KRRGF - Karora Resources: Cheap For No Reason

Summary

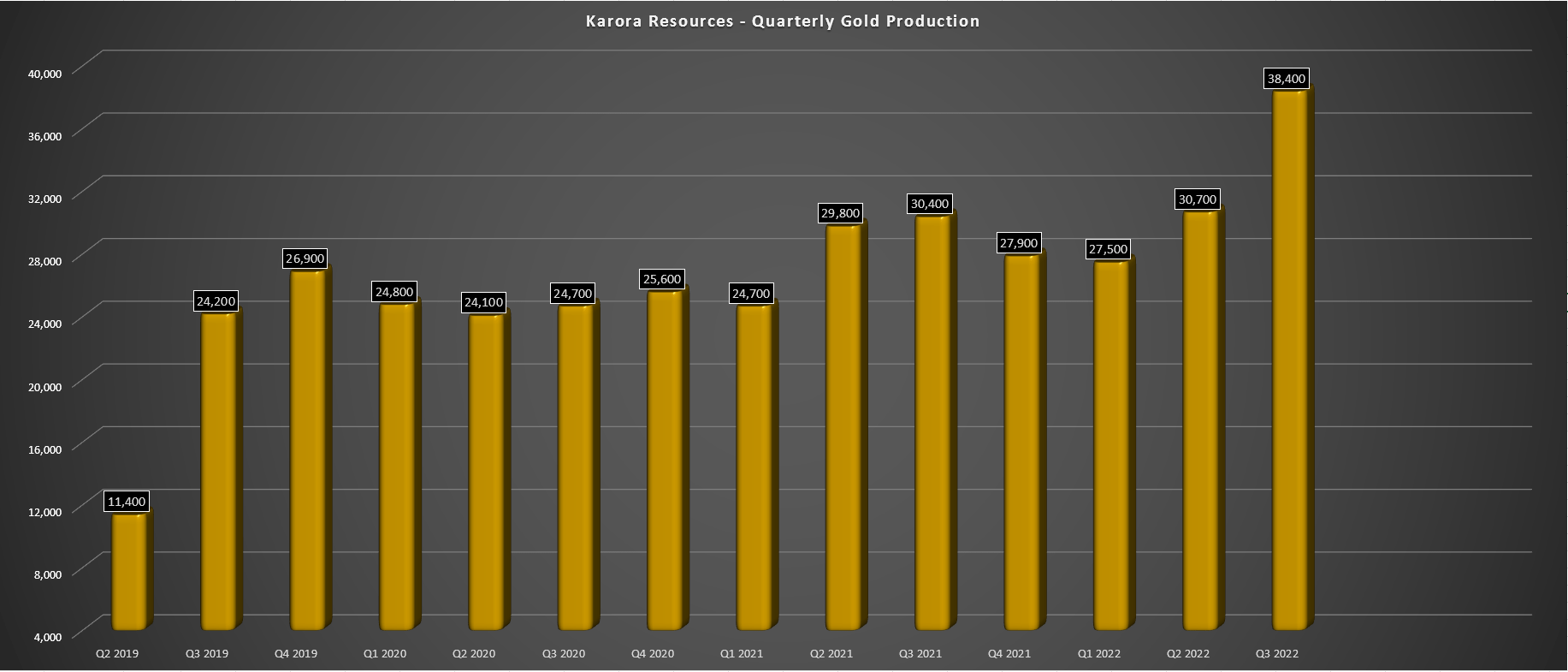

- Karora Resources released its Q3 production results last month, reporting record production of ~38,400 ounces, a 25% beat vs. its previous record.

- In addition to solid operational results, the company remains on time/budget for its second decline, which will be operational by Q2 2023 and continues to have exploration success.

- With one of the best growth profiles sector-wide and an improving cost profile, I see this pullback in Karora towards US$2.00 as a gift.

While the general market has suffered a significant correction, with its drawdown exceeding 27%, the Gold Miners Index ( GDX ) has suffered the real bear market. This is evidenced by a 53% correction from its 2020 highs. Given that bear markets take time and damage to eradicate bullish sentiment, I continue to see immense opportunity in the gold sector, where the 27-month cyclical bear market has ground any remaining optimism to fine dust. So, with one of the sector's highest-growth producers trading at barely ~2.0x FY2023 cash flow, I see this pullback in Karora Resources ( KRRGF ) towards US$2.00 as a gift.

Q3 Production & Sales

Karora Resources ("Karora") released its preliminary Q3 results last month, reporting a new quarterly record of ~38,400 ounces of gold production, a 26% increase from the year-ago period. This was driven by adding a second mill (Lakewood purchase) that increased total mill throughput and the benefit of a coarse gold discovery made earlier this year that contributed ~2,500 ounces of gold. The result is that Karora has produced nearly 97,000 ounces year-to-date, on track to beat its FY2022 guidance mid-point of 122,500 ounces despite a very challenging start to the year due to COVID-19 exclusions combined with a tight labor market in Western Australia.

Karora - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Karora noted in its prepared remarks that adding the second mill at Lakewood allowed for the optimization of feed blend from multiple mines combined with surface stockpiles. Just as importantly, the Lakewood Mill is closer to its Beta Hunt Operations than the Higginsville Mill, allowing for savings from a fuel standpoint for its gold operations. In addition, it's already benefiting from shorter haulage distances for its nickel due to the restart of the Kambalda Nickel Concentrator, a more than 300-kilometer savings per trip vs. the previous drive to Leinster. Finally, as of the most recent update, Karora's second decline was 67% complete and ahead of schedule, an impressive feat given the tight labor market for contractors and workers.

Karora Resources - Annual Gold Production & Forward Estimates (Company Filings, Author's Chart)

{kind=link}

Looking at the big picture, we can see that Karora is well on its way to mid-tier producer status (200,000+ ounces per annum), with a new record of 132,000+ ounces on deck this year, and over 175,000 ounces likely to be produced next year. Moving ahead to FY2024-FY2026, I would expect annual gold production to average at least 200,000 ounces per annum, in line with the company's stated goal of 185,000 to 205,000 ounces per annum of annual gold production by 2024. At the same time, Karora is working to increase its nickel production, resulting in a significant decline in operating costs with a higher denominator and additional by-product credits.

Most importantly, unlike other companies looking to grow production, Karora side-stepped a potential capex blowout by acquiring Lakewood and not trying to upgrade its Higginsville Mill in an inflationary environment with elevated labor costs. This should translate to a higher multiple for the company vs. peers where there's elevated uncertainty of share dilution and taking on high amounts of debt to complete growth projects. One example is Argonaut ( ARNGF ), which diluted shareholders by over 100% in the past two years due to a mismanaged build of its new Magino Mine. Karora is not in this position, and its second decline to boost throughput to 2.0 million tonnes per annum remains on budget .

Recent Developments

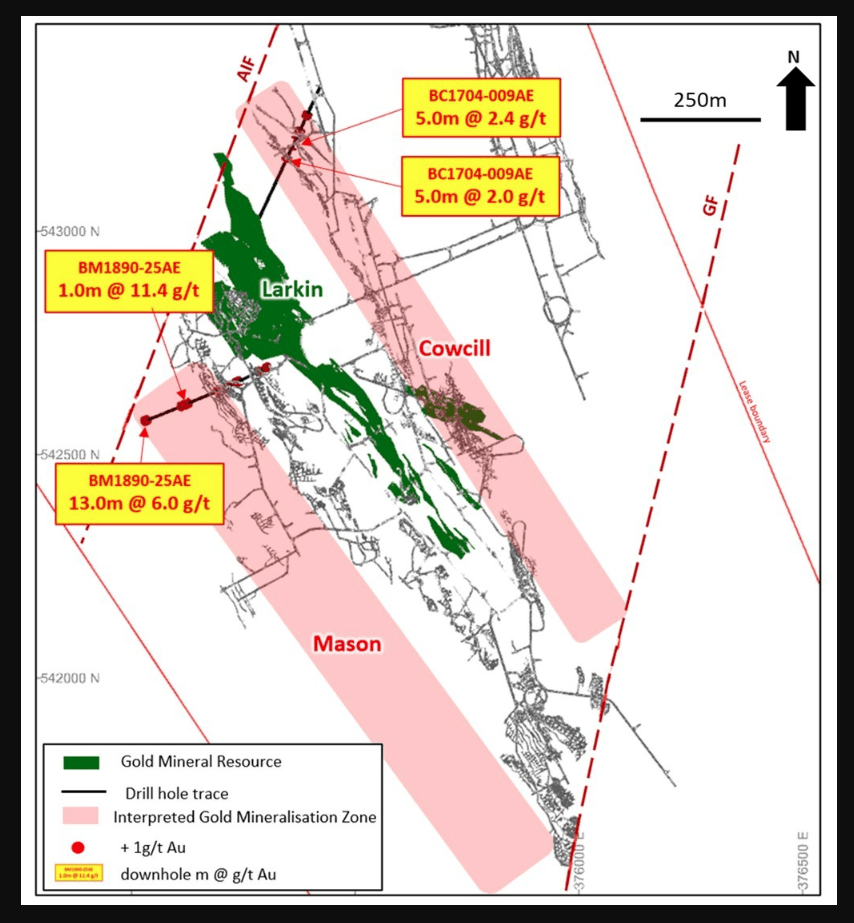

While the execution by the team to date has been solid from an operational and development standpoint, the exploration success is also noteworthy. On top of a new high-grade coarse gold discovery announced in August on level 16 of the A Zone (just below the Father's Day Vein), Karora continues to report high-grade mineralization near Larkin and Western Flanks. Beginning with Larkin, Karora hit high-grade intercepts in two parallel mineralization systems to Larkin (Cowcill and Mason), with highlight intercepts from Mason including 13.0 meters at 6.0 grams per tonne of gold and 17 meters at 12.0 grams per tonne of gold.

These high-grade intercepts suggest the potential to grow resources materially south of the Alpha Island Fault, with the Larkin Zone discovery interpreted as the southern fault offset extension of the Western Flanks. As we saw from the Q2 news release, Larkin has attractive grades (2.4+ grams per tonne of gold) and remains open along strike and down-dip, boding very well for mine-life extensions at similar or better grades. Importantly, these areas were previously relatively untested for gold mineralization, suggesting that a lot of gold may have been left here by previous operators. Notably, these areas were relatively untested for gold mineralization with a focus on nickel previously, with this being somewhat virgin ground for new gold discoveries.

{kind=link}

Meanwhile, Karora intersected 10.8 meters at 3.1 grams per tonne of gold and 5.4 meters at 3.6 grams per tonne of gold (true widths not yet available) that have extending mineralization 250 meters below the current Western Flanks mineral resource at slightly higher grades. Separately, infill drilling at Western Flanks to upgrade inferred resources has impressed as well, with highlight intercepts including 4.7 meters at 11.5 grams per tonne of gold and 3.5 meters at 20.2 grams per tonne of gold.

Finally, on the nickel front, Karora made a new discovery just 25 meters from its existing mining infrastructure in September. The company hit a highlight intercept of 6.5% nickel over 11.9 meters above its gold mineral resource in the Hunt Block above the Western Flanks. Karora noted that it believes this could be an offset to the 4C nickel trough mined by Reliance in 2004/2005. Overall, this continued exploration success at Beta Hunt certainly justifies the construction of a second decline, given that this mine has a lot to offer from a resource growth standpoint, and it makes sense to pull this cash flow forward with higher mining rates.

Valuation

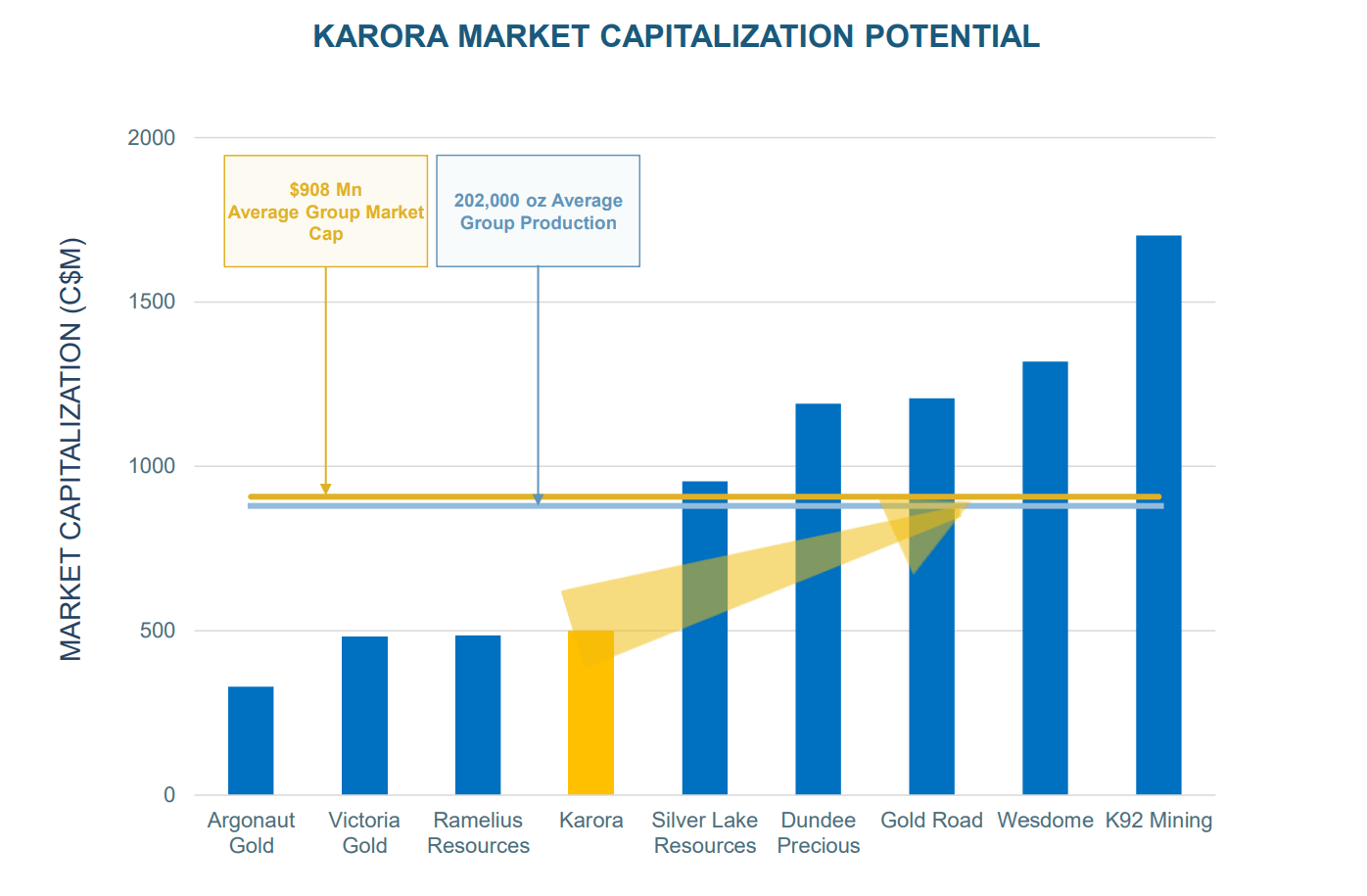

Based on ~181 million fully diluted shares and a share price of US$2.05, Karora Resources currently trades at a market cap of ~$371 million. This is a dirt-cheap valuation for a company set to grow into a ~200,000-ounce producer in 2024 at industry-leading all-in-sustaining costs below $1,000/oz. This has left the company at a similar valuation to some explorers that will be lucky to be free-cash-flow positive this decade, like Snowline Gold ( SNWGF ), and it's left Karora trading at just ~$137/oz on M&I resources and ~$94/oz on total resources. However, these figures don't include any upside at Larkin, nor do they include potential resources at Mason and Cowcill (parallel to Larkin) or potential reserve upside at Western Flanks Deeps (250 meters below current resources).

From a P/NAV and cash flow standpoint, Karora trades below 0.40x P/NAV despite operating in a Tier-1 jurisdiction with well-below-average costs and considerable resource upside. Meanwhile, from a cash flow standpoint, Karora trades at just ~2.3x FY2023 cash flow estimates using conservative estimates of US$0.89, making it one of the cheapest producers sector-wide. So, based on what I believe to be a fair multiple of 4.5x cash flow and 1.0x P/NAV, I see more than a 120% upside from current levels. Importantly, these cash flow estimates don't incorporate any upside in the gold price, so I see these estimates as achievable and beatable, especially if the company continues its track record of over-delivering on promises.

{kind=link}

If we dig into the chart above, we can see the re-rating potential of the stock, with Karora trading at half the market cap of its peer group. Regarding the low end of the peer group, Karora should not be trading anywhere near Victoria ( VITFF ) and Argonaut, who have higher-cost operations and poor track records of delivering on promises. On the high end, outside of grades, Karora shares many similarities with Wesdome ( WDOFF ), given that it's in a Tier-1 jurisdiction (Australia vs. Canada), is growing to ~200,000 ounces per annum, and continues to grow its resources/reserves. Some might argue that Wesdome deserves a premium for grades, which is fair. Still, what Karora lacks in grades, it makes up for with nickel by-product credits and existing development at Beta Hunt, allowing it to enjoy industry-leading margins.

Summary

Given the violent correction we've seen in the gold sector, there are now several names on the sale rack, especially in the small-cap space. The problem is that many of these names are cheap due to an inability to deliver on promises, cost increases that have led to razor-thin margins, and/or weak balance sheets/risk of share dilution. In Karora's case, the company continues to over-deliver, it continues to generate significant cash flow even at $1,650/oz gold prices, its growth is fully funded, it has less capex risk than peers (purchased a mill vs. upgraded one), and it continues to release exceptional drill results at its flagship mine.

Finally, like Agnico Eagle ( AEM ), Karora has a benefit that, unlike many of its peers, should reduce operating costs year-over-year and help claw back lost margins. This is because nickel by-product credits could shave ~$50/oz off costs despite a conservative nickel price assumption ($20,000/ton) as its contribution from nickel increases. So, with Karora set to see a more robust profile despite lower gold prices yet being thrown out with the proverbial bathwater, I see this pullback towards US$2.00 as a buying opportunity.

For further details see:

Karora Resources: Cheap For No Reason