KPTI - Karyopharm Therapeutics: Promising Potential With 3 Ongoing Phase 3 Studies But Risky

2023-11-29 18:48:21 ET

Summary

- Selinexor has received three approvals but has faced disappointing sales due to competition and toxicity. Nevertheless, an already established global commercial infrastructure will support the launch of additional indications.

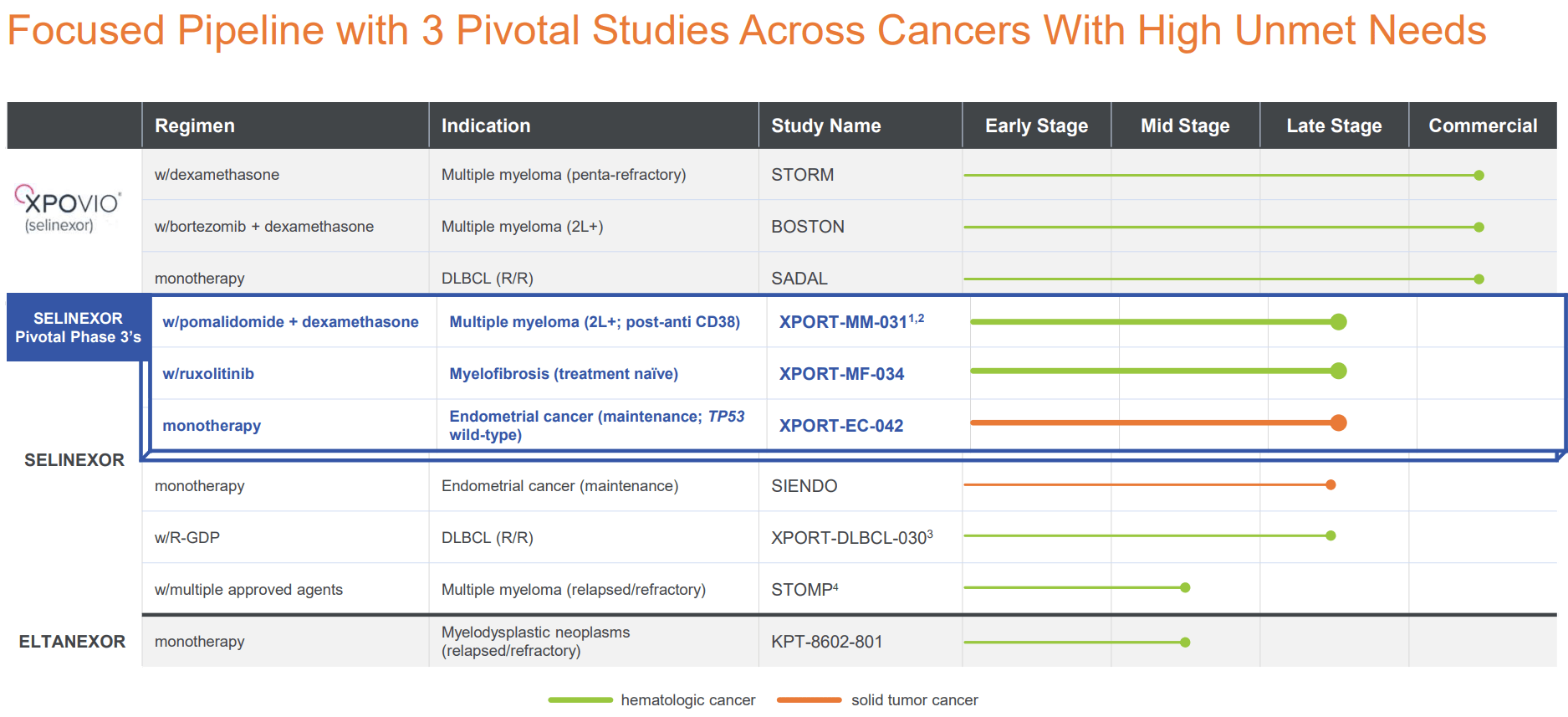

- Selinexor is being evaluated in three phase 3 trials; (1) multiple myeloma, (2) endometrial cancer, (3) myelofibrosis. The probability of success is high based on prior data.

- Topline results are anticipated in 2H 2024, 1H 2025, and 2025, respectively. Each of the above trials, if successful, may add $1-2B in peak annual sales.

- Cash runaway to late 2025 is sufficient to fund operations through the topline results but does not account for liabilities maturing in mid/late 2025. KPTI will also face fierce competition.

Thesis overview

Karyopharm's ( KPTI ) lead candidate is selinexor, which has a novel mechanism of action. It acts as a selective inhibitor of nuclear export by binding to exporting 1 (XPO1). KPTI has been the leader in targeting this pathway and has successfully developed selinexor, with 3 approvals so far; in penta-refractory multiple myeloma, in 2nd-line+ multiple myeloma (2L+ MM) and in relapsed/refractory Diffuse Large B-Cell Lymphoma (r/r DLBCL). However, due to significant competition by numerous approved therapies for the same indications, as well as toxicity, selinexor sales in these indications have been disappointing. Nevertheless, there are reasons to believe that selinexor sales may improve, especially if the ongoing phase 3 trial in 2L+ MM is successful (topline expected 2H 2024). Furthermore, selinexor is being evaluated in 2 ongoing pivotal randomized controlled trials; in advanced/metastatic endometrial cancer (topline expected in H1 2025), and frontline myelofibrosis in combination with ruxolitinib (topline expected in 2025). Based on results from a prior phase 3 in endometrial cancer probability of success seems high. Similarly, phase 1 results in myelofibrosis compare favorably with competitors.

Considering a guided cash runaway to late 2025, i.e. beyond expected catalysts, high-probability of success in ongoing phase 3s and global commercial infrastructure that can support label expansions, KPTI seems undervalued. The main problem is that whoever invests in KPTI now will likely have to be patient for at least 1.5-2 years for KPTI's potential to be realized. In the meantime, unless there are positive surprises (e.g. new partnerships), I don't expect major upside and it is possible that the downtrend will continue. Liabilities by mid/late 2025 are also a concern. For me starting with a small watchlist position seems worth the risk.

{kind=link}

KPTI's pipeline (KPTI's November corporate presentation)

Overview of selinexor's approved indications

Selinexor has the following approved indications;

- Selinexor+dexamethasone for penta-refractory MM (patients who have received at least 4 prior therapies). Approved July 2019.

- Selinexor+bortezomib+dexamethasone for 2L+ MM (patients who have received at least 1 prior therapy). Approved December 2020.

- Selinexor monotherapy for r/r DLBCL after ?2 lines of systemic therapy. Approved in August 2021.

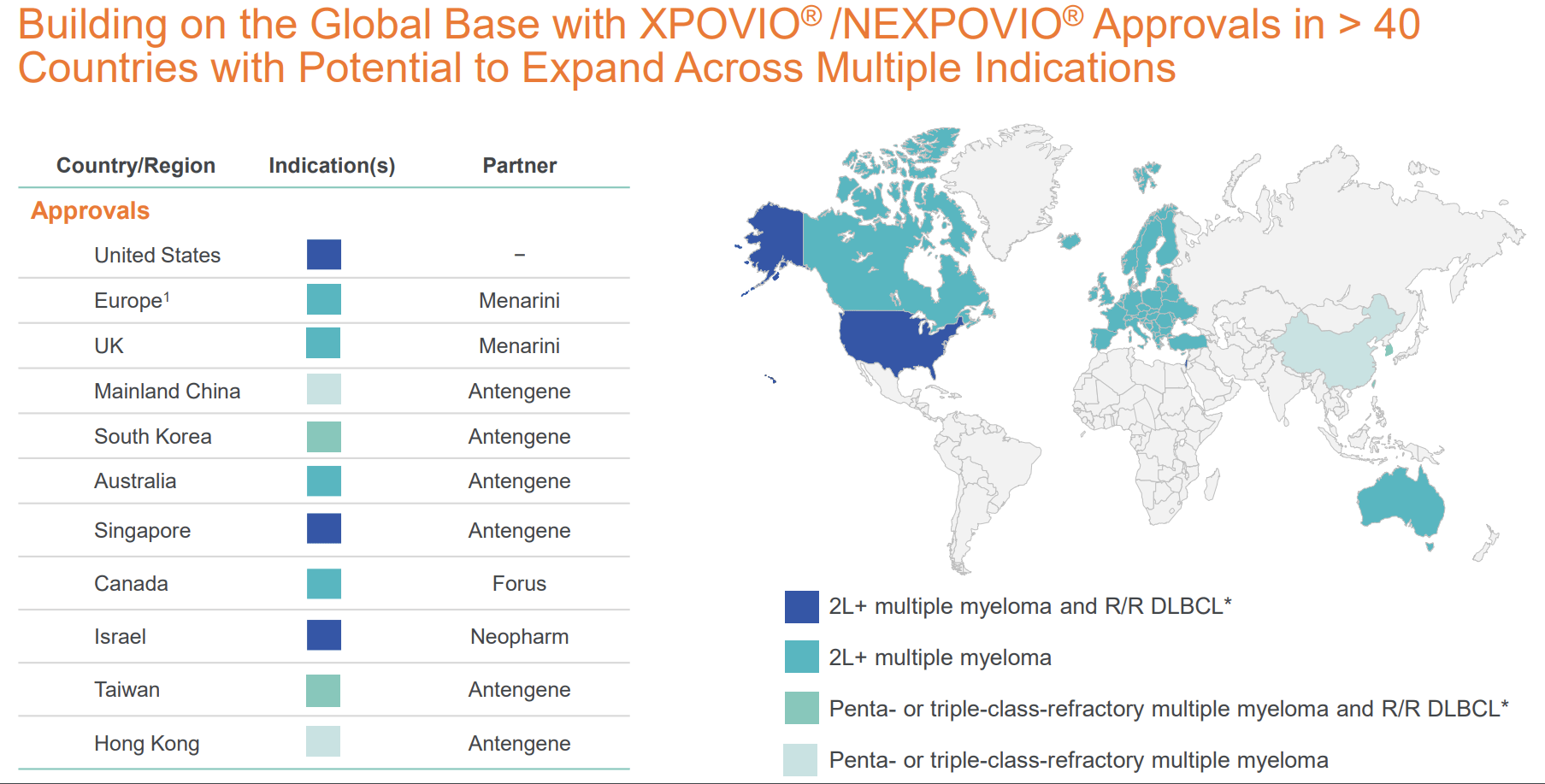

These 3 approvals suggest a successful drug developer who has already established a global presence. However, this does not always translate to a successful commercial product. Despite these 3 approvals, and despite expansion to 2L+ MM since December 2020, revenues are underwhelming and not growing. The 2 main reasons for this, beyond pricing, are; (1) Toxicity, (2) Competition. These issues, as well as reasons why I believe there is still probability for growing revenues, will be discussed below.

{kind=link}

Global presence of KPTI (KPTI November corporate presentation)

Selinexor toxicity

A major limitation of selinexor is toxicity, including cytopenias (mainly thrombocytopenia and neutropenia), neurotoxicity (dizziness, fatigue and confusion being major side effects), hyponatremia, nausea/vomiting and ocular toxicity (e.g. cataract). Notably, "in the clinical trials evaluating selinexor, all patients received antiemetic prophylaxis with a 5-HT3 receptor antagonist. In clinical practice, patients receiving selinexor often require multiple antiemetics, which in addition to a 5-HT3 receptor antagonist may include prochlorperazine or olanzapine".

To some extent toxicity is manageable by supportive measures (antinausea agents, granulocyte colony-stimulating factors, thrombopoietin-receptor agonists, appropriate fluid and caloric intake, appetite stimulants, psychostimulants) or by reducing the dose, but some patients will discontinue treatment due to intolerance. In the STORM study (which used the highest dose); 18% discontinued treatment because of an adverse event, while a dose modification or interruption was necessary in 80% of the patients due to adverse events.

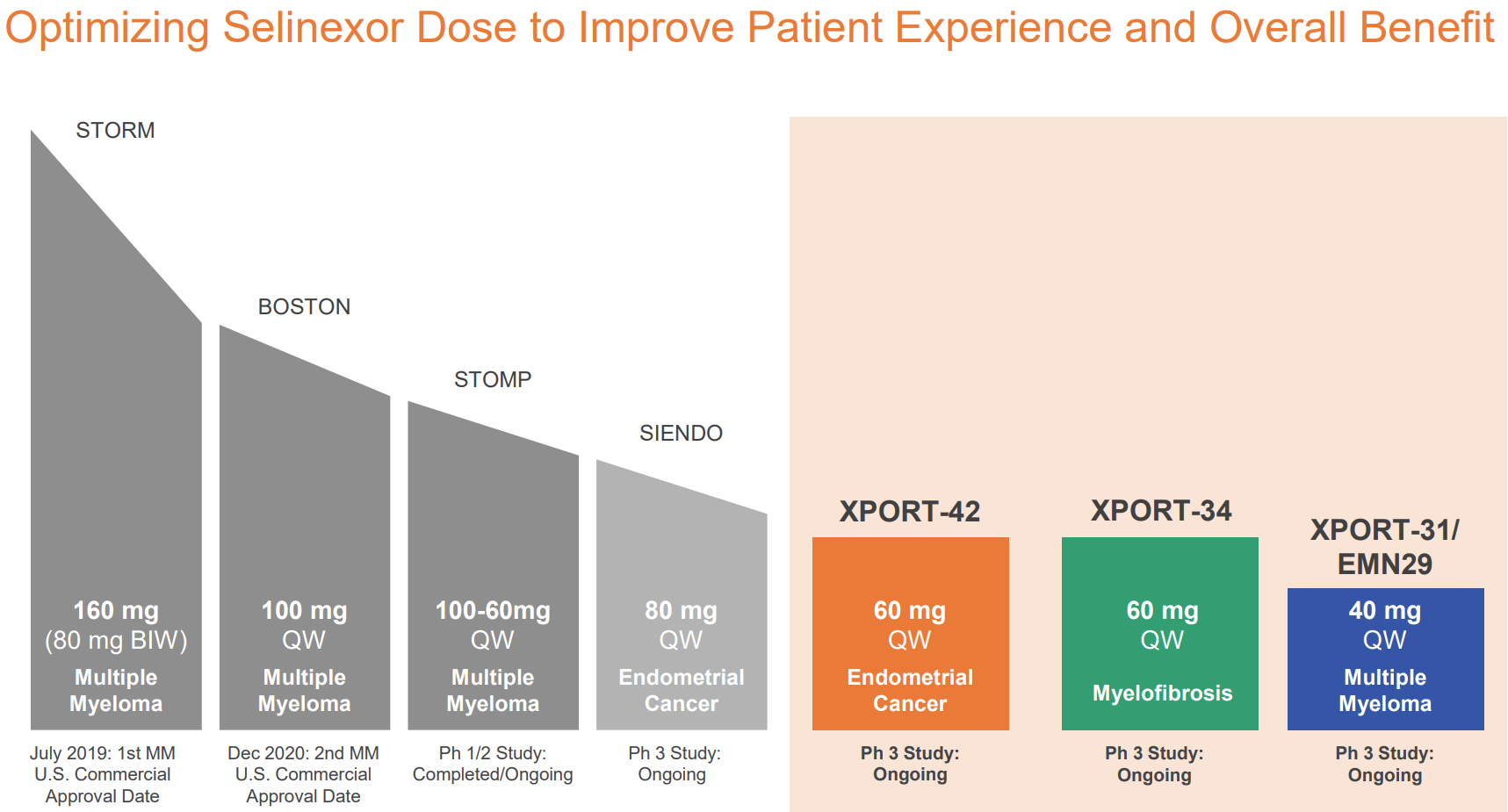

In subsequent trials, lower doses were used. In BOSTON trial (100mg QW vs 80mg BIW) discontinuation rate was 21% (vs 16% in comparator arm) and dose modification was necessary in 89% (vs 76% in comparator arm). In SIENDO trial, using half the dose (80mg QW vs 80mg BIW), discontinuation rate was 15.8%. Doses used in ongoing phase 3s are even lower (40-60mg QW), which may improve tolerability, hopefully without negatively affecting efficacy. Notably, new data from BOSTON trial suggest that appropriate dose reductions in response to adverse events were associated with improved efficacy, reduced adverse events and improved quality of life. Therefore, KPTI's rationale for lower dosing seems strong.

{kind=link}

Lower selinexor dose in ongoing trials may improve tolerability (KPTI November corporate presentation)

Selinexor competition in MM and DLBCL

There are numerous approved treatment combinations for patients with relapsed and/or refractory MM. "Although direct comparisons between these combinations have not been conducted, network meta-analyses that incorporated both direct and indirect comparisons identified monoclonal antibody-containing three-drug combinations among the most active regimens in relapsed MM". Even the ongoing phase 3 study (selinexor w/pomalidomide+dexamethasone) is enrolling patients with post anti-CD38. Therefore, selinexor is not generally considered a first choice for 2L MM patients. Notably, according to UpToDate authors (see suggested treatment algorithms below), selinexor-based combinations seem to be considered a last resort option. Nevertheless, "most patients experience serial relapses over time and will ultimately receive most if not all available agents at some point during their disease course". So those that do survive long enough will eventually get selinexor, but this number is much smaller than the total r/r MM patients.

The same problem applies to r/r DLBCL, where preferable treatment options are CAR-T cells, BiTE antibodies and monoclonal antibodies directed against antigens expressed by DLBCL (e.g., CD19, CD79b).

Selinexor-based combinations are very low in UpToDate's suggested treatment algorithm for 2L+ MM. MM: Multiple myeloma; DRd: Daratumumab, lenalidomide, and dexamethasone; KRd: Carfilzomib, lenalidomide, and dexamethasone; IRd: Ixazomib, lenalidomide, and dexamethasone; ERd: Elotuzumab, lenalidomide, dexamethasone; DKd: Daratumumab, carfilzomib, and dexamethasone; IsaKd: Isatuximab, carfilzomib, and dexamethasone; DPd: Daratumumab, pomalidomide, and dexamethasone; IsaPd: Isatuximab, pomalidomide, and dexamethasone; KPd: Carfilzomib, pomalidomide, and dexamethasone; VPd: Bortezomib, pomalidomide, and dexamethasone; VCd: Bortezomib, cyclophosphamide, and dexamethasone; SVd: Selinexor, bortezomib, and dexamethasone; DVd: Daratumumab, bortezomib, dexamethasone (UpToDate)

Selinexor market potential in MM

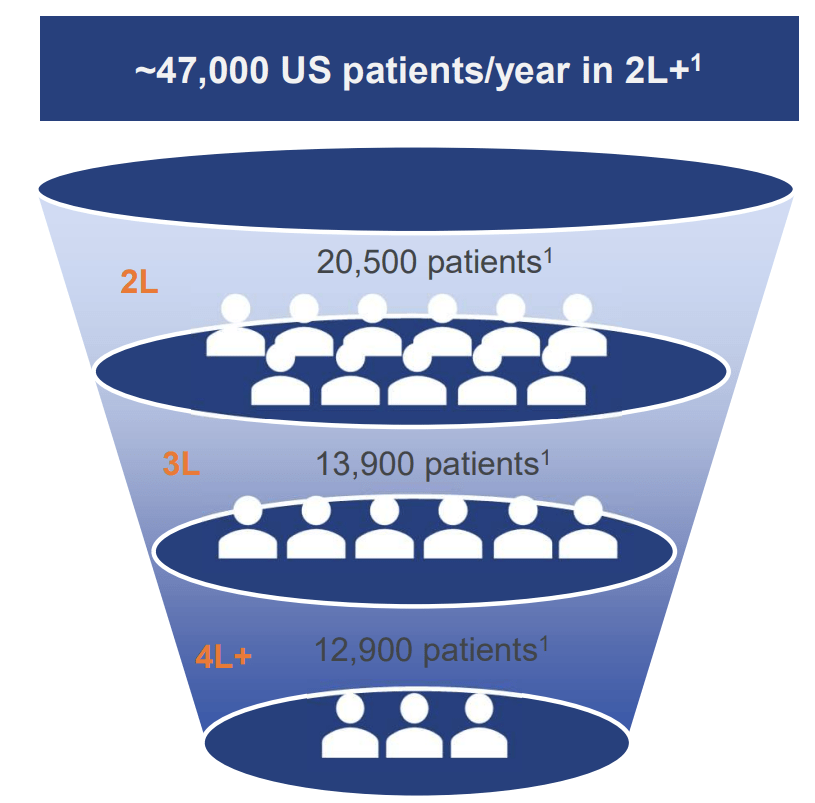

According to KPTI there are 20,500 US patients/year in 2L MM, 13,900 in 3L and 12,900 in 4L+. Considering a dosing of 100mg/week (about 50 doses per year) and price of $29K per 8 x50mg tablets ($7.3K per 100mg dose), the above numbers would correspond to a potential target market of $4.7B just for 4L+ US patients. However, many patients discontinue treatment (either due to side effects or due to progression), many will require dose reduction (=lower revenues) and many will get treated with other options first. So the actual target market is much lower. For example, in a recent real-world small study , selinexor-treated patients had a median progression-free survival of 3 months and 56% required dose-reduction. Based on these data (i.e. assuming that a patient will on average get selinexor for only 3 months and half will require a dose reduction), I estimate a target market at about 10-20% of the above estimate, i.e. about $0.5-1B. If selinexor can penetrate earlier-line patients, the market potential will be much higher, not only due to higher number of eligible patients but also because earlier-line patients are expected to stay longer on treatment.

However, despite approval in 2L MM since December 2020, selinexor sales have been far lower than my above estimate. Not only is there limited growth in revenue but KPTI also cut its 2023 guidance. Specifically, KPTI has guided $110-$125M US revenue for 2023, which is very low compared to the above-estimated target market. This is reflective of preference for other treatment options over selinexor-based options. KPTI hopes to capture more patients in 2L and 3L. However, as explained above, at least based on UpToDate authors, selinexor-based regimens may be considered a last-resort option by clinicians. Therefore, the 4L+ patients seem a more feasible target and there appears to be upside potential even there.

Furthermore, as will be discussed in the next sections, there might be hope for better revenues in MM if the ongoing phase 3 is successful.

{kind=link}

Number of MM patients in US per year in 2L+ (KPTI November corporate presentation)

Will the ongoing phase 3 trial in 2L+ MM improve revenues?

In the ongoing phase 3, selinexor is being evaluated in combination with pomalidomide + dexamethasone. KPTI hopes this will help improve sales considering the following;

- All-oral regimen (patient convenience, especially in the community setting)

- Pomalidomide-dexamethasone is a commonly used backbone, which might allow better market penetration.

- Lower selinexor dose (at 40mg) might prove to be better tolerated. As has been discussed above, available clinical data suggest that lower doses can improve tolerability and quality of life, while at the same time preserving efficacy.

- The combination of selinexor with pomalidomide may preserve T-cell function better than regimens including proteasome inhibitors and/or alkylating agents. This may improve probability of success with subsequent T-cell engaging therapies (see section below).

T-cell function preservation by selinexor

KPTI, in collaboration with academic institutions, is trying to generate evidence to show that selinexor treatment may be advantageous in terms of preserving T-cell function, which may help enhance efficacy and/or durability of response of therapies that depend on T-cell function (CAR-Ts and bispecific antibodies). The success of T-cell engaging therapies may depend on the immune system status, specifically on the competence and fitness of T-cell populations. For example, "crucial to developing a clinically effective biologic CAR-T product is a fit and numerically adequate T-cell population pre-leukapheresis". "Likewise, mitigating T-cell exhaustion after the CAR-T product is infused into the patient to maintain the CAR-T effector function and achieve prolonged clinical potency remains a challenge". Alkylating agents and proteasome inhibitors have been associated with inferior T-cell therapy clinical results. On the contrary, XPO1 inhibitors and immunomodulatory agents may promote T-cell health. Hence, the very promising potential of the combination being studied in the ongoing phase 3 (selinexor+pomalidomide+dexamethasone). Selinexor may have a role both pre- and post-treatment with T-cell engaging therapies.

For those interested, the topic has been recently reviewed . These research efforts may help further improve selinexor's sales. But more clinical data will be needed. As an example, promising initial data have been reported from an ongoing study in relapsed/refractory extramedullary multiple myeloma.

Selinexor in endometrial cancer

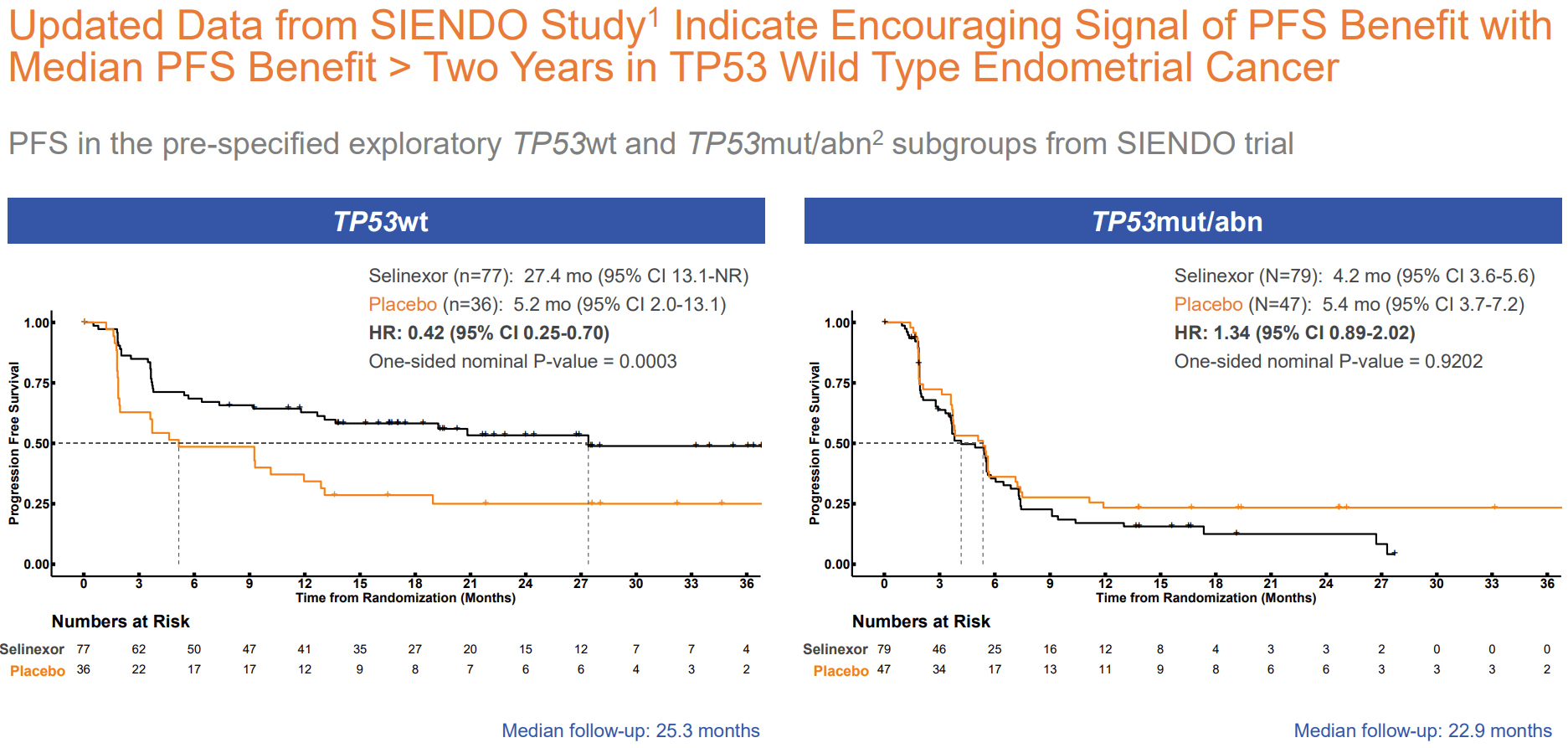

Selinexor's potential in endometrial cancer is well-summarized in KPTI's presentation. In the preceding phase 3 trial (SIENDO) evaluating selinexor as maintenance therapy in advanced/recurrent endometrial cancer, a clinically meaningful and statistically significant improvement in progression free survival was shown in the pre-specified wild-type TP53 (TP53wt) population. This was not just a chance finding but is also supported by strong pathophysiological rationale (retention of tumor suppressor p53 in the nucleus by inhibition of XPO1). Based on these results (a limitation being the small number of placebo patients in the subgroup analysis), I believe probability of success of the ongoing phase 3 trial, which will only enroll TP53wt patients, is high. Notably a lower dose is being used in this trial (60mg vs 80mg QW) which may improve tolerability. KPTI estimates a target population of 8K patients just in the US, which at current selinexor price would correspond to a $3B target market.

{kind=link}

Selinexor's potential in endometrial cancer (KPTI's November corporate presentation)

{kind=link}

Impressive benefit in TP53wt patients (KPTI November corporate presentation)

Selinexor in myelofibrosis

Selinexor is being evaluated in an ongoing ph1/3 study in frontline JAKi-naive myelofibrosis in combination with ruxolitinib. Results of the phase 1 part were impressive (see image below). Promising is also the durability of responses; "As of the August 1, 2023 data cut-off date, all patients treated with 60mg selinexor and who achieved ?35% reduction in spleen volume (SVR35) at week 24 (n=11), continued to remain in radiographic response. In addition, all of the seven patients who achieved TSS50 at Week 24 remained in response as of the data cut-off". KPTI will have an oral presentation at ASH, December 10.

Phase 1 results compare favorably to pelabresib (SVR35 66%, TSS50 52%) and navitoclax (SVR35 52%, TSS50 31% in the phase 2 study), which are the main late-stage competitors for the same indication. However, between-trial comparison is not recommended and KPTI's study was very small (n=12). Therefore, it is uncertain whether ph3 topline will be as impressive, but if they are selinexor may have a major commercial advantage over competition. Notably, both pelabresib and navitoclax did not meet the TSS50 endpoint in their ph3 trials.

The myelofibrosis market has been discussed in my recent coverage of MOR. Therefore, I refer readers to that article for more info. KPTI estimates a target population of 4.3K patients in the US, which based on current pricing of selinexor would correspond a market potential of about $1.5B. However, considering competition and pending phase 3 topline it is unclear if selinexor will be able to successfully penetrate the myelofibrosis market.

{kind=link}

Impressive results in ph1 myelofibrosis study (KPTI November corporate presentation)

Competitors in XPO1 targeting?

Searching the term XPO1 in ClinicalTrials.gov almost all of retrieved studies were on selinexor and eltanexor. On the one hand, this suggests KPTI is the leader in targeting this pathway, with limited risk from competition emerging targeting the same pathway. On the other hand, other pharmas not pursuing this target could suggest perceived lack of potential. Nevertheless, I did find a single phase 1 study by Stemline Therapeutics, which seems to be developing felezonexor (an XPO1 inhibitor) for solid tumors. In a recent review , there also does not seem to be any competition targeting XPO1.

Financials

KPTI reported that cash and cash equivalents, restricted cash and investments as of September 30, 2023 totaled $209.2M, compared to $279.7M as of December 31, 2022. Total revenue was $36M (predominantly from US selinexor sales), while total operating expenses were $67M (cost of sales $0.9M, R&D $35.6M, SG&A $30.8M). In other words, KPTI's expenses are currently about double the revenues. Notably, revenues have remained stagnant since 2022, adversely affected by more patients using the patient assistance program, as well as higher gross to net discounts.

Based on available cash and projected revenues (US sales and license revenues) KPTI has guided a cash runaway into late 2025, "excluding maturity of convertible bonds in October of 2025". This seems sufficient for topline of all 3 ongoing phase 3 studies, at the minimum for MM and endometrial cancer.

Of note are total liabilities of $370M, including $170M in senior convertible senior bonds maturing in October 2025 (not accounted for in the projected cash runaway) and $133M in deferred royalty obligations. With regards to the latter, KPTI will have to pay $56M by June 30, 2025 (unclear if these are accounted for in the projected runaway) .

Risks

- The main risk is failure in ongoing phase 3 trials.

- Another risk is emergence of competition with better efficacy and/or better tolerability. As acknowledged by KPTI in the latest 10Q ; "Several new novel therapeutics have recently entered, and are expected to continue to enter, the multiple myeloma treatment landscape. TECVAYLI™ (teclistamab-cqyv), the first bispecific T-Cell engager was approved by the FDA in October 2022, followed by approvals of two more bispecifics, ELREXFIO™ (elranatamab-bcmm) and TALVEY™ (talquetamab-tgvs) in August 2023. Other T-cell engaging therapies, bispecifics with different targets, immunomodulators, and a BCL-2 inhibitor are in clinical development and may be introduced into the multiple myeloma market in 2023. In addition, future label expansions into earlier lines of existing therapies are anticipated in 2023 and beyond. The approval of these anti-cancer agents, or any others which may receive regulatory approval, may have a significant impact on the therapeutic landscape and our product revenues.". Nevertheless, "While we expect further intensification of the competitive landscape in the late lines, in the mid to long term, we believe that the potential approval of SPD and further data generation around the T-cell fitness space with novel combinations could unlock further benefits for myeloma patients with XPOVIO". As explained above I agree that the T-cell sparing potential of SPD combination could prove to be a major commercial advantage.

- Even though projected cash runaway is beyond expected catalysts there KPTI will need to raise cash before. Lower than anticipated revenues may impact KPTI's estimated cash runaway. Furthermore, projected cash runaway does not seem to account for liabilities, especially convertible senior notes maturing in October 2025. Hopefully, with good results from ongoing phase 3s dilutional impact from raising cash will be lower.

- Finally, with a current bid price <$1 there is risk of de-listing. Considering the potential for 2x 180-day extensions, KPTI will have about a year to increase the price to >$1. However, considering the timing of anticipated catalysts there is a chance KPTI might be forced to a reverse-split. Personally, I believe there is decent probability of getting back to >$1.

Conclusion

KPTI has a decent cash runaway for a micro-cap biotech, which seems to be sufficient for major catalysts. Success in any of the 3 ongoing phase 3 trials could significantly improve revenues by selinexor. On the other hand, with catalysts being far away the downward momentum may continue or there may be little if any upside in the short term. Notably, KPTI is rated as a "Strong Sell" according to SA's quant rating. Therefore, investing closer to the upcoming catalysts may be safer. However, I believe KPTI is undervalued and may be close to the bottom considering; (1) approved commercial product (despite underwhelming revenue growth so far, 3 approvals indicate a successful drug developer) with established global commercial infrastructure to support new launches after potential label expansions, (2) cash runaway beyond major catalysts, (3) potential for $1-2B annual peak sales if any of ongoing phase 3s are successful (compared to a current EV of $182M). I believe the market is underestimating selinexor's potential. At least a small watchlist position may be worth it, but will require patience and represents a high-risk speculative investment facing fierce competition. Considering liabilities KPTI will also have to raise cash before mid-2025.

For further details see:

Karyopharm Therapeutics: Promising Potential With 3 Ongoing Phase 3 Studies But Risky