KRRGF - Karora Resources: Another Record Quarter

2023-08-01 13:26:45 ET

Summary

- Karora Resources reported record Q2 production and sales, exceeding previous records and putting the company on track to meet and potentially beat its annual guidance.

- Just as importantly, the company has controlled costs well and is expected to see improved margins in Q2 2023 compared to Q2 2022 and Q1 2023.

- However, while Karora is arguably a top-12 gold producer sector-wide given its solid execution & higher margins than peers, I still don't see enough margin of safety at US$3.18.

The Q2 Earnings Season for the Gold Miners Index ( GDX ) has finally begun, and it's been a mixed start overall. This is because while we've seen producers benefit from some softness in energy prices and a stronger gold price, labor, and contraction inflation has remained sticky (which represents a larger proportion of costs), and extreme weather has rained on the miners' parade in many jurisdictions. In Turkey, severe rain throttled back production at Kisladag, in Quebec and Ontario, weather-related power outages and wildfires translated to headwinds at multiple assets (Casa Berardi, LaRonde, Island Gold, Young-Davidson, Lamaque). Fortunately, it's been business as usual in Australia (except for flooding in Queensland that pushed Ernest Henry offline ), and Karora Resources ( KRRGF ) put up another record quarter, releasing its preliminary results last week. Let's inspect the results below:

{kind=link}

All figures are in United States Dollars unless otherwise noted with a C$ in front (Canadian Dollars).

Q2 Production & Sales

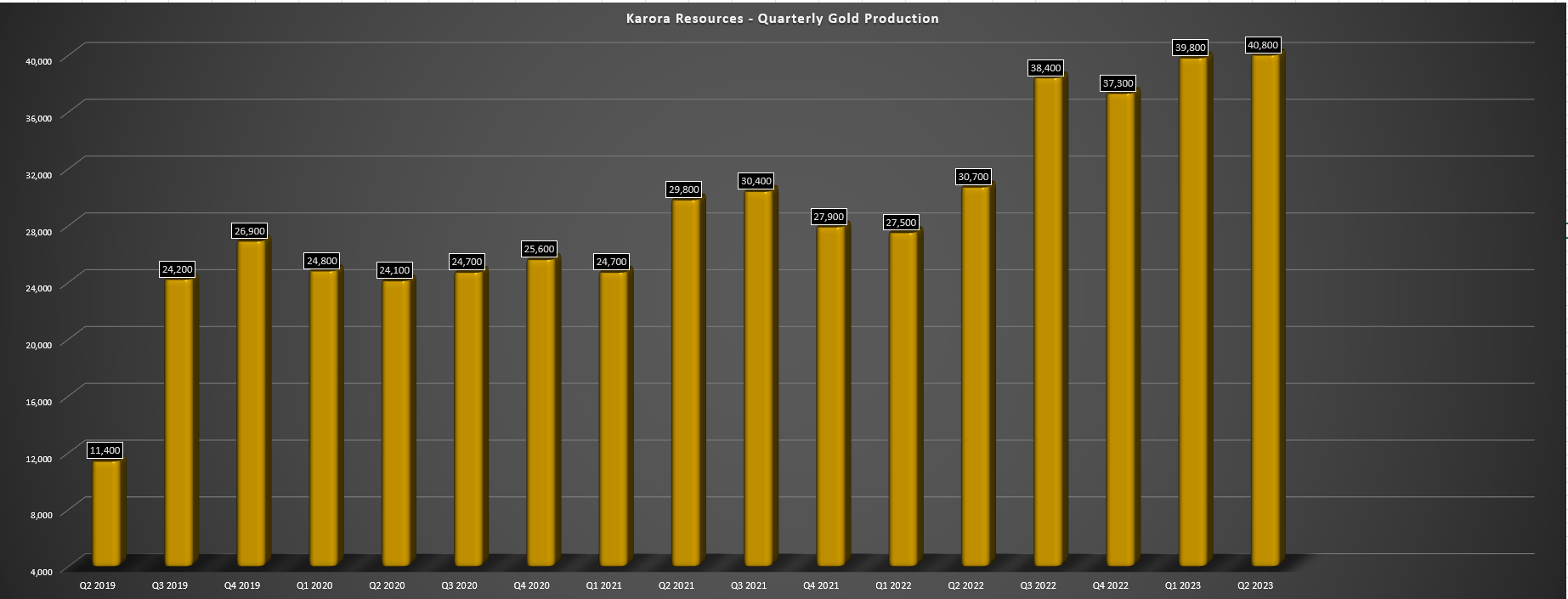

Karora released its preliminary Q2 results last week, reporting quarterly production of ~40,800 ounces of gold, a record that bested its previous record of ~39,800 ounces in Q1 2023. This solid performance translated to a ~33% increase in output year-over-year, and has placed the company well on track to meet its F2023 guidance midpoint of 152,500 ounces, with Karora tracking at ~52.9% of annual guidance ahead of what should be a similar second half with the benefit of its completed second decline at its flagship Beta Hunt Mine and the completion of its remaining two vent raises. Meanwhile, Karora's gold sales came in at ~42,200 and combined with the higher average realized gold price, it should allow the company to generate over C$107 million of revenue in the period (Q1 2023: C$96.8 million), which would also represent a quarterly record.

Karora - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Overall, the solid performance out of Karora is not surprising given its track record of over-delivering on promises since Paul Huet took over as CEO, outside of the odd quarterly hiccup related to unforeseen events such as COVID-19 related labor tightness, absenteeism, and supply chain headwinds that affected its H1 2022 results. And among junior producers, this consistent execution is a rarity, with other names like Jaguar Mining ( JAGGF ), Guanajuato Silver ( GSVRF ) and McEwen Mining ( MUX ) appearing to be on track to miss their guidance midpoints this year, let alone deliver at or near the top end of guidance like Karora in 2023 (Karora's production is sitting at 50.4% of the top end of its guidance). Just as impressively, its second decline was completed early, a critical item to its ~200,000 ounces per annum production goal. So, for investors that are looking for smaller-cap growth stories that can be trusted, this is certainly one of the better names sector-wide among sub $1.0 billion market cap companies in my view.

Costs & Margins

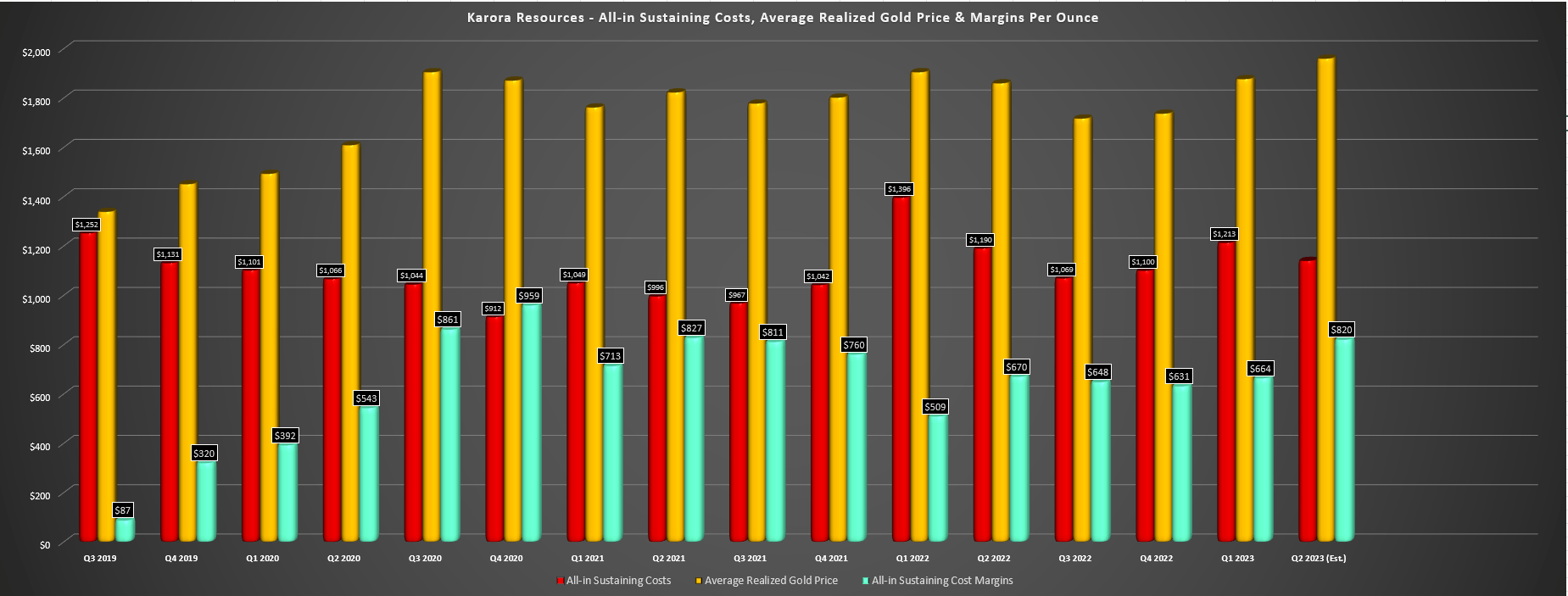

Moving over to costs and margins, Karora benefited from a higher average realized gold price in Q2 2023, with the average producer reporting a gold sales price of US$1,950/oz or better quarter-to-date, suggesting Karora should report a realized price at similar levels. And while the violent decline in nickel prices, elevated sustaining capital year-over-year plus continued mentions of contractor/labor inflation in prolific regions (including Western Australia) were headwinds in the period, Karora's record sales should offset this, allowing it to report sub US$1,150/oz all-in sustaining costs in Q2 2023. And assuming a US$1,960/oz or better average realized gold price, we should see Karora's AISC margins improve to US$800/oz, a meaningful improvement from Q2 2022 levels (US$670/oz) and Q1 2023 levels (US$664/oz).

Karora - Quarterly Costs, Gold Price & AISC Margins (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Meanwhile, from a bigger picture standpoint, Karora may be guiding for higher sustaining capital next year, and we could see labor and contractor inflation persist because of competition for skilled labor in prolific mining regions (and especially Australia where multiple commodities are being produced and sought after like coal, iron ore, gold, and lithium), but the company fortunately has offsets in place. For starters, it's expecting to increase production to upwards of 180,000 ounces of gold next year, helping to offset the impact of increased sustaining capital on costs and overall capex spend on its free cash flow generation. Second, it's also working to ramp up its nickel production next year which will benefit its by-product credits, and added Leigh Junk to its team as Managing Director, Australia. For those unfamiliar, Leigh Junk was previously at Doray Minerals until its merger with Silver Lake ( SVLKF ) to add its high-grade Deflector Project, and has experience with nickel, successfully acquiring/recommissioning nickel operations in the Kambalda area of Western Australia as co-founder of Donegal Resources (private company).

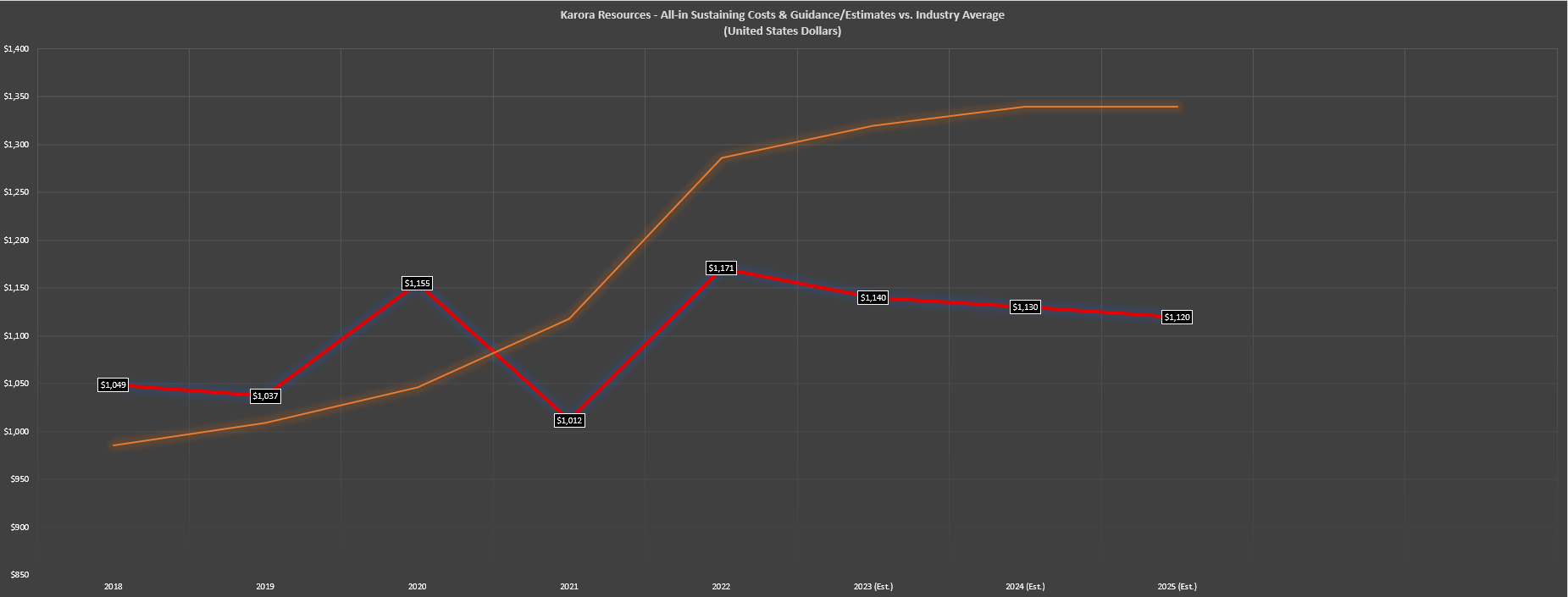

Karora - Annual All-in Sustaining Costs, Forward Estimates vs. Industry Average (Company Filings, Author's Chart)

{kind=link}

This solid addition to the Karora team is a positive as the company looks to ramp up nickel production, and as we can see above, Karora is unique in the sense that it has controlled costs much better than its peer group in a nearly unprecedented inflationary environment. In fact, Karora's all-in sustaining costs should actually decline from FY2020 to FY2025 levels ($1,120/oz estimates vs. $1,155/oz) with the benefit of increased gold and nickel production at Beta Hunt, with the possibility of further gains on production and costs if it increases throughput at Lakewood (1.0 million tonnes per annum to 1.20 million tonnes per annum). So, while many investors may prefer to shy away from producers and stick with royalty companies given the margin compression that we've seen sector-wide (evidenced by the rising costs of the average producer shown above), Karora is an exception, and I would expect a trend of slightly improving costs and rising production looking out to 2025.

Let's look at Karora's valuation and see whether investors are getting an adequate margin of safety to invest in this growth story (160,000 ounces ---> 190,000+ ounces per annum):

Valuation & Technical Picture

Based on ~183 million fully diluted shares and a share price of US$3.48, Karora trades at a market cap of US$637 million, a very reasonable valuation for a company looking to grow production to 190,000+ ounces of gold per annum in a Tier-1 jurisdiction. This is especially true when the company is one of the better exploration stories sector-wide with material upside along its newly discovered Fletcher Shear Zone, and untapped potential in the Gamma Block that's yet to be mined for additional nickel discoveries. That said, the stock has massively outperformed its peers since the Q3 2022 lows with a ~90% gain and while it's held onto these gains, this has contributed to a much less attractive relative valuation vs. some names that have struggled to gain traction. And this is especially true on a risk-adjusted basis relative to some majors that are trading at their lowest P/NAV multiples in years outside of March 2020 and September 2022.

Using what I believe to be a fair multiple of 1.0x P/NAV for a Tier-1 jurisdiction producer with below-average costs and 7.0x FY2024 operating cash flow estimates and applying a 65/35 weighting for price to net asset value (65%) and price to cash flow (35%), I see a fair value for Karora of US$4.18. This points to a 20% upside from current levels to its 18-month price target (year-end 2024). And while this is a decent upside, I am looking for a minimum 40% discount to fair value to justify buying new positions in small-cap producers, regardless of if they have a solid track record of beating estimates and whether they operate in Tier-1 jurisdictions. So, while I see some upside in Karora here to fair value, the updated low-risk buy zone comes in at US$2.52 or lower, making it tough to justify paying up for the stock here.

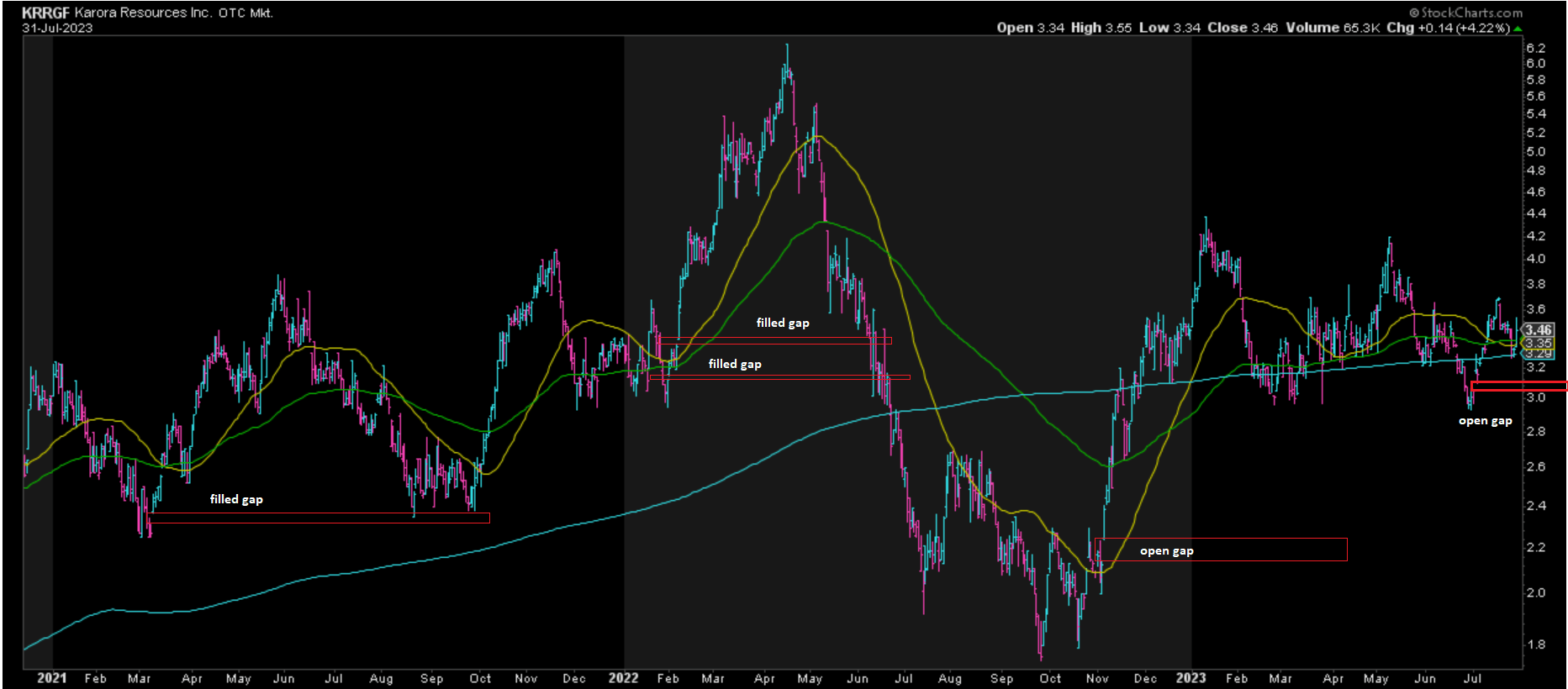

The last point worth noting is while Karora may have upside to fair value, the stock has a track record of filling its open gaps, and we continue to have open gaps at US$3.05 and US$2.15. And while the lower one looks like it could go unfilled due to being a runaway gap, it's harder to rule out the upper gap at US$3.05 being filled. And just as some investors said that the stock would never fill its open gaps following the Father's Day Vein discovery in 2018, it filled these gaps at ~US$0.75, ~US$1.10 and ~US$2.05, and it did not chase the stock after its violent rally. This time could be different with Karora being a more established producer that's on its way to generating meaningful free cash flow in 2025, but we saw the same in 2021, with two gaps that never looked like they'd get filled being filled before a 20% drawdown below these open gaps. So, while there are no certainties, it's hard to have a strong conviction that there's limited downside from here, given Karora's propensity to fill gaps in the past.

{kind=link}

{kind=link}

Summary

Karora put together another solid quarter in Q2 and continues to meet or exceed my expectations for execution on its growth plans and exploration upside, with the latter helping to support its valuation from a NAV standpoint. That said, the stock has massively outperformed its junior producer peer group, and while it remains very reasonably valued, I prefer to buy miners when they're hated and being given away, not when they're up ~100% off their 52-week lows. This doesn't mean that Karora can't head higher short term, and if the gold price can cooperate, the stock could break its streak of filling over 80% of its unfilled gaps. That said, with several other names on the sale rack among miners and other sectors and Karora offering significantly less margin of safety than its peers, I remain focused on what I believe to be more attractive opportunities elsewhere.

For further details see:

Karora Resources: Another Record Quarter