SBAC - Keeping The Strong Buy On SBA Communications

2023-05-10 18:00:32 ET

Summary

- Great performance on fundamentals.

- Beat consensus estimates and raised full year guidance.

- Commentary from management was outstanding and reflects confidence in their ability to continue delivering results.

- Analysts are sad about no buybacks. I like paying down debt with a yield over 6%. I don't want my REITs borrowing at higher rates.

- Backing up my view with cash. We added to our SBAC position again.

It's remarkable how much the market seems to dislike this quarter. Since SBA Communications ( SBAC ) reported, share prices dropped pretty hard. That's not what you normally expect on a "Beat and Raise" . It's worth noting that there have been some strange sector movements this month, but that doesn't explain so much weakness following a strong report.

American Tower ( AMT ) and Crown Castle International ( CCI ) have also suffered lately. I own shares in all three. The market is betting against the sector, but prices are too low to merit those merits bets.

Most of the articles we provide for members stay behind the paywall indefinitely. A small portion of them make it out to the public side, including this article . You may notice the layout is slightly different when I'm writing for members. I aim to provide a small number on the public side so readers know what to expect. This is the note we provided for members following the earnings release.

SBAC Guidance for 2023

There was a nice boost to guidance:

- Old AFFO Per Share Guidance: $12.46 to $12.83

- New AFFO Per Share Guidance: $12.55 to $12.91

That's up 0.6% to 0.7%. Excluding foreign exchange impacts, it would be more like 0.2%.

When AFFO guidance is the only line that is increased, it can leave investors wondering about the cause. However, SBAC was extremely transparent in updating guidance:

{kind=link}

SBAC

That's clear. With such strong results, it's no wonder SBAC wants to be clear.

SBAC Acquisitions

Per SBAC's Q1 2023 earnings release :

Subsequent to the first quarter of 2023, the Company purchased or is under contract to purchase 66 communication sites for an aggregate consideration of $63.7 million in cash. The Company anticipates that these acquisitions will be consummated by the end of the fourth quarter of 2023.

For reference, $63.7 million is barely material. SBAC should produce around $1 billion in free cash flow.

SBAC International Churn

SBAC and AMT have headwinds for 2023 in Brazil from Oi churn. Oi is (or was) the name of a major operator in Brazil. Churn is the term for a lease not being renewed. Since "vacancy" is harder to articulate when a single asset can hold multiple customers, we use "churn" to reflect any headwind from any lease not being renewed.

For simplicity, if you have one lease ending and another lease starting down the street for the same amount, you have churn and organic growth. The net would be $0 in that scenario. The tower REITs are always signing new customers, but they will always have some level of churn as well. When churn is higher, that is a headwind.

As SBAC highlights in the conference call, international churn for 2023 is still in line with expectations and prior guidance. 2023 should be the high watermark for international churn. In other words, 2024 and beyond should be easier than 2023.

Management is estimating $25 to $35 million in revenue exposed to the Oi consolidation. About $10 million has already been locked in for 2023, so that leaves $15 to $25 million over the coming years.

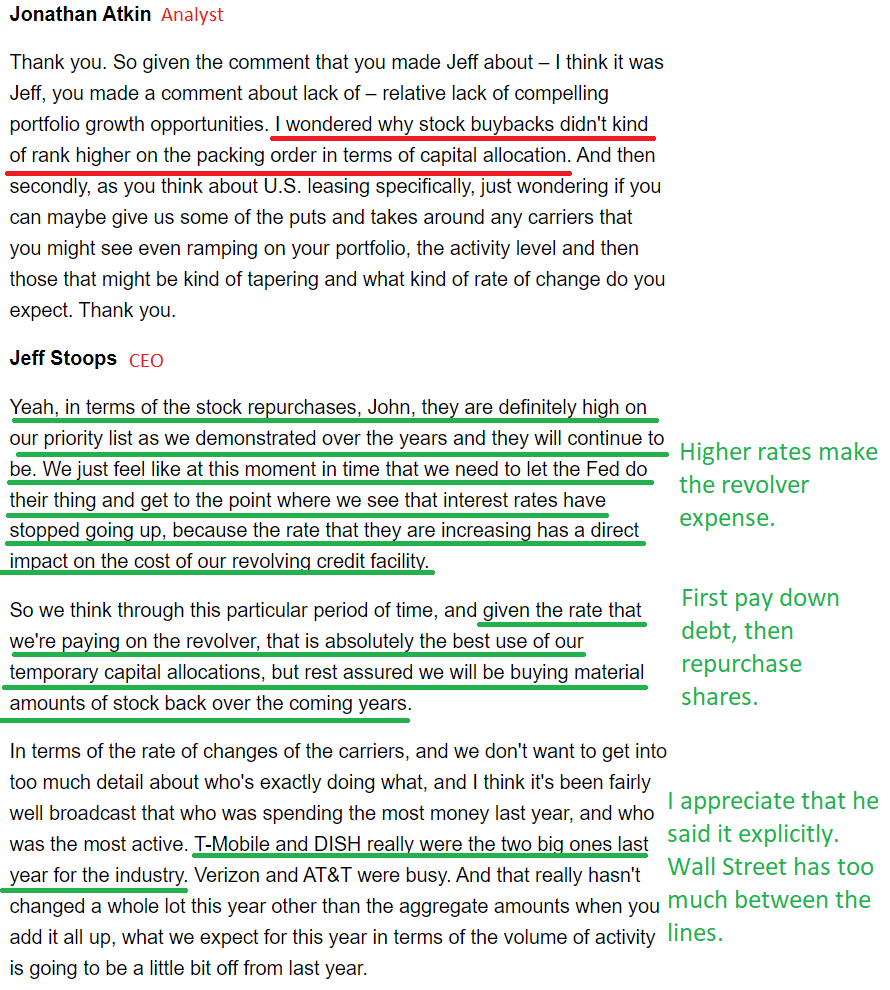

SBAC Transcript on Buybacks and Debt

I think the earnings call was great, but I also think some analysts and investors were disappointed with one part of it. Specifically, this part:

{kind=link}

Seeking Alpha

SBAC is trading at an unusually low multiple. It's perfectly reasonable that investors and analysts are looking at the $1 billion in free cash flow and thinking this is an ideal time for SBAC to repurchase shares.

Seeing as we've bought shares twice in the last couple of months, clearly I think buying SBAC shares is a good use of cash. However, I also respect management's decision here. They have reduced floating-rate debt to only 7% of their total debt. They aren't just locking in high fixed rates (which many REITs are doing).

This is how I would summarize SBAC's strategy:

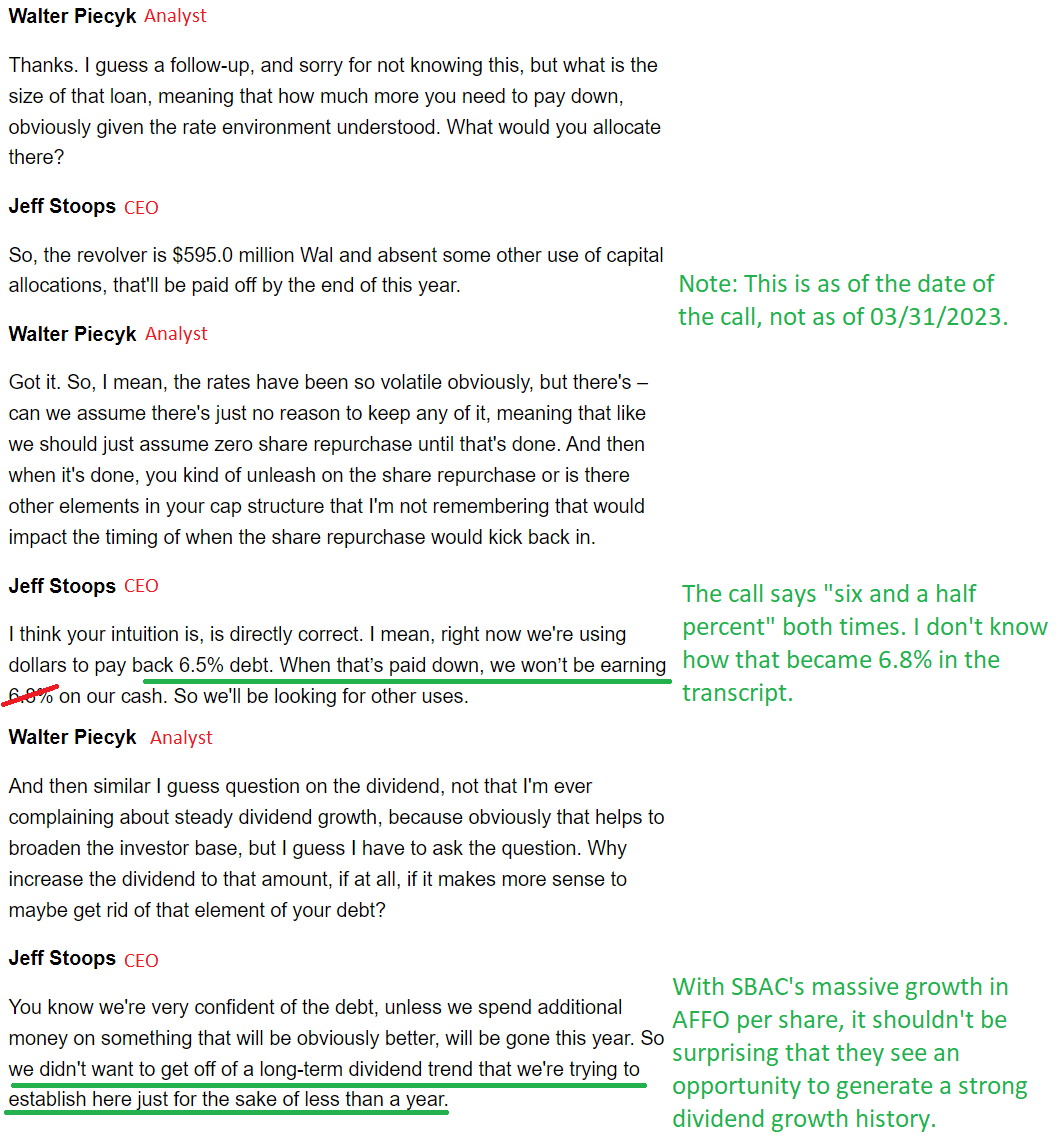

If we pay off all of our floating rate debt, that's a nice tailwind for AFFO in 2024. We're saving 6.5% to 6.8% on every dollar we pay off. We don't mind running at higher leverage, but we're not over 6% to do it. No. We like cheap debt, not expensive debt.

That works for me. SBAC has a higher risk rating than the other tower REITs because they tend to use more leverage . But they also have a very small dividend, so they are retaining a huge amount of free cash flow. They responded to higher interest rates on debt by simply paying it off. That's a lesson many households and businesses could learn from.

By the end of 2023, they should be down to 0% floating rate debt or very close to it. When that happens, they may look to use their buyback authorization if shares are still cheap. If shares are not cheap, should we all complain to management that the price went up? This is a fine strategy. Buybacks can be very good, but paying back debt at over 6% is also good.

However, analysts really want buybacks:

{kind=link}

Seeking Alpha

The very next question was about buybacks also:

{kind=link}

Seeking Alpha

It seems pretty clear analysts really want to see buybacks, but I'm content with management's emphasis on wiping out that debt. I'm not going to get 6.5% with zero risk. I don't want my dividends to be funded by keeping extra debt outstanding at 6.5%. Knock that debt out.

SBAC Transcript on Demand

Management's prepared remarks were outstanding. They drilled this. Here are my notes on the section I considered most important:

{kind=link}

Seeking Alpha

That was a powerful affirmation of the expected demand.

Further, meeting this demand through new construction will be challenging because the cost of new construction is up dramatically. That is a big incentive for more colocation, which is how tower REITs gain improved operating leverage.

{kind=link}

Seeking Alpha

SBAC Transcript Timing of Leases

The only thing that comes even remotely close to weakness is that the leasing was so strong in the first quarter, that it implies a modestly lower rate for the next three quarters. In theory, that means less of a tailwind for 2024. For any given amount of revenue, if you start most of it in Q4, then the year-over-year comparison gets boosted. For reference, it was about $21 million in the first quarter, so the next three should be around $50 to $51 million combined (about $17 million average over the next three quarters).

That's the "weakness" and it is too small to mention except for the fact that SBAC was simply lacking in flaws.

SBAC Summary

That was a great earnings release and a great call. The market seems upset that SBAC isn't using this opportunity to repurchase shares at such low prices. While management isn't buying back shares yet, they are hammering away at their floating rate debt. I can't complain, since the only things that previously concerned us about SBAC were the higher leverage and how hard it was to find shares on a solid sale. SBAC is handling the leverage and letting us get that lower entry price.

I can't fault SBAC for having revenues starting earlier in the year. This is a close one between a 9 and a 10, but the strength of management's commentary pushed it over the top. I'm giving SBAC a 10. I could say that we might buy more shares, but our recent buy alert on SBAC should still be echoing. My bullish view was backed up by dropping another $12,600 into SBAC. Clearly, I'm not dumping any shares.

As the share price indicates, the market saw it differently. However, SBAC simply did so many things right:

- Delivered a beat and raise with guidance going up across all metrics. Guidance isn't up dramatically, but it is still up.

- Paid down debts while increasing guidance.

- Pounded home the message about demand continuing for several years.

- Identified precise factors that would make it more difficult for the carriers to expand quickly in 2023 along with when and how those factors are being resolved.

Outlook with today's prices: Bullish on SBAC at $237.05, AMT at $196.36, and CCI at $118.95.

Prices are included for each share for easy reference a few years from today.

For further details see:

Keeping The Strong Buy On SBA Communications