BYND - Kellogg: An Interesting Play Heading Into 2023

Summary

- K isn't an exciting growth stock, but there has been some more exciting news with the company splitting up.

- This company has given a consistently growing dividend for years, making it a great choice for income investors.

- After the split, the company is still looking to "maintain a strong aggregate dividend."

Written by Nick Ackerman. This article was included with a trade alert for Cash Builder Opportunities originally on January 18th, 2023.

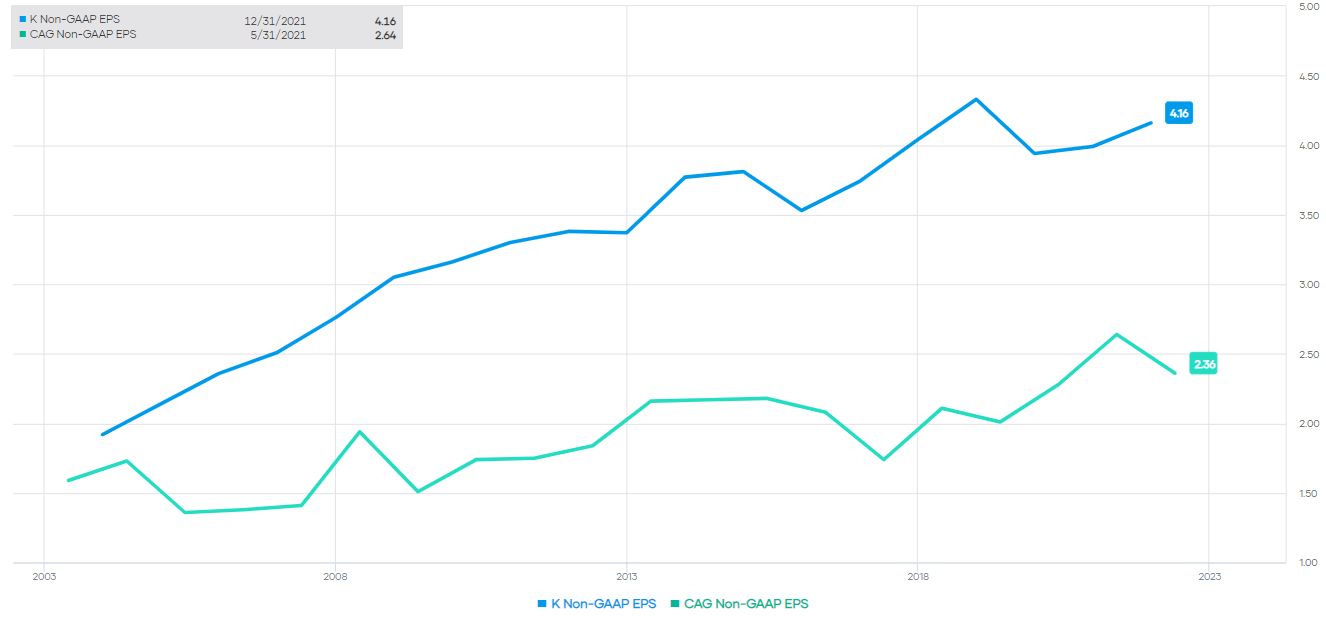

Kellogg ( K ) has been a name on my watchlist for quite some time. It was intended to be included as one of the names that could be incorporated into the Core Portfolio. However, that slot for consumer staple food names was filled by Conagra ( CAG ). As consumer staples in the food industry, they are often boring and slow-growth businesses. Both of these have performed well in the last year as defensive plays.

Ultimately, it comes down to the fact that people have to eat, and that leads to strong pricing power in the face of inflation. Inflation isn't great, but it is one of the sectors that can handle it. Below is how K and CAG have been performing in the last year relative to the Consumer Staples SPDR ( XLP ) and the broader market measured by the SPDR S&P 500 ( SPY ).

YCharts

This inelastic demand for companies like K and CAG means that, generally, earnings aren't going to be swinging wildly. This leads to slow and steady dividend machines and share prices that should also be less volatile. As exhibited above, investors in these stocks might not have even known a bear market was happening.

Albeit, they usually aren't going to be epic growth plays either. You won't tend to see their dividends double every few years. Again, boring is the keyword here, and I find a place in my portfolio for those boring names.

{kind=link}

Splitting Up

Looking at the biggest news from Kellogg is the transformation they will embark on. There are still some details that aren't known yet, but I suspect we should get some more with the next earnings coming up in February. This split is expected to happen before the end of 2023, but I haven't seen an exact date.

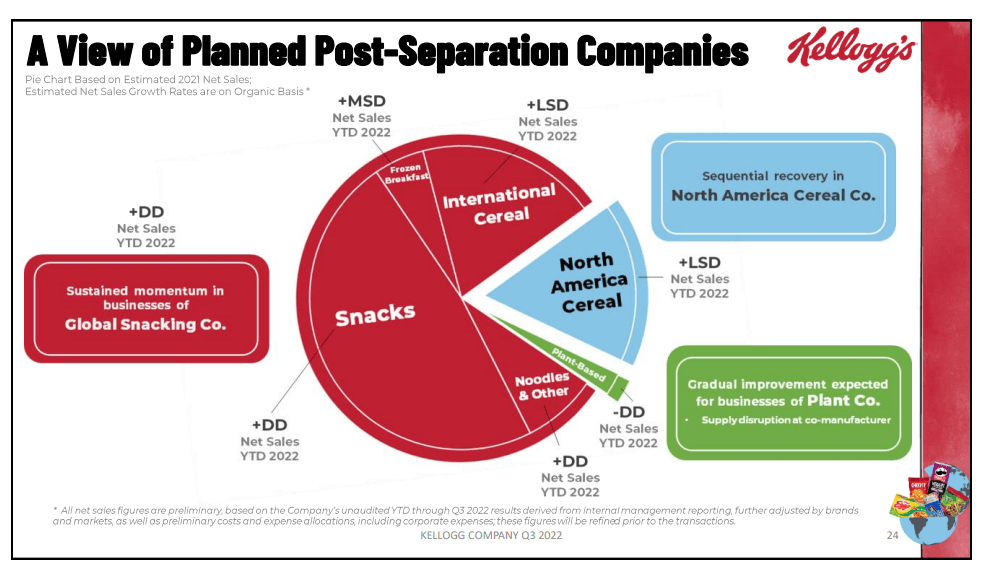

As most investors probably know at this point, they are planning to split into three companies. This transformation will include the global snacking business, which will be the largest piece of the pie held together. Then they will have their North American cereal business.

There will also be the plant-based foods company, which will be the smallest of the three, but the one expected to provide the most growth.

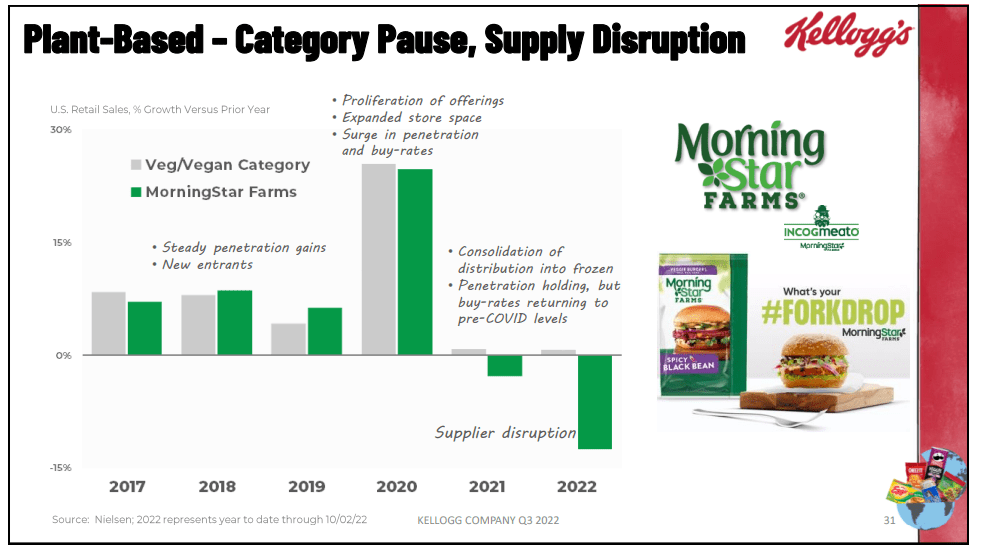

The latest conversation is pointing to the "Plant Company" as having softness due to supply disruptions in the latest conference call.

However, despite that, they remarked on how even after the surge in demand, they are experiencing household penetration at pre-COVID levels. So the entire surge didn't stick, but it also still was a net benefit.

For context, this business represents only about 2% of our total net sales, but it gets a lot of attention because of its promising long-term prospects and because of the recent slowdown of its category. This is a category that experienced the equivalent of a few years' worth of acceleration in a single year 2020. It had already been in elevated growth with new entrants, new technologies and new space in stores, then COVID hit and product proliferation was soaked up by the surge in at-home demand, bringing penetration and buy rates up with it.

The category lapped that surge in 2021 and in 2022 it has experienced a pause in growth and point of distribution have decreased in stores as many retailers consolidated into the frozen aisle. But household penetration remains above pre-COVID levels with ample opportunities to return to consistent growth behind underlying consumer focus on health and environmental concerns. These are demand fundamentals that remain firmly in place for a long runway of growth.

The Plant Company had $340 million in net sales for 2021. The "North America Cereal Co" had $2.4 billion in sales, and the "Global Snacks" business had $11.4 billion in net sales.

To help visualize the different business sizes besides just the numbers, they provide a pie chart in their last earnings slide. It's quite clear how large the snacking unit will be.

{kind=link}

However, note that they are looking at the net sales of 2021 and then estimating the net sales growth rates for each unit. The "+DD" means they are up double digits on a YTD through fiscal Q3, 2022. "+LSD" here means that they are up low-single digits.

While the cereal business is generally slower, they mentioned that the cereal business picked up to double-digit growth in Q3 due to increased prices and "below average elasticity." On a YTD 2022 vs. YTD 2021 period, it showed 3% organic net sales but jumped to 12% for Q3. Some of this goes back to the strike at the end of 2021, where they had to rebuild back inventory.

K U.S. Cereal Weekly Category Share in % (Kellogg)

Then, the "-DD" in the pie chart shared above means that the Plant Co. is down double digits. However, as noted, this was primarily linked to supplier disruptions. Prior to this, this was experiencing much faster growth from 2017 through 2019.

{kind=link}

Takeover Targets?

One reason that I believe K could be worth playing once they split up is the fact that each of these divisions becomes much smaller. The Plant Co., in particular, could be a takeover candidate for just about any food company that wants to add to their or begin a plant-based category.

If they could get back to the growth they had been experiencing, which seems plausible, that seems more likely. Due to the size, it wouldn't be overly difficult for something like a PepsiCo ( PEP ) to swoop in and pick it up.

The North American cereal business might not be the most attractive, but due to its size would also be a candidate for being bought out. However, being a slower growing, for the most part, it might not be the most attractive candidate.

Finally, even the Global Snacks business, despite being the largest of the pie, could be at play. With organic net sales growth of 18% in Q3, 2022 and 14% YTD in 2022 vs. the prior 2021 period, there is growth there. So while being the largest, it is generally the more attractive of the three businesses, in my opinion. I believe that would make it the most attractive to other food companies.

Due to size, however, it wouldn't be as easy to fold in as an acquisition. PEP could afford it but is unlikely to add it as they have their own little snack division. They have a little company called Frito-Lay; not sure if anyone has heard of it. It's the company that has 60% of the salty snacks business.

A merger could be a viable option. Thinking back to when Kraft Foods spun off from what was Kraft, then later named Mondelez ( MDLZ ), Kraft and Heinz ended up merging together to form what we see as Kraft Heinz ( KHC ) that we see today.

Speaking of MDLZ, they also have a sizeable snacks business more focused on sweets. With revenue pushing around $30 billion in 2021, that would be a bit hard of an acquisition swallow. For some context of a recent acquisition , MDLZ bought Clif Bars in 2022 for $2.9 billion.

The Dividend Going Forward

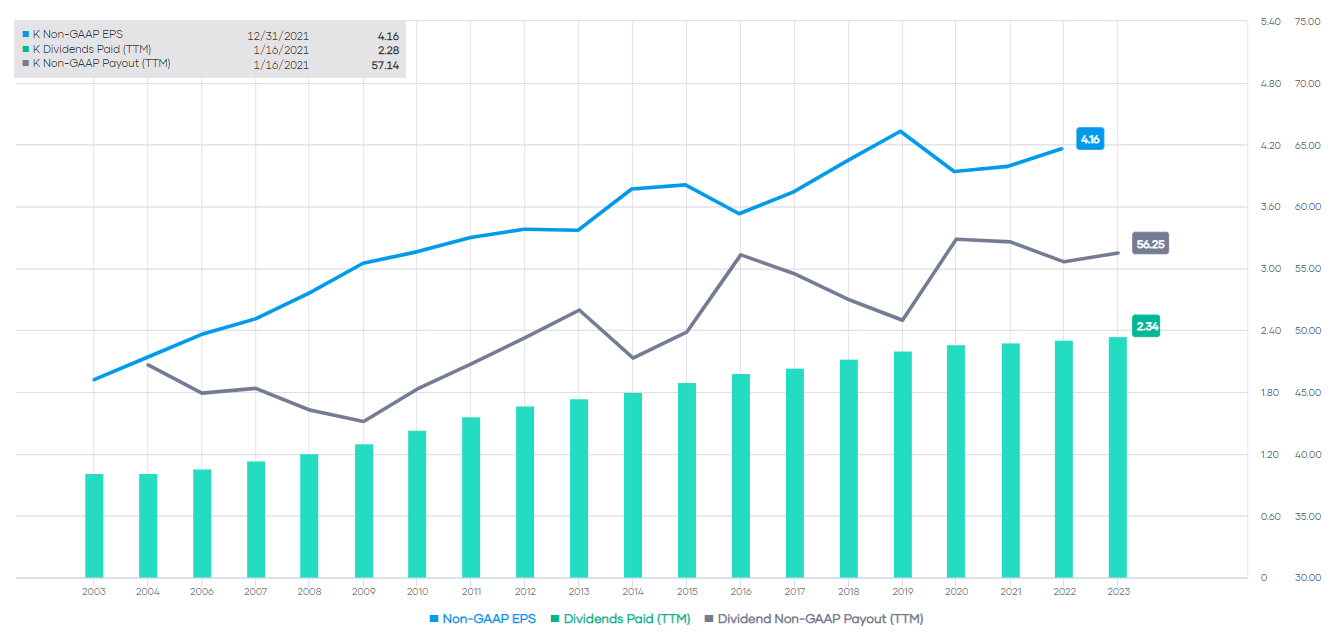

While the takeover targets are ideas that I'm just spitballing, what is known is that investors own K for the dividend. The combined entity has 33 years of consecutive dividends, and 18 of the last years were increasing growth.

The growth in more recent years hasn't been anything to brag about, but it has been trending higher. The payout ratio of the dividend comes in at quite a safe level. However, the payout ratio has been trending higher as it catches up with its non-GAAP earnings.

{kind=link}

This is another exact detail that isn't yet known at this time, what the three will pay in terms of dividends. They specifically state that:

In addition, the Company expects to maintain a strong aggregate dividend and return-on-capital profile across the three businesses. The independent dividend and capital structure policies for each business are expected to be competitive relative to their relevant peer sets. The independent dividend and capital structure policies for each business are expected to be competitive relative to their relevant peer sets.

So we should expect dividends if they "maintain a strong aggregate dividend." However, the division of how that is split is completely unknown. While the payout ratio is healthy, I expect that there will be a dividend cut here.

What makes it more difficult here is that finding peers isn't quite easy. Most food companies span several different categories, basically as K is structured today. For the Plant Co., we have Beyond Meat ( BYND ), which could be seen as a competitor. However, they have no profits and pay no dividends. There is also Impossible Foods, but they haven't gone public yet.

Having the expectation that this is supposed to be more of a growth company, I wouldn't necessarily count on a dividend. If they do end up with a dividend, it would probably be quite low.

For the North American Cereal business, we don't have a direct peer, either. However, we have General Mills ( GIS ) and Post Holdings ( POST ). These are heavy cereal-focused businesses. With GIS, we have an impressive dividend track record, and with POST, there is no dividend.

GIS shows a similar growth expectation of single-digit growth in the following years. Given the 2.64% dividend yield, that's around something we could expect, in my opinion. Growth, in this case, could be fairly limited.

I go back to thinking of Kraft when it was focused on North America alone; while having a diversified portfolio of brands, it lacked any growth. Being tied up with Heinz, it was supposed to broaden its focus and bring it back to global markets. That ultimately brought a dividend cut eventually, and it has been frozen at the same quarterly amount since 2019.

Looking at the Global Snacks business, given the higher growth expectations, it reminds me more of MDLZ. Except that if the Global Snacks business can keep up its pace of growth, it will be growing even faster than MDLZ. MDLZ has been able to grow its dividend continuously.

So, I have much higher hopes for this business unit. MDLZ has a yield of 2.30%, and PEP comes in at 2.61%. If the yield is anywhere around 2% to 3%, it stands to reason that it could be viewed as "competitive relative to their relevant peer sets."

Conclusion

The split of K makes it a bit less boring of a company for now. Despite announcing it last year, there are a lot of unknowns at this point. We should be getting more details as we go through the year. At least, that would be the common sense way to view it, with the expected split to happen before the year ends.

For further details see:

Kellogg: An Interesting Play Heading Into 2023