KBCSF - KBC Group: Impressive But Expensive

2023-04-21 06:30:00 ET

Summary

- The bank looks sensitive on Held to Maturity and Available for Sale bonds.

- The negative implication from Czech Bank Tax and €673 million less in equity value from the IFRS17 update.

- KBC offers a lower dividend yield within our EU banking coverage.

- Solid capital requirements (with no impact from IFRS17 implementation), but the valuation looks full on a tangible book value. We prefer other banks.

This week, KBC Group NV ( OTCPK:KBCSF , OTCPK:KBCSY ) released its IFRS 17 implementation estimate and it is time to review our company's investment case. Before analyzing the restated 2022 financial figures, we would like to say that, here at the Lab, we are not forecasting a banking crisis, but it is important to review banks on three potential main issues. The first is the bank bond portfolios and their weight as a percentage of deposits; the second is the number of bonds classified in banks' financial statements as mark-to-market (subject to market price changes called Available For Sale) and those held to maturity (Held To Maturity), in addition, the third check is on the potential deposit outflows. Following SVB's failure, we believe that regulators will increase the oversight framework for smaller banks. On the positive side, there will be further improvements in short-term profit margins with rates approaching 4%, but as already mentioned, attention will shift to refinancing costs for companies and possible asset quality problems.

While SVB had a heavily bond-biased balance sheet, in Europe, bond portfolios account for around 20% of total deposits. We should add that 88% of SVB's deposits were uninsured, a fact truly unique compared to the main US and European banks. At this point, we calculated the weight of Available for Sale (AFS) and Hold to Maturity bonds (up to maturity) as a percentage of deposits to understand capital sensitivity. Looking at Europe, Held to Maturity bonds represent around 10% of deposits.

Why are we still neutral?

- In our top-down sector analysis, the most sensitive banks to a hypothetical 1% decrease in bond prices due to an increase in interest rates concern KBC Group with a potential 36 basis points downgrade on the CET 1 ratio. There is also Banco BPM with 30 basis points (that we cross-covered with Credit Agricole ), and Erste Bank that might be impacted by 22 basis points. For this reason, we recently decided to downgrade Erste Bank;

- Available-for-sale bonds are also equivalent to 10% of total deposits but, we believe are less problematic. Although government bonds lost 18% in value in the Eurozone and 12% in the United States, year-to-date bond movements imply a 0.05% gain in Europe. So, we expect a limited impact on capital from bond moves in the first quarter. Despite that, a 1% decline in AFS will deteriorate the CET1 ratio of KBC Group NV by 44 basis points;

- The bank CEO recently reiterated a 3-4% volume growth outlook in 2023. In the Belgium market as well as in the Czech Republic, mortgage volumes are cooling off;

- Given Ireland's disposal and RBI Bulgaria's acquisition , KBC's portfolio composition is not the same. RBI integration is expected within 18 months and our banking player is moving forward to mitigate inflationary cost pressure with investments in technology. According to our calculation, this would imply a 1.5% productivity gain which might be difficult to achieve.

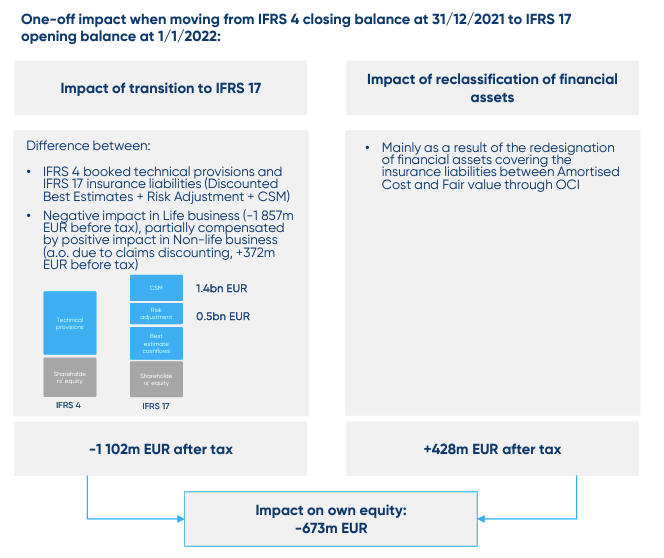

IFRS17 implication and Czech Bank Tax

As a reminder, KBC is a bank-insurer entity, and as a consequence of IFRS17 implementation, the bank is integrated with the new regulation. Indeed, KBC restated its figures and there is an impact of €673 million on the equity side (fig below). Despite that, the company confirmed its dividend policy and capital distribution. IFRS 17 does not impact the company's short-term & long-term guidance and there was no restatement of the CET1 ratio.

{kind=link}

On the negative side, the KBC Czech division recorded a €121 million post-tax legal charge. Well, we are not surprised given the fact that, during the FY analyst call, the CEO made some comments on the Czech banking impact. And he explained that tax charges will be very limited. This is happening of a windfall tax decided by the Czech government . In our numbers, we are estimating a lower tax on 2023 numbers, this is due to a higher provision in the region and lower earnings driven by higher expenses.

Conclusion and Valuation

Aside from the HTM and AFS consideration, KBC is a solid bank and this is demonstrated by its Common Equity Tier 1 and Solvency II ratio. KBC has also ample liquidity buffers with 84% of the deposit book related to small-medium enterprises and retail clients, while the rest is related to corporates. In detail, 48% of deposits are insured and below €100k. However, another risk to consider is its sizeable exposure to the Benelux mortgage market (which still is a relatively high-quality asset class, even if spreads will likely be volatile going forward). Despite some potential further hiccups in the short term, the company looks quite solid, and our internal team would not have concerns about its balance sheet. KBC Group NV business is sensitive to bond yields, with falling long-term yields being harmful to earnings and value. Also, the company is exposed to translation risk in respect of adverse US$/Euro movements. Last time, we decided to raise our 2023 EPS estimates by 20%, and we also adjusted the KBV cost of risk. Therefore, we are not changing our 12-month visible period forecast, and we reiterated our neutral valuation of €68 and $36.5 per share respectively. In addition:

- Despite KBC Group was a 2020 top pick ; however, we believe that the bank valuation looks full . In detail, the Belgian bank is currently trading at a premium on its TBV at 1.38x and an implied Return on Tangible Equity above 17%. As a reminder, the EU banking sector is trading at an average TBV of 0.8x. For this reason, here at the Lab, we suggest re-entering into BNP Paribas and Intesa Sanpaolo ;

- CET1 ratio is in the first quartile in the EU banking sector with a fully loaded ratio at 15.4% (and also a Liquidity Coverage Ratio at 152%). On the bancassurance, the SII is at 203% (above the 180% minimum capital requirements from the EIOPA). These ratios will provide a margin of safety for uncertain future times;

- In addition, KBC is yielding 6.25% versus BNP, ISP, and SocGen which are at 7.06%, 10.12%, and 8.18% yield respectively.

Here at the Lab, we believe other banks are better positioned to deliver higher shareholder remuneration and potential capital upside.

For further details see:

KBC Group: Impressive But Expensive