BEKE - KE Holdings Q2: Affluent Consumer Focus Buoyed By Government Stimulus

2023-09-01 11:38:24 ET

Summary

- KE Holdings reported strong Q2 2023 earnings, with GTV and revenues growing 22% and 44% respectively.

- The company is well-positioned in the China real estate market, targeting affluent consumers and expanding into rental and home renovation sectors.

- The Chinese government's recent stimulus policies, including loosening restrictions on purchasing new homes, permit real estate developers to lower prices, and continuing to loosen the interest rate environment, support BEKE's growth prospects.

Recent Results

KE Holdings (BEKE) reported Q2 2023 earnings on August 31st. The stock went up 14% as we wrapped up the report.

The company demonstrated great results as its GTV and revenues grew 22% and 44% in the quarter, suggesting that BEKE grabbed market share amid the sluggish China real estate market.

Growth Thesis

Our original thesis about KE Holdings is that the company holds a leadership position in the China real estate market and was expanding into high-growth sectors such as rental and home renovation. Rental demand is more stable than home sales and can provide a more steady income stream for the company. Home renovation is supported by affluent Chinese consumers. BEKE's Q2 results reinforce our thesis, as top-line growth was fueled by the high-growth home renovation and emerging services businesses, with renovation revenues up 260% and rental/financial services up 213% year-over-year.

In our recent article "The resilience of China's affluent consumers" , we noticed that the Chinese affluent consumer base is relatively resilient with the supporting data that Tesla and Apple's product unit sales surpassed the US during the quarter. The affluent Chinese consumer is actually better prepared than the general public to seek opportunities in the real estate market. As a result, BEKE as a real estate middleman, who targets this group of customers, is less impacted by the sluggish Chinese real estate market.

Since COVID lockdowns are over in China in 2023, there are many affluent Chinese consumers moving out of China. This created downward pressure on China's real estate market. However, as a result, we think there will be a new class of affluent Chinese consumers who decide to stay in China, constituting the new middle-class force in the Chinese market to take over the shares of those who left China. We think BEKE will be able to continue to grow as this new middle-class affluent consumer base can sustain the purchasing power. Chinese real estate market will be supported by the new class.

In fact, according to management , despite the forecasted 9% decline in revenues in Q3 2023 as the result of a recent slow in demand due to developers struggling with news such as Country Garden and Evergreen. As the Chinese government recently came up with a couple of new stimulus policies we share the same view with management that the Chinese real estate market is bottom.

Government Stimulus

Chinese government's recent policies include:

(1) Loosen restrictions on purchasing new homes. The new policy "recognizes home ownership without recognizing mortgage" - Recognizing home ownership or mortgage is the reference standard for banks to determine whether it is the first home when issuing mortgage loans. "Recognizing home ownership" refers to the bank referencing the number of housing units actually owned by the homebuyer family in the local area; "recognizing mortgage" refers to the bank determining whether it is the first home based on whether the homebuyer family has a history of housing loans nationwide.

According to BEKE Research Institute's estimates, in Beijing, for a 650,000 RMB improved residential property (non-ordinary residence), the down payment ratio is 40% under "recognizing home ownership without recognizing mortgage", while under "recognizing home ownership and recognizing mortgage", the down payment ratio doubles to 80%, with 260,000 RMB more in the down payment amount.

For those with mortgage records from other places, no local housing, and "sell one to buy one" replacement demands, the down payment ratio and mortgage interest rates will decrease significantly, while real estate-related taxes and fees are also expected to be executed as first home purchases. This policy reduces the threshold for families purchasing homes while also reducing home purchase costs, which facilitates the release of demands.

The policy is executed first in top-tier cities. We think this policy is a stimulus for affluent Chinese consumers as this policy gives them more leverage to buy houses. As a result, BEKE as the industry leader is well-positioned to cater to this demand.

(2) Permit real estate developers to lower the price

Chinese real estate market demand and supply are extremely unbalanced as the government restricted the supply of house sales through price control. China's government released the restriction on price control this month. We think it will lower the price of the house and act as a stimulus for housing transaction volume. Chinese real estate transaction volume is likely to pick up as liquidity is improving as a result of the policy. BEKE as the middleman, who earns commission rather than profits from the appreciation of home prices, is better positioned to profit from this beneficial policy as well.

(3) Continue loosening interest rate environment

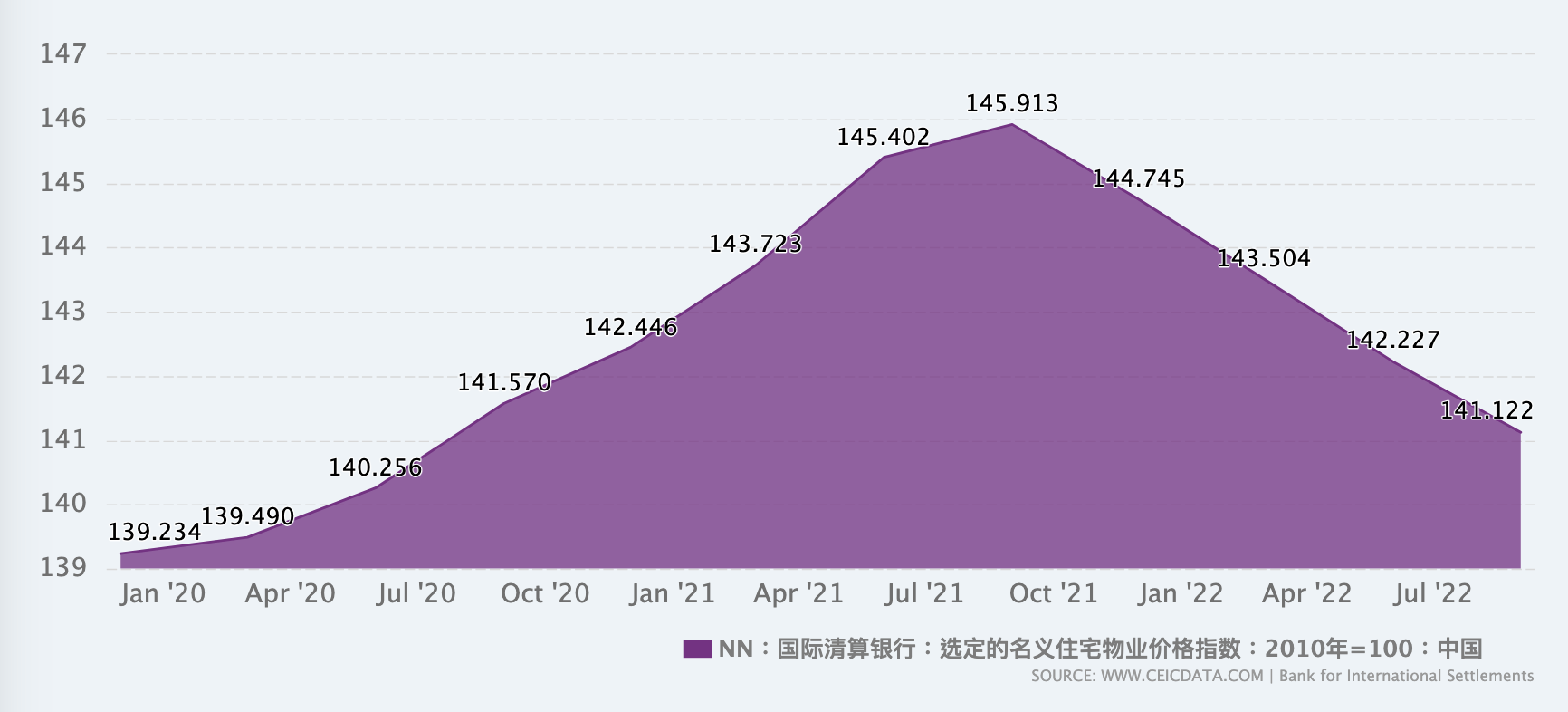

The real estate market price index has been trending down since 2021, signaling sluggish real estate demand to the restriction policy and pessimistic consumer sentiment.

{kind=link}

Nominal Residential Property Price Index in China (CEIC)

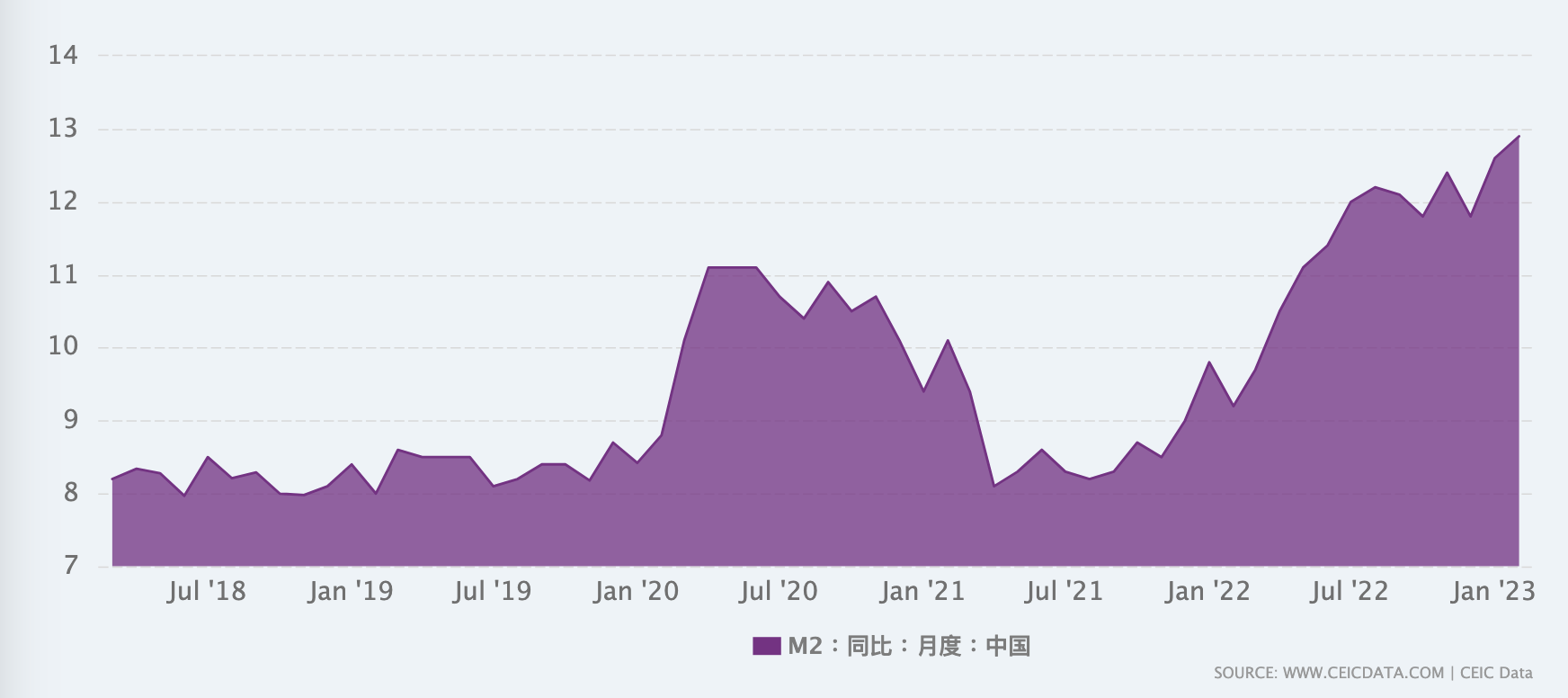

On August 29, the Chinese government decided to lower the mortgage rate by 60 bps to 4.18%. The first time the Chinese government lowered mortgage rates.

The Chinese government has lowered the 1-year LPR interest rate for the second time in 2023. Its M2 growth rate has skyrocketed to double digits since 2022.

{kind=link}

China M2 growth (CEIC)

As the government loosens purchase policy and lowers mortgage rate, combined with the relatively loosened monetary environment for the past 12 months, we think the Chinese real estate market is prepared for the bottom and stabilization.

Financials and Execution

BEKE as the industry leader in the space with no debt on the balance sheet is better positioned to double down its investment when the market is about to bottom. The company had $ 7.4 billion USD cash and cash equivalents as of June 2023 with zero long-term debt. Its impressive growth amid the pessimistic real estate environment during H1 2023 is a strong testimony to its capability of execution.

Its operating expense was flat during Q2 2023, suggesting strong cost control discipline. Its adjusted income from operations was RMB 2.1 billion an increase from the loss of RMB 690 million last year. The company is also shareholder friendly as they sized up the share repurchase program to $1 billion USD and had returned value to shareholders of $605 million USD through share repurchase. In addition, the company announced a special dividend of 0.17 per ADS to reward supporting shareholders.

Geopolitical Risks

We also think the geopolitical risk is overblown for a couple of reasons.

Mitigating Geopolitical Concerns

We acknowledge the apprehension among US investors regarding Chinese companies. However, the resulting negative sentiment has made BEKE stock attractively valued for several reasons:

Benefits of US Listing

Delisting Chinese firms does not align with US interests. Mature US capital markets are a key American advantage underpinned by its legal system. When Chinese companies rely on US markets, it enhances this edge since China lacks equivalent investor protections. The US favors engagement with China provided key technology and consumer ties persist.

Investor caution is understandable given the limited visibility into China's aims. But China still needs US capital and expertise at the moment, so listings benefit both countries. Developed US and Hong Kong markets provide efficient funding still lacking in China. BEKE's domestic focus also limits security concerns, unlike more strategic industries.

Conclusion

We believe geopolitical risks are overhyped by media and politicians given mutual US-China interests. BEKE's US listing provides governance benefits relative to domestic peers. The regulatory concerns seem overblown considering the interdependent relationship between the two powers.

BEKE's affluent consumer focus insulates it from broader economic challenges, and valuations remain undemanding. The fact that the Chinese government maintains a loosening interest rate environment and loose real estate investment restriction policy is beneficial for BEKE. BEKE as the leader in the space with a strong balance sheet is well positioned to invest during the cycle.

For US investors, BEKE provides selective exposure to the resilient upper-middle-class consumers in China. This diversifying growth angle is overlooked amid excessive macro pessimism.

During periods of volatility, it is important to look past sensationalist headlines and find high-quality companies whose true fundamentals are obscured by temporary pessimism. We believe BEKE offers such an opportunity – it is a strong business currently undervalued due to macroeconomic fears that we expect to subside.

For further details see:

KE Holdings Q2: Affluent Consumer Focus Buoyed By Government Stimulus