KBCSF - KBC: Valuation Looks Full

Summary

- KBC delivered a solid Q4 result supported by NII development.

- The bank scored a solid CET1 ratio coupled with its 203% Solvency II ratio in the insurance business (higher than the EU regulatory requirements).

- KBC is currently trading at a premium valuation on its TBV, so we decided to lower our rating to neutral.

A few years ago, here at the lab, we provided a top-down analysis of the EU banking sector, emphasizing quality names and cherry-picking banks in our European universe coverage. Our analysis was based on 1) a bank-assurance business model with a dominant market position, 2) solid fundamentals supported by a superior CET1 ratio compared to closest peers and a focus on cost/income ratio evolution, and 3) a tasty dividend per share. KBC Group NV ([[KBCSF]], KBCSY ) was our local champion and for the above reason, we decided to initiate to cover the bank with a clear buy rating .

Mare Evidence Lab's previous publication

{kind=link}

Since our analysis which was released in May 2020, the bank's stock price appreciation (including its dividend per share) was a plus 94% compared to an average S&P 500 return of +40%.

Mare Evidence Lab's previous publication

{kind=link}

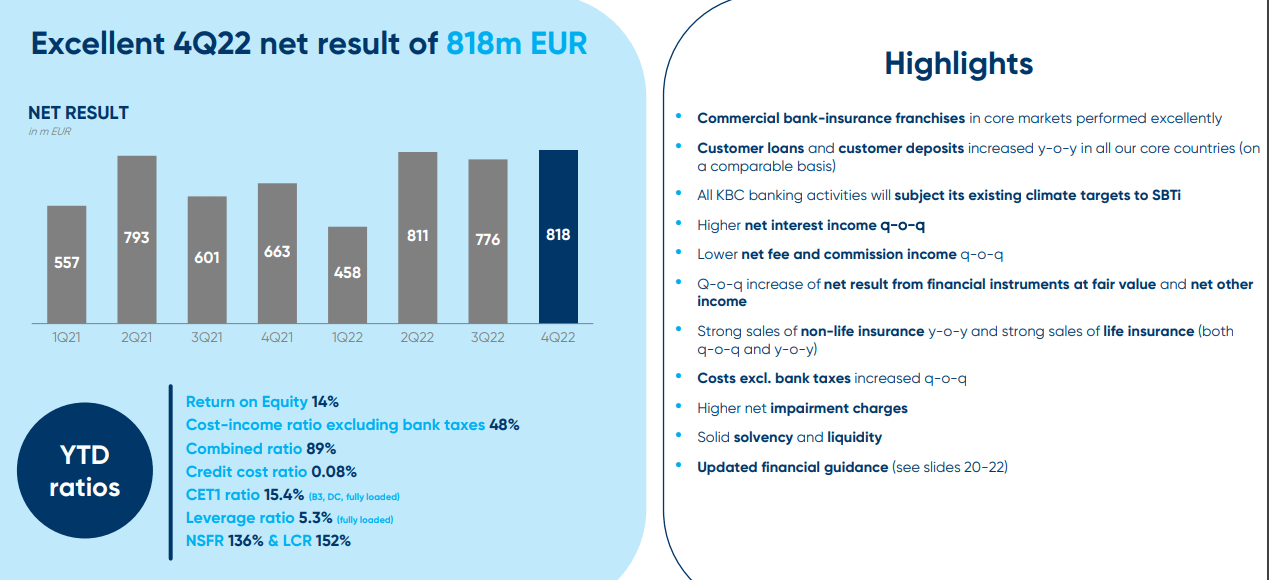

Today, we are back to comment on the Belgian banking major. Last week, the company released its financials with a net profit of €818 million compared to Wall Street analyst estimates of €708 million. Net interest income was stronger than anticipated and fully offset the higher operating costs. The bank confirmed its solid capital position with a CET1 up by 0.4% on a quarterly basis at 15.4% (vs. consensus at 15.0%). Still related to KBC's solvency, in the insurance business, the company has a safe SII ratio of 203%.

KBC Group financials in a Snap

{kind=link}

More in detail, KBC's net interest income reached €1.4 billion thanks to higher rates, while fee income generation was lower than anticipated due to lower performance in the company's AuM. Insurance income was also decremental, this was mainly due to higher normal claims. KBC's combined ratio stood at 89% confirming a solid performance versus other insurance players. Important to note is also the impairments evolution which stood at €132 million, including €25 million related to the Hungarian loan losses. Looking at our buy target summary, KBC's 2022 cost/income ratio amounted to 54%; however, excluding all bank taxes and a few non-operating items, the ratio stood at 48%.

On the Q&A analyst call, KBC's top management provided important details to model the bank's profit over the next three-year period. Here are the main highlights:

- For 2023, net interest income new guidance is expected at €5.7 billion (vs consensus at €5.5 billion) with top-line sales at €9.4 billion (vs consensus at €9.0 billion). In the new 2022-25 outlook, KBC is forecasting a sales CAGR of 6%;

- Aside from NII evolution, with a fully integrated business model, the company also expects earnings growth driven by its non-life insurance division supported by its low Combined Ratio;

- While OPEX CAGR is set at 1.8%, with a cost outlook that assumes to stay flat at €4.4 billion thanks to cost-savings initiatives, higher efficiency improvements, and lower AML costs. In addition, equity research analysts were forecasting lower expenses at €4.3 billion;

- 2023 credit costs are set at 20-25 basis points below the TTC rate. This is due to no material portfolio deterioration and a better macroeconomic outlook.

Conclusion and Valuation

Following the management indications, we decide to raise our 2023 EPS estimate by 20%, adjusting also for the higher cost of risks expected on macro uncertainties and emerging risks, while we are lowering our 2024 EPS by 8% (with a consequent mismatched on a higher cost of risks vs management expectations). Here at the Lab, we believe that the EU will face a crisis, and banks will suffer write off on higher non-performing loans and higher unlikely to pay evolution. Our new 2025 financials already implied a conservative 5% top-line sales CAGR and a 3.5% cost CAGR over 2022-25. As already mentioned, the CET1 ratio reached 15.4% and was helped by its internal insurance dividend payment that fully confirm Mare Evidence Lab's thesis. In addition, there will be no impact of IFRS17, and more important the bank still intends to manage its dividend payment in accordance with its CET1 ratio evolution.

For this reason, the company announced a dividend payment of €4 per share and will distribute €1.4 billion of capital surplus (for the Ireland disposal). This is still subject to ECB approval and might be performed via buyback or a special dividend. Regarding the valuation, KBC is trading at a premium on its tangible book value at 1.7x with an implied medium RoTE at 17.5%. For this reason, we decide to move our position from a buy to a neutral rating at 68 and 36.5 per share in Euro and US Dollars (ADR) respectively. KBC's valuation looks full, and we suggest increasing position in the other two top EU picks: ISP and Credit Agricole. Here are our recent follow-up notes:

- Credit Agricole Q4 Earnings: A Solid Buy

- Intesa Sanpaolo: Record Year, Reiterating Buy

For further details see:

KBC: Valuation Looks Full