KBWY - KBWY: Revisiting This Risky REIT ETF After Rates Have Peaked

2023-12-15 16:06:55 ET

Summary

- Going into the monetary tightening cycle, KBWY had an unfavorable risk and reward profile due to its bias toward small-cap REITs and exposure to potential value traps.

- KBWY has performed poorly and has not recovered from losses in early 2020, but has done well compared to the overall REIT market recently.

- The future outlook of KBWY has improved due to more accommodative monetary policy conditions and major dividend cuts but is dependent on the path of SOFR in 2024.

- Given the huge dependency of KBWY's performance on how the interest rates evolve, investing in KBWY still seems too speculative for me.

As we were going into the Fed tightening cycle and facing huge uncertainty around the trajectory of future interest rates, I wrote an article on the Invesco KBW Premium Yield Equity REIT ETF ( KBWY ) highlighting a very unfavorable risk and reward profile.

There were two key fundamental reasons, which, in my opinion, rendered the ETF unattractive for relatively risk-averse investors:

- Bias toward small-cap REITs. Considering that KBWY's policy is to invest at least 90% of its AuM into small- and mid-cap REITs, there is per definition more elevated exposure toward companies which do not carry as strong balance sheets as large-cap peers. During times of restrictive interest rates and constrained access to financing, strong balance sheets are critical for the REIT sector (i.e., to maintain positive spreads between cost of capital and cap rates, and conduct successful refinancings).

- High risk of value traps. Given that KBWY allocates its assets based on dividend-yield weighting methodology, where a significant skew is directed toward higher-yielding REITs, the underlying risk profile is further increased. Again, in the high-interest environment, an exposure to relatively weak balance sheets and high-yielding stocks introduces an inherent focus on potential value traps.

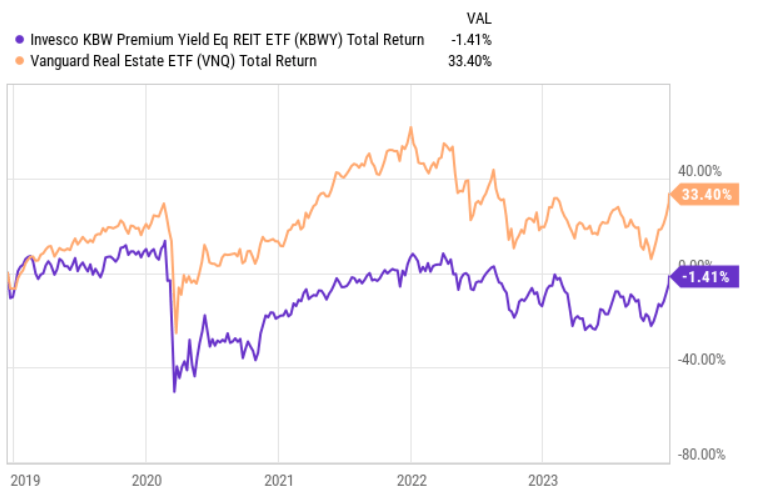

All in all, KBWY still has performed poorly starting from the period, when COVID-19 broke out.

{kind=link}

On a total return basis, KBWY has still not recovered from all of the losses registered in early 2020.

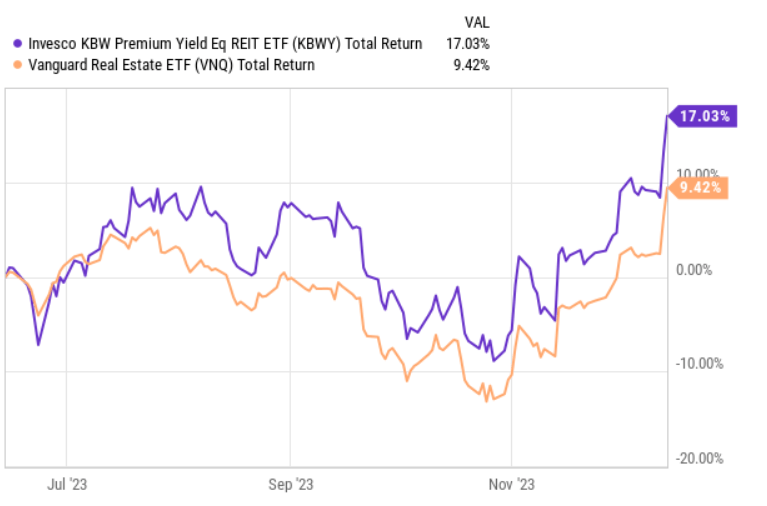

Yet, if we compare KBWY's recent performance to that of the overall REIT market, the picture looks totally different.

{kind=link}

We can see that since the market started to factor in a scenario of already peaked interest rates and a convergence back to the previous levels already in the foreseeable future, KBWY has done extremely well.

Thesis Update

Now the question is whether KBWY is positioned to capitalize on the declining interest rates, thus closing the performance gap from the broader REIT market that is still there since the pandemic years.

Here, the fact that ca. 40% of KBWY's portfolio is in the small-cap REIT space and ca. 55% in mid-cap REITs should stimulate a more pronounced recovery process.

{kind=link}

The explanation lies in the same logic as elaborated above. Namely, the less capitalized REITs should be greater beneficiaries of more relaxed financing conditions.

In addition, the concerns around 2024 and 2025 debt maturity walls consisting of pre-2022 assumed loans seem to be less pronounced, especially when it comes to the higher spread component. While new refinancings will still inflict damage on the underlying cash flows (as the previous low-rate loans are repriced to market-level interest rates), the extent of this seems to be lower, which again benefits more less capitalized REITs.

In terms of the sector allocations, KBWY still remains exposed to the riskier spectrum of the real estate segment simply because the valuations and dividend yields are higher there.

Invesco Distributors, Inc.

For example, healthcare and office REITs, which together account for more than one-third of the total AuM have been one of the major laggards in the entire REIT (or commercial real estate) space. Consequently, the falling inflation rate and a more realistic scenario of dropping SOFR in the near future should provide strong tailwinds for these two sectors to bounce back in a material fashion.

Reduced inflation is crucial for healthcare REITs to keep the NOI margins in check. Similarly, now that the uncertainty around how far the interest rates can go has effectively disappeared, some of the struggling office REITs now can experience improved prospects for deal transactions and fixed rate refinancings, which previously were very limited since the market did not have the necessary clarity (visibility) on how to price the capital.

{kind=link}

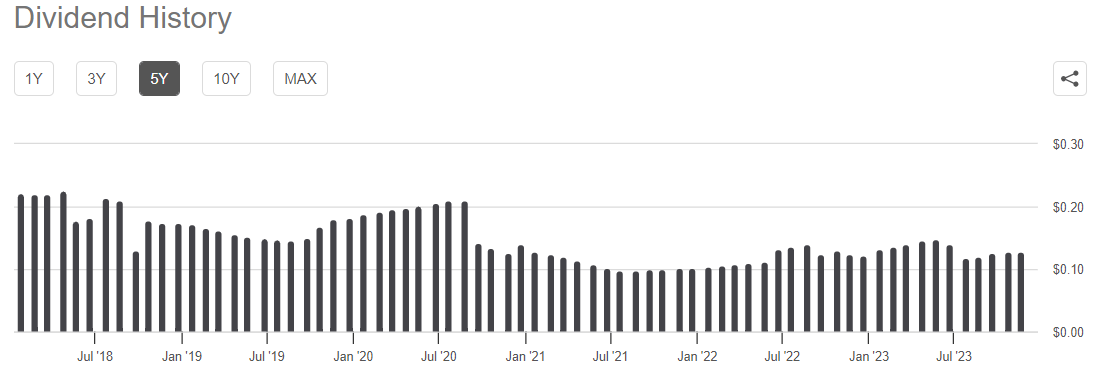

Finally, in the chart above, we can see how KBWY was forced to make a series of dividend cuts starting from mid-2020. Plus, almost half a year ago, there was an additional cut, which ended 5 months of increasing dividends in a row. This was driven by the overall reduction of dividend payouts, mostly in healthcare and office segments.

With that being said, it seems that KBWY has achieved one of its lowest points in terms of the monthly dividend distributions as the recent runup in the REIT valuations and more favorable conditions (directionality) in the monetary policy should help the underlying companies of KBWY to preserve their distributions (especially, against the backdrop of already recognized cuts and the recent data on improving FFO generation across the board).

The Bottom Line

All in all, considering the combination of more accommodative monetary policy conditions and a series of major dividend cuts already made by KBWY, the future outlook of KBWY has definitely improved.

At the same time, the entire thesis is fully dependent on the path of SOFR in 2024, where even the slightest deviation from the already priced-in cuts could send KBWY materially lower from where it is trading currently.

Lastly, as of now, KBWY offers a dividend yield of 8%, which is not that high in the context of the underlying risk profile (e.g., huge bias toward small-cap REITs located in fundamentally risky segments such as office and healthcare).

While the KBWY's overall prospects have indeed improved and the ETF is in a solid position to register further gains from the recovery process, the fact that there is so huge reliance on downward moves in SOFR (which are impossible to predict and where the market has been wrong many times) does not substantiate a solid buy for me.

For further details see:

KBWY: Revisiting This Risky REIT ETF After Rates Have Peaked