KCE - KCE: Why I'm Very Bullish On This Capital Markets ETF

2023-12-28 13:26:52 ET

Summary

- The market expected rates to be 'higher for longer' and capital market companies have guided based on this assumption.

- But the latest Fed's commentary suggests rate cut possibilities in 2024 and the market has started to respond accordingly.

- Rate cuts are expected to boost activity in the capital markets sector, via higher M&A, IPO, and trading activity.

- The equally weighted KCE ETF is recommended as a better way to play the sectoral tailwind compared to the concentrated IAI ETF.

Thesis

Changing sentiments on the markets' rates expectations fuel my very bullish view on the SPDR® S&P Capital Markets ETF ( KCE ):

- The market expected rates to be 'higher for longer'

- But the latest Fed's commentary suggests rate cut possibilities in 2024

- Rate cuts are expected to boost activity in the capital markets sector

- The equally weighted KCE ETF is a better way to play the sectoral tailwind

The market expected rates to be 'higher for longer'

Before December, the prevailing sentiment was for the Fed to hold rates 'higher for longer'. For example, the headline for S&P Global's November 2023 report on the Capital Markets outlook had this clause: "... despite notably higher rates". According to their outlook,

"bear steepening of the US yield curve have cemented that interest rates are likely to remain higher for longer"

Commentary from key capital market firms echoed this view. In the 2023 Global Sachs US Financial Services Conference, CFO Martin Small from BlackRock ( BLK ) - the world's largest asset management firm - noted a challenging environment amid high and rising rates:

...environment where beta has been a little less friendly over the last 2 years and rates are going to be higher for longer, which is what the Fed has told us.

Guidance communications from capital markets companies have also reflected a higher-for-longer rates assumption. For instance :

"So -- and so therefore, imagine that, that included scenarios that incorporated, obviously, the forward curve but clearly pausing for longer and also something that's higher for longer. So all of that was sort of contemplated in the guidance."

- JP Morgan's ( JPM ) Co-CEO of Consumer & Community Banking, Marianne Lake in the 2023 Global Sachs US Financial Services Conference

But the latest Fed's commentary suggests rate cut possibilities in 2024

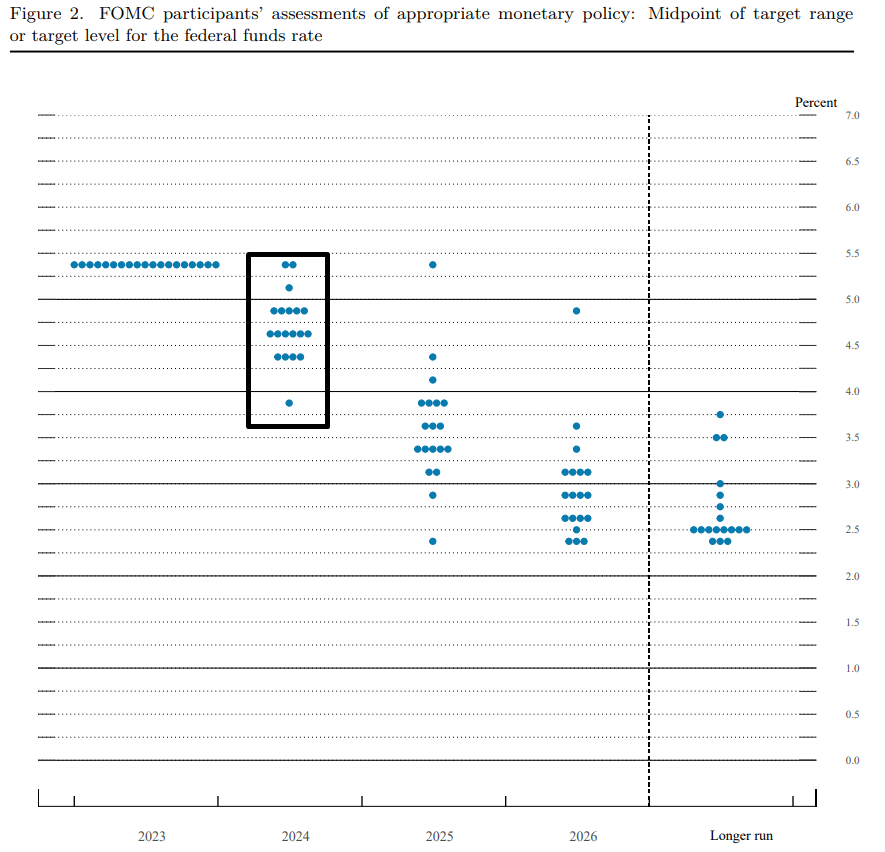

According to the dot plot of Federal Reserve members' expectations of rates, 2024 is expected to end with a median federal funds rate of 4.6%:

FOMC Participants' Target Fed Funds Rate Expectations (Federal Reserve's December Summary of Economic Projections)

{kind=link}

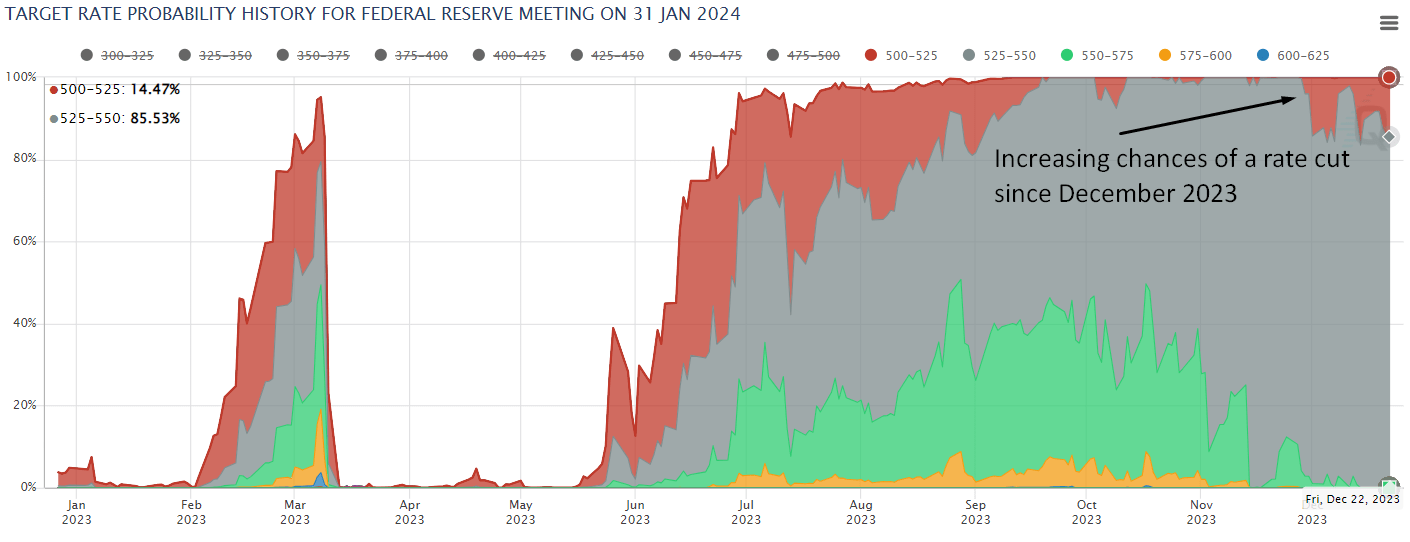

In the FOMC conference, Powell said the timing of rate cuts would be the Fed's "next question", which signals that rate cuts are not a question of if, but when. This is at odds with the previous 'higher-for-longer' sentiment. The market has started to recognize the new reality as well. The target rate probabilities for January 2024's Federal Reserve Meeting imply a 0% chance of a rate hike and a 14.47% chance of a rate cut:

Target Rate Probabilities for January 2024 Federal Reserve Meeting (CME FedWatch)

{kind=link}

I believe these new developments on rate expectations undermine previously cautious outlooks for the capital markets sector since:

Rate cuts are expected to boost activity in the capital markets sector

So far, higher rates have led to a higher cost of capital for pursuing enterprising activities in the economy. Two key barometers to reflect this include M&A activity levels :

US M&A Market Announcements (FactSet US M&A News & Trends)

{kind=link}

And IPO activity levels :

IPOs and SPAC Listings (PwC 2024 Capital Markets Outlook)

As can be seen in the charts above, both M&A and IPO activity have been slow in 2023. However, as rates ease in 2024, I anticipate both these capital market deal types to run hot again. This would particularly benefit investment banks such as Morgan Stanley ( MS ) and asset management companies such as TPG ( TPG ). I also expect increased trading activity across exchanges such as ( CBOE ) as fixed deposit options become relatively less attractive when rates fall. This would increase the commissions of brokerages such as Interactive Brokers ( IBKR ) and also serve to boost sales for financial data platforms such as S&P Global ( SPGI ).

I also anticipate the new narratives on rates to lead to guidance upgrades and positive earnings surprises in 2024 by the sector's companies as companies revise their base case scenarios. These events are likely to further propel the stocks in the capital markets sector.

The equally weighted KCE ETF is a better way to play the sectoral tailwind

Among Capital Markets ETFs, 2 main choices include KCE and the iShares U.S. Broker-Dealers & Securities Exchanges ETF ( IAI ). The Sunday Investor has delved deeper into the key differences here . I think the most important thing to note is that KCE is mostly equally weighted across a diverse set of 63 companies. The top 10 holdings for KCE make up only 18.57% of the total ETF's weight; a good sign of broad diversification.

KCE Holdings Composition (KCE Top Holdings Page)

This is in line with the KCE ETF's objectives :

Seeks to track a modified equal weighted index which provides the potential for unconcentrated industry exposure across large, mid and small cap stocks.

- Author's bolded highlight

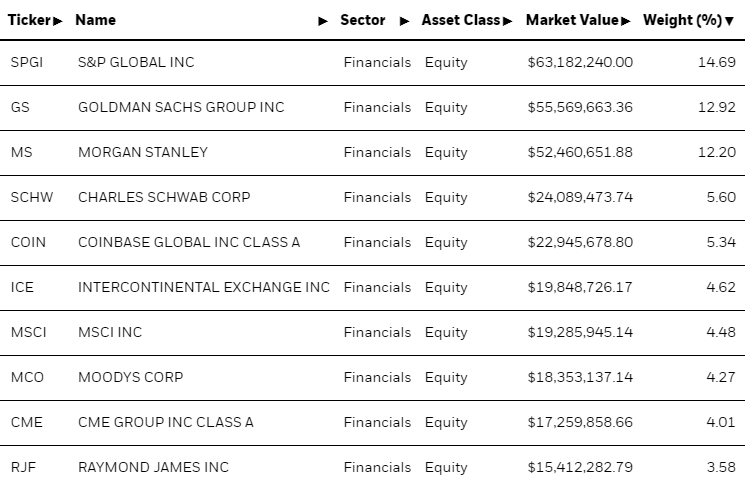

IAI is far more concentrated; its top 3 holdings of S&P Global Inc, Goldman Sachs ( GS ) and Morgan Stanley make up almost 40% of the overall portfolio and its top 10 holdings make up 71.71% of the overall ETF; a sign of the much lower degree of diversification.

IAI Top Holdings Composition (iShares IAI Holdings Page)

{kind=link}

In this environment of a broad sectoral tailwind, I believe we are facing a situation where a rising tide lifts all boats, not just the largest heavyweights. In fact, the greatest tailwinds are more likely to be felt outside the industry leaders. Hence, I deem the more diversified KCE to be the better capital markets ETF vehicle to ride the broad-based optimism in the sector. I expect KCE to outperform IAI.

Valuation, Momentum, and the Opportunity Window

1-yr fwd P/E of Index of KCE Constituents (Capital IQ, Author's Analysis)

{kind=link}

The current 1-yr fwd P/E for my proxy for the KCE index stands at 19.49x; a 16.8% premium from the overall 3-yr average of 16.68x. This is because this ETF has seen a very sharp price appreciation over the last couple of months, and especially since the start of December 2023.

Hence, from a valuation perspective, it may seem uncomfortable to buy at first glance. However, I overcome these hesitations when I consider 2 things:

Firstly, The momentum of flows into KCE is very strong. The ETF has an A+ momentum rating . And there is evidence to suggest that momentum factors are relevant sources of alpha creation.

Secondly, the key catalyst of a fall in rates has not yet materialized. I believe investment idea theses are valid until expectations about the future are unfolded. If we wait for everything to be written into reality, it is often too late. In Stanley Druckenmiller's own words :

...you always have to sort of imagine the world the way it's going to be in 18 to 24 months as opposed to now. If you buy it now, you're buying into every single fad every single moment. Whereas if you envision the future, you're trying to imagine how that might be reflected differently in security prices.

I try to stick by this principle. For instance, this is why I don't believe my earlier bullish thesis point for Palantir ( PLTR ) regarding S&P500 ( SPY ) ( SPX ) inclusion is relevant anymore; even though this catalyst hasn't materialized yet, there is now 0 uncertainty about the stock's eligibility for S&P500 inclusion. Similarly, I believe the opportunity window in KCE is open now before the expected rate cuts materialize. When the thesis starts to play out, I believe the alpha opportunity would have evaporated.

Over the longer term, I do anticipate the fair value P/E to mean-revert back down to the mid-high teens levels. Now some may wonder:

But if the fair value equilibrium is likely below the current valuation multiples, how can one justify a buy?

I think this is a deep question as the answer depends on one's underlying beliefs on market mechanics. I believe the act of returning to fair value itself needs a trigger. And until such a trigger occurs, the incumbent fundamental biases can continue. This is the kind of view about market mechanics that legendary investor George Soros has discussed in his Reflexivity Theory treatise. As Investopedia describes it :

Reflexivity is a theory that positive feedback loops between expectations and economic fundamentals can cause price trends that substantially and persistently deviate from equilibrium prices.

- Author's bolded emphasis

I believe such a situation is playing out over here in KCE. I do not anticipate that mean-reversion effect back to mid-late teen valuation multiples to kick in until the rate cut catalyst starts to materialize. This is not expected to happen until March 2024 . Hence, I expect the current fundamental thesis to be valid through Q1 CY24.

Key Risks and Things to Monitor

My thesis here is centered around the implications of the rates narrative by the Federal Reserve, making any changes to this parameter critical to track for continually assessing the validity of the bullish idea. The M&A and IPO activity levels are key coincident indicators to help check whether the inferred implications are indeed following through. I am also expecting a change toward more bullish narratives and surprises in key capital markets companies in the Q4 CY23 earnings season.

If the sentiment around rates turns hawkish again, then out of the 2 Capital Markets ETF options, I think the diversified KCE would be worse-positioned than IAI, which is more concentrated on blue-chip names. This is because I expect an adverse development in the rates scenario to highlight more weaknesses in smaller companies with slightly riskier balance sheets compared to the steady ships of larger, reputed names such as S&P Global Inc, Goldman Sachs and Morgan Stanley.

Takeaway

I posit that December 2023's Federal Reserve Meeting has made the earlier 'higher for longer' narrative redundant. This prompts a fresh look at the outlook for the Capital Markets Sector in 2024. Based on Federal Reserve Members' expectations, the market is starting to recognize the likelihood of rate cuts in 2024. I expect this to be a boon for the capital markets sector, sparking an activity rebound in M&A, IPO and SPACs, higher trading activity in exchanges, increased commissions for brokerages, and a boost in sales for financial data providers. As this is a broad-based sectoral tailwind, I think the equally weighted SPDR® S&P Capital Markets ETF (KCE) is a superior option to play this theme compared to the concentrated iShares U.S. Broker-Dealers & Securities Exchanges ETF (IAI).

Hence, I rate KCE a 'Strong Buy'.

How to interpret Hunting Alpha's ratings:

Strong Buy: Expect the company to outperform the S&P500 on a total shareholder return basis, with higher-than-usual confidence

Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in line with the S&P500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

For further details see:

KCE: Why I'm Very Bullish On This Capital Markets ETF