KBWB - KBWB: Stress Test Cleared But Not Out Of The Woods Yet

2023-07-06 15:07:20 ET

Summary

- US banks have been a major laggard this year.

- While they have passed the Fed's stress test, more regulatory hurdles remain.

- At the current premium to book, the Invesco KBW Bank ETF doesn't scream value.

Having passed the Federal Reserve's stress test with surprisingly strong results and no major upward revisions to their indicative stress capital buffers (SCBs), the major US banks will be enormously relieved. That said, the sector isn't out of the woods just yet - recent H8 data revealed more deposit pressures across the banking system, while systemically important banks continue to lag on loan growth relative to the smaller-sized banks. As a result, net interest margin pressure will remain a key headwind into the upcoming quarter, along with the prospect of rising credit losses amid slowing customer activity and a looming US recession.

The biggest mid- to long-term concern remains the regulatory outlook, particularly for the global systemically important banks (GSIBs), all of which will be heavily impacted by the upcoming Basel III revisions. While the shape of the new capital rules is anyone's guess right now, the most likely scenario is significantly higher capital requirements, particularly for the big banks, impairing their mid- to long-term earnings power. At the current ~10% premium to its underlying book value, the GSIB-heavy Invesco KBW Bank ETF (KBWB) is probably fairly priced ahead of the Q2 2023 bank reporting season.

Fund Overview - Gain Exposure to a High-Quality US Bank Portfolio

The Invesco KBW Bank ETF seeks to track (pre-expenses) the performance of the modified-market cap-weighted KBW Nasdaq Bank Index, comprising a basket of publicly traded US banking stocks (including regional banks and thrift institutions). The ETF maintains a 0.4% expense ratio (mainly management fees) and a net asset base of $1.3bn, making it a competitively priced banking sector ETF.

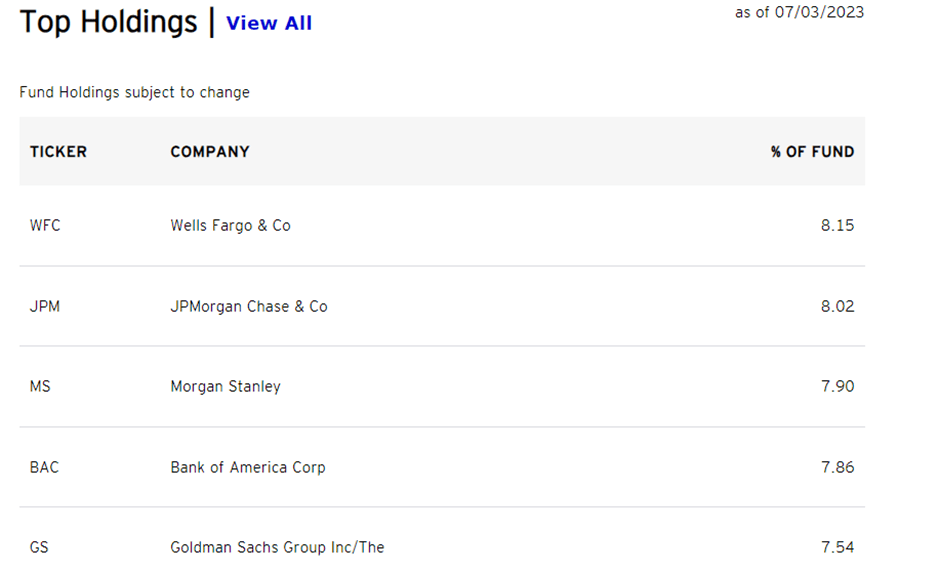

The fund's banking exposure is split across large-caps (51.9%), mid-caps (41.2%), and small-caps (6.8%). In line with the outsized large-cap bank holdings, the fund's largest single-stock allocations are to Wells Fargo (WFC) at 8.2%, JPMorgan Chase (JPM) at 8.0%, and Morgan Stanley (MS) at 7.9%. Rounding out the top-five list are Bank of America (BAC) at 7.9% and Goldman Sachs (GS) at 7.5%. No other bank holding in the 26-stock portfolio contributes more than 5%. With the five largest holdings (all GSIBs) contributing 39.5% of the overall portfolio, KBWB investors will need to be mindful of the concentration risk.

{kind=link}

Fund Performance - Steady Compounding and Distribution Through the Cycles

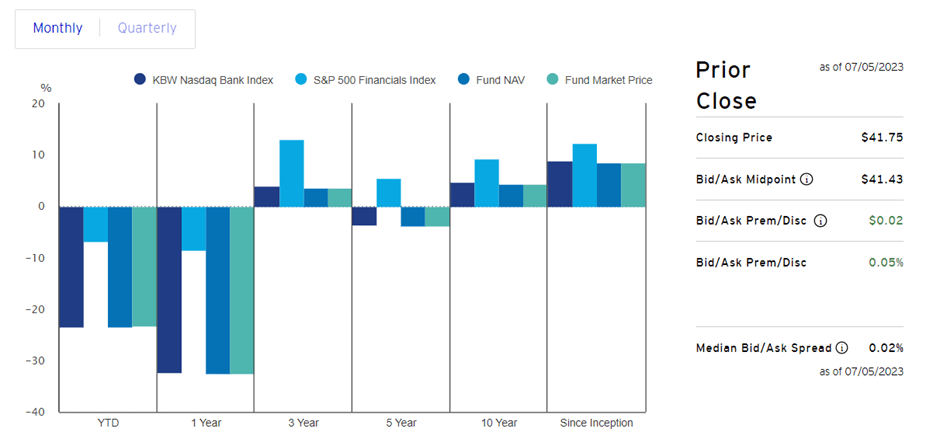

Per its latest reporting , the ETF has returned -23.4% YTD, underperforming the broader financials space (proxied by the S&P 500 Financials Index) by a wide margin. Zooming out from the last year, the fund has still compounded at an annualized +8.5% pace since its inception in 2011, though the track record over the last five and ten years has been less than stellar at -3.8% and 4.4%, respectively. KBWB does, however, maintain an impressively small tracking error vs. its benchmark KBW Nasdaq Bank Index - fund expenses account for almost all the <40bps annualized delta since inception.

{kind=link}

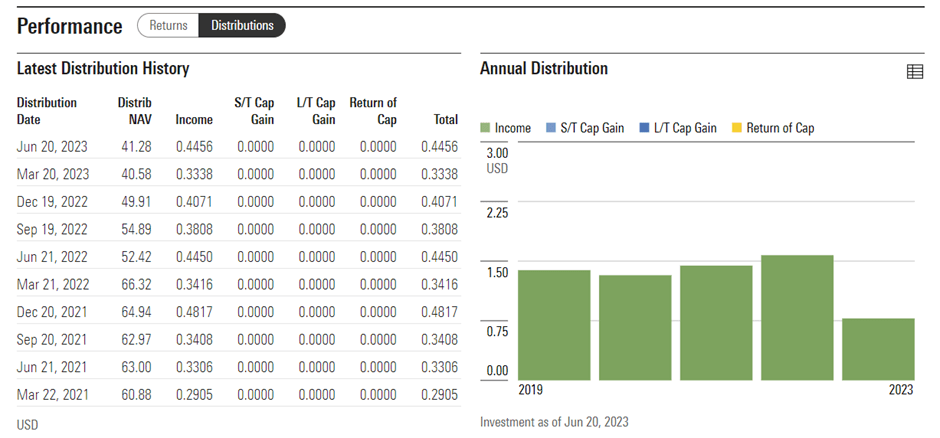

The fund's distribution outshines broader financial sector ETFs - supported by consistent capital returns from its bank holdings, the 3.8% yield will appeal to income investors. As I get into later in this article, there are some material headwinds on the horizon for US banks, though, which could weigh on their ability to pay out dividends at a similar rate. Hence, investors should be mindful of underwriting the current yield into mid- to long-term investment decisions.

{kind=link}

H8 Data Indicates Near-Term Margin Pressure Ahead

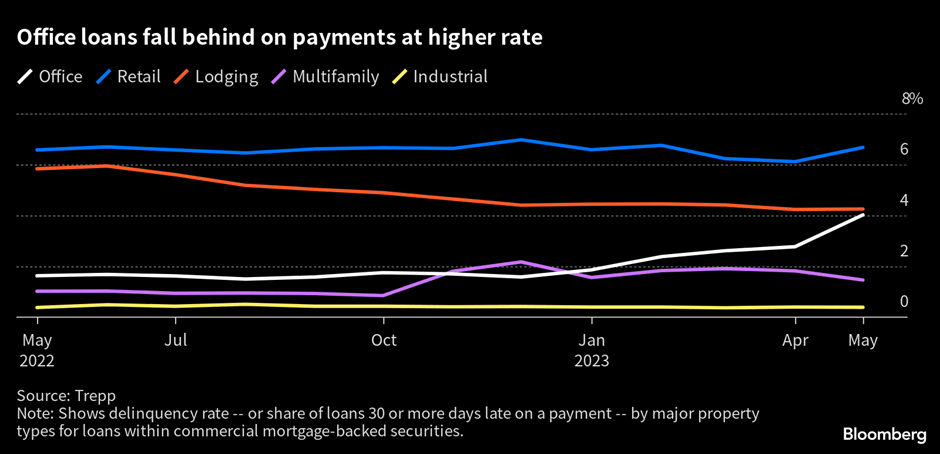

Per the Fed's latest H8 release (week ending June 21, 2023), industry loans continued to move higher at +7% for the year (non-seasonally adjusted). Large domestic bank credit (defined as the top 25 domestically chartered commercial banks) continued to lag, however, at +4% YoY (vs. +11% YoY for the domestic banks outside the top 25). The biggest divergence was in commercial and residential real estate credit, as well as home equity; the larger banks appear to be more conservative in terms of credit growth in these areas. Still, the continued growth in commercial real estate presents a material risk across the banking group, particularly in light of the recent spike in office-linked mortgage-backed securities delinquencies (up 125bps in May). And with more rate hikes in the pipeline later this year, the >4% delinquency rate (highest since 2018) for offices could get worse from here.

{kind=link}

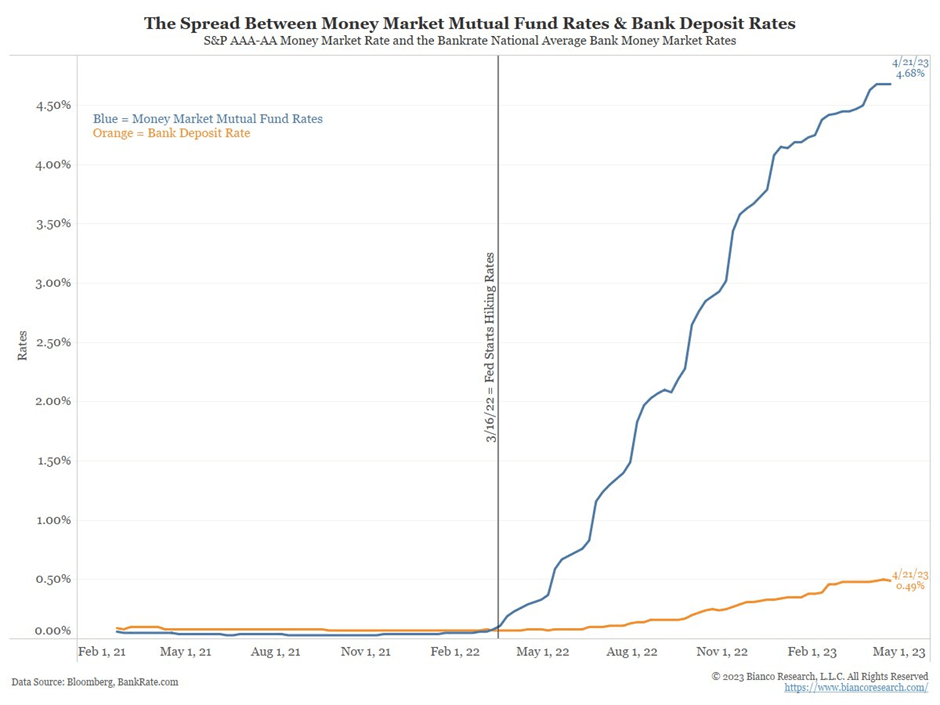

In contrast, the deposit base (non-seasonally adjusted) was down ~4% YoY, with total deposits now well below its 2022 peak. The erosion of confidence in the banking system post-SVB collapse has been a key contributor to the rising deposit betas; in the likely scenario this doesn't resolve anytime soon, deposit rates will likely remain pressured in the near term. Another key issue is the elevated money market fund rates at >5%, which has incentivized further deposit flight - note the money market fund to bank deposit rate spread (see chart below) is now at record-wide levels . And with Fed funds only heading higher from here, banks will need to reprice their offerings accordingly; given the limited offset on the lending side currently, net interest margins are likely to come under further pressure.

{kind=link}

More Regulatory Headwinds Post-Stress Test; Structural Earnings Power Headed Lower

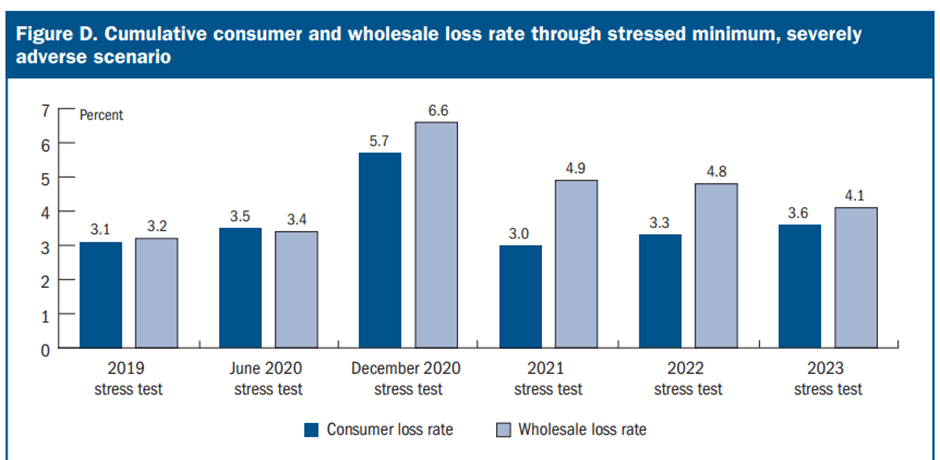

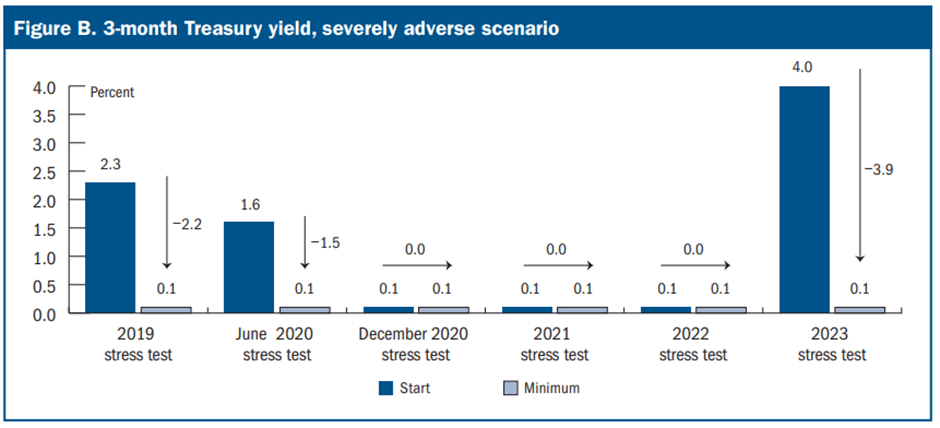

Over the last week, the key positive news from the banking space was that all banks had passed this year's Fed Supervisory Stress Test . This was a surprise, given the more pessimistic assumptions underlying this year's test, including steep GDP and property price declines. For the large banks, there was notable divergence - consumer-focused bank lending portfolios were more heavily penalized by the macro assumptions, with projected expense and provision growth also outweighing any net interest income offset. Hence, banks with large consumer books like Citi (C) and Capital One (COF) saw their stress capital buffers, calculated based on a bank's capital drawdown in a stressed scenario after applying a haircut for four quarters of dividends, revised higher.

{kind=link}

Somewhat ironically, banks that suffered the largest unrealized losses on their securities books benefited the most in terms of SCB requirements. This was largely due to the boost in portfolio value from declining rates (per stress test assumptions) more than outweighing the decline in interest earned on these assets, as well as the earnings hit at their lending operations. Given KBWB's top holdings, JPM, MS, and BAC, fall into this category; the ETF understandably moved higher post-release. That said, any benefit for the big banks from this year's stress test could well be unwound from future regulatory reform. The planned Basel III Revisions ('Endgame') will be key for the banks, as tougher capital and risk-weighted asset requirements are likely in the pipeline (especially for GSIBs). Also, worth keeping an eye on are shorter phase-ins or increasingly severe assumptions in future Fed stress tests in the post-SVB fallout; either way, I see more downside than upside to banks' future earnings power.

{kind=link}

Stress Test Cleared but Not Out of the Woods Yet

Investors will be relieved following the lack of major negative surprises following the Fed's latest stress test. While banks like Citi and Capital One were penalized for higher expected losses on their consumer loan books, there were positive rate-driven surprises from banks with large unrealized losses on their securities books, such as Bank of America. While there was no upward pressure on bank SCBs in aggregate, the results do not mean banks are in the clear. Ahead of next week's Q2 earnings reports, expect near-term earnings growth headwinds from NIM compression and credit losses as rate hikes start to bite. And beyond Q2, banks' earnings power will be hindered by regulatory headwinds, most notably from higher risk-weighted assets and capital requirements from the 'Basel III Endgame' implementation. So while the KBWB portfolio's 1.1x P/B screens cheaply relative to its 11% trailing ROE, the prospect of a structurally lower return profile means the ETF isn't particularly good value here.

For further details see:

KBWB: Stress Test Cleared But Not Out Of The Woods Yet