KPTI - Karyopharm Therapeutics: Expanding Beyond The Crowded Multiple Myeloma Market

2023-03-20 04:43:40 ET

Summary

- Shares are down 50% over the past year as fierce competition in the multiple myeloma space negatively impacts Xpovio's growth prospects.

- However, there is significant optionality via expansion opportunities into new indications, starting with relapsed/refractory MDS readout in the near term.

- Myelofibrosis is coming back into focus with a data update due in April (presentation at AACR) followed by phase 3 initiation.

- Bear thesis is that selinexor's tolerability issues (including nausea) will limit its uptake and ultimate potential versus other novel MOAs.

- KPTI stock is a Buy. I see a pathway to value creation via MDS readout, updated MF combo data midyear, and pivotal endometrial cancer results in 2024.

*This article was originally published for ROTY Biotech Community subscribers on December 15th but has been updated where necessary.

Shares of Karyopharm Therapeutics ( KPTI ) have lost 80% of their value over the past 3 years and sport a 50% loss in the past twelve months.

Back in February, they spiked above $12 on speculation of potential buyout as well as in anticipation of pivotal phase 3 results in endometrial cancer (key expansion opportunity for lead drug selinexor). While data was positive (50% improvement in PFS and 30% reduction in risk of disease progression or death versus placebo), it was insufficient to go to the FDA with. Additionally, the outstanding benefit in patients with wild-type p53 endometrial cancer (13.7 month PFS versus 3.7 months for placebo) was based on subgroup analysis and thus the company needed to run yet another trial in that specific population to move forward.

One key devil's advocate point here has consistently been that selinexor, a selective inhibitor of nuclear export, has shown decent activity but never been able to achieve its true potential due to narrow therapeutic window (such adverse events as nausea negatively impacting its uptake).

A review of recent presentations and data coupled with Q4 capital raise (dilution overhang removed or at least postponed) convinced me to regain exposure here ahead of data for key expansion opportunities, including myelofibrosis ((MF)) and myelodysplastic syndrome ((MDS)).

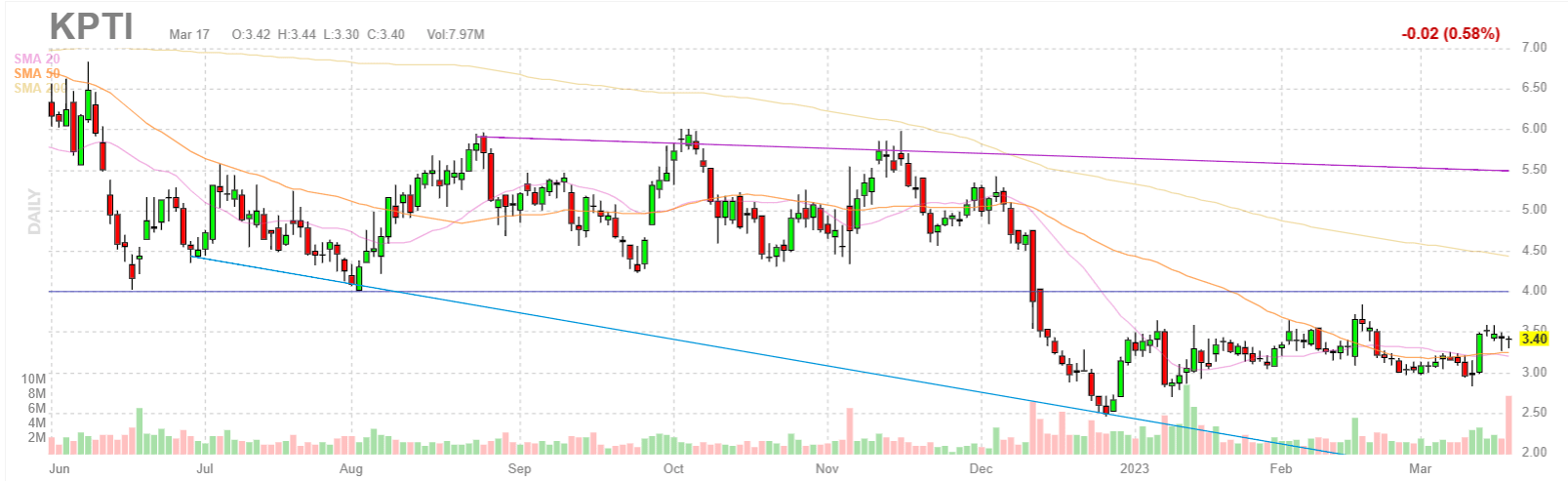

Chart

{kind=link}

Figure 1: KPTI daily chart

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the daily chart above, we can see shares trade as high as $8 back in April. From there, they declined and bounced around in the $4 to $6 range for the past couple quarters. At the beginning of December the company was able to raise much-needed capital in a secondary offering at $5.19/share, but post ASH presentations the selloff continued to the $3.50 level. My initial impression for readers is that the current range is an ideal spot for making a pilot purchase, from there awaiting confirmation from news flow (including upcoming MDS data and quarterly sales numbers) before adding more exposure.

Overview

Founded in 2008 with headquarters in Massachusetts (70+ employees), Karyopharm Therapeutics currently sports enterprise value of ~$270M and current cash position of ~$279M providing them operational runway for 1.5 years. There were ~75M shares of common stock outstanding at Q3 but tack on to that the Q4 financing consisting of ~31.8M share of common stock along with warrants to purchase ~9.5M shares of common stock. It's important to also take into account the $169M worth of convertible debt.

One potential green flag, although they are underwater after the ASH selloff, is that key existing and new shareholders participated in December's private placement (led by Avidity Partners with others involved including Adage Capital Partners, Armistice Capital and Healthcor Management, among others).

At November's presentation during Piper Sandler Healthcare Conference, CEO notes that the company was founded over a decade ago on the research and promise of selective inhibition of nuclear export as a mechanism of action to fight cancer. Now, Karyopharm is at commercial-stage with selinexor (Xpovio) approved in over 40 countries to treat multiple myeloma and DLCBL with 2022 revenue guidance of $155M - $165M. Pipeline is focused on moving into endometrial cancer, MF and MDS (the latter via second compound eltanexor).

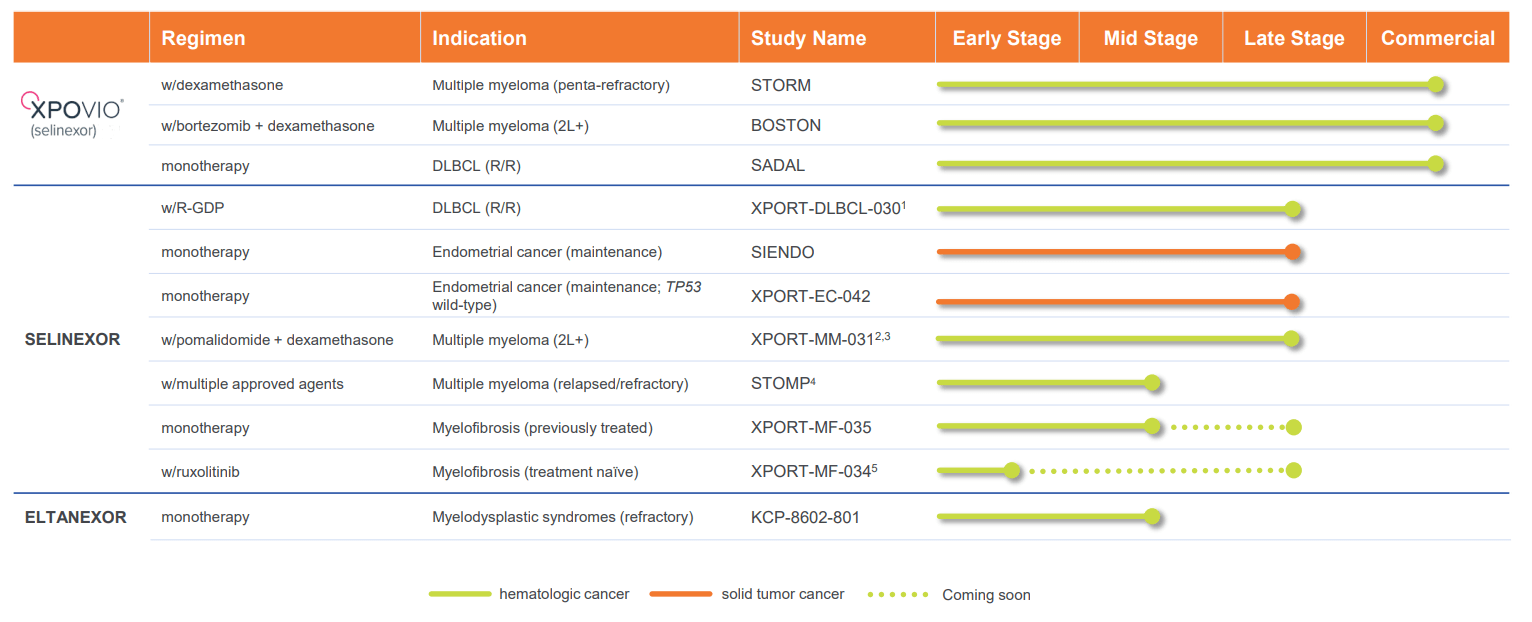

{kind=link}

Figure 2: Pipeline

Inhibition of nuclear export is foundational across tumor suppressor proteins, in oncogenes and corticoid receptors all leading to cell death. Karyopharm is the global leader in this MOA and is moving into 4 core areas (MM, endometrial cancer maintenance setting, MF and MDS).

Q3 results showed $32M revenue (20% year over year growth) driven by growth of Xpovio in the community setting in earlier 2L to 4L (were fastest growing agent in 3rd line 1H 22). Global launches are moving forward, with EU approval earlier this year and partner Menarini launched recently in Germany and Austria.

They've initiated registration-enabling phase 3 study in TP-53 wild-type advanced or recurrent endometrial cancer using Foundational Medicines tissue-based sequencing to identify patients whose tumors are TP-53 wild-type.

Looking first at commercial-stage area, in MM they are focused on 2nd to 4th line setting (building on IMiD, PIs and anti-CD38's). Patients benefit significantly from having multiple MOAs to manage their multiple myeloma. They are building on that with XpD trial combining with Pomalyst and continuing to expand their presence in MM.

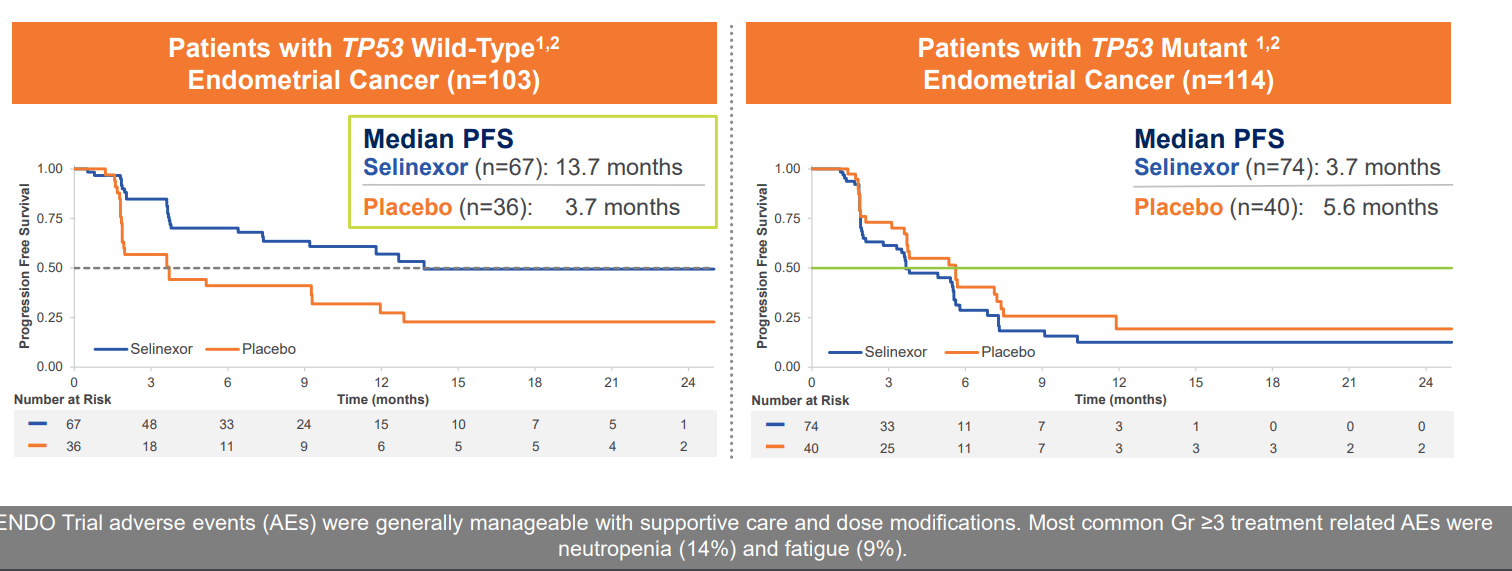

Moving on to the pipeline, for endometrial cancer this is the most common gynecologic cancer afflicting women. It's a significant unmet need especially in advanced or recurrent stage of disease. Treatment regimens are quite sparse for this population, treated with platinum doublet for limited duration and from there NCCN recommends watch and wait approach. When these patients progress, survival is very poor. First, they conducted SIENDO study in the maintenance setting in patients that completed platinum therapy and were in response. They identified a very robust subgroup analysis in TP53-wild type, accounting for 50% of these patients. As seen below, median PFS was 13.7 months for selinexor-treated patients comparing very favorably to 3.7 months for placebo.

{kind=link}

Figure 3: Supportive data from SIENDO study in TP53 wild-type population

These data highlight the importance of this biomarker and its ability to identify patients that best respond to selinexor. Based on these data, another trial was initiated enrolling only TP-53 wild-type patients.

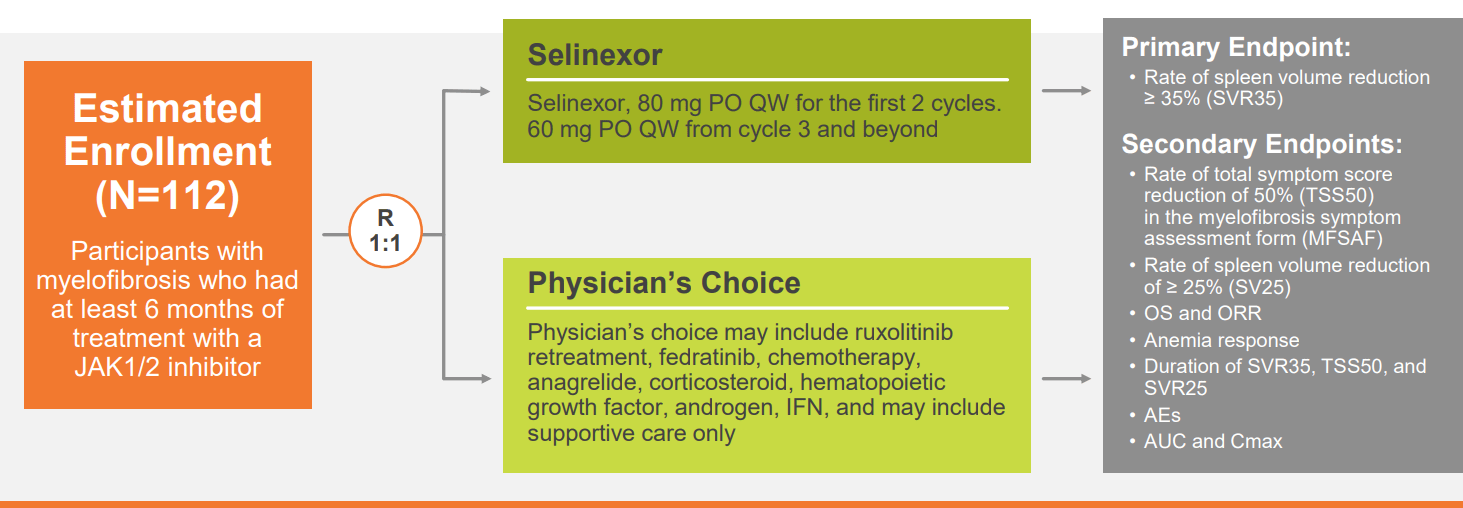

Moving on to myelofibrosis, the only standard of care available to these patients are the JAK inhibitors. Ruxolitinib is standard of care and 40% of patients respond, but once they stop responding prognosis and median survival is very poor (14 months). There has been no other approved class of drugs in the past 10 years here. Selinexor can inhibit multiple aspects of JAK pathway upstream and downstream of JAK inhibitors and potentially can be additive if not synergistic in its effect. Clinical proof-of-concept ESSENTIAL single arm, phase 2 study in pretreated patient population showed SVR35 rate at week 24 at 30% and beyond climbed to 40%. Available therapies for this population can achieve 15%, roughly half that. 035 study is ongoing (all patients previously exposed to JAK inhibitors) and sports randomized design comparing selinexor monotherapy to physician's choice therapy.

{kind=link}

Figure 4: Phase 2 trial design in MF

112 patients are being enrolled with primary endpoint of efficacy as well as safety endpoints.

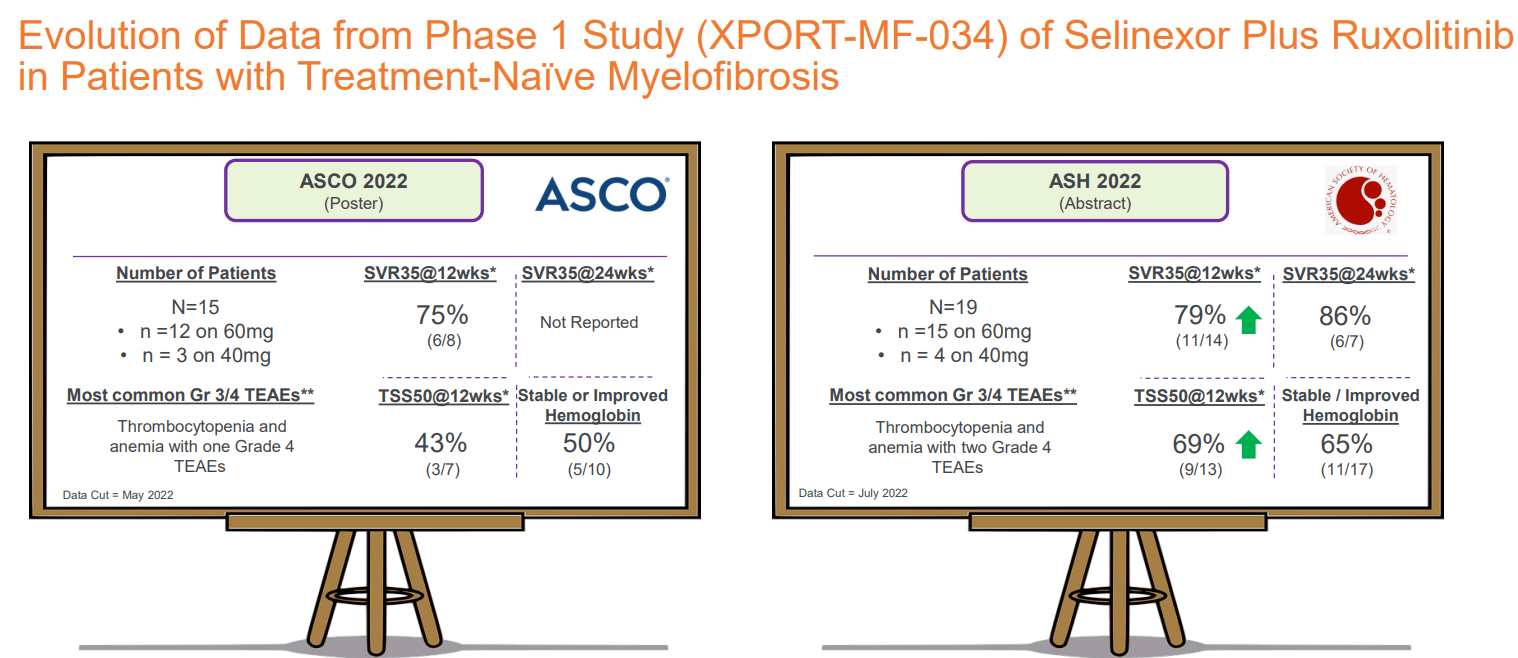

Ongoing 034 trial in naive population is comparing selinexor plus ruxolitinib in patients that have never been treated with systemic therapy. ASH data was from phase 1 portion of this trial (24 patients), with prior abstract data showing encouraging SVR35 rate and TSS50 scores. SVR35 rate at weeks 12 and 24 included 79% and 80%, and TSS50 score at 69% as early as week 12 along with promising impact on hemoglobin levels (65% of patients maintaining or improving compared to baseline). Safety profile was tolerable, though certainly it's worth exploring lowest doses to improve further if possible.

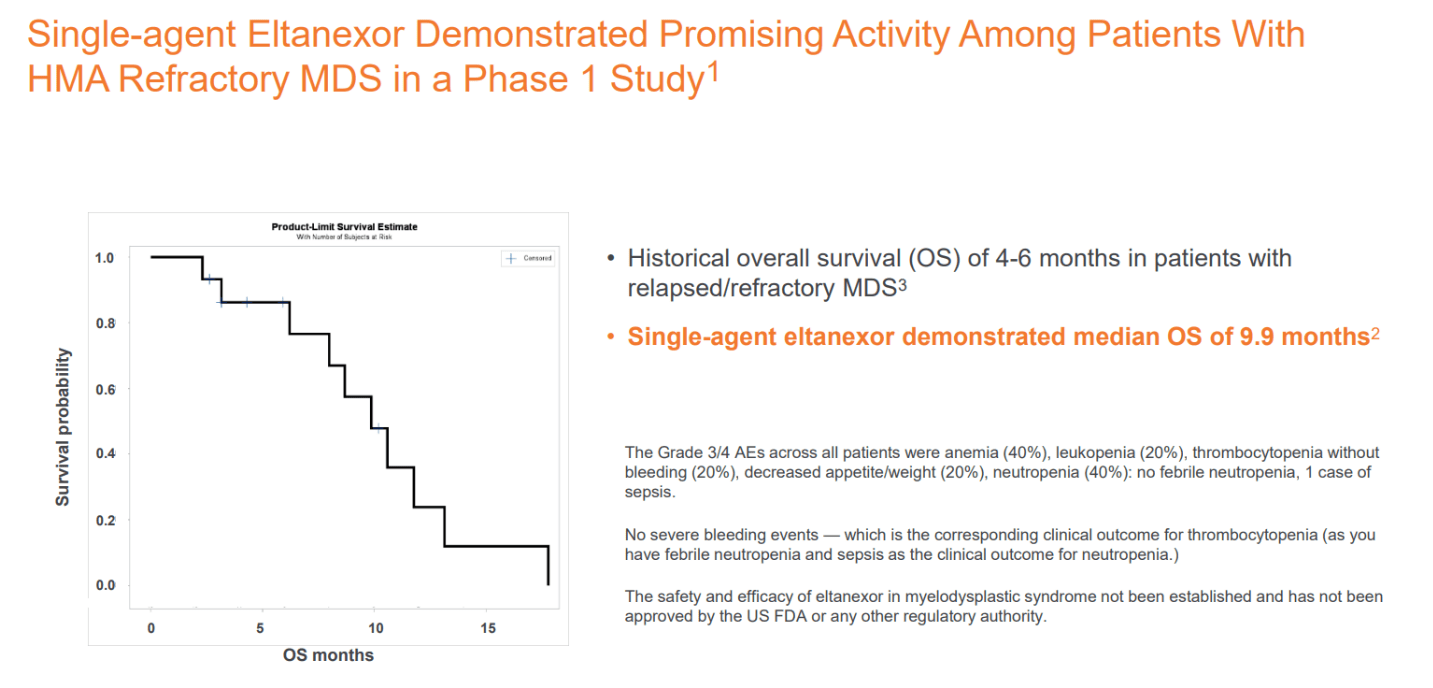

Lastly, for Gen2 compound eltanexor, it is being developed in MDS. This condition leads to cytopenias including anemia, neutropenia and thrombocytopenia. Relapsed/refractory population has very poor prognosis with median overall survival of 4 to 6 months. Initial phase 1 data in this population achieved OS rate of 53% and median OS of 10 months. Phase 2 study is ongoing (monotherapy) and enrollment is completed as part of pre-planned interim analysis with OS data expected later this year or early 2023.

On February 21st, the company announced UK full approval for Nexpovio (converted from accelerated approval) in combination with bortezomib and low-dose dexamethasone in multiple myeloma patients who have received at least one prior therapy. Partner for that area is Menarini.

On March 14th the company announced that phase 1 results from the combo of once-weekly selinexor with standard dose ruxolitinib in patients with treatment-naive myelofibrosis have been selected for poster presentation at AACR. Investor webcast is being held to discuss updated results on April 18th.

Other Information

For Q4 the company reported $279M of cash as compared to net loss of $38.5M (around 1.5 years of operational runway). Looking at the full year 2022, SG&A came in about flat at $145.4M while research & development expenses fell slightly to $148.7M.

Q4 net product revenue rose just 4% to $31.1M versus Q4 2021, while for the full year $120.4M represented a 22% increase versus the prior year.

As for 2023 outlook, the company is guiding for $160M-$175M of total revenue including $125M-$140M of US Xpovio net product revenue. Non-GAAP R&D and SG&A expenses should fall in the range of $260M-$280M, with management guiding for operational runway into late 2025.

As for near term catalysts, key ones to look forward to include phase 2 readout of eltanexor in relapsed/refractory myelodysplastic syndromes (1H 23) and updated data from phase 2 study of selinexor ruxolitinib combination in treatment-naive MF (1H 2023) to be followed by initiation of phase 3 front-line MF study. The company also plans to present updated subgroup analysis results in patients with TP53 wild-type endometrial cancer from the SIENDO study of selinexor versus placebo as maintenance therapy after first-line chemo for advanced or recurrent endometrial cancer at a medical conference this year. Lastly, the company will explore additional biomarker subsets to identify patient populations who could best respond to SINE compounds (this one adds significant optionality to thesis, in my opinion).

Moving on to the conference call , here are a few nuggets worth highlighting (see slides as well ):

- For high-risk r/r MDS, they look forward to seeing OS data mature in phase 2 study (glad they mentioned, as I recall prior calls where this indication was not touched on).

- Community setting contributed to 70% of Q4 sales for Xpovio. They achieved 28% sales growth in the community for 2022 versus prior year. For academic setting (heavy competition with CAR-T), they grew sales by just 7% in 2022. Growth drivers include shifting into earlier lines of therapy and increasing duration of therapy. Perception of the product continues to improve.

- Proportion of patients in earlier lines has grown with 55% of patients treated in 2nd to 4th line (driven by 3rd line setting). 2023 projected growth is just 10% which management calls solid in a competitive landscape expected to intensify with 4 new competitor approvals coming.

- In 2023 they will generate data pre and post T-cell mediated therapies to strengthen position in 2L to 4L. All oral phase 3 study in combination with pom & dex for targeting community setting could be key driver as well (if approved).

- Eltanexor has lower blood brain barrier penetration and IC50 (measure of potency) is lower, enabling more continuous dosing. Animal models show continuous XPO1 inhibition results in greater potency.

- Lower doses of selinexor can be utilized to optimize tolerability profile, allow patients to be on therapy longer and improve overall benefit. All ongoing studies incorporate doses at 40mg or 60mg once-weekly (1/4th to less than 1/2 of initially improved dose of 160mg).

- Moving on to endometrial cancer, treatment landscape for advanced disease is first line chemo followed by "watch & wait" approach until disease progression. 5-year survival rate in this population is just 17%. Selinexor has the potential to offer a maintenance option in TP53 wild-type (50% of patients). Subgroup data from SIENDO study showed these patients demonstrated median PFS of 13.7 months compared to 3.7 months for patients treated with placebo. Updated PFS results with December 2022 cutoff shows median PFS has increased to 20.8 months compared to 5.2 months for placebo with no observed change in safety profile. Pivotal study is ongoing with topline results expected 2H 2024 (paradigm shift for this population if positive).

- For eltanexor in MDS, prognosis in HMA-refractory disease is poor with median OS of 4 to 6 months (no approved therapies). Eltanexor achieved median OS of 10 months in phase 1. Interim phase 2 analysis (efficacy and safety) is expected 1H 2023 followed by topline results in 2024.

- On Q&A, timing for MDS interim analysis is dependent on overall survival data. Identify robust OS signal allows them to identify best path forward. They are still following OS data and looks like it will occur first half of the year. They will be opportunistic on how they present the data (company event or major medical meeting).

- For MF, they are following all 24 patients for maturity across all key efficacy endpoints (TSS, hemoglobin, SVR, etc). Recommended phase 2 dose will be about efficacy at week 24, safety profile and pharmacodynamic data.

- Management highly encouraged by ASH 2022 phase 1 MDS data for eltanexor. Phase 2 data will allow them to best determine registration path in this population (again, may not seem like much but glad they are mentioning this indication more than in the past).

- Overall survival for SIENDO data in endometrial cancer is still immature.

As noted prior, early phase 1 data for selinexor combination with SoC ruxolitinib in treatment-naive myelofibrosis patients was quite promising with 79% and 86% achieving ?35% reduction in spleen volume (SVR 35) at week 12 and at week 24, respectively. 69% of efficacy-evaluable patients experienced ?50% reduction (TSS50) at week 12 and 65% of transfusion-independent patients who had at least 8 weeks of treatment maintained stable hemoglobin (± 2g/dL) or improved hemoglobin level (>2g/dL increase) at last follow up. Importantly, AE profile was generally manageable with no dose limiting toxicities- as would be expected for selinexor, rate of nausea was high at 58% in addition to anemia (42%) and vomiting (42%). However, majority of events were Grades 1 to 2.

Analyst questions seem to focus on the myelofibrosis opportunity, noting that TSS (symptoms) scores improved since the last data cut. At ASCO in June 43% of patients achieved TSS50, while the next update showed that increased to 69%. One of the key differentiators for selinexor versus competitor treatments is its robust monotherapy activity in the relapsed refractory population (preclinical data shows selinexor is active in JAK resistant cells).

{kind=link}

Figure 6: SVR35 and TSS50 measures improving over time in addition to # of patients with stable/improved hemoglobin

As for eltanexor's opportunity in myelodysplastic syndromes ((MDS)), they completed enrollment of the phase 2 study in relapsed refractory population and are waiting for interim analysis (looking at overall survival) with data to be presented later this year or more likely early in 2023. Also, they stopped enrollment in phase 1 combination trial in treatment-naive MDS so they can reevaluate the combination regimen.

{kind=link}

Figure 7: OS from phase 1 in MDS significantly better than available therapies for these relapsed/refractory patients

As noted above, initial monotherapy median OS of nearly 10 months bodes very well for this HMA-refractory population where the norm is just 4 to 6 months. I would think the upcoming interim data has a good shot at being positive, but the key unknown (and risk factor) here is any safety issues/adverse events of note that show up as well as making the jump from low number of patients to higher N (from 15 to 83).

A review of last year's webcast on MF provides us with a few useful nuggets:

- There is an emphasis on spleen reduction because it is correlated with survival benefit. The goal is to intervene early, as the better the spleen response the longer the survival. Long-term treatment with ruxolitinib accomplishes this, but there is still much room to improve (especially in terms of durability). As observed below, average duration on ruxolitinib is 3 years. Black one is for patients with low platelet counts (very bad). This is no longer due to underdosing as a result of adverse events (anemia, thrombocytopenia).

{kind=link}

- From community standpoint, average duration of ruxolitinib therapy is 1 year to 1.5 years in the US (not 3 years, studies are always better than community practice).

- Once you stop ruxolitinib, the story goes down and it's devastating for patients (average survival from there is 14 months). So the goal is to improve experience on ruxolitinib or develop an agent to be utilized after ruxolitinib with a new mechanism of action (we need something different other than another JAK inhibitor after a JAK inhibitor).

- There are several drugs already in phase 3 studies for possible approval with different modes of action for different populations of patients, combinations for first line as well as 2nd line or patients with suboptimal response (see below).

{kind=link}

-

In the data summary, management notes that data builds on the selinexor's single agent activity demonstrated in the ESSENTIAL study in JAKi exposed MF and suggests the drug candidate could be utilized in both treatment naive and JAKi exposed populations.

- Moving on to Q&A, analyst asks for competitive landscape versus other ruxolitinib combination treatments as well as tolerability profile & how it compares. Efficacy is tied to safety and simplicity (drug given once a week) and tolerability can be improved on but is quite good already, per investigator. I nvestigator notes that efficacy is higher than any other treatment, very simple unlike any other treatment and acceptable tolerability which is quite compelling for further development. They need to wait for complete 24 weeks of data to select go forward dose.

- As for dose modifications or discontinuations so far, they haven't provided these rates yet as waiting for data to mature. They are very encouraged by dose intensity they are seeing (82%, 83% for selinexor and ruxolitinib) which suggests that planned doses investigator had indicated for patients by and large are getting administered to patients (not seeing many dose reductions or modifications). This is a relatively easy and simple combination.

- Nausea & vomiting symptoms typically occur on day 1 when patient receives treatment, gets other drugs to help and usually the regimen is very tolerable (symptoms improve) after 2 cycles. Their experience in multiple myeloma on the market reflects this as well (BOSTON study showed nausea experienced early on with substantial improvement by end of cycle 1 and almost 92% of patients resolve their nausea by end of cycle 2). In this study they only required one anti-mimetic and going forward will require 2 to further improve the nausea.

- They are looking for more maturity at 40mg (lower dose) next year to determine go forward dose (better AE profile). Degree of anemia they saw is less pronounced than with ruxolitinib alone and there is NO contribution of myelosuppression to management of ruxolitinib alone (which is a common problem, compromising simplicity and tolerability of potential combinations).

- As for pathway to approval, this is pending discussion with FDA on both monotherapy as well as combination (looking for both).

As for possible points of comparison on valuation, one could argue that the recent buyout of Imago BioSciences ( IMGO ) for 100%+ premium by Merck ($1.35B) also has positive readthrough to Karyopharm, given that Imago's lead drug bomedemstat was in phase 2 studies including for the myelofibrosis indication. Imago's slides highlight similar unmet need here for sustained improvement in QoL and outcomes such as survival (also that 40% of patients discontinue JAK inhibitors after 3 years). However, it's interesting that change in spleen size is placed behind other measures and focuses on change in total spleen volume (versus the more accepted SVR35 measure, which KPTI's 30%+ greatly exceeds mid-single digits for bomedemstat).

Another point of comparison is versus Sierra Oncology, bought out by GSK for $1.9B earlier this year. Per press release , momoletinib achieved (in patients previously treated with JAK) SRR >35% of 23% (versus 40% for selinexor in phase 2 ESSENTIAL study, caveat for low N and cross trial comparisons).

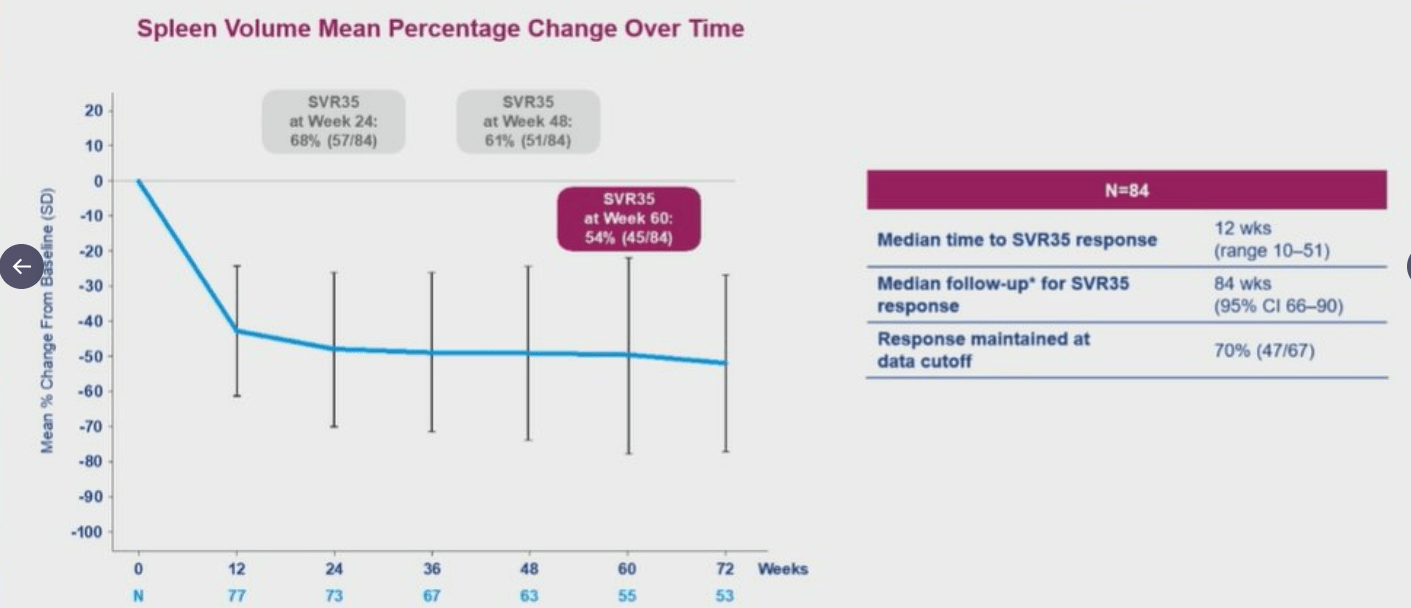

One last point of comparison that comes to mind is Constellation Pharmaceuticals, bought out by MorphoSys for $1.7B for its BET inhibitor pelabresib. Here, Jakafi combo data showed 53% of patients (1st line) achieve SVR35 and 59% of patients achieve reduction in TSS (Total Symptom Score) >50%. Selinexor's phase 1 ruxolitinib combo data looks arguable better to my eyes, again caveat for low N and cross trial comparisons. Updated data for pelabresib combination at ASH 2022 looked quite promising, with 83% of patients achieving TSS50 at any point in time with 54% SVR35 at Week 60 and 70% of patients still in response at data cutoff.

{kind=link}

Figure 10: MANIFEST 3 spleen volume response over time for pelabresib ruxolitinib combo

Durability of effect for selinexor, including at lower doses, remains a key unknown and risk factor in that respect (more clarification with data update next year).

It's also worth mentioning AbbVie's navitoclax, which achieved 63% SVR35 rate for its ruxolitinib combination and just 9% of patients discontinuing therapy due to adverse events.

Moving on to competition in endometrial cancer, I note that lenvatinib pembrolizumab combo achieved PFS of 6.6 to 7.2 months vs 3.8 months for physician choice (also keeping in mind that side effect profile for lenvatinib is quite harsh). Looking at clinical trials website, I see that AstraZeneca's durvalumab is being evaluated in maintenance setting (with or without PARP inhibitor olaparib) in this 700 patient phase 3 study with primary completion date of September 2023. Evaluate article noted earlier this year that other PD-1s (Jemperli, Keytruda, etc) are also being evaluated in late-stage studies.

Here are a few new or incremental nuggets from Barclay's presentation:

- CEO has been with the company for 2 years now (was on the board for a year prior). Novel MOA for multiple areas of cancer excited him enough to join at the helm. Chief Medical Officer has been at the company for 11 months, joined due to the science and intrigued by the mechanism (develop SINE compounds in additional tumor types).

- 70% of multiple myeloma business is in the community, 30% in institutions and academics. The space continues to get more competitive with T-cell therapies and bispecifics being approved. Goal now is to use selinexor ahead of these T-cell therapies in 2L to 4L in community (multiple other agents in MM have a negative impact on T-cell environment and efficacy patients achieve with those immunotherapies). Selinexor can maintain and potentially even improve that T-cell environment. Growth in 2023 should come from 2L to 4L post anti-CD38 and pre CAR-T. 3rd line has been the greatest source of growth (community) and they will continue to grow breadth of prescribers. They will continue using lower dose and anti-mimetics for first couple months to drive depth (key accounts becoming more comfortable with selinexor, able to mitigate the nausea). Many patients are not eligible with T-cell therapies (older patients, or those in more rural areas). Earlier lines of therapy have greater duration (patients on triplet have been on selinexor for over a couple years).

- First-line MF update for selinexor ruxolitinib combination will include 24-week data for all 24 patients. Data to date has been "extremely encouraging", as efficacy has remained stable (not seeing erosion). SVR35 and TSS50 data suggests the combination substantially improves benefit and suggests they can develop the combo in treatment-naive population. Phase 3 trial will be initiated 1H 2023 (data expected in 2 years).

- As for how treatment landscape changes with BET inhibitors, they anticipate 1st line space becoming more competitive. However, the question is which combo drives the most meaningful efficacy and they believe selinexor "really checks that box". Competitively speaking, they are not worried because regardless of what competitors are doing, the only standard of care right now for 1L is ruxolitinib. Not all patients benefit equally, more patients need to start on low dose of ruxolitinib due to low platelet counts and see lower efficacy here. KPTI aims to show equal efficacy across ALL patients.

- For eltanexor in MDS, phase 2 data is due in the near term. Unlike selinexor, it crosses the blood brain barrier at a lower rate (lower rates of non-heme toxicity such as nausea and fatigue). Lower IC50 allows the drug to be dosed more frequently (5 days on, 2 off) and more continuous inhibition of XPO1 drives greater antitumor activity. Patient population in phase 2 is very similar to phase 1 (poor prognosis, median expected OS of 4 to 6 months). Efficacy data from phase 1 was very encouraging (OS of almost double historical norms). These are primary refractory patients (sickest and poorest prognosis). Data will be for 30 patients and focus will be on overall survival and ORR. Within MDS landscape, definition of ORR is rapidly evolving with no true consensus (thus focus is on maturity of overall survival data so they can compare it to historical controls ).

- For endometrial cancer (TP53 wild type) phase 3 trial, there is a lot of excitement with most recent data cut (SIENDO PFS increased from 13.7 months to 21 months). They have also identified a very important biomarker, a tool for physicians to identify the best therapy for this patient population.

As for institutional investors of note , Avidity Partners Management owns 9.9% of the company and participated in the recent financing. For insiders, CEO Richard Paulson owns ~600,000 shares with a stream of small sales throughout 2022.

As for relevant leadership experience, CEO Richard Paulson served prior as CEO for Ipsen North America and prior to that as VP & GM of Amgen's US Oncology Business. His experience is a green flag in my book and I note he joined Karyopharm in 2021. Chief Business Officer Stephen Mitchener joined in December 2020 and served prior at Novartis as Head of Strategy (responsible for US oncology). Chief Development Officer Stuart Poulton joined in February this year and served prior as VP Clinical Development at Amgen. Lastly, Chief Medical Officer Reshma Rangwala served prior as VP Medical at Genmab and Executive Clinical Director at Merck.

Moving onto useful nuggets from members of the ROTY community, TDMInvest noted the following at the beginning of November in Chat:

KPTI still spending a lot on SG&A, losing a bunch of money ($36M), and getting low on cash ($148M, down from $228M just 90-days ago). Until they show the world that they are trying to run a real profit-generating business, it's hard to imagine that they'll go up much.

Obviously application expansions and pipeline development successes could tilt the scale in an improved direction, but economically, they're not looking great. When you incur over $1.00 of sales expense for every dollar of sales, it's pretty hard to make money.

Moving on to IP, the company is sole owner of 32 US patents and has 16 pending applications in the US along with 98 granted foreign patents plus 99 pending applications in foreign jurisdictions. For selinexor, issued patents have expiration dates between 2032 and 2035 (pending patents could extent up to 2041).

I would be remiss to note that selinexor is the subject of many investigator-initiated or investigator-sponsored studies where Karyopharm just supplies drug for these trials to explore additional shots on goal. I count over 40 such studies currently recruiting patients. Venetoclax combo study in high-risk heme malignancies should read out in late 2023, while venetoclax combo trial in pediatric AML has primary completion date of June 2023. I highlight these because of ASH publications ( including from last year ) hint at potential synergies including effects on pro-apoptotic proteins.

Final Thoughts

To conclude, with enterprise value of $270M, I continue to think Karyopharm Therapeutics is significantly undervalued here and recent progress across balance sheet, sales growth and pipeline is not being appreciated. As for what could change sentiment in 2023, I look forward to near term monotherapy MDS data and April's MF combo update (including on durability).

For the former, I note that in Q2 and Q3 quarterly presentations management rarely touched on eltanexor's prospects in MDS, but that changed in Q4 where it was highlighted several times. As this is an event-driven readout, my thought is that it's a net positive the longer it takes for survival data to come out (patients lasting longer on therapy). Again, that's just speculation on my part and should be taken with a grain of skepticism.

For readers who are interested in the story and have done their due diligence, KPTI is a Buy and I suggest initiating a pilot position (half of desired exposure level) in the current range. From there, I suggest prudently waiting for MDS data in the near term before considering further action.

Taking a long term perspective (3 to 5 years), value creation should take place as selinexor's commercial potential expands to additional indications such as MF, MDS and endometrial cancer. I think there's multiple other opportunities where nuclear export inhibition is likely to be tried out, including via investigator sponsored studies (company sponsored trials to follow ONLY where data merits).

Key risks include disappointing clinical data that would in term hamper expansion efforts, as I do NOT consider multiple myeloma alone to be worth investing in the company (novel CAR-T therapies and bispecifics will win this war as they move into frontline setting). I also highlighted growing competition in MF and endometrial cancer indications, among others. If the MDS readout is negative, eltanexor program would likely be discontinued. The company continues to burn a lot of cash and I wouldn't be surprised to see further dilution by Q4.

For further details see:

Karyopharm Therapeutics: Expanding Beyond The Crowded Multiple Myeloma Market