KBH - KB Home: Buy Into The Weakness

2023-03-30 12:31:48 ET

Summary

- KB Home has had a great few years, but leading indicators imply that weakness lies ahead.

- A plunge in backlog, caused by weak orders and a surge in the firm's cancellation rate, points to a decline in revenue, profits, and cash flows this year and beyond.

- Despite this pain, shares of the business are cheap and likely warrant some upside.

After years of attractive growth, the home-building space is starting to be viewed as rather taboo. A mixture of factors, including inflation that allowed home builders to hike their prices and a nationwide housing shortage, resulted in a surge of orders, new deliveries, revenues, profits, and cash flows in the space. One of the beneficiaries of this has been KB Home ( KBH ), a home builder with a long history spanning more than 65 years. Based on the data that's currently available, it seems very likely to me that the next year or so will be particularly unpleasant for the business. Having said that, there are some strong catalysts that should help to propel it forward in the long run. Relative to similar firms, the stock looks to be pretty much fairly valued. But on an absolute basis, shares do look cheap enough to warrant a bit of upside even with the pain that lies ahead.

Great growth

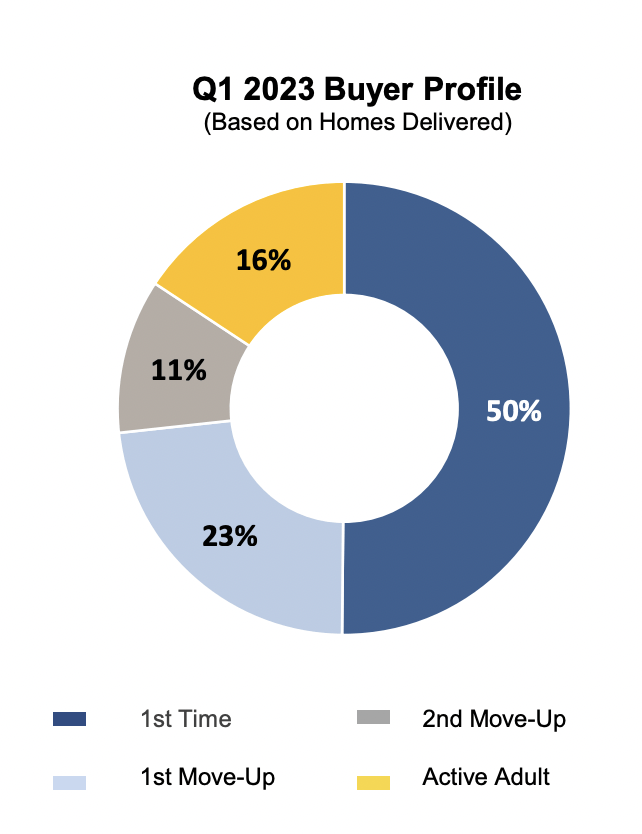

According to the management team at KB Home, the company specializes in providing homes to first-time home buyers. In fact, based on the homes that were delivered in the first quarter of the 2023 fiscal year, 50% of all deliveries were to first-time home buyers. Another 23% of deliveries were to first move-up buyers. The company targets these home buyers specifically by acquiring land positions in prime growth sub-markets, and positioning the homes that they make to appeal to the median household income in each sub-market.

{kind=link}

With a market capitalization of only $3.3 billion, KB Home is a fairly small firm. However, it has operations spanning across many parts of the US. On the West Coast, for instance, the company engages in home-building activities throughout California, Idaho, and Washington state. In the southwest, it operates in Arizona and Nevada. It also engages in activities throughout Colorado, Texas, Florida, and North Carolina. This is basically a list of some of the hottest real estate markets in the country. This is not to say, however, that the activities look the same everywhere. For instance, on the West Coast, the average selling price of a home is the highest, coming in at $687,000. That compares to the $394,000 in average pricing seen in the southeast. Even though pricing is highest on the West Coast, the largest number of deliveries reported by the company comes from places like Colorado and Texas. But 39% of its sales, accounting for the lion's share of revenue, comes from the West Coast.

{kind=link}

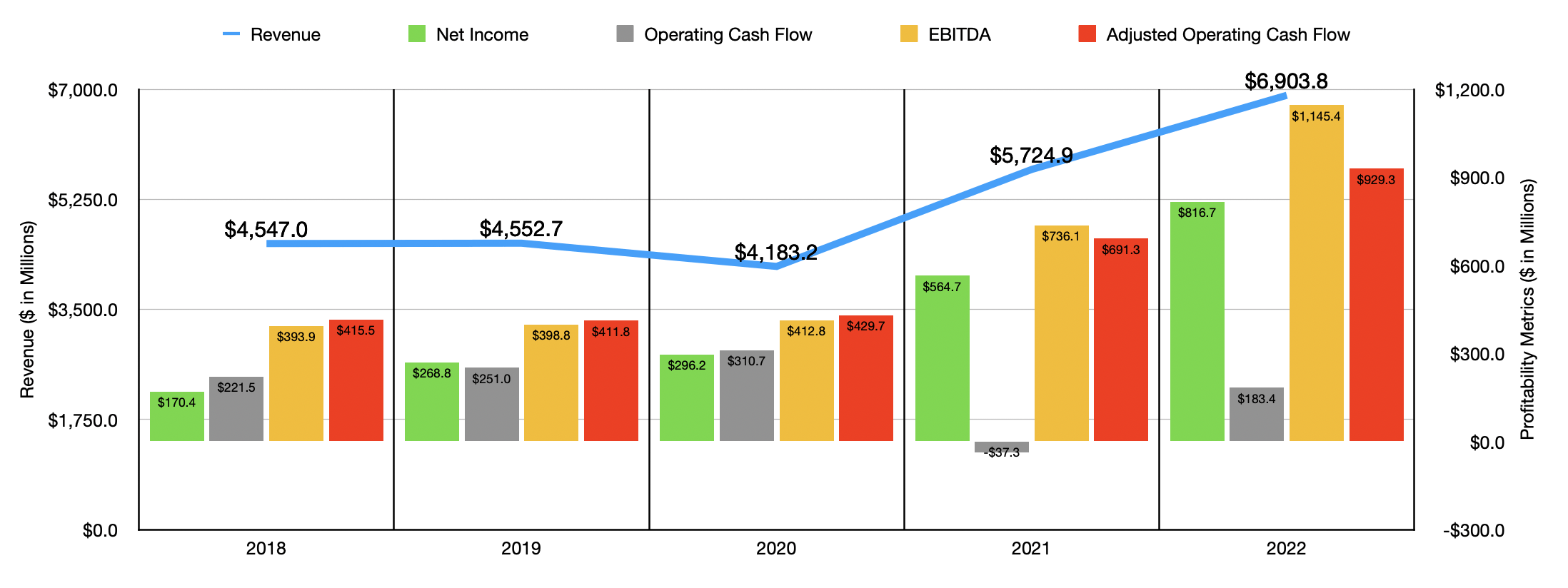

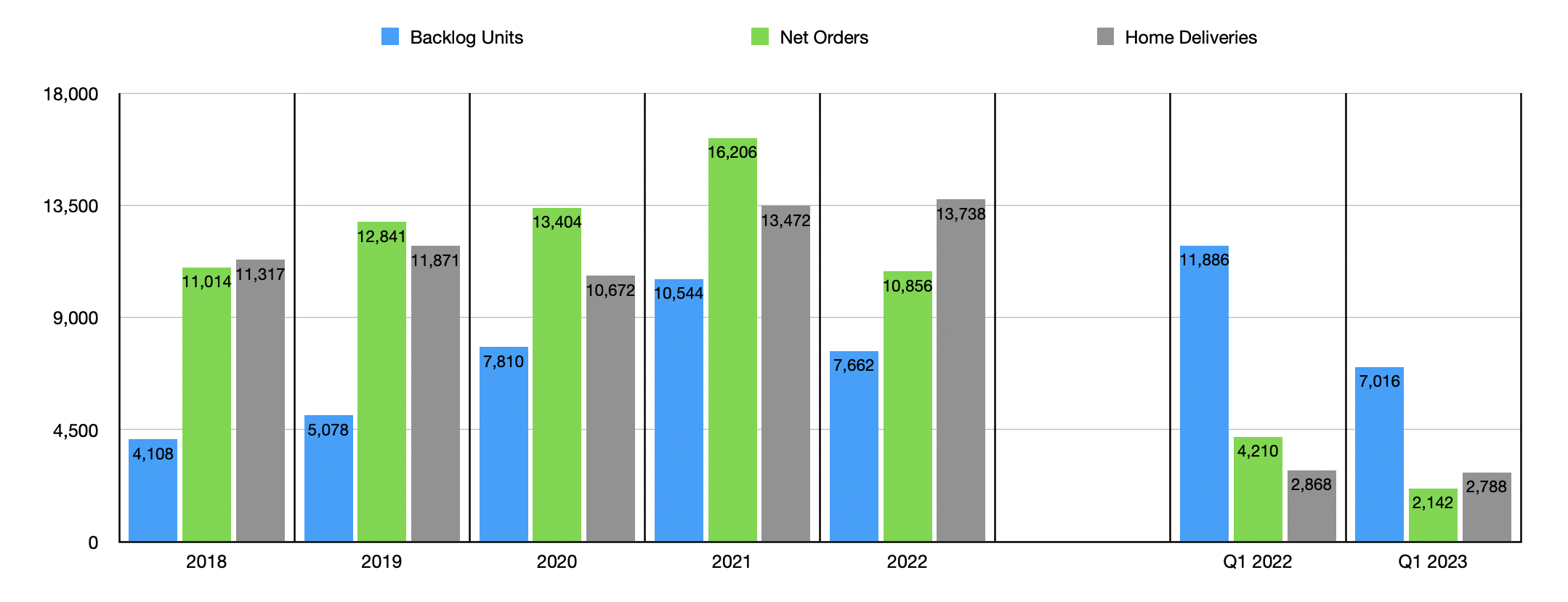

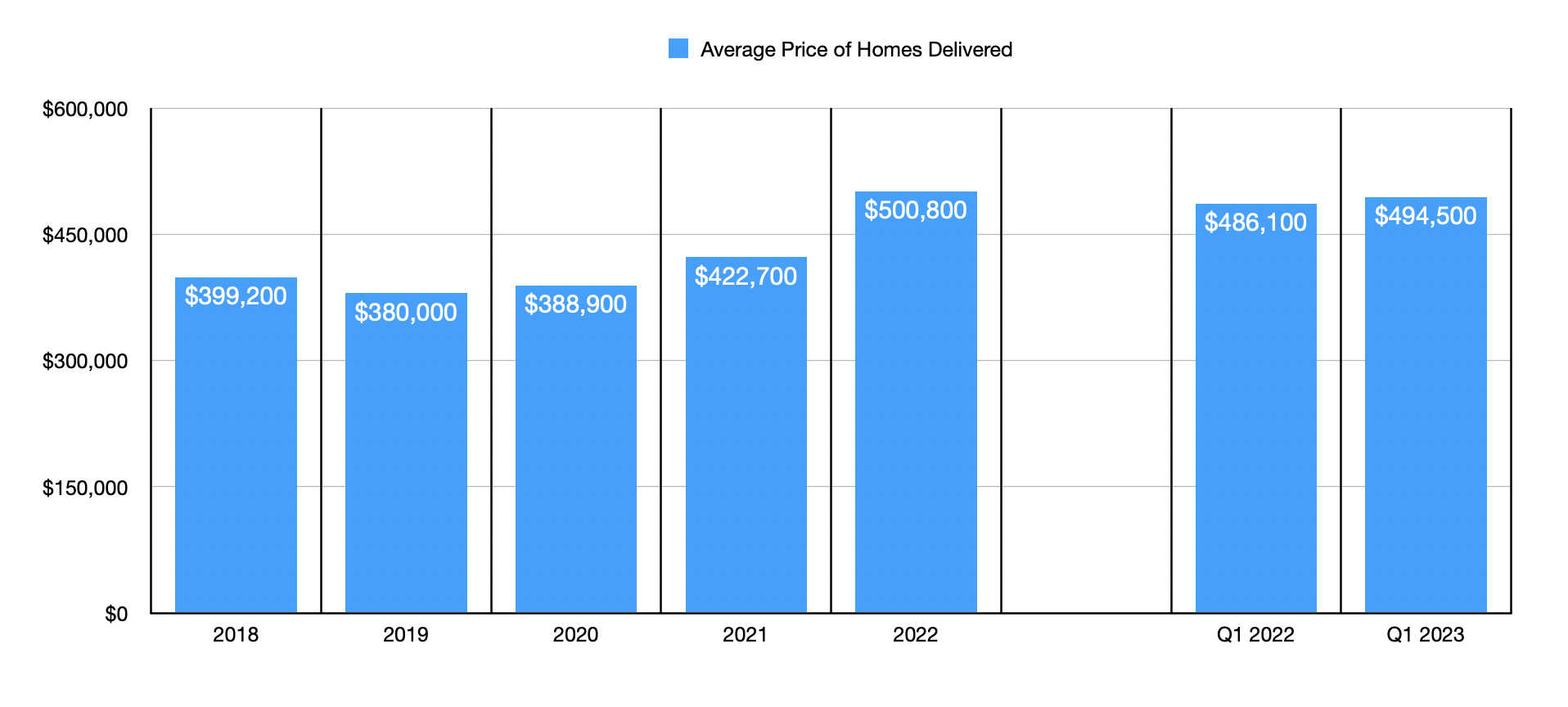

Over the past five fiscal years, the financial picture seen by KB Home has been quite positive. Revenue for the business has grown from $4.55 billion in 2018 to $6.90 billion in 2022. It is worth noting, however, that between 2018 and 2020, sales for the company actually declined. This drop was driven by both a fall and the number of homes delivered and eight o'clock nine in the average selling prices of the homes that were delivered. But starting in 2021, that picture improved markedly. The company went from 10,672 deliveries in 2020 to 13,472 and 2021. By 2022, that number had grown to 13,738. Over that window of time, the average price per home delivered grew from $388,900 to $500,800.

{kind=link}

On the bottom line, the picture for the business has also improved. In each of the past five years, net profits have grown, climbing from $170.4 million in 2018 to $816.7 million in 2022. Other profitability metrics largely followed suit. The one exception is operating cash flow. As you can see in the first chart in this article, that number has bounced all over the map. But if we adjust for changes in working capital, we would see that number rise almost every year, climbing from $415.5 million to $929.3 million. Meanwhile, EBITDA for the business expanded from $393.9 million to $1.15 billion over the past five years.

{kind=link}

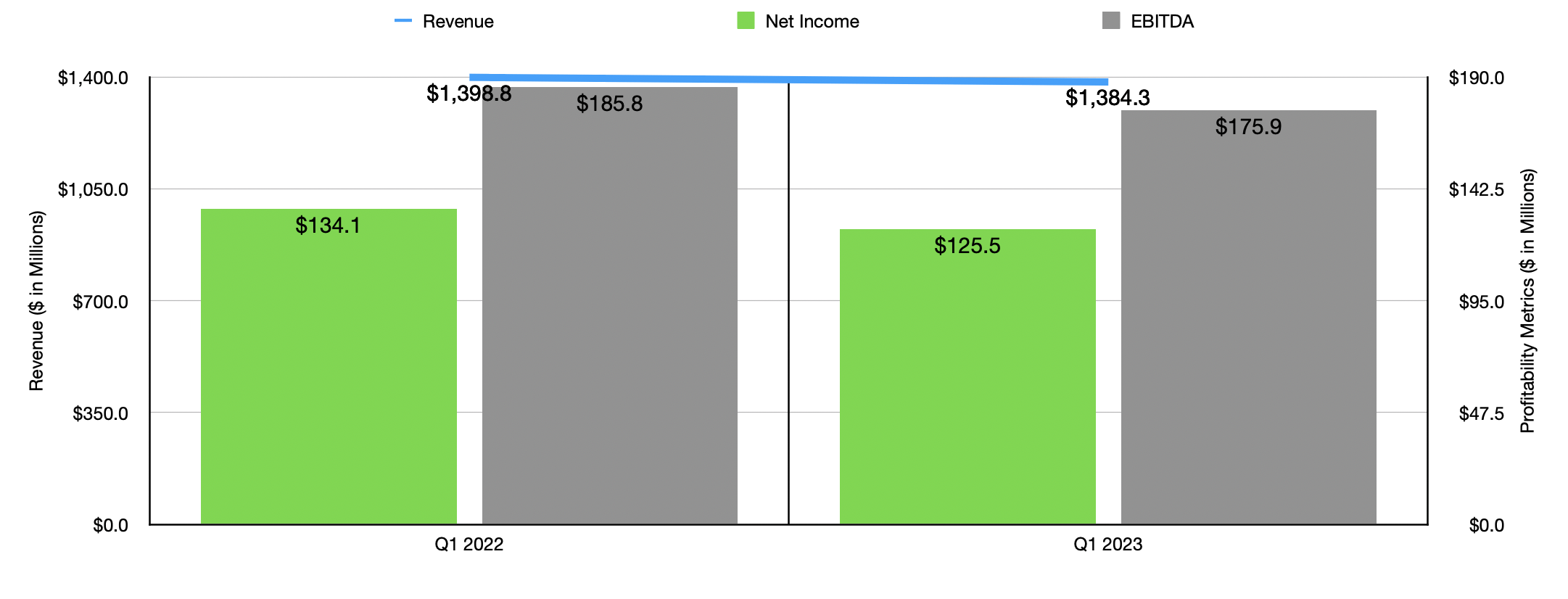

Management has provided some data covering the first quarter of the 2023 fiscal year. During this time, revenue pulled back slightly, dropping from $1.40 billion to $1.38 billion. This was largely the result of home deliveries falling from 2,868 to 2,788. Thankfully, this was largely offset by a rise in the average price of homes delivered from $486,100 to $494,500. Unfortunately, the drop in revenue also brought with it a decline in profits. Net income, for instance, dropped from $134.3 million to $125.5 million. We have not seen operating cash flow data reported yet. But EBITDA for the company fell from $185.8 million to $175.9 million over the same window of time.

{kind=link}

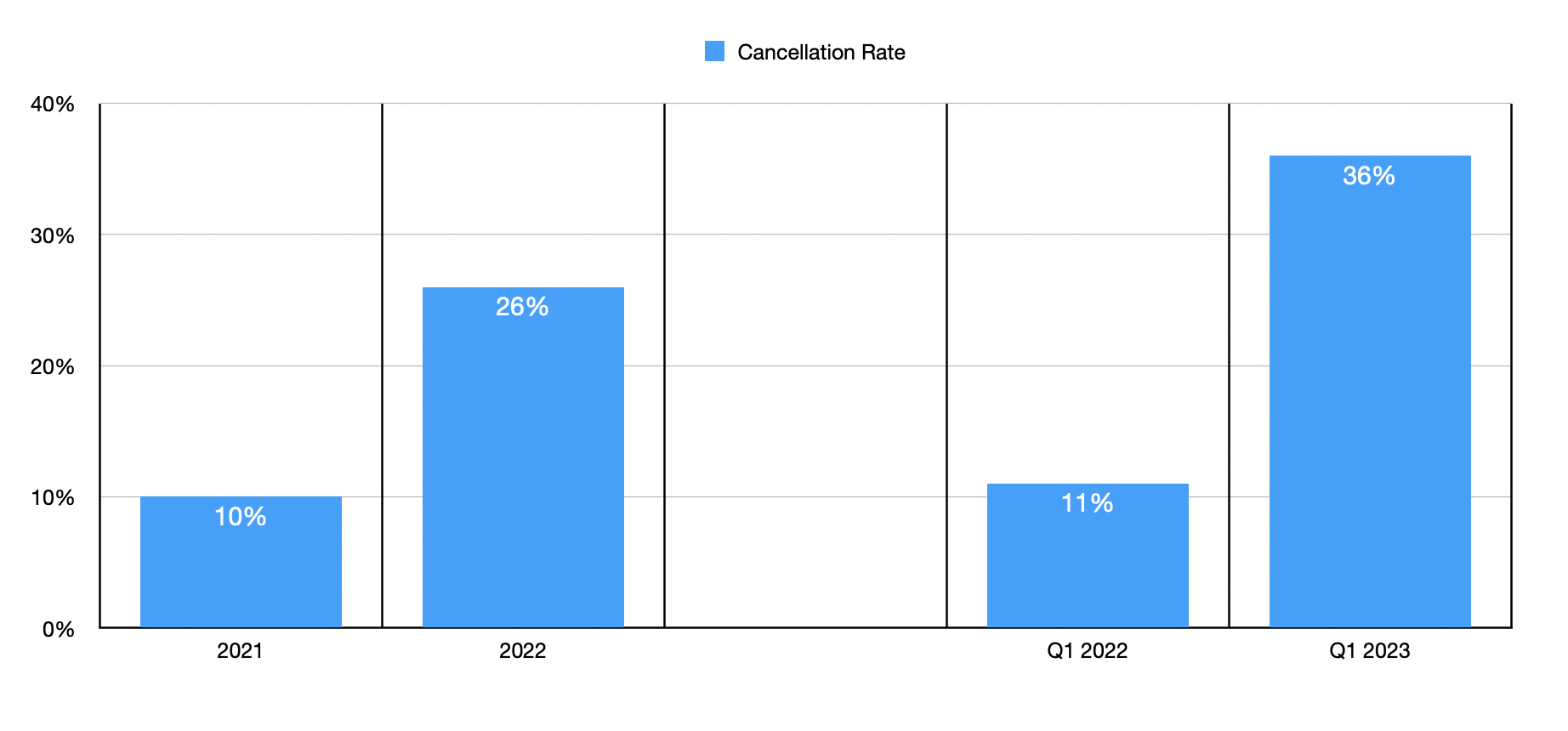

At first glance, this all looks like a blip on the radar. After all, not every quarter can be better than the year before it in perpetuity. But when you dig deeper, you start to see some problems. The number of net orders for homes, for instance, totaled 16,206 in 2021. That number dropped to 10,856 in 2022. This decline, coupled with the modest rise in deliveries, resulted in ending backlog for the company dropping from 10,544 to 7,662. Also problematic was the fact that the cancellation rate for the business nearly tripled from 10% in 2021 to 26% in 2022. When it comes to the first quarter this year, the picture looks even worse. Ending backlog of 7,016 came in far lower than the 11,886 properties reported one year earlier. In addition to deliveries still remaining fairly robust, the company also suffered from a surge in cancellation rates from 11% to 36%. On top of this, the company saw the number of net orders fall from 4,210 in the first quarter of 2022 to 2,142 in the first quarter of this year.

{kind=link}

Management is well aware of these issues and the impact they might have on the company. For 2023, for instance, management is forecasting housing revenue of between $5.20 billion and $5.90 billion. At the midpoint, that would translate to a year-over-year decline of 19.3%. The company has not provided a great deal of detail into what will cause the decline. The only thing that they have said is that the average selling price should drop to between $480,000 and $490,000. So not only is the company dealing with elevated cancellation rates and low new net order rates, it is also contending with being forced to lower prices to keep the picture from being even worse. When you consider that the focus of the business is on first-time home buyers, such weakness does make a lot of sense. After all, those who are candidates to buy a home for the first time would be those who are most likely to be financially vulnerable during periods of economic uncertainty. So you would expect them to show the greatest weakness compared to other types of home buyers.

{kind=link}

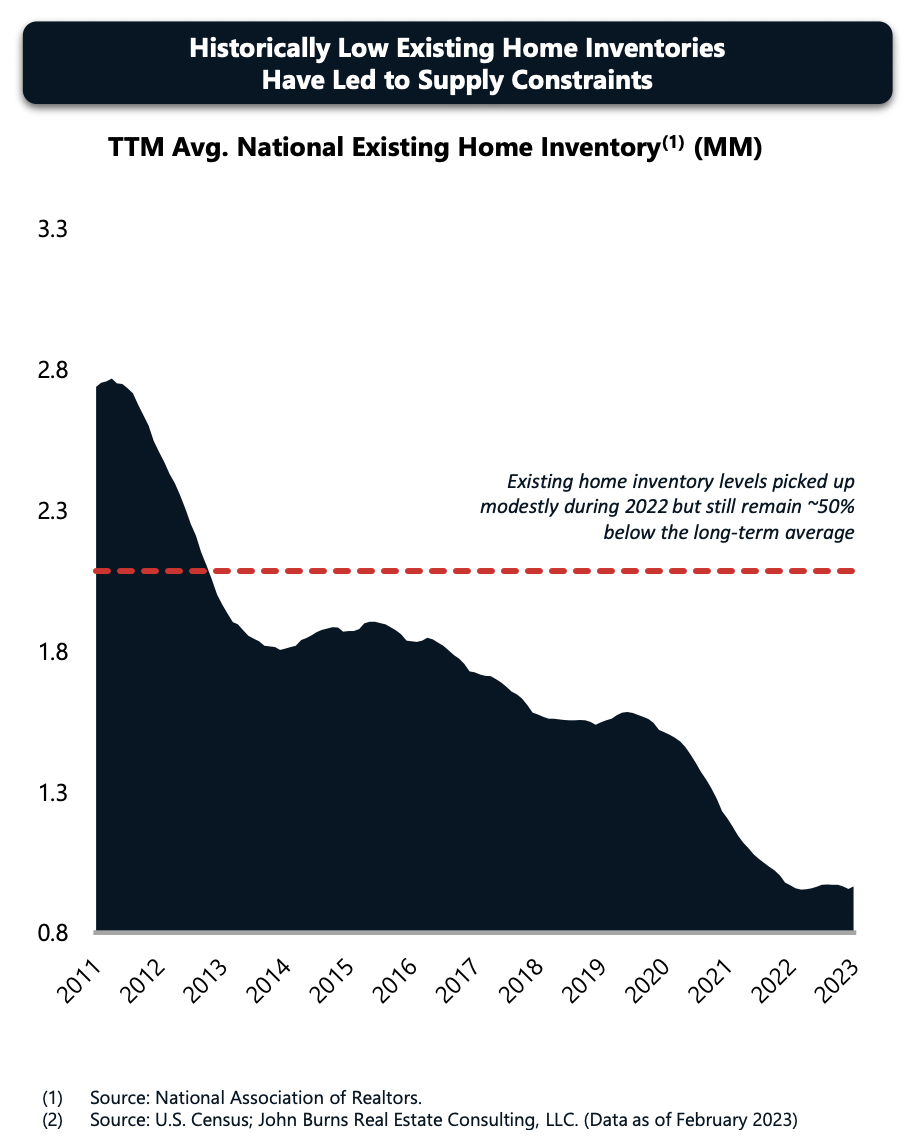

Another company that I'm currently looking at is a REIT known as American Homes 4 Rent ( AMH ). In my research for that company, I came across some interesting data regarding the national existing home inventory. In 2011, home inventories in the US came out to around 2.8 million. But in recent years, that number has plunged. For 2023, it's estimated that the number is right around 900,000. What this suggests to me is that, while we may face some weakness in the home building market in the near term because of economic issues, rising interest rates, and other factors, the construction of new homes must eventually pick up again. I see this as a long-term catalyst for KB Home, as well as other similar enterprises.

{kind=link}

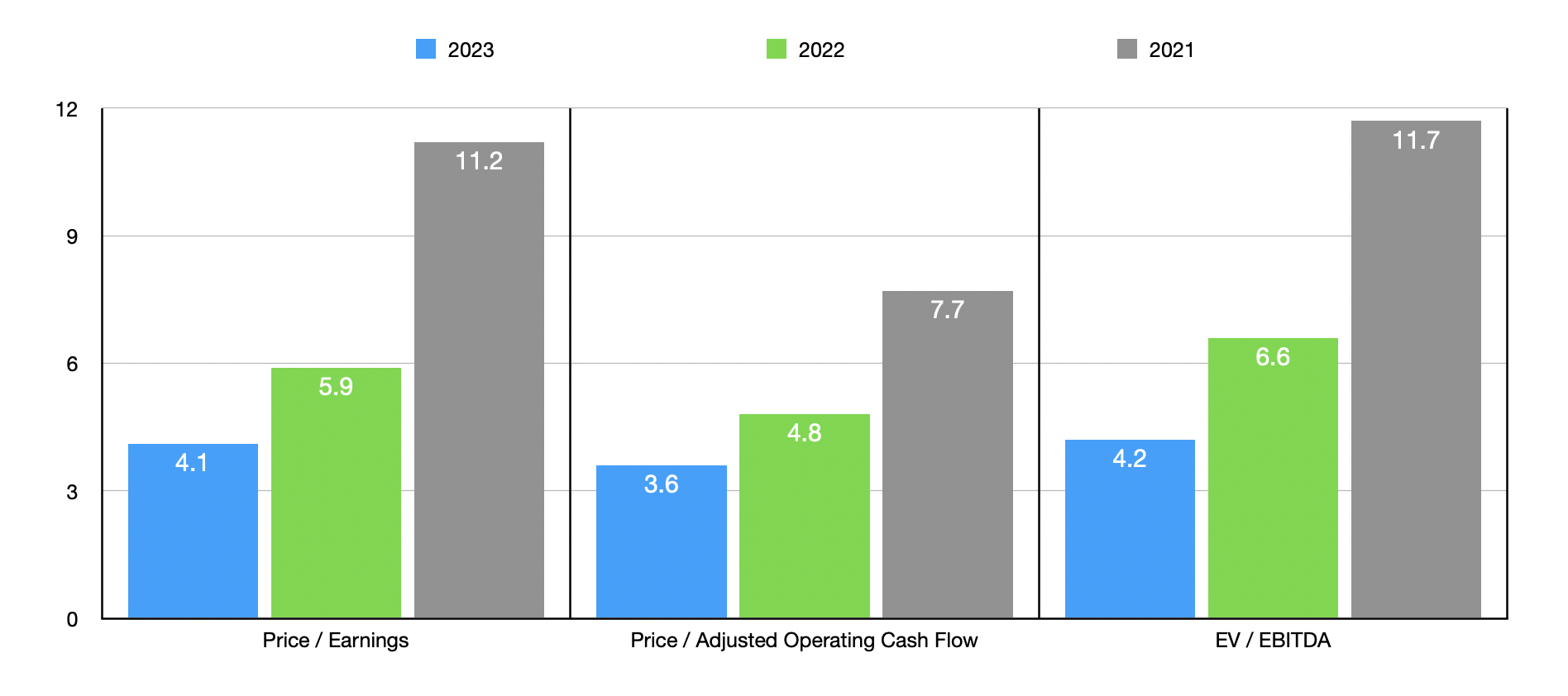

Of course, investors also need to pay attention to how much they pay for the company in question. Growth does not necessarily equate to upside. The good news for shareholders is that the stock looks very cheap. In the chart above, I priced the company using data from 2020, 2021, and 2022. And in the table below I compared the firm to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 2.2 to a high of 7.8. Two of the five firms were cheaper than KB Home, while another one was tied with it. Using the price to operating cash flow approach, the range was from 3.9 to 44.3. Our prospect was the cheapest of the group in this case. And finally, using the EV to EBITDA approach, we get a range of between 3.4 and 5.9. Three of the five companies were cheaper than our prospect in this scenario.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| KB Home |

| 4.1 |

| 3.6 |

| 4.2 |

| Taylor Morrison Home Corporation ( TMHC ) |

| 4.1 |

| 3.9 |

| 3.9 |

| Legacy Housing ( LEGH ) |

| 7.8 |

| 44.3 |

| 5.9 |

| Meritage Homes ( MTH ) |

| 4.3 |

| 10.5 |

| 3.4 |

| Century Communities ( CCS ) |

| 3.9 |

| 6.4 |

| 4.0 |

| Beazer Homes USA ( BZH ) |

| 2.2 |

| 6.3 |

| 4.8 |

Takeaway

From what I can see, KB Home is a solid enterprise that has done quite well for itself in recent years. We are seeing some signs of significant weakness on the horizon and it looks like that weakness will affect the business starting this year. But this doesn't necessarily mean that investors should stay away from the firm. Although the stock looks more or less fairly valued compared to similar businesses, it looks very cheap on an absolute basis. It boasts an attractive catalyst that should help it to grow in the years to come, and even if financial performance reverts back to what it was in 2020, the stock does not look all that pricey. Due to these factors, I've decided to rate the company a soft ‘buy’ at this time.

For further details see:

KB Home: Buy Into The Weakness