KPLT - Katapult Redemption

2023-06-13 09:00:00 ET

Summary

- First Positive Adjusted EBITDA Since Q3-2021.

- Healthy NPS and Repeat Customers Are Gold for Katapult.

- 12 "Direct" Merchants Added with "Enterprise-class" Ones on Horizon.

- New Revenue Booster Success Using Targeted Marketing Campaigns.

- Merchant Advisory Group Partnership Adds Synergy.

Katapult is a Lease-To-Own company that focuses on the subprime market; it has a disruptive virtual payment technology called Katapult Pay , and its true value proposition is in providing a smooth customer user experience supporting checkout conversion with tight collaboration from a growing army of merchants. The company IPO'ed at $10 and is now selling for ~$0.60 at the time of this article. For Q2, Katapult is expecting flat sales, but for Q3 and forward, the company could finally achieve profitability. Their gross originations have been increasing steadily in the double-digits, and it takes at least 2 quarters to realize that revenue. As stated in my last article on Katapult , I believe they have a niche , and their TAM is growing in size considering the current economy.

Katapult ( KPLT ) investors knew going into the Q1 call that the company would experience another loss; in their Q4 earnings call , they had specifically mentioned upcoming " one-time Q1 expenses related to severance ". The real crux for Q1 was to see that if the severance costs were removed whether Katapult would show a profit, and they did.

Katapult is now on a roll, and as CEO Orlando " Oz " Zayas stated on the call, Katapult " had an outstanding Q1. " As he has repeated in past calls, " historically lease-to-own solutions benefit from periods of shrinking prime credit availability, creating a counter-cyclical hedge against the challenging macro environment." So, in our current economy, Katapult is a recession-proof , beacon of hope for " over 30% of Americans overlooked by traditional financing options [with] 39% not being able to cover $400 of an emergency expense without assistance. " The CEO's logic has proven true, and Katapult booked a 17% y-o-y increase in gross originations in Q1 and achieved the company's first positive adjusted EBITDA since Q3-2021.

{kind=link}

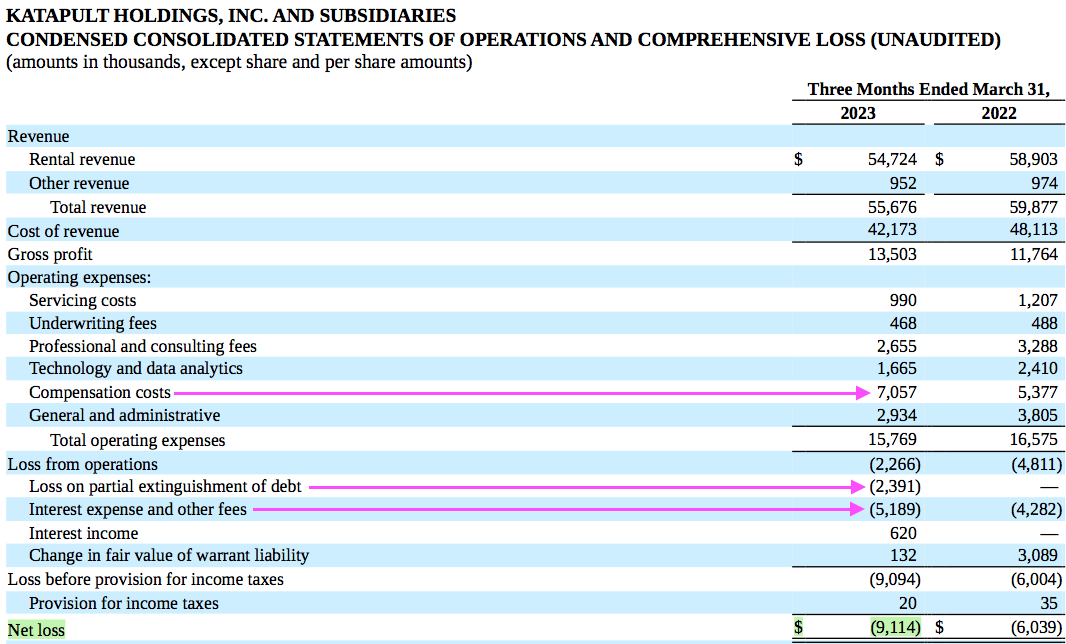

If you look at Katapult's latest 10-Q above, there are three costs which would catapult Katapult into the black if they were removed or reduced; however, in any type of fundamental analysis, they would really never be excluded. The first involves employee " Compensation costs" which includes severance and was $7.057mm; the second was the penalty for prepaying the Term Loan which was a hefty $2.391mm; the third was the " Interest expense and other fees " which were $5.189mm; that's almost $15mm; the company posted a $9.114mm net loss, so if these costs were removed or reduced, that would bring Katapult into profitable territory. Still, Katapult did not disclose the severance costs, so I am really just highlighting costs to look for in the next earnings call.

The company paid $25mm on its $50mm Term Loan; this move protects Katapult from a 1.5% interest rate increase on the PIK by maintaining greater than $25mm liquidity as defined in the credit agreement ; the PIK stays at 4.5% and has not increased to 6%.

Katapult also reduced the $125M RLOC to $75M to create a more efficient capital structure.

Of course, all " Compensation costs " cannot be removed, but Q1 severance costs did play a part which will not be present going forward. The penalty was definitely a one-time cost. The " Interest expense and other fees " cannot be removed entirely; this is a high-interest rate environment right now, and all eyes are on the Federal Reserve's next policy meeting where they are expected to hold pat which would be good news for Katapult.

Since Katapult's Q4-2022 earnings call when major cost-cutting was announced, including headcount reduction, Katapult's stock has taken a beating and hit a low of $0.40. The stock was at a $1+ perch, and then Silicon Valley Bank collapsed ; this caused a lot of collateral damage to many stocks, and Katapult was not spared with theirs sinking more than 50% in just a week. Panic on the market is a wild sight to see, and always makes me return to Warren Buffett - " be fearful when the markets get greedy, be greedy when the markets get fearful" , especially if you believe in a company's value proposition.

Although Katapult trades below $1 per share, I don't think investors should be too worried about delisting potential. If by the end of the year, they are still below $1, they did state in an SEC prospectus supplement on 4/12 a reverse-split potential which would bring them above $1 and negate the delisting threat. However, I doubt they'll remain at less than $1 for the entire year, and even if they are by the October delist-deadline, they're still eligible for a 180-day extension.

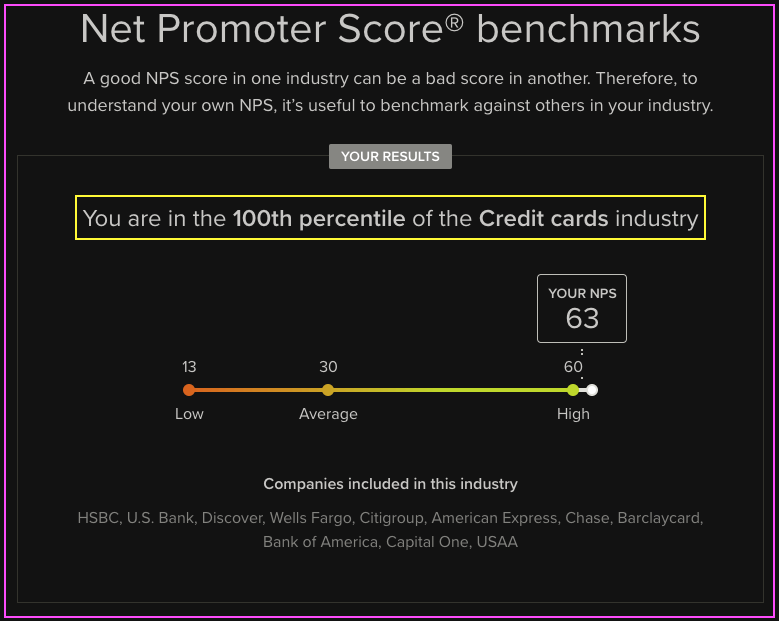

Katapult Net Promoter Score Q1-2023 (Delighted.com)

{kind=link}

It's a nebulous statistic albeit an important one ( image above ); it's called the Net Promoter Score , and it was the first thing Oz mentioned on the call. Katapult achieved an NPS of 63 which is excellent considering the range is from -100 to +100. If you compare Katapult's grade to the industry , they're in the top 100% percentile. This is a very important statistic and should help increase confidence in the company.

In addition, the company continues to tout its repeat customers business each quarter which makes up a significant proportion of the revenue. This quarter's repeat business was 47% of all gross originations. Last quarter's repeat business was 50% , and the quarter before that it was 46% . Katapult understands the importance of this statistic, for it represents the overall health of the company and the perception consumers have of it. The statistic also represents a much safer revenue stream since this is coming from past customers who have paid their bills responsibly.

Putting all your eggs in one basket is never a good idea. Katapult understands that, and albeit an unfavorable economic climate, it continues to exhibit growth by acquiring new merchants; in Q1 alone, Katapult added 12 new " direct " merchants. As Katapult has continued to add more merchants, the percentage of gross originations from their biggest partner has decreased. Last quarter, Wayfair ( W ), went from 58% to 51% year over year. Also important to understand is that with a " direct " integration of Katapult into a merchant's POS system, it facilitates a much tighter collaboration with that merchant, along with a greater probability of a checkout conversion in Katapult's favor. It gives Katapult an advantage over competitors like Affirm ( AFRM ), Acima, Westcreek et al. Companies like Wayfair, Sears and many others are " direct " merchants with Katapult.

In addition to the new " direct " merchants, Katapult also added IKEA as a Katapult Pay merchant; over 775 million people visited IKEA last year alone, so that is yet another addition to Katapult's revenue stream.

Katapult Adds 12 New Merchants (SeekingAlpha.com)

In addition to the merchant acquisitions, the CEO also mentioned that Katapult continues " to have active discussions with several new enterprise-class prospects , as well as build their active sales funnel in a variety of product categories. " If Katapult were to add another Wayfair this year, their stock would surely jump on the news.

Katapult - Targeted Marketing (SlideServe.com)

In addition to expanding growth by adding new merchants , Katapult is testing a new strategy of " targeted marketing ". Last quarter, they joined Wayfair in their big Way Day sale from April 26-28 which more than doubled Wayfair's average gross originations with Katapult during those three days. In addition to the success of this new marketing strategy, " results from a recent test marketing campaign for spring home and garden improvement showed significantly enhanced levels of effectiveness compared to traditional methods. "

Mission Statement (Merchant Advisory Group)

{kind=link}

A final positive to mention about this past quarter is Katapult's new partnership with the Merchant Advisory Group , the leading payments industry association for enterprise merchants; this partnership gives Katapult more credentials in the Lease-to-Own arena and makes them even more legitimate in customers' eyes. From their mission statement, the organization collaborates, educates and advocates for its " partners " which Katapult now is, so that is a good thing.

The table below lists revenue declared for the following quarters over this past year along with EPS; note that Q1-2023's EPS got hit with the one-time expenses aforementioned that will not be present for Q2:

- Q1-2022 Revenue: $59.9mm EPS: -$0.06.

- Q2-2022 Revenue: $53.0mm EPS: -$0.10.

- Q3-2022 Revenue: $50.3mm EPS: -$0.08.

- Q4-2022 Revenue: $48.8mm EPS: -$0.15.

- Q1-2023 Revenue: $55.7mm EPS: -$0.09.

Katapult must work within this revenue, streamline the company and profit could be on the near horizon. The Katapult CFO claims Q2 revenue growth will be " flat " year-over-year, but she is holding her cards closely and wisely being conservative. With 1) the relatively new Katapult Pay feature on their mobile app continuing to generate increased revenue, 2) the recent success of their targeted marketing campaigns, 3) the continued repeat-customer percentage of revenue at almost 50%, 4) the consistent Net Promoter Score excellence and 5) the steady stream of new merchant acquisitions, growth is clearly visible. Since this increase in gross originations takes a couple quarters to be realized, that means the good news on gross originations in Q1 will really hit in Q3. With the one-time costs behind Katapult, anything is possible for the next call, but a breakeven would be grand. Regardless though, on the Q2 earnings call, it will be the Q3 guidance that will be the real harbinger.

In my last article on Katapult, I advised investors to Hold their Katapult shares, and I still believe that, or add more and average down. I think the new CFO is a godsend for the company. The CEO, Orlando Zayas comes from the street and is no stranger to the subprime credit arena. Thus, he makes a good and humble leader for Katapult. I think the next few quarters will mark Katapult's turnaround year.

There is a big risk investing in a stock like Katapult, but there is also potential for a big reward. I rode with Enphase Energy ( ENPH ) from $15 down to below $1 a share and almost lost my shirt, but I always believed in their company's value proposition, and luckily they received a cash infusion from TJ Rodgers and L. John Doerr in 2017, or they would have gone bankrupt, and the rest is history. The good guys and the better technology does not always win; the Betamax versus VHS tech story is a prime example, and BetaMax was better. As always, do your own due diligence. Do not bet what you are not willing to lose. Good luck.

For further details see:

Katapult Redemption