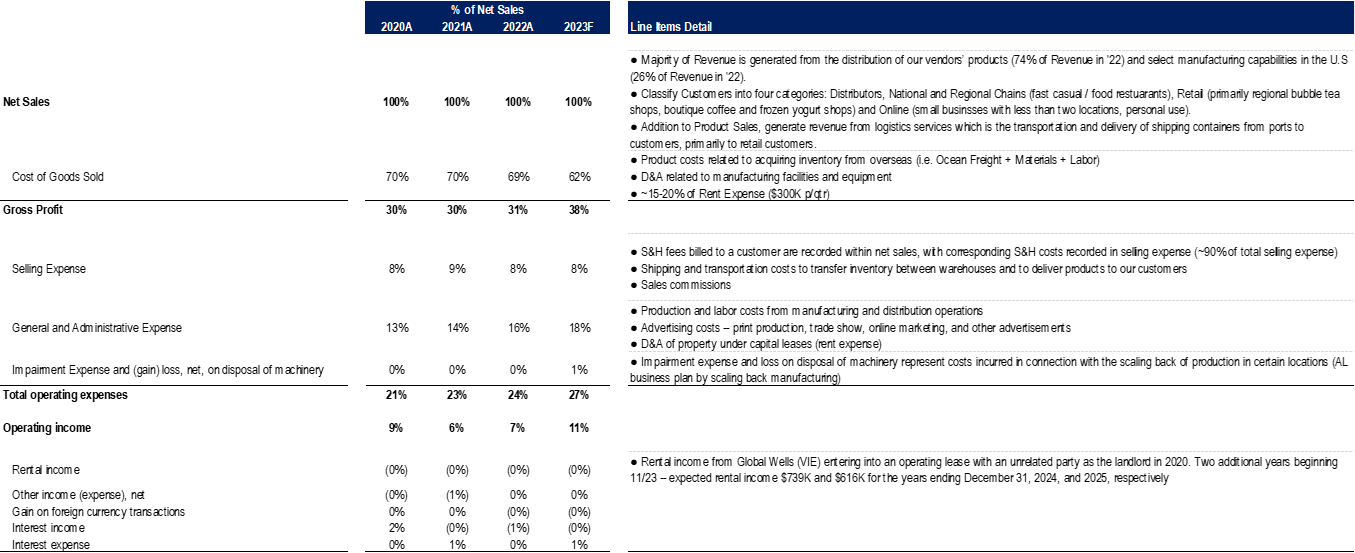

The second pillar is premised on executing on asset-light network by scaling back lower-margin manufacturing business (goal of 10-15% of Net Sales, down from 21% across 1H23) while over-indexing to a higher-margin asset-light import business. We expect Gross Profit Margins to land at 38% in 2023, 7pts higher Y/Y helped by declining shipping costs (YTD mid-single-digit Ocean Freight expense as a % of Net Sales, improved from 14% in 2022), and Karat's strong supplier relationships. At year-end 2022, Karat offered over 8.6K SKUs across a gamut of product categories with an inventory sourcing network increasing from "only a handful of vendors initially to over 70 active vendors". Having the capacity to manufacture offers upside optionality particularly when weighing procurement versus domestic manufacturing costs. The shift towards the higher margin asset-light import business coupled with increased contribution out of eco-friendly Net Sales pads profitability from a challenging volume environment seeing that a higher share of revenue drops to the bottom line.

The third pillar is premised on M&A. Even after $20M of dividends are expected to be paid out in 2024, we forecast Karat to end the year with combined Cash + Short Term Investments in excess of $60M, far ahead of liquidity needed to run day-to-day operations. Barring any unforeseeable hiccups, which is an incredible caveat, we expect Karat to end the year with a strong balance sheet and would encourage inorganic growth avenues - at a reasonable price - which we are not currently modeling. Management has griped about valuation multiples earlier in the year, but has noted an improving environment for potential deal activity. Potential targets include businesses with functioning warehouses and an established customer base largely in underpenetrated geographies.

A Differentiated Model

When we think of sales slides advocating " a differentiated model " in a legacy industry our brains wander to the age-old adage "this time is different". It's more than likely not. However, we can recognize differences versus legacy players and attempt to understand why, and more importantly, for how long will this assumed differentiator last. Karat's secret sauce is its deep supplier relationships. However, like other non-quantifiable assets, what's "it" worth and is the value ascribed in perpetuity. Hard to say. What we can say with certainty is that Karat made its mark during the pandemic sourcing and delivering when many competitors were unable to thanks to deep supplier ties in Asia. The pandemic was a resounding wake-up for customers in need of diversified sourcing options. The reliability Karat provided strengthened its reputation for perhaps not primary slots, but second or third provider roles - which is all incremental sales. The size and nimbleness of Karat is different from its significantly larger peers which separates it from the pack.

I don't let people do projections for me because I don't like throwing up on the desk - Charlie Munger

With Any Forecast Comes Risks to the Model

Net Sales is always a risk and Management has often overpromised and underdelivered with Gross Profit Margin outperformance regularly making up the difference. We see a risk to prices stabilizing in 2024 especially with the sharp deceleration in pricing that's expected to continue into 4Q23. We are not forecasting a sharp rebound, but a flattening of pricing to 2023 levels across the upcoming year. We rank this perceived risk higher than our volume forecast given the new warehouses that came online across the last 12 months.

Costs of Sales such as ocean freight rates, raw materials and labor are variables that are highly unpredictable from where we sit. However, the Gross Profit Margin guide is rarely missed by Karat and we have forecasted margin to worsen 1pt from 2023 (despite the shift to higher margin products and channels) in line with Management's guidance. Perhaps capacity stays loose, and inputs remain cheap and there's upside - were not economists, and firmly believe in Charlie Munger's above quote. If pricing returns, eco-friendly outperforms, or there's an accelerated shift away from Manufacturing there's likely upside in our margin guide. However, if input costs creep higher and there's a lag between passing inflationary costs off to vendors, our forecast may not provide enough padding.

G&A as a % of Net Sales has been a meaningful margin drag with the sell side community left searching for leverage and questioning what's the right run-rate. There's been little to no leverage in this line that comprises 50/50 fixed and variable costs. The Y/Y change to G&A has exceeded Net Sales in six of the last seven quarters with G&A tracking +10% Y/Y in 2023 versus a (5%) decline to Net Sales. We are told the increase is a result of workforce expansion costs (higher warehouse headcount), higher marketing expenses, and increased rental expenses from an expanded warehouse footprint. Conceptually, these make sense. Our pushback is, are there not saves from the shift away from a higher-skilled Manufacturing workforce? Also, Advertising spend has accounted for just 5% of G&A across the 2021 and 2022 fiscal years, while it may be +$2 million versus the same period last year, that is not the sole culprit behind the overall G&A increase. But in that vein, should Management begin reporting out CAC / LTV / ROAS KPIs as a way for the buy and sell side communities to track marketing on the highest margin online channel which is a key pillar of the growth and margin strategy?

It's not all doom and gloom. AI is a real needle-mover not just for automation of office tasks (i.e. Accounting / POs), but in and around warehouse operations, too. We're looking forward to seeing what this could unlock. It's admittedly early innings and we recognize Karat is creating a cost base capable of growth - we just want to underscore that for 3Q23, Karat delivered Net Sales of $106 million on G&A expense of $20 million / 19% of Net Sales. The last reported quarter nearest to this amount was 1Q22 where Net Sales totaled $105 million on G&A expense of $15 million / 15%. Yes, volume is up translating to higher staffing and rental costs associated with servicing this demand, but this is a potential paint point that could erode Gross Profit Margin flowing 1:1 down to EBITDA that needs addressing.

Karat's Current and Forecast Valuation

2024E P&L is not materially different from 2023. Puts and takes are Net Sales are 8% higher and Gross Profit Margin a touch lower, translating to Operating Income and EBITDA +$4 million Y/Y to 11% and 13% of Net Sales, respectively. There's no material change to Working Capital or Cash Flow from Operations, but Free Cash will be strengthened on reduced CapEx required to support the asset-light model. Much of the saves will translate into shareholder returns by way of dividends. Net/net year-end Cash + Short-Term Investments is expected to gain + $18 million ending the year at over $60 million straddling a break-even Net Debt balance.

Objectively, Karat executed in 2023. Assuming 4Q23 hits Management's guide, the improvements to the model have been stairstep - Gross Profit Margin +7pts, EBITDA + $15 million, Cash +$20 million Y/Y. Management has explicitly stated that the margin profile of the business has structurally changed, for the better, because of the shift towards asset-light. 2023 also included declaring and paying out over $17 million of Dividends YTD ($20 million expected in 2024, excluding any special dividends issued). Another year of executing in the public sphere, a structural improvement to the model, and a Management team eager to return shareholder value, it leaves us wondering, has the market rewarded Karat? EV / TTM EBITDA is not relevant when forecasting future returns. However, it is a helpful frame of reference when comparing what new money is willing to pay today for the last 12 months EBITDA versus what a new investor was willing to pay a year ago for the preceding twelve months. We would assume, based on the mentioned improvements to the model, a similar stairstep improvement exiting 2023 to Karat valuation, but to our surprise, it's near identical at 8x TTM EBITDA. Said differently, EV on Dec 31, 2022, was at 8x FY22 / TTM EBITDA, while EV as of Dec 31, 2023, is at a similar multiple on FY23E / TTM EBITDA despite the progress achieved YTD. Make of it what you want, but the reward for a successful 2023 feels like a lot more stick than Karat.

Our F12M Price Target of $27 is arrived by capitalizing FY24 EBITDA of $60 million. The 9x multiple used to capitalize FY24 EBITDA is in line with industry peers, despite the industry-leading margins that Karat offers. When layering in the expected FY24 dividend, an investment in Karat today implies a return greater than 25%. We are incredibly constructive with the stock and recommend this entry point with further upside.

Karat Valuation and F12M Price Target (Company Reports and Proinsias Capital Estimates)

{kind=link}

{kind=link}

Conclusion

We believe an investment today offers a potential Karat shareholder an attractive entry point into a business with experienced operators who collectively own over 65% of shares outstanding, regulatory and secular tailwinds, and industry-leading margins. We encourage investors to strongly consider adding Karat to their portfolio for these reasons.

For further details see:

Karat Packaging: More Karat, Less Stick