KBWY - KBWY: A Highly Speculative High Yield Play

2023-10-02 16:31:35 ET

Summary

- Invesco KBW Premium Yield Equity REIT ETF has a high dividend yield of 9% but is considered highly speculative and risky.

- The fund invests mainly in traditional REITs, not mREITs, and achieves its high yield by investing in troubled companies with crashed stock prices (mostly small caps).

- The fund's performance has been poor, with a negative stock price return of -41% over the past decade and inconsistent dividend distributions.

Invesco KBW Premium Yield Equity REIT ETF ( KBWY ) is highly popular among income investors due to its high dividend yield of 9%, but I find this fund to be highly speculative in nature and possibly too risky due to many of its holdings, which I will explain below.

The fund mainly invests in REITs and when you see the fund's high yield you might be inclined to believe that it invests in mREITs (mortgage REITs) which I already explained to be too risky in the past but as a matter of fact this fund mostly invests its assets into traditional REITs. It also doesn't use leverage and doesn't write covered calls either. Then where does the high yield come from? It invests into many companies whose stock crashed significantly because they may be in deep trouble, so this creates a high yield, but the yield might or might not be sustainable in the long run.

The fund's top holdings include Brandywine Realty Trust ( BDN ) which yields close to 8% but down more than 65% in the last 10 years, Global Net Lease ( GNL ) which yields 16% but pays more in dividends than it earns making its dividend hard to sustain, and a bunch of medical REITs and office REITs which may be at risk of cutting dividends. The fund holds only 30 stocks, and the top 10 stocks account for roughly half of its total weight.

Top 10 Holdings (Seeking Alpha)

The fund's performance in the last decade has been less than desirable with stock price being down -41% and total return being 17% which means it generated an average annual return of 1.6% for the last decade including reinvestment of dividends. This doesn't even keep up with the rate of inflation.

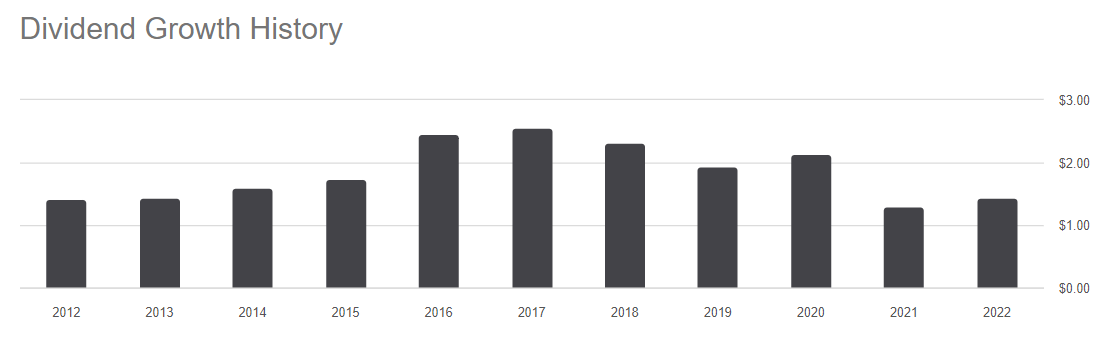

The fund's dividend distribution history has been somewhat sporadic, with some rises and falls through the years. In 2022, the fund distributed $1.44 per share in total distributions, which is only 2 cents higher than what it distributed ($1.42) a decade ago in 2012. The fund posted nice distribution growth from 2012 to 2017, but that seems to have marked a peak, and dividends have been lagging or shrinking annually since then.

{kind=link}

To be fair, REITs have been in a bear market since 2021 and most REITs got sold off during this period, with very few of them proving to be safe. As the Fed and other central banks around the world started hiking rates and reducing liquidity across the world, many income vehicles such as bonds, bond funds, debt instruments, REITs (both traditional and mREITs), and utility stocks suffered tremendously. During this time KBWY actually dropped less than the overall REIT index measured by VNQ in total returns, but it was still down 22.5% even after reinvestment of dividends, nevertheless.

Many investors would say that the best time to buy an asset or asset class is during a bear market because that's when most people panic and oversell their assets, which creates a value that is hard to come by any other time. Sooner or later bear markets reach a bottom and the next bull cycle follows, so it makes sense to buy an asset during bear markets, which I generally agree with, but you still want to invest in quality assets. Not all assets survive a bear market, and many assets could even face an irreversible destruction during bear markets. For example, you can see the long-term chart of a REIT fund ( REM ) in the past. Notice how it dropped so sharply in 2009 and never recovered from that over the years.

This is why it's important for investors and funds to stick to high-quality investments rather than chasing yield. KBWY looks like one of those funds that chases yield and invests into stocks with the highest yield, without paying much attention to anything else so that they can generate the highest distributions for investors; but this seems to result in meager total returns that can't even match the rate of inflation in the long run.

Also, notice that a lot of the stocks held by this fund are small caps in nature. Small caps tend to be riskier in environments like the current one we are experiencing today where liquidity is drying up, interest rates are rising, and it's becoming more difficult to roll debt because they generally have less access to capital to begin with, and their credit ratings tend to be less ideal as well which makes them more susceptible and vulnerable. Large-cap companies typically have much more resources and better access to extra capital, which makes it easier for them to ride out tough times, but small caps are not as lucky.

Less than a couple of months ago, we witnessed Medical Properties Trust ( MPW ) cut their dividend by nearly half in order to strengthen their balance sheet and increase chances of survival in this difficult environment. Prior to the cut, the stock had a dividend yield of 16% which resulted in many yield-chasers buying up the stock and suffering huge capital losses. The stock still has a high yield, but it's still not perfectly safe. This is just one example, and we may see more examples in the coming months.

Now, I am not saying that this fund will blow up or that it will crash and burn, but it is far more likely to underperform than outperform. The market's history tells us chasing yield rarely works well for investors in the long term, especially when it comes to smaller caps, which are far more fragile than large caps. Many of these stocks have a high yield for a reason because their stock crashed. When a stock has a high yield because its price crashed, many times, it's inevitable for the dividend to be cut as well because it is more likely than not that the company is in trouble.

Of course, my thesis could be wrong, and we could have a scenario where the economy experiences a soft landing which leads to a flat market performance for years, which would mean that high-yielding stocks would outperform the overall markets. This could happen within the realm of possibilities but unlikely to last for many years.

Having said that, I still see a lot of value in REITs overall after a 2-year bear market. Investors could start slowly buying a REIT index fund like VNQ if they have a long-term horizon and keep adding to their position if it dips further (not to mention reinvesting dividends). I absolutely wouldn't write off REITs as a whole (maybe with the exception of mREITs).

For further details see:

KBWY: A Highly Speculative High Yield Play