KBWB - KBWB: A Great Buy In October But I'm More Hesitant Now (Rating Downgrade)

2023-12-08 06:49:29 ET

Summary

- The article evaluates the Invesco KBW Bank ETF as an investment option at its current market price.

- This is a sector that has seen a bull run since my last buy call. I am happy to see it, but it makes me less optimistic in the short run.

- Higher rates could persist, which can be profitable for banks and lenders. But if credit quality suffers, the net result may not be positive.

Main Thesis & Background

The purpose of this article is to evaluate the Invesco KBW Bank ETF ( KBWB ) as an investment option at its current market price. This is a sector-specific fund, with a focus on bank stocks exclusively. Importantly, it is heavily weighted towards the biggest banking names, and it is managed by Invesco.

As followers of this sector surely know, banking stocks faced a number of different headwinds in 2023. Most notable of them were some of the regional bank failures, and this took its toll on share prices across banks large and small. While some weakness was anticipated, I saw the above-average drops in some of the largest banks as a great buying opportunity. I believed that regional bank failures would actually make the biggest banks even bigger - helping to improve their profitability down the road. This led me to suggest buying KBWB back in October - and that was a great call in hindsight:

Fund Performance (Seeking Alpha)

This was certainly a welcome move and long overdue in my opinion! But while celebrating success is fun, we have to now consider what the forward outlook for KBWB is after such a big run.

Personally, I have concerns whenever I see a 20% pop in such a short timeframe (roughly six weeks). This makes me cautious as a rule, and there are other macro-forces at work that suggest taking some profit or being extra selective with new entry points is the right call here. Therefore, I will be downgrading my rating to "hold", and I will explain why in detail below.

Broader Market Concerns Are Relevant Here

To begin this review I want to highlight that I am getting cautious on most US equities as a whole right now. I have certainly enjoyed the run higher in funds like KBWB and others. It was a welcome move to see such strong gains to wrap up the year - especially after 2022's weakness. But my concern going forward is that the market is getting too optimistic.

This is for a variety of reasons. It seems the market is ignoring geo-political risks in the Middle East and Europe, the US (and other developed markets) consumers remain under pressure from higher borrowing costs, and - perhaps most importantly - investors are banking (pardon the pun) on Fed rate cuts in 2024. The last reason, rate cut expectations, is where I begin to disagree with the market. I think the Fed is unlikely to cut rates before mid-year, and then only if there are serious cracks in the economy. If that is the case, it won't really be "good" for bank stocks since there will be other headwinds to consider.

This is an important point because the run-up in US equities, banks included, has coincided with market expectations for a dovish Fed in 2024. The outlook shifted to cuts dramatically, and the S&P 500 rose in sync with that outlook:

Stock Prices vs. Fed Funds Rate (outlook) (Yahoo Finance)

{kind=link}

As you can see, the market's rate cut expectations have been a clear catalyst for higher stock prices. This is positive for those who already owned stock, but for evaluating new positions it looks to me like the market is a bit disconnected from reality. The Fed has not suggested rate cuts are coming any time soon, yet stocks are rallying on the prospect that they are. This leads me to believe that now is a good time to take some chips off the table - and a good place to start is in positions where I'm up 20% in just weeks - such as through KBWB.

Higher Rates Can Be Good, But Lending Volume Has Not Risen

The next topic to consider is that banking stocks and other financial companies tend to perform well when rates are higher. This means the general economic backdrop over the past couple of reasons has been favorable for lenders because when borrowing costs rise, they are often able to pass those costs on to their customers. While costs for deposits (bank expenses) also go up, those tend to rise at a slower and less dramatic level, improving net interest margins for lenders. This is central to why large-cap banks, the likes of JPMorgan ( JPM ), Bank of America ( BAC ), and Wells Fargo ( WFC ) have seen margins expand over the past few quarters. This is good news since these companies - and other large-cap banks - account for a large portion of KBWB's portfolio:

Top Fund Holdings (KBWB) (Invesco)

This begs the question - why wouldn't one continue to be bullish on bank stocks given that interest rates remain high?

The reason stems from the "all other things being equal" disclaimer. Higher borrowing costs are good for lenders when we assume every other variable is constant. But that is hardly ever the case. Lenders want to earn higher net interest, but they also have to contend with demand for loans and borrowing and creditworthiness. If demand dries up, it doesn't matter how much they can charge for loans if nobody wants one! Similarly, if credit quality suffers, then the net result may not be favorable. If someone borrows at a high interest rate but goes into arrears or default, the bank could be worse off than with a lower interest rate and on-time payments.

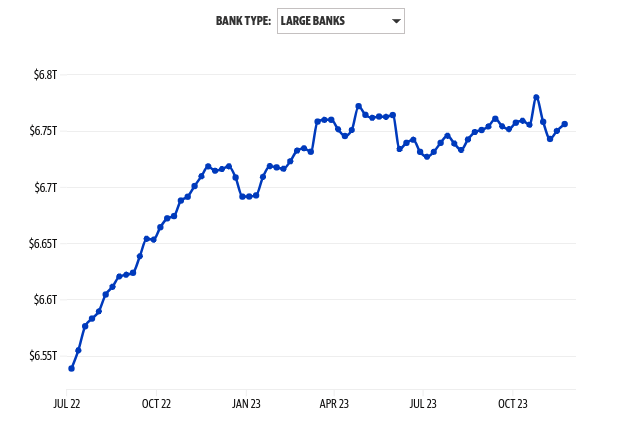

Hopefully, this makes logical sense because it points to one of my supporting reasons for downgrading KBWB right now. This is due to softening demand for bank services. If we look at total lending at large US banks, we see growth has only recently picked up by a modest amount - and it has been dropping in Q2 of the current year:

Lending Growth at US Banks (large-cap) (Federal Reserve)

{kind=link}

This is not meant to be alarmist by any means. This figure is not "bad" and it does show growth on a year-over-year basis. That is the good news. But it also shows that higher borrowing costs have taken their toll on businesses and consumers in the sense that they are borrowing less. Without loan growth, it will be hard for banks to continue to see earnings growth, and that limits the investment opportunity. If bank stocks had been performing sluggishly, then I would probably take the opposite position and say it is worth the risk. But considering KBWB's short-term move higher, I think metrics like this signal that there is merit to being cautious and not overly bullish at these levels.

Economic Growth Is Stalling

Another concern I have with bank stocks right now is how cyclical in nature this sector is. It tends to be tied very closely with GDP figures and economic growth - in both the US and abroad. The upside is that if the US and other developed markets continue to avoid a recession in 2024, then there could be more gains on the way. The other scenario is that economic measures disappoint and, if they do, they will likely take bank shares down with them.

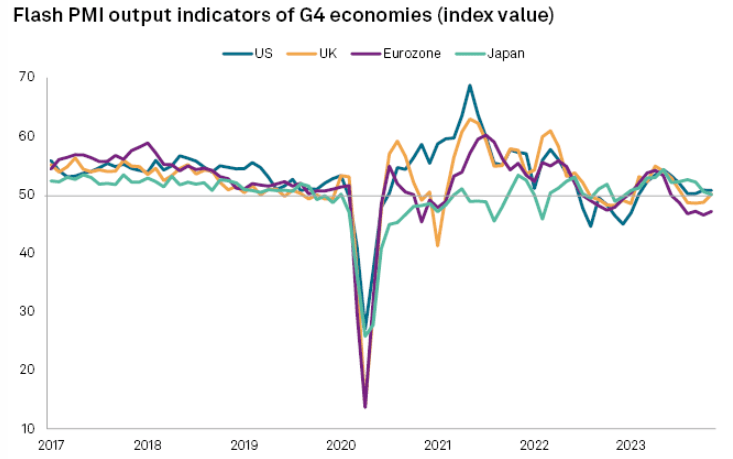

There is a valid rationale for this concern. If we consider PMI measures globally, we see that developed markets are fairly consistent in that growth has been muted:

PMI's (Various Regions) (S&P Global)

{kind=link}

By this metric, the Euro-zone is in contraction territory and the other developed regions are not faring much better.

This is another opportunity to manage expectations. Are these PMI figures very poor? Of course not. But they aren't great either and reinforce the disconnect between bank share prices and global economic conditions. This is just one more reason why I see some of the recent strength in bank stocks as a bit "too far, too fast". And when that dynamic occurs, patience is the name of the game for me.

Non-Performing Loans Another Headwind

My final topic for discussion reverts back to the lending aspect of US bank's books of business. This creditworthiness aspect is an extension of the idea I highlighted earlier - that higher rates are only one piece of the puzzle. If loans go bad - as many have started to - then net margins can take a hit even if borrowing costs have risen.

This is a definite watch item for me heading into the new calendar year because credit loss provisions are climbing quickly at banks large and small here in the US (and abroad). While this does not indicate loans have failed, it indicates management is anticipating these loans may not be collectible. That is a sign that more trouble could be ahead - and the stark climb in this figure is what concerns me the most:

Q3 Credit Loss Provisions (US Banks - Aggregate) (FDIC)

{kind=link}

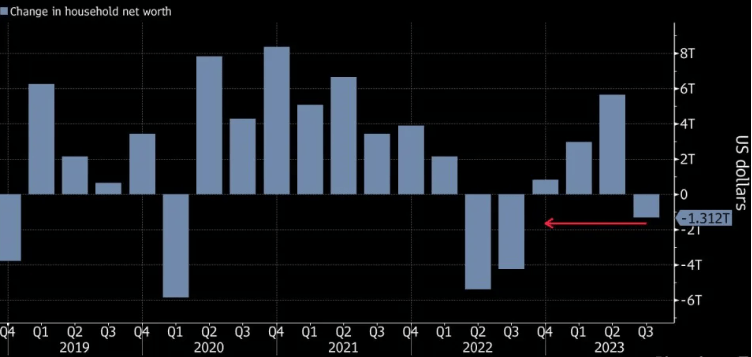

The issue I have here is there are multiple reasons for this increasing metric so we can't just hope to see improvement in one area and the problem will go away. There are under-performing commercial loans as the demand for commercial real estate declines due to a remote work environment. There is a challenging borrower backdrop because of higher borrowing costs - for both retail and business customers. Further, American households remain under pressure from both inflation and slowing wage growth. These factors, coupled with a rockier stock market, and culprits of the decline in American household net worth last quarter - another signal that more lending defaults could be in the cards:

Change in Household Net Worth (US) (Bloomberg)

{kind=link}

The takeaway for me is that all is not rosy beneath the surface. While it doesn't mean to automatically be a bear and/or avoid bank stocks, it does mean to be selective with positions and timing. This makes chasing a sector that has just seen a 20% pop to be a bit of an over-reach in my view.

Bottom-line

KBWB has seen a surge in its share price in recent weeks and, despite this rise, banking stocks as a whole remain under-valued compared to the broader market. This reality does suggest that being an outright bear on this sector probably is not appropriate:

KBWB Fast Facts (Invesco)

However, I do believe a downward shift in tone is warranted given the bull market run this ETF has had despite some challenging macro-developments. While elevated rates have allowed lenders to charge customers higher borrowing costs rates, this has hurt demand for mortgages and consumer lending - which make up a good chunk of the bank's core business. Further, bad loans are starting to cloud the outlook for many lenders, driven by a softening job market and a resilient remote work environment. Finally, stocks as a whole have been rallying on expectations for a dovish Fed - and I believe this sentiment is much too optimistic in the near term.

All of this adds up for me to say to take some wins where you can. KBWB has been a strong winner since my buy call, and I see holding off on new positions and/or taking some profit as the right move. That leads me to suggest "hold" is the right rating for the time being, and I urge my followers to be very selective with this fund going forward.

For further details see:

KBWB: A Great Buy In October, But I'm More Hesitant Now (Rating Downgrade)