KBR - KBR: Good Growth Prospects And A Low Valuation

2023-11-07 10:46:00 ET

Summary

- KBR, Inc. is well-positioned to benefit from a strong order book and backlog levels.

- The company's revenue growth prospects remain healthy, with a good demand in defense, space, and intelligence end markets and secular trends such as the energy transition and decarbonization.

- The stock is trading at a discount compared to historical averages, making it an attractive investment with favorable growth prospects.

Investment Thesis

I previously covered KBR, Inc. ( KBR ) in May. While the company has reported strong results and order growth since then, its stock price has corrected due to the delay in starting and ramping up of the HomeSafe Alliance work. I believe this decline presents a good buying opportunity as KBR is well-positioned to benefit from strong order book and backlog levels in the near as well as long term. The company is seeing good momentum in defense, space, and intelligence end markets due to ongoing geopolitical instability which is driving demand for the company’s Government Solutions ('GS') services. Further, secular trends such as energy transition, decarbonization, and infrastructure modernization are supporting its Sustainable Technology Solutions ('STS') business. This should result in continued orders, backlog and revenue growth in the coming years. Moreover, while the HomeSafe Alliance project has seen some delays, it should eventually ramp-up over the next few years accelerating revenue growth.

On the margin front, the company’s margins should benefit from a mix shift towards high-margin STS business which is growing at a much faster rate compared to the GS business. Coming to valuation, the stock is trading at a discount compared to its historical averages. Considering the company’s favorable growth prospects and a low valuation, I have a buy rating on KBR's stock.

Revenue Analysis and Outlook

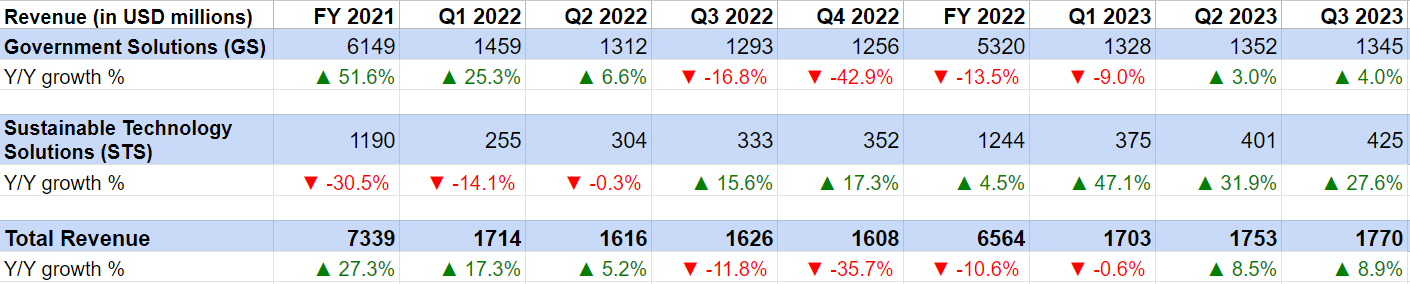

The company experienced robust growth in FY21 and 1H2022, with its GS segment benefiting from the Operations Allies Welcome (OAW) program. This program involved low-margin humanitarian work associated with the evacuation of U.S. military personnel and their allies from Afghanistan following the U.S. withdrawal. Subsequently, as this program concluded, the growth turned negative from Q3 2022 to Q1 2023. However, after the company surpassed its impact, growth has once again turned positive in recent quarters.

In the third quarter of 2023, KBR’s Government Solutions segment’s revenue increased 4% Y/Y attributed to new and ongoing contract growth in Science & Space, Defense & Intel, Readiness & Sustainment and International businesses. In the Sustainable Technology Solutions segment, revenues grew 27.6% Y/Y driven by rising demand in sustainable services and technology, particularly for its engineering and professional services and technology service offerings.

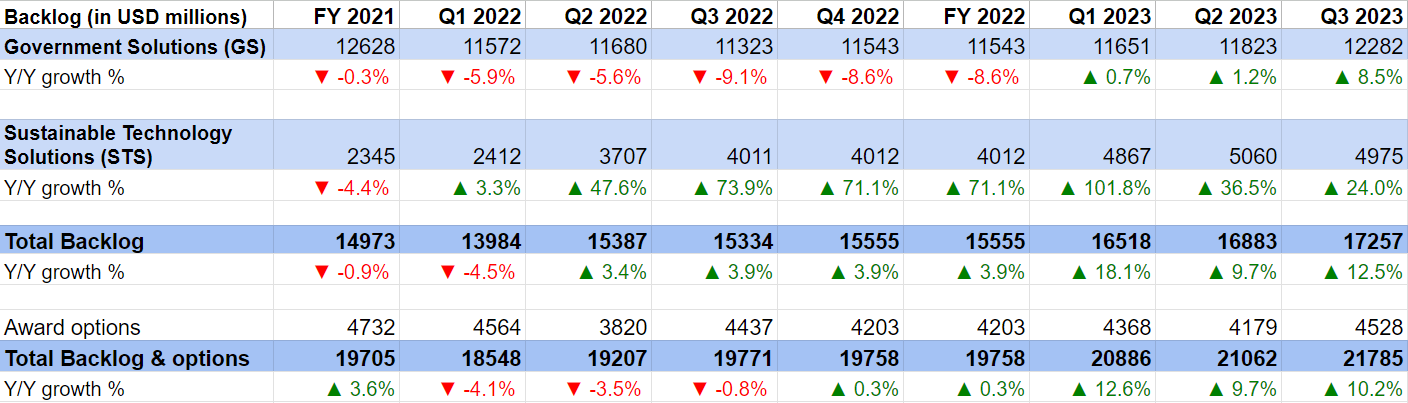

KBR’s Historical Revenue Growth (Company Data, GS Analytics Research) KBR’s Historical Backlog Growth (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Looking forward, the company’s revenue growth prospects remain healthy. The company ended the last quarter with 12.5% Y/Y growth in backlog. While the Government Services segment’s backlog was up 8.5% Y/Y, the STS segment saw a strong TTM book to bill of 1.3x and ended the quarter with 24% Y/Y growth in backlog. The company’s total backlog and award option increased 10.2% Y/Y and reached ~$21.8 bn. This strong order book provides a good visibility on the company’s revenue growth in the coming years.

The company’s end markets remain strong with good momentum in space, defense and intelligence driving the GS segment; while trending towards the energy transition, decarbonization and infrastructure modernization helped the STS segment.

The company’s leadership position in Ammonia Technology continue to help it with major projects and the company received several awards last quarter including the world’s first commercial ammonia cracking unit using KBR’s H2ACT technology in Daesan, Republic of Korea; an engineering, procurement and construction management (EPCm) contract for the modification of the Pluto Train 1 LNG facility to enable processing of scarborough gas and enhance life of the plant; and the blue hydrogen process technology and front-end engineering design (FEED) contract by EET Hydrogen for its hydrogen facility at HyNet, the largest blue hydrogen project in the U.K.

On the government side, the ongoing and recent geopolitical events have resulted in increased focus on defense spending across the globe as well as increased need for greater multi-government collaboration. With the company’s business engaged in high-end consulting services in critical areas of defense and intelligence across the globe, it is well-positioned to benefit from this trend and this is getting reflected in its order wins.

One area that has thus far disappointed investors within the GS segment and resulted in a significant correction in the stock price following the recent earnings is the HomeSafe Alliance project.

HomeSafe Alliance is a joint venture led by KBR and it won a TRANSCOM contract related to transporting household goods for the U.S. Armed Forces, DoD civilians, and their families in 2021. The contract has a ceiling value of ~$20 bn over the nine years.

The contract was initially delayed because of litigation and after a judgement in its favor in late 2022, KBR communicated its expectations about starting this project by end of FY23 and significantly ramping it up in FY24. However, there have been continued delays in starting this project and management now expects this project to start in Q1 2024 with uncertainty around how fast it ramps up. Management expects some clarity around it over the next couple of quarters and intends to communicate it to the street at the time of its next Investor Day (likely in May 2024).

While the stock has seen a meaningful correction post earnings as the expectations were high around this projects’ ramp-up in 2024 and management commentary disappointed investors, I am not too worried about it. The company’s healthy backlog and strong demand indicates that it should be able to grow its topline even without any contribution from the HomeSafe Alliance project. Even after lowered expectations post Q3 results, sell-side consensus is still expecting a healthy 13.18% Y/Y growth next year and these numbers include expectations around a slower ramp-up of the HomeSafe Alliance project. Further, this project is only delayed, not canceled. So, as TRANSCOM and KBR work to sort out execution issues, it should eventually ramp up over the next few years helping overall revenues. So, I am optimistic about overall revenue growth.

Margin Analysis and Outlook

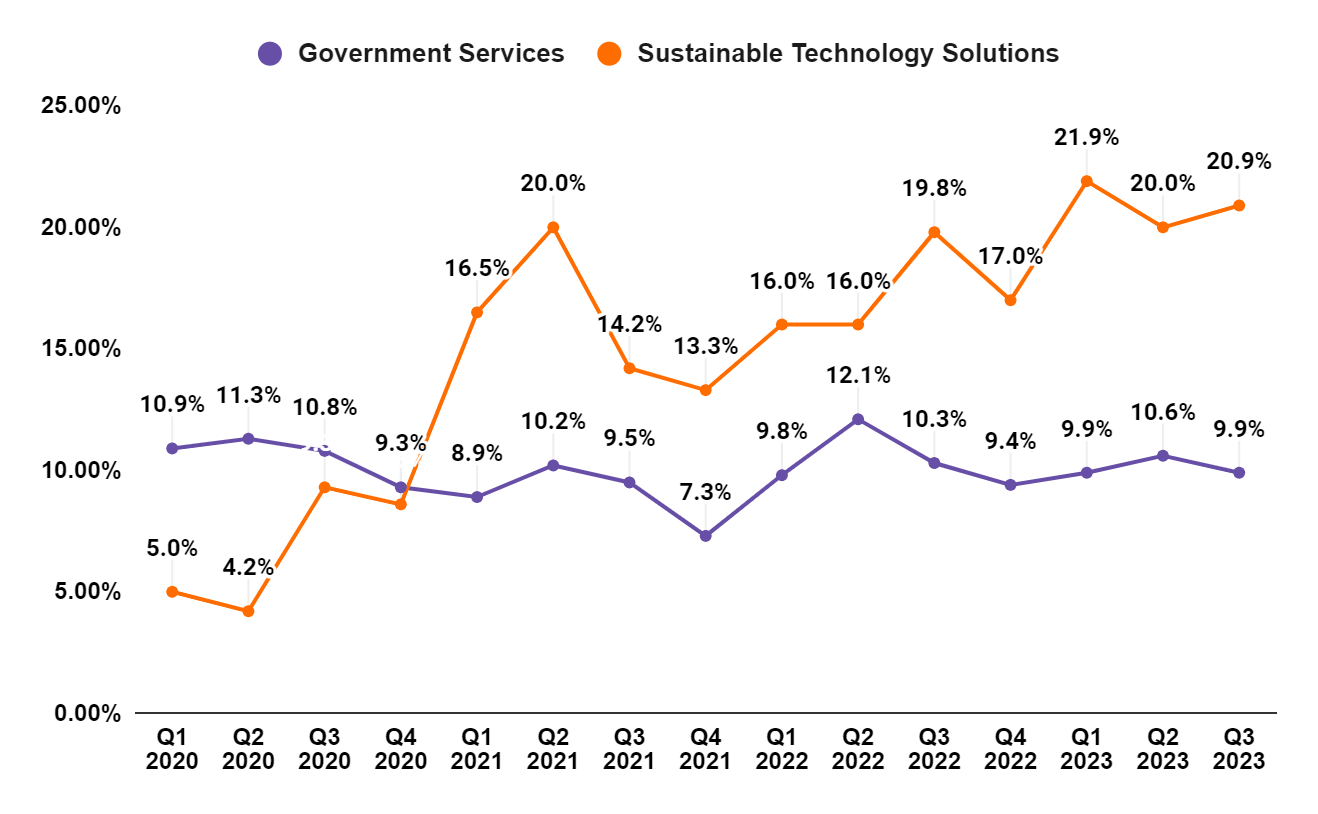

In Q3 2023, the STS segment’s adjusted EBITDA margin expanded 110 bps Y/Y benefitting from favorable revenue and licensing mix, which offset the 40 bps Y/Y decline in GS segment’s adjusted EBITDA margin. As a result, the consolidated adjusted EBITDA margin of 11% was flat Y/Y in the quarter.

KBR’s Segment Wise Adjusted EBITDA margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company’s margin should benefit from mix improvement as STS business which has higher margins is growing at a much faster pace than GS segment. Segment Wise, the growing demand for hydrogen as a clean fuel should continue to increase demand for the licensing of the company’s technology benefiting STS’ margins. For the GS segment I am expecting a flattish margin.

Valuation and Conclusion

KBR is currently trading at a 14.89x FY24 consensus EPS estimate of $3.41 and a 11.89x FY25 consensus EPS estimate of $4.27. This is a discount versus the company’s 5-year average forward P/E of 16.91x.

The current sell-side estimates are already below the $4.75 EPS target for FY25 that management communicated last year as the delay in HomeSafe Alliance project ramp-up is likely to cause them to miss their target. It is worth recalling that prior to the inclusion of the HomeSafe Alliance project's benefits, on its 2021 Investor Day, management had set a target of $4 in EPS for FY25 through organic growth, with the potential for additional upside from potential M&As.

If we take $4 in EPS for FY25 as the worst case scenario ignoring any benefit from the HomeSafe Alliance work, the stock is still trading at a ~12.50x P/E based on the current stock price of around $50, which still looks cheap. So, I believe after the recent correction, the stock is already pricing in this headwind. Given the company’s good growth prospects and low valuation, I have a buy rating on the stock.

For further details see:

KBR: Good Growth Prospects And A Low Valuation