KBWB - KBWB: The Hammering Of Banking Stocks Presents An Opportunity

2023-10-23 03:31:12 ET

Summary

- The article evaluates the Invesco KBW Bank ETF as an investment option at its current market price.

- I shifted to a bullish stance on the banking sector after the sell-off in the first half of the year but was too early as large banks continued to decline.

- Despite poor stock performance, I believe there is inherent value in the fund as banks have had strong earnings and net interest margin growth.

Main Thesis & Background

The purpose of this article is to evaluate the Invesco KBW Bank ETF ( KBWB ) as an investment option at its current market price. This is a sector-specific fund, with a focus on bank stocks exclusively. Importantly, it is heavily weighted towards the biggest banking names, and it is managed by Invesco.

This is an area I was cautious on when 2023 got underway for a variety of reasons . But the sell-off in the sector got to be so intense that I shifted to a bullish stance not long after to take advantage of lower prices. The net result ended up being that I was too early - as large banks had further to fall:

Fund Performance (Seeking Alpha)

Clearly, the past six months have not been kind to the banks that make up the KBW bank index (which KBWB tracks). But with earnings season underway and most of the largest banks posting fairly decent numbers, I thought it was time to take another look at this fund. Simply, there seems to be a disconnect between actual company performance and stock performance, which piques my interest. I think there is inherent value at these levels which makes me reluctant to downgrade this fund. Therefore, I will be keeping my "buy" rating in place and will explain why in detail below.

Let's Recap: 2023 Has Been Miserable For Banks

To begin I want to take a moment to manage expectations here. I personally see value and have a willingness to plow some cash into this sector in the hopes that a turnaround is forthcoming. But this idea may not be for everyone. There is a lot of inherent risk - and this calendar exemplifies that very clearly:

YTD Performance (KBWB) (Seeking Alpha)

Banks have been a major pain point for a lot of reasons in 2023. Concerns that interest rates (which normally can help the sector's margins) are moving too fast are stifling loan and mortgage demand. Fewer loans can often result in lower profits - even with higher rates on each loan written. Further, slowing economic growth and continued fears of a recession are punishing cyclical areas. That includes banks, both large and small.

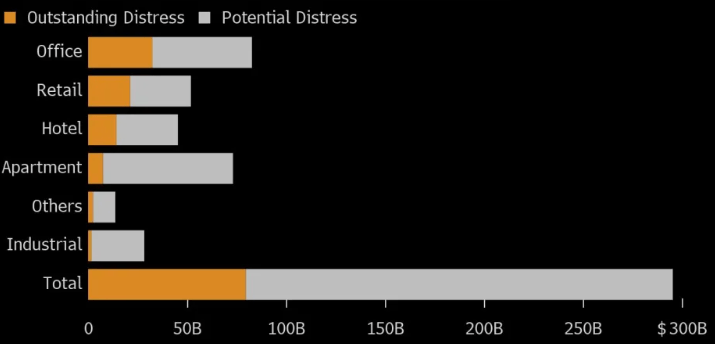

Finally, we are starting to see cracks in the commercial real estate market. This is an area many large banks have a lot of exposure to. The number of distressed properties - and the value of them - keeps rising. That is hurting the forward outlook for banks if they have to realize losses on these investments:

Real Estate Distress Levels (Bloomberg)

{kind=link}

What I am trying to convey here is I am not suggesting this is not a risk-on play. The banking sector - in the US and globally - has a lot of challenges right now. I am not a pumper of any investment idea - whether it be a stock, fund, or sector. So while I like the backdrop for banks at these levels, I am upfront in saying there is plenty of risk and a 30% draw-down in the sector does not automatically mean gains are on the way. Losses could continue for the reasons I noted in this paragraph, so weigh this carefully before buying.

Top Banks Are Seeing Margin Improvements

Now let's get to some of the good news. One aspect I like about this sector is how it is able to benefit from rising interest rates - something that is unique for it compared to many other areas like Tech, Utilities, or Retail. The largest banks are actually benefiting from this higher rate environment, which has seen the 10-year rise to the 5% mark (something that the new investor generation may just be seeing for the first time!):

10-Year Treasury Yield Curve (Federal Reserve)

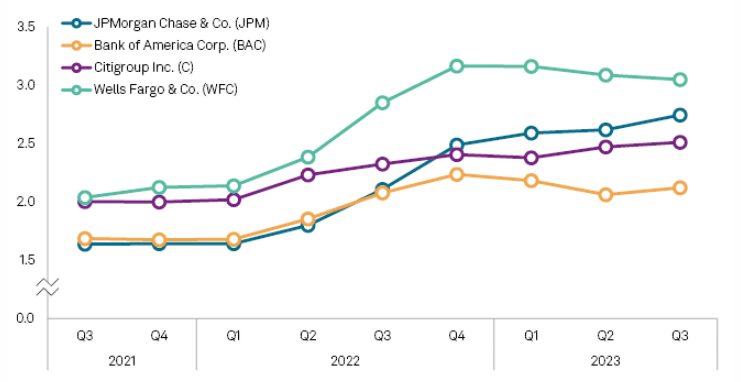

This relates back to banks because, as lenders, they have been able to increase what they charge for loans and other services. Typically, banks will increase their loan rate at a faster pace than the rates they offer for savings accounts to their customers. The net result is interest margins improve, and that is precisely what the Q3 earnings round has shown us across the largest US financial institutions:

Net Interest Margin (Big 4) (S&P Global)

{kind=link}

This helps to justify a bull thesis because there is underlying strength in a key attribute for banks. Margins are improving - and with rates staying higher for longer - this is a theme that should continue into Q4 as well. And as a reminder, these four banks combine to make up a substantial part of the overall KBWB portfolio:

KBWB - Top Holdings (Invesco)

That is a development that helps to offset some of the challenges facing this sector - especially for the four banks that represent 30% of the KBWB ETF. This is a critical reason why I don't see a need to downgrade my outlook at this time and to keep the buy rating in place.

Value Gap Clearly In KBWB's Favor

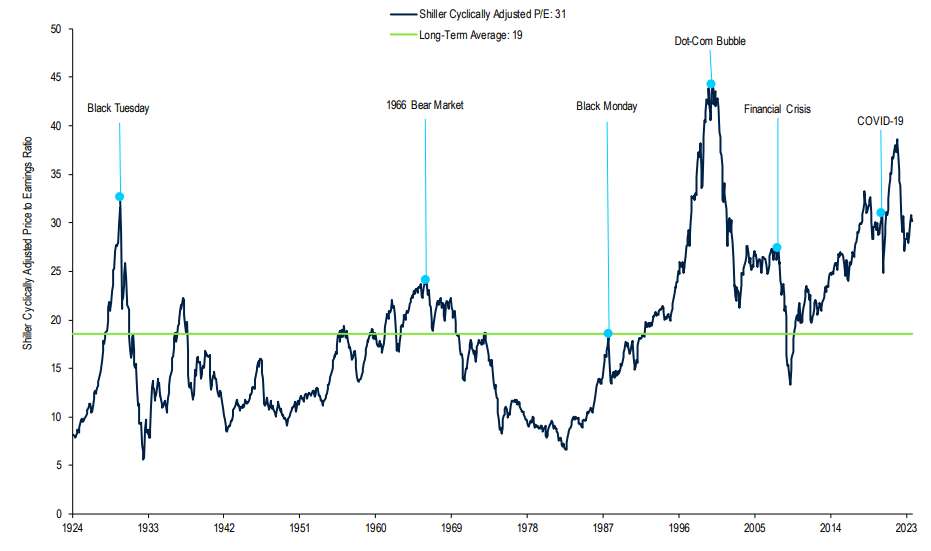

My next topic looks at the broader equity market with respect to valuations. It should not be a shock to readers to know that equities are not exactly in bargain territory. While valuation levels have been higher in the past, equities - as measured by the S&P 500 - are trading markedly above their long-term average when it comes to two key metrics:

Equity Valuations (as measured by S&P 500) (Vanguard)

{kind=link}

This reality makes me generally cautious on putting down cash into the broad market or large-cap ETFs at this point in time. I see an environment where we have to be more selective as investors since Tech valuations are pushing US indices up to levels that will require strong earnings going forward to justify them.

By contrast, the banking sector is not participating in this P/E surge. While the top banks are seeing reasonable earnings come in, their share prices are tumbling (as mentioned earlier). This has led funds like KBWB to trade at levels that look quite enticing compared to the S&P 500 (and other indices):

KBWB Fast Facts (Invesco)

I will emphasize again that this is not a "sure thing". A stock or sector being "cheap" - whether in isolation or relative to the market - doesn't automatically mean anything. Bank stocks have looked like bargains for most of 2023 and we all know what that has meant so far. So while I think this is a reasonable time to start building/adding to positions, valuations can take a long time to normalize or recover. Do the large banks look cheap here? Yes - and I see that as a buy signal. But recognize this is not the only attribute to consider.

A Reasonable Idea For Income

Another positive aspect of KBWB is the yield. While I would hesitate to call most equity ideas "income" plays given where the treasury yield stands and how high inflation is, everything is relative. At over 4%, KBWB definitely stands out as an income play compared to other equity sectors. This includes even Energy and Utilities, which are traditionally some of the highest-yielding sectors:

KBWB's Yield (Invesco)

Of course, a 4% boost to income doesn't mean much when an ETF drops 30% in a year. So, again, this is only a useful aspect if the share prices hold up well. Losing capital while earning income isn't a great proposition over the short or long term.

But the good news is that the dividend suggests underlying health, in a way similar to the net interest margin. While the market frets about large banks and punishes their share prices, banks keep delivering on metrics that count. In the case of the dividends, KBWB has managed to increase its payout on a year-over-year basis. This, in turn with the declining share price, is why the yield stands above 4% at the moment:

| Q3 Distribution - 2022 |

| Q3 Distribution - 2023 |

| YOY Growth |

| $.38/share |

| $.405/share |

| 6% |

Source: Invesco

The bottom-line is KBWB (and the banking sector by extension) is a place that my followers can go to get above-average income and below-average valuations. As a dividend seeker and value-oriented investor, it should be clear why it's on my radar.

Getting Serious About Cost Cutting

The next topic for discussion is that banks are taking aggressive actions to lower their expenses. While not "good" for those impacted and perhaps the broader labor market, large banks in particular are shedding jobs in a meaningful way. This, in addition to lowering their office and retail footprint, is helping to keep costs down in a challenging market environment. I view this discipline favorably as an investor - and expect this trend to continue into 2024 with almost certainty:

Headcount at Top Financial Institutions (Reuters)

{kind=link}

What I see here is management groups across the sector taking action to help their companies remain competitive in a difficult macro-environment. This is a trend playing out in other sectors as well - such as Tech and Consumer-oriented firms - and I welcome these moves. After years of being saddled with workforces that were too large and inefficient, large banks in particular are making the correct moves here to right-size their headcounts. As an investor, this is long overdue in my eyes and helps me get bullish in an area where I started the year off cautiously.

We Aren't Out Of The Wood

My final thought is to keep an eye on the broader banking sector when evaluating this investment. While I believe large US banks remain some of the safest companies in the world - due to the size, implicit government support, and large cash reserves - their share prices can still be rattled by weakness elsewhere in the sector.

Think about earlier this year when a handful of US banks went bankrupt. Did large-cap banks get punished by this? Absolutely - even though these firms may have benefited by bringing on clients/accounts and looking relatively healthier as a result. Despite not being truly impacted by the failures at First Republic ( FRCB ) and Silicon Valley Bank (SIVBQ), the share prices took a nose-dive anyway because the whole sector came under scrutiny. Whether that was justified or not (and I think it wasn't), it happened all the same.

So, why does this matter now? Because there still remains a major cloud over many US and global banks in terms of their safety and soundness. If these weaker institutions end up seeing a similar fate as FRCB or SVB, then watch out:

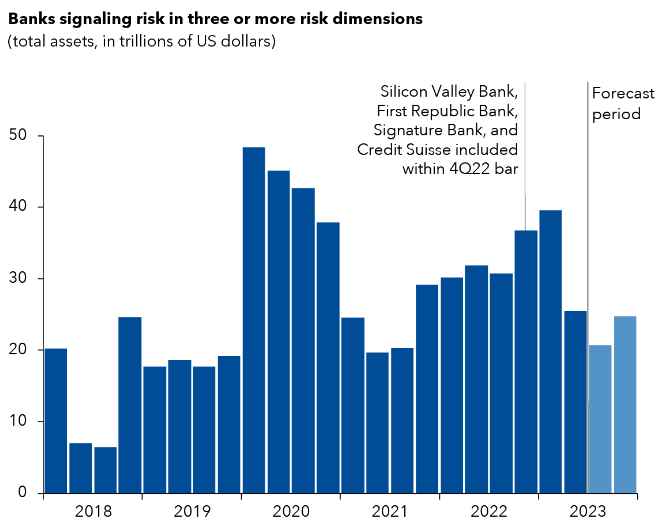

Number of Banks "At-Risk" (IMF)

{kind=link}

This is where macro-forces will likely come into play. If the US - and the world - can avoid steep recessions, then I think the banking sector rallies from here. But if economic growth disappoints and the Fed and other central banks maintain restrictive growth policies, the banking sector could be set up for further trouble.

With a large number of banks already "at risk" by global standards, it won't take much to tilt them over the edge. If that happens the entire sector will feel some short-term pain, similar to what we saw in Q1 this year. While it may not seem fair, it happens all the same, and this remains a major headwind going forward.

Bottom-line

KBWB has had a rough go of things and it would be easy to throw in the towel here. But with a cheap valuation, a growing income stream, and much of the worst behind it (in my view), I see an opportunity here. The largest US banks have gotten serious about cost cutting, their net interest margins have improved, and their share prices have been beaten down to the point where a lot of bad news is baked in. In this environment, the contrarian bell signal goes off in my head and I become a buyer. Therefore, I believe the "buy" rating on KBWB is justified, and I suggest to my followers that they give this idea some thought at this time.

For further details see:

KBWB: The Hammering Of Banking Stocks Presents An Opportunity