KRT - Karat Packaging's Q2: A Stellar Outperformer

2023-08-18 17:30:09 ET

Summary

- Karat Packaging Inc.'s Q2 2023 earnings report showed resilience and strategic adaptability, beating expectations for non-GAAP EPS but missing revenue expectations.

- The company positions itself as a significant player in the single-use disposable products sector, offering a wide range of products and value-added services.

- Despite short-term headwinds, Karat's strategic moves, robust operational model, and outperformance in its sector make it a promising investment for long-term growth and shareholder value creation.

Thesis

Karat Packaging Inc. 's ( KRT ) Q2 2023 earnings report presents a resilient and strategically adaptive company. Despite anticipated price reductions, decreased revenue from logistics services, and shipping charges, the company's Q2 2023 non-GAAP EPS of $0.69 significantly beat expectations by $0.39, although revenue of $108.74M missed by $0.46M. This analysis argues that, despite some short-term headwinds, Karat's strategic moves, robust operational model, and notable outperformance relative to its sector position it as a promising investment, with significant potential for long-term growth and shareholder value creation.

Company Profile

{kind=link}

In examining Karat Packaging Inc. and its subsidiaries, it's clear that they have positioned themselves as significant players in the single-use disposable products sector. Their product lines, marketed under the Karat, Karat Earth Total Clean and Tea Zone brands, are notably comprehensive and encompass plastic, paper, biopolymer-based, and compostable items. Strategically, the company casts a wide net with its customer base, extending its reach to national and regional distributors, restaurant chains, retail establishments, and online consumers. It doesn't stop at products; Karat Packaging also offers value-added services, such as new product development, design, printing, and logistics-a move that suggests a holistic approach to client engagement.

Karat Packaging's Q2 2023 Earnings Highlights

In the face of anticipated price reductions, decreased revenue from logistics services, and shipping charges, Karat Packaging's second quarter results in 2023 have emerged stronger than one might expect. Within this framework, the company's core disposable foodservice product has proven resilient, exhibiting a 5% volume increase compared to the same period in the prior year. What catches my attention is the sustained demand for Karat's eco-friendly products, which has not waned-in fact, sales in this category surged by 22% in the second quarter over the prior year. This is closely aligned with Karat's 2023 goal: for these eco-friendly products to make up about 35% of total sales, marking a clear strategic response to the burgeoning consumer demand for sustainable options.

Now, let's talk margins. Despite a deflationary environment that's affecting the entire industry, Karat's gross margin has held steady-a noteworthy achievement when you factor in the multiple price reductions that have been enacted, and a raw material write-off tied to the disposal of certain machinery and equipment. It seems that Karat's growth strategy, which leans towards being asset-light and focuses heavily on import and distribution, is serving as the key driver of this margin expansion. It's also contributing to improvements in inventory management and fill rates.

On the operational front, there's been substantial movement, too. Karat has been adeptly maneuvering through a phase of operational restructuring and expansion. They're opening warehouses in Chicago and Houston (more on this below in "Risks & Headwinds") and are on the hunt for additional strategic locations, such as Arizona and Florida. The company's vision? To construct a more streamlined and extensive distribution network. This strategy, when coupled with a reduction of manufacturing footprints in certain U.S. locations and a boost in imported items, appears to be a formula that's helping Karat not just achieve, but sustain, a higher margin.

There's also been a significant development on the investment front. Karat finalized the sale of its stake in a joint venture project in Taiwan, and in doing so, recouped a payment that matched its full investment of $6 million, plus interest. When I consider this move in conjunction with Karat's overall operational model and strategic initiatives, it's clear how the company is generating strong operating cash flow. This seems to resonate with the company's Board as well, as evidenced by the decision to declare a special dividend of $0.40 per share, as well as kick off a regular quarterly cash dividend policy at $0.10 per share. It's a tangible way the Board is signaling its confidence in Karat's trajectory and its intent to return value to the shareholders.

Performance: Surpassing Standards, Leading the Sector

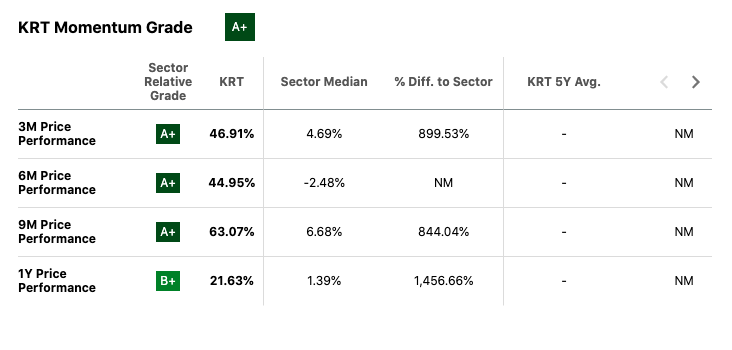

KRT is significantly outperforming its peers, not just slightly edging past them. The Momentum Grade of " A+ " is indicative of this strong performance. Specifically, the data highlights notable distinctions between KRT and the Industrials sector median. For example, KRT's 3M price performance is recorded at 46.91%, in stark contrast to the sector median of 4.69%. The differential here, 899.53%, suggests a remarkable lead within the sector.

{kind=link}

The 9M Price Performance for KRT is 63.07%, which is notably higher compared to the sector's 6.68%. These figures, even if they normalize over time, illustrate a significant point: KRT is setting its own pace, independent of broader market trends.

Moving to KRT's 1Y Price Performance, there is a moderation to a "B+" grade, but its performance of 21.63% still substantially exceeds the sector's median of 1.39%. The wide gap, specifically the 1,456.66% difference relative to the sector, signals noteworthy potential. While the "B+" grade may not be as striking as an "A+," it indicates that KRT has maintained a steady and strong performance over an extended period.

{kind=link}

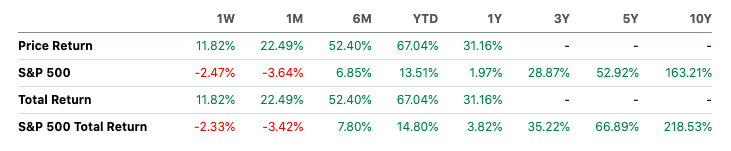

In the context of the broader market, KRT is outperforming not only its sector but also the S&P 500. For instance, KRT's YTD total return stands at 66.76%, which is significantly higher than the S&P 500's (SP500) 14.74%.

Valuation

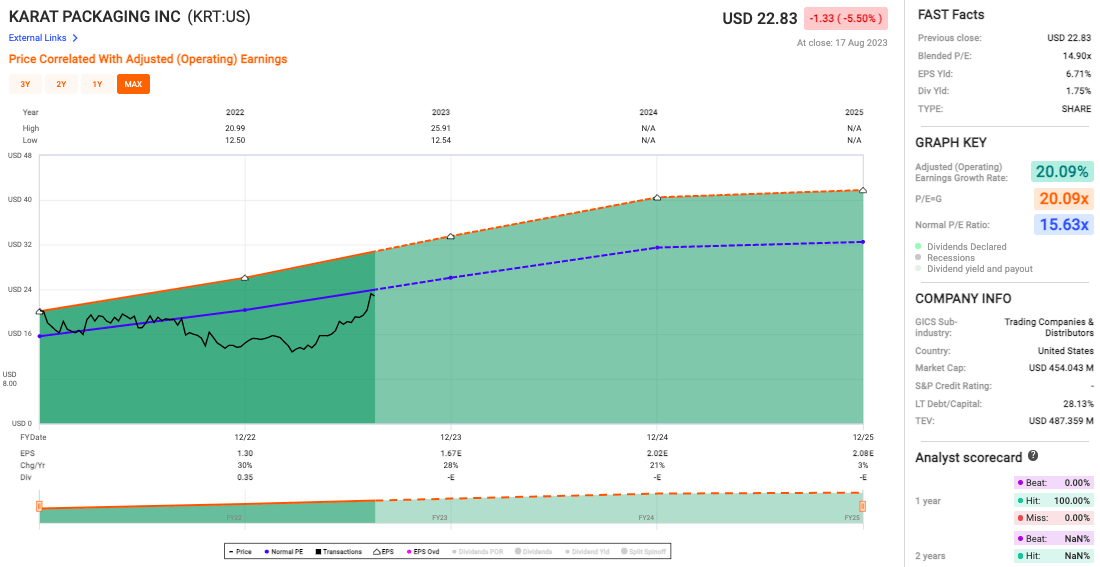

Karat Packaging is sitting at a blended P/E ratio of 14.90x, just a touch below its usual P/E of 15.63x. When stacking that up against its historical average, it's trading at a bit of a discount and puts it on the radar for those who fancy a stock with a decent valuation in terms of its earnings.

{kind=link}

As for the Earnings Per Share ((EPS)) yield, it's hanging out at 6.71%. Typically, a beefier EPS yield might hint that the stock's a bit of a bargain, especially with the kind of ROI it promises which could suggest that the company's earnings are holding strong compared to its stock price.

Risks & Headwinds

Turning the lens to the other side of the picture, Karat's second quarter marked a dip in net sales, decreasing by 5.3% to $108.7 million from $114.9 million in the previous year. This slide is largely tethered to pricing reductions and a downturn in logistics and shipping revenue. Taking a deeper dive into the channels, sales to distributors-which serve as Karat's primary avenue-softened by 5.7% in the 2023 second quarter. It's also worth noting that sales to the retail channel contracted by 13.7%.

The operational hurdles tied to opening new warehouses weren't just a brief hiccup. According to the company, the expectation is for both the Chicago and Houston warehouses to cross the finish line and be fully operational by the end of September 2023. These delays aren't just dates on a calendar-they are translating into tangible impact, as seen in the company's projection for the third quarter of 2023. Here, net sales are forecasted to dip by approximately 3% to 4% year-over-year. This anticipated ebb in the third quarter can be partly traced back to these delayed warehouse operations and unforeseen hold-ups in rolling out certain new chain account agreements.

Now, let's pivot to operating expenses. In the second quarter of 2023, these expenses tallied up to $28.5 million, or 26.2% of net sales, a climb from $26.2 million, or 22.8% of net sales, in the same quarter of the prior year. A standout in this category is the incorporation of impairment expenses and a loss totaling $2.5 million tied to the disposal of machinery. This chunk of change, predominantly stemming from the decision to pare back manufacturing in certain locations, is a clear signal-restructuring, while strategic, comes with its own price tag.

Rating: Buy

I would rate Karat Packaging as a "Buy." Despite facing headwinds such as decreased net sales, operational delays, and increased operating expenses, the company is showing healthy signs of resilience and strategic planning. Financially, the company is outperforming its sector significantly and has a promising valuation with a blended P/E ratio slightly below its historical average. While Karat is navigating through short-term challenges, such as the costs associated with restructuring and anticipated dips in net sales, its strong performance relative to its peers, proactive strategic shifts, and the board's confidence as indicated by the dividend policy, suggest that Karat is positioned for long-term growth and shareholder value creation.

For further details see:

Karat Packaging's Q2: A Stellar Outperformer