KPTI - Karyopharm: Recent Sell-Off Hits A New Buy Target

Summary

- Karyopharm is still reporting growth, but the market continues to punish KPTI to fresh 52-week lows.

- I take a look at the company's Q3 earnings report. XPOVIO delivered strong year-over-year growth with $32M, up from $26.7M in Q3 of last year, representing 20% growth year-over-year.

- My KPTI position is still dormant, but the recent sell-off has moved KPTI to my Buy Target 2. I discuss how I determine my Buy Target 2.

- KPTI has a few downside risks to consider. Therefore, KPTI will remain in the Compounding Healthcare “Bio Boom” speculative portfolio with a 3 out of 5 conviction rating.

Karyopharm Therapeutics ( KPTI ) has sustained its efforts in supporting XPOVIO’s growth, which has led to another quarter of significant growth in net product revenue growth. Karyopharm continued to maximize XPOVIO's growth in the multiple myeloma market while pushing its clinical pipeline programs closer to the finish line. Unfortunately, the market has continued to disregard the company's progress and has allowed the stock to hit fresh 52-week lows in this recent sell-off. I have remained patient throughout 2022 while looking for a high conviction reversal setup to add to my position, but I have yet to see an attractive opportunity. Now, the stock’s valuation is around “Buy Target 2”, which has encouraged me to finally take advantage of this opening and will add to my inactive KPTI position.

I intend to review Karyopharm's Q3 performance and will highlight the company's long-term growth prospects. In addition, I discuss my “Buy Target 2” and how it impacts my buying activity. Finally, point out some notable downside risks and how they will influence my position management in the coming years.

Q3 Performance

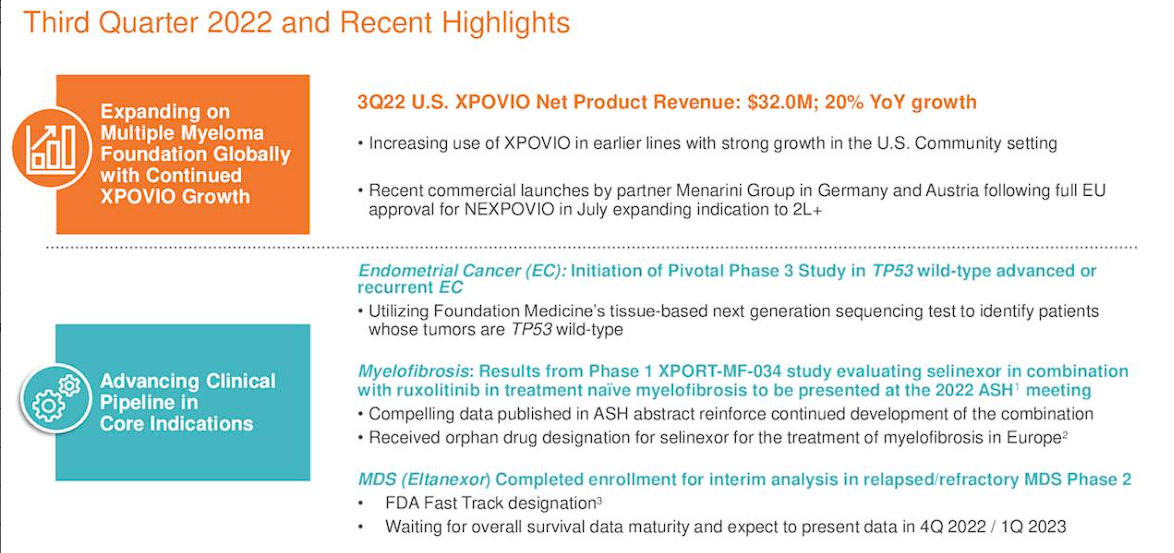

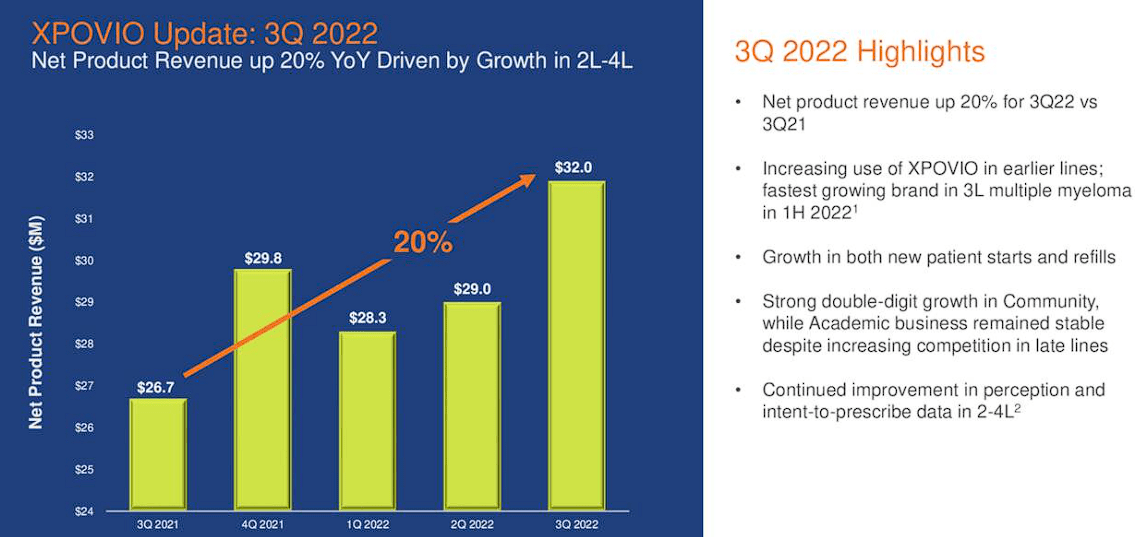

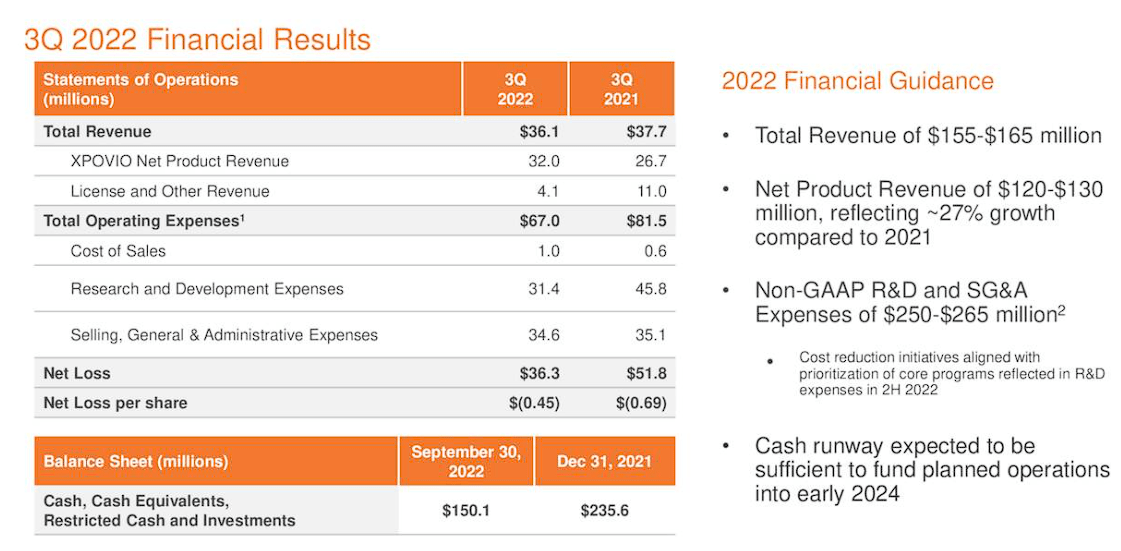

In Q3 , Karyopharm's total revenues dropped to $36.1M, down 4% from $37.7M in Q3 of last year. The drop in total revenues was attributable to a decrease in partner revenue, which was only $4.1M, compared to $11M for Q3 of 2021. It is important to note that last year the company had $9.8M in milestones from Antengene Therapeutics. However, XPOVIO delivered strong year-over-year growth with $32M, up from $26.7M in Q3 of last year, representing 20% growth year-over-year.

Karyopharm Therapeutics Q3 Highlights (Karyopharm Therapeutics)

{kind=link}

What is more, the company reported that it is seeing growth in new patient starts and reviews. Moreover, XPOVIO is being employed in earlier lines of therapy and is the fastest-growing brand in the third-line MM in the first half of 2022.

Karyopharm Therapeutics XPOVIO Update (Karyopharm Therapeutics)

{kind=link}

Furthermore, the company’s market research indicates that prescribers have a favorable view of XPOVIO and have a strong intent to prescribe in the second-to-fourth lines. Moreover, Karyopharm’s partners have recently launched XPOVIO (NEXPOVIO in Europe) in some EU countries. All of these items should lead to additional growth in the coming quarters.

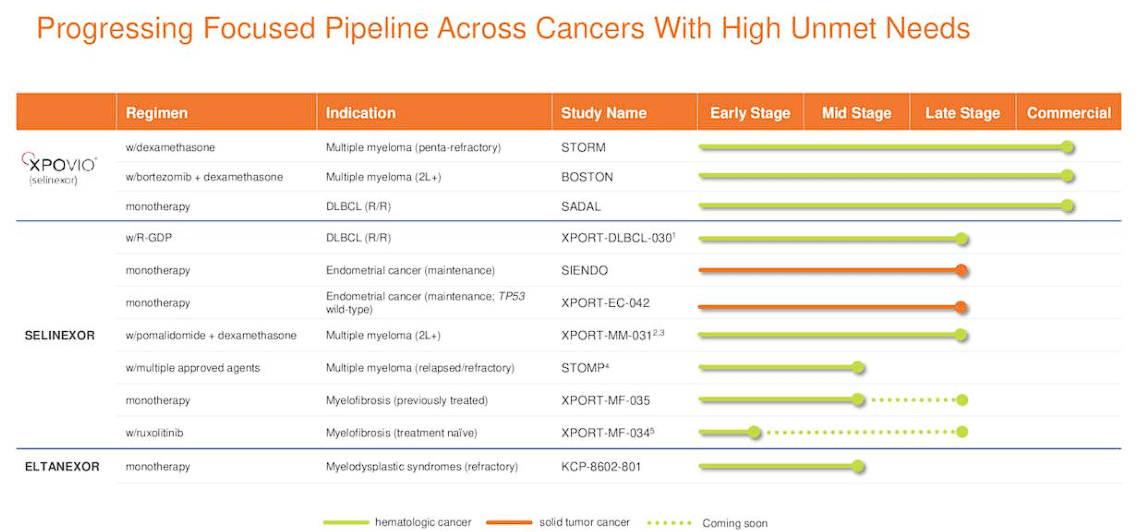

In terms of the pipeline, the company initiated its pivotal Phase III study in TP53 wild-type advanced or recurrent endometrial cancer. Eltanexor’s enrollment in the Phase II study in MDS is complete and the company expects data before year-end or Q1 of 2023.

Karyopharm Therapeutics Pipeline Progress (Karyopharm Therapeutics)

{kind=link}

In terms of expenses, the company's Q3 R&D expenses were $31.4M, down from $45.8M in Q3 of last year. The decrease was primarily attributable to a $7.4M cost from the acquisition of assets from Neumedicines in Q3 of 2021. Moreover, the company reported that clinical trial costs decreased year-over-year. For SG&A, Karyopharm posted $34.6M for Q3, down from $35.1M for Q3 of last year. Overall, the company reported a $36.3M net loss for the quarter, down from $51.8M in Q3 of last year. Looking at the company’s cash position, it finished Q3 with $150.1M in cash, cash equivalents, restricted cash, and investments, which the company believes will fund operations into 2024.

Karyopharm Therapeutics Q3 Financials (Karyopharm Therapeutics)

{kind=link}

The company’s Q3 performance encouraged Karyopharm to update its 2022 revenue guidance to $155M-$165M, with net product revenue coming in at $120M-$130M… up 27% over 2021. The company’s non-GAAP expenses will be in the range of $250M-$265M for 2022.

A Discussion On My “Buy Target 2”

My systematic approach to position management employs both fundamental and technical analysis in order to take advantage of the opportunities those forces provide to buy or sell at near-optimum prices. I use “Buy Thresholds” or “Buy Targets” in order to define prices that will determine my buying frequency and sizing. I use “Sell Targets” for sell orders in order to book profits and help move my positions to a “house money” status.

My “Buy Target 2” is essentially where I believe the share price is discounted based on the company’s fundamentals and is oversold on the stock’s technical analysis. Once a stock gets to Buy Target 2, the gloves come off and I am looking to make upsized buy orders on almost any reversal setup. The size and frequency of these orders are dependent on how many shares I will need to get to a full-sized position, so every ticker has a unique game plan to get there.

KPTI is currently trading near its Buy Target 2 of $3.00 per share, which indicates that I believe this price is discounted.

Why Do I Think KPTI Is Discounted?

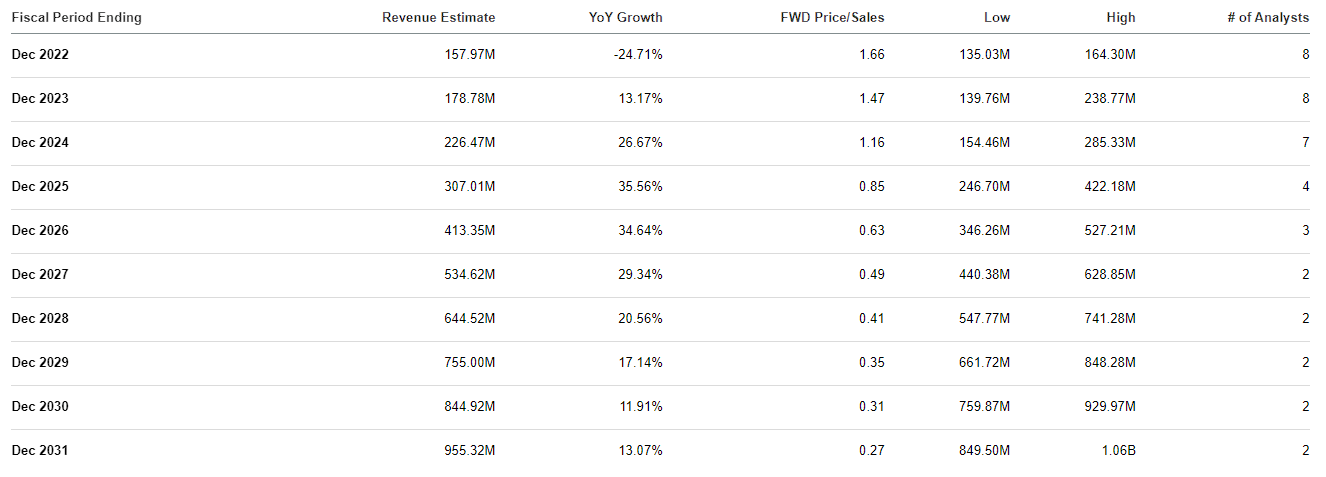

First, the company’s 2022 revenue guidance is $155M-$165M, and the market cap is ~$245M, so the stock is trading less than 2x price-to-sales. Considering the sector’s average price-to-sales is 4x-5x, we can say KPTI is trading at a discount to its peers.

Karyopharm Revenue Estimates (Seeking Alpha)

{kind=link}

Indeed, Karyopharm is reporting losses and is thinning its cash position, so we can’t expect KPTI to be trading at a premium and there is a strong likelihood there will be a dilution event at some point in the coming years. However, it is still hard to believe that KPTI is trading at such a discount for 2022 projected revenue, especially considering the projected revenue growth over the remainder of the decade. In fact, the Street projects that Karyopharm will report strong double-digit growth in the coming years and will cross $500M in revenue in 2027, which would be a 0.49x forward price-to-sales. So, not only is KPTI discounted for its projected 2022 revenue but it is dramatically discounted for forward estimates. What is more, the company could more than double the amount of KPTI shares and the share price would still be trading at a discount.

In addition to price-to-sales, I often employ a DCF growth model, EV/EBITDA model, P/E Multiple, Earnings Power Value, and a Dividend Discount Model to determine Buy Targets and Sell Targets. Most “Bio Boom” tickers are not profitable, so I am limited to enterprise values and forward estimates to help determine my targets.

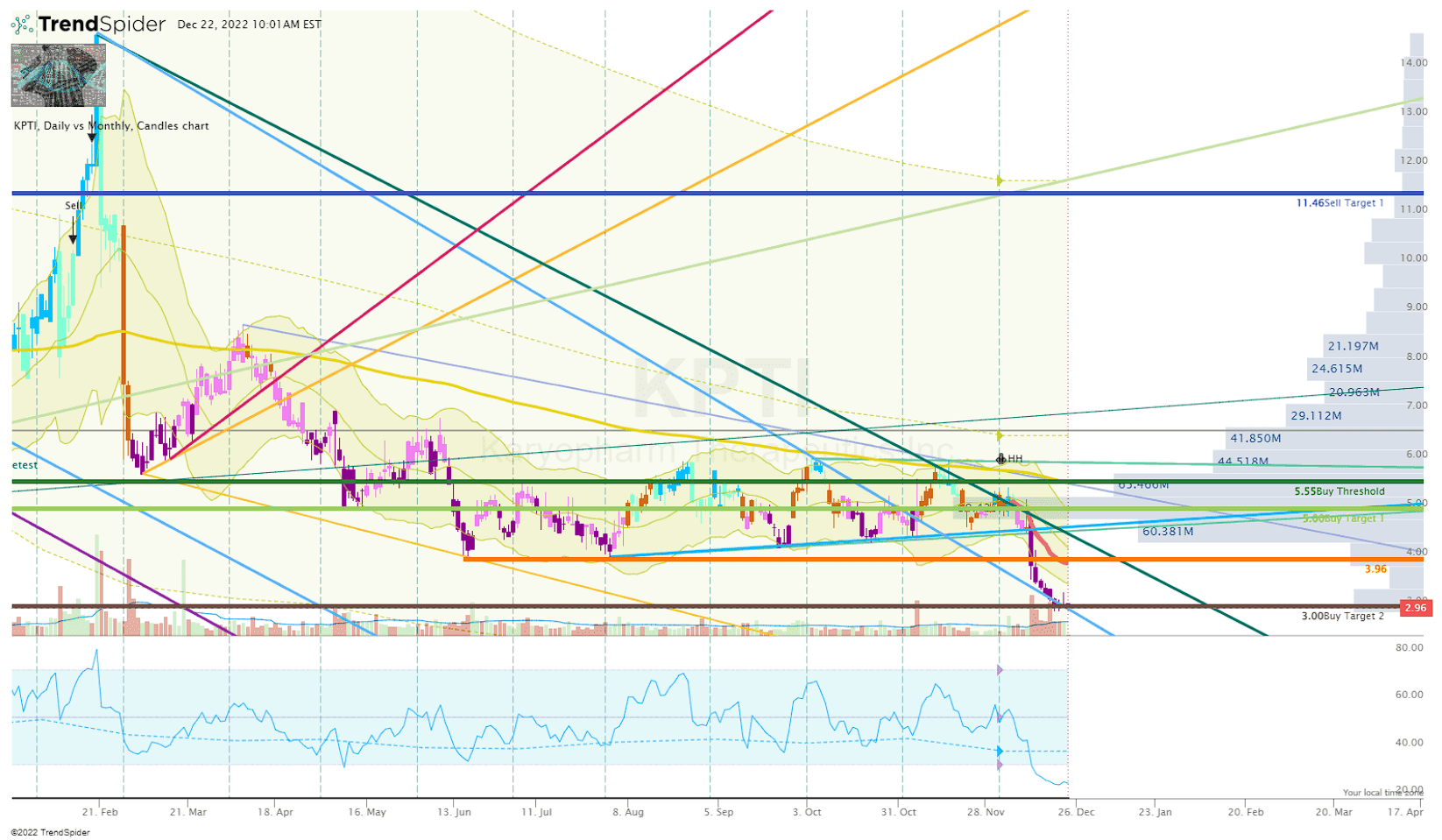

On the technical side, the stock has been selling off for most of 2022 and has lost over 50% of its value over the past twelve months. KPTI just dropped below $3 per share to hit fresh 52-week lows.

KPTI Daily Chart ( TrendSpider )

{kind=link}

The latest downturn in the market has pushed the share price outside the Keltner Channel and plunged the Daily RSI below the Monthly RSI. Typically, these steep dives outside the Keltner Channel generate an opportunity to add near a new low before a potential mean reversion move.

As I mentioned above, the Buy Target 2 is determined by a combination of fundamental and technical analysis. Considering KPTI’s valuation and oversold state, I have determined the ticker’s Buy Target 2 is $3.00 per share.

Conviction While In The Red

It is not wise to simply pick any ticker and haphazardly click the buy button just because the ticker is trading at a discount or it is oversold. It is possible the ticker continues its collapse and the investor could end up losing some or all of their investment. On the other hand, if an investor has a high conviction in the company and the ticker’s performance, adding in the midst of steep sell-offs can be an opportunity to manage their position during elevated trading volume. My high conviction in KPTI is primarily fueled by XPOVIO’s potential in multiple myeloma, endometrial cancer, and myelofibrosis.

In addition, the company has Eltanexor for myelodysplastic syndromes. Collectively, these programs could lead to a number of regulatory approvals over the next few years, thus, profoundly growing the company’s markets.

Another aspect to consider is Karyopharm’s partners which should deliver growing revenue streams in the coming years as they secure additional approvals in their respective regions.

Indeed, it is possible that the company and its partners fall short of expectations, but it is hard to find a convincing argument that Karyopharm’s intrinsic value is going to deteriorate in the next few years. The company's flagship product still has sufficient opportunities to grow, as well as additional upside potential from Eltanexor that could help fuel the estimated double-digit growth for the balance of the decade.

Perhaps Peter Lynch’s adage of “know what you own and why you own it” works well in this circumstance… a ticker that is trading at a discount for its current revenue with plenty of opportunities for additional growth.

Downside Risks

Of course, KPTI has a few risks that do challenge my bullish conviction. Primarily, Karyopharm has strong competition in the late-line from cell therapies and immunotherapies. Certainly, these therapies are expensive and can be a multi-stage process, so they are not a true match-up for XPOVIO. However, these cutting-edge therapies could become a concern if their durability improves and their performance justifies their price tags. Another concern is if XPOVIO fails to expand its label, which will hurt the company's long-term growth outlook and the share price. Last, the company’s funding could become a concern in the coming years even if XPOVIO’s growth remains on track with projections. The company’s current cash position should last into 2024, but it doesn’t look like the company will be able to hit breakeven beforehand. Therefore, investors need to accept there is a strong likelihood the company will have to perform some form of dilutive funding in the future.

Considering these arguments, KPTI will remain in the Compounding Healthcare "Bio Boom" speculative portfolio with a 3 out of 5 conviction rating.

My Plan

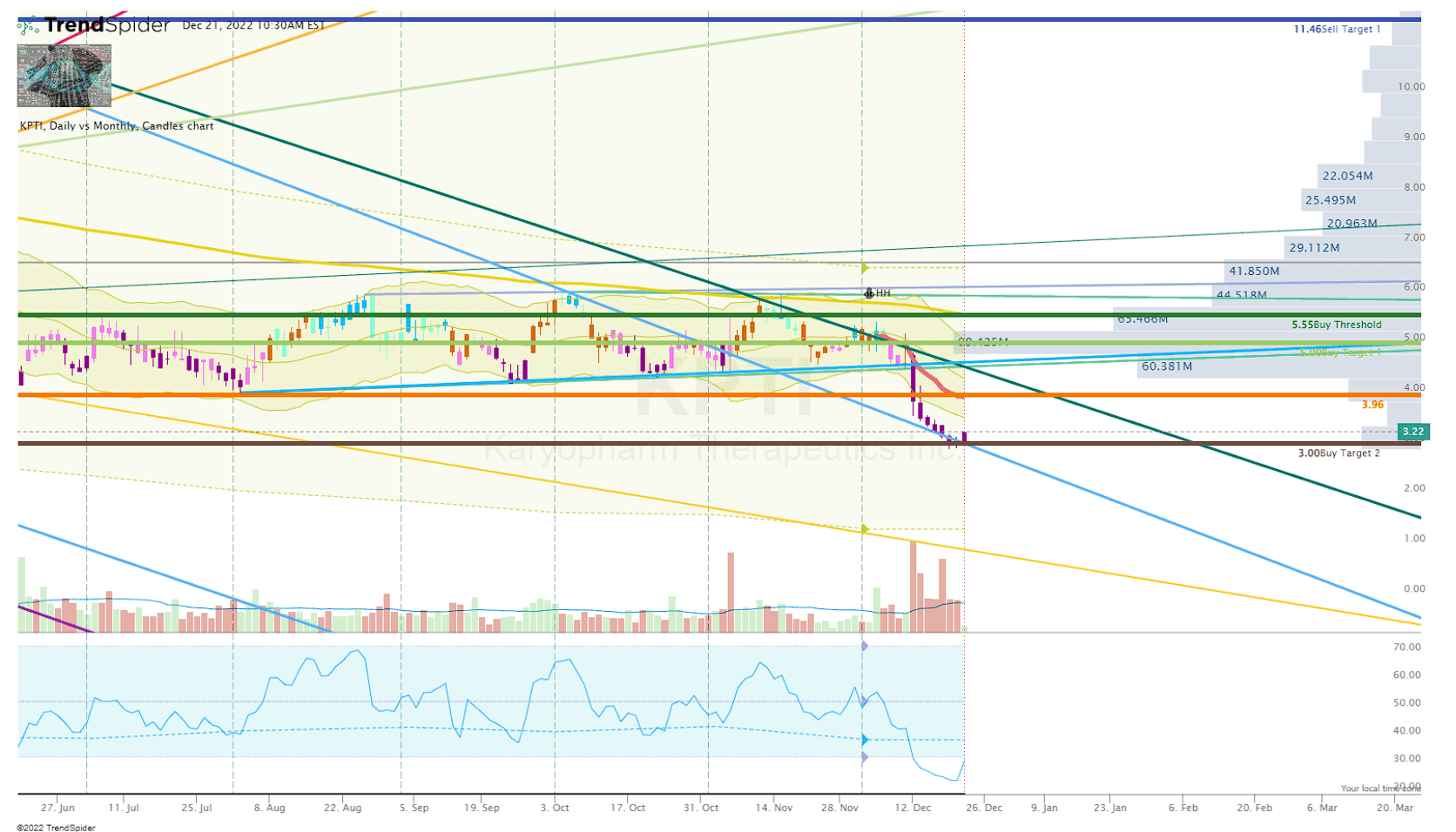

As I mentioned earlier, my KPTI position has been dormant for 2022 as previously set buy orders expired and the overall market has failed to show support for small-cap healthcare tickers. However, KPTI’s recent plummet below my Buy Target 2 has the ticker at the top of my daily watch list as I look for a sign of reversal.

KPTI Daily Chart ( TrendSpider )

{kind=link}

Once I see a solid reversal setup, I will click the buy button and will continue to do so until the share price rises above my Buy Target 1. I will also immediately set equal sell orders at my Sell Targets, with the purpose of transitioning the position back into a "House Money" state.

Long-term, I am dedicated to maintaining a decent position in KPTI with the expectation the company will make the most of XPOVIO and/or be acquired at a premium valuation.

For further details see:

Karyopharm: Recent Sell-Off Hits A New Buy Target