KELYB - Kelly Services: Not A Buy For Now

2023-06-15 06:38:29 ET

Summary

- Kelly Services has not seen much revenue change in the last decade.

- The education segment might give a slight boost, but I remain skeptical.

- Currently, the shares are too expensive, but I cannot recommend selling them as there is potential for revenue rejuvenation, which may reward loyal shareholders.

Investment Thesis

With no growth in revenues in the last decade, I argue that Kelly Services ( KELYA ) will go nowhere in the next decade also unless their education services become a decent catalyst for their revenues. Current long-term holders of the shares can continue holding on to their position, while I wouldn't recommend buying in right now if you don't have any shares and I would wait for some sort of improvement to revenue growth in the future.

I wanted to take a look at the company's financials and come up with a reasonable valuation if the company continues to chug along at these growth rates.

Financials

The graphs below will be as of FY22 because they show a fuller picture of where the company is going. I will add some numbers from the latest quarter if needed.

As of Q1'23, KELYA had $111m in cash and equivalents, while having no debt on the books. This is a great financial position to be in because it gives the company more flexibility on how it can spend its cash, whether that would be paying dividends, share buybacks, or acquisitions to increase revenue.

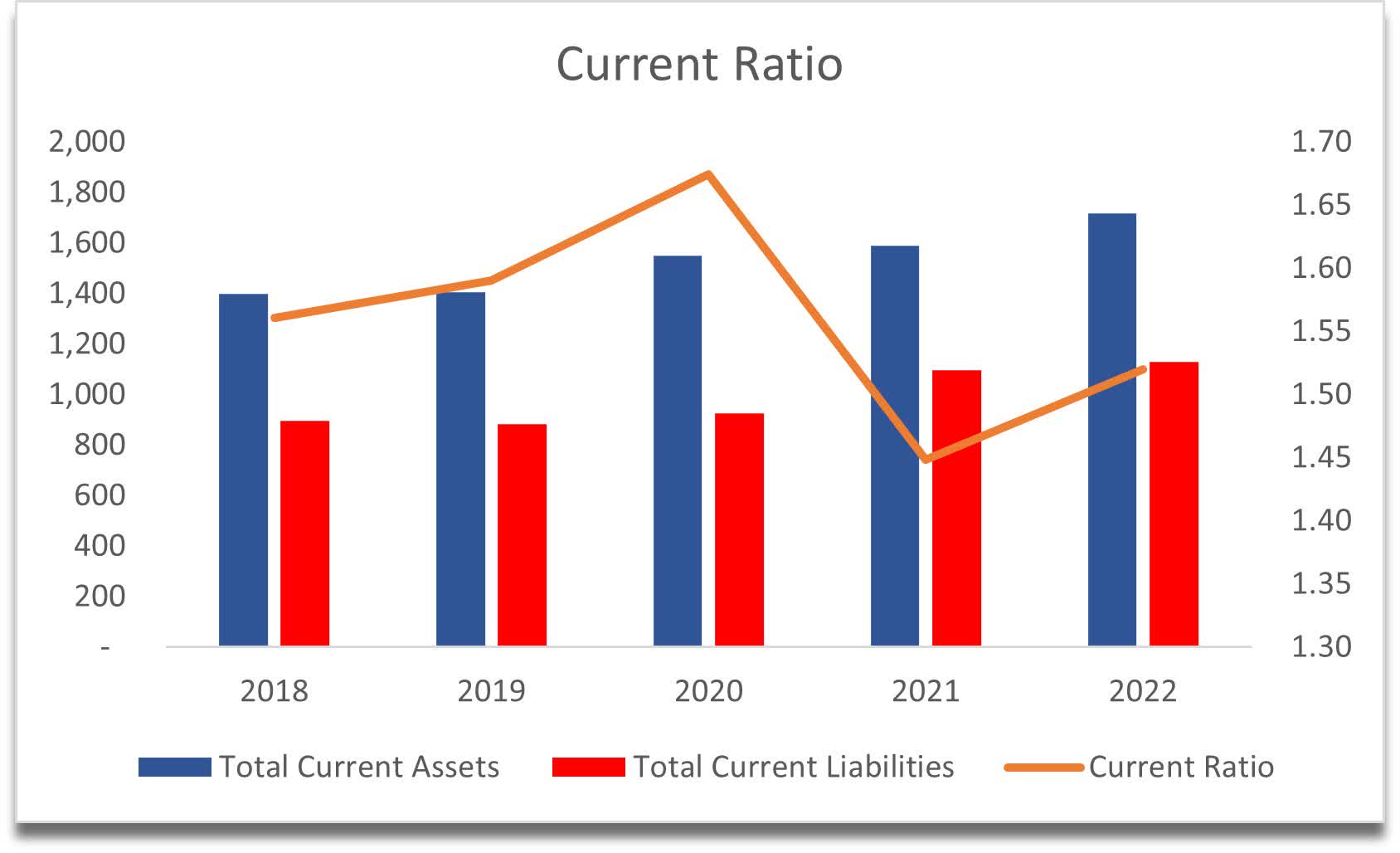

The company's working capital ratio or the current ratio has been decent throughout the last 5 years, hovering at around 1.5. This means that the company has no problems paying off its short-term obligations.

Current Ratio (Own Calculations)

{kind=link}

In terms of liquidity, the company should be fine even during some sort of bad macroeconomic environment that we are supposedly going to be entering very soon.

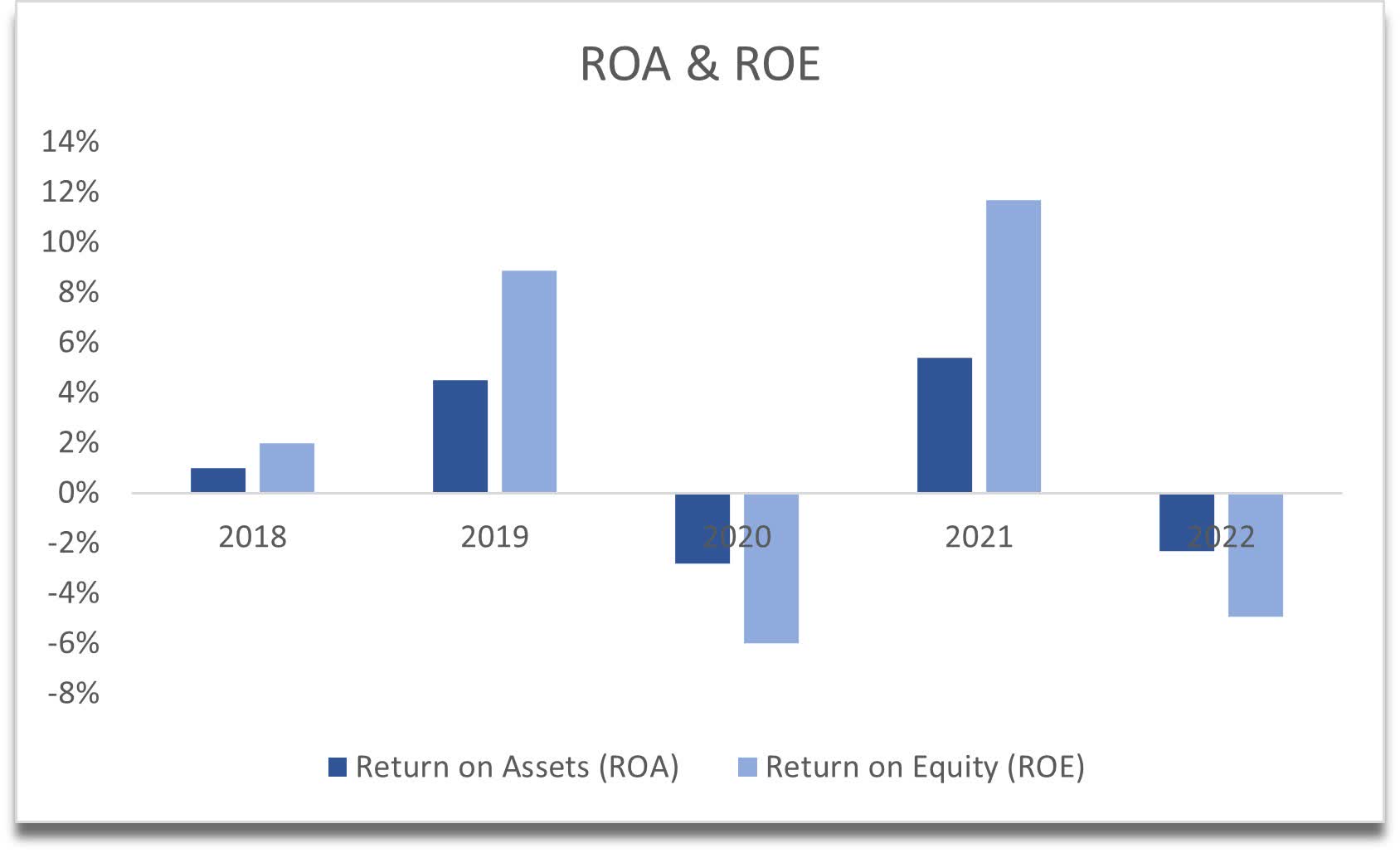

In terms of efficiency and profitability, the company's ROA and ROE have not been very attractive in at least the last 5 years. They fluctuate quite a bit, and no trend is visible. I like to invest in companies that already have been performing consistently in these metrics and KELYA is far from it. I would like to see at least 5% on ROA and 10% on ROE.

ROA and ROE (Own Calculations)

{kind=link}

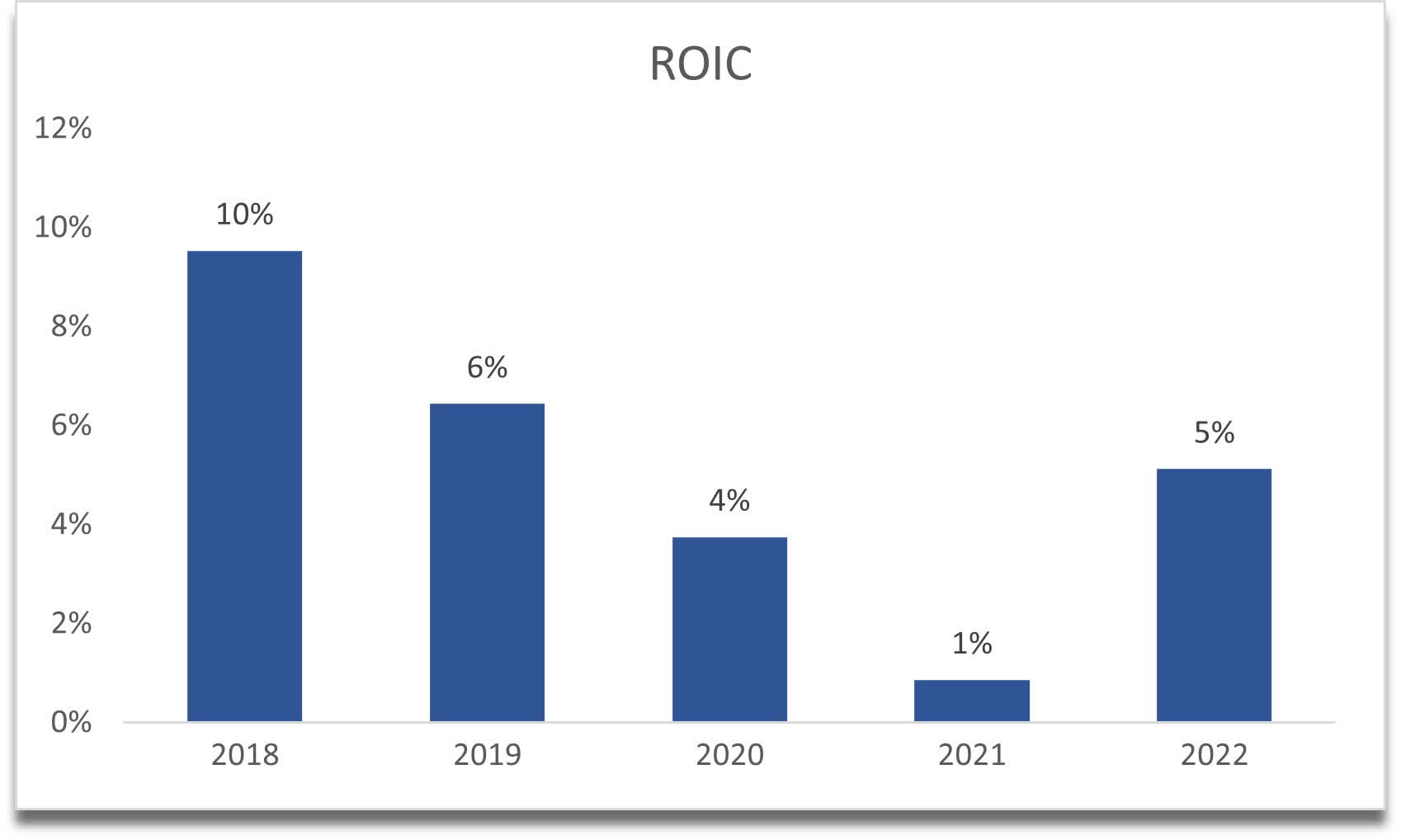

The company's return on invested capital is slightly better, especially since it broke that downtrend it experienced from '18 to '21. It is still not the greatest return; however, it does indicate that the company has some sort of competitive advantage and a moat. For ROIC, I like to see at least 9%-10% consistently as the company had in '18. The good thing is that it seems to have broken the downtrend, however, we'll have to get a couple of more reports to confirm that it is indeed the case.

{kind=link}

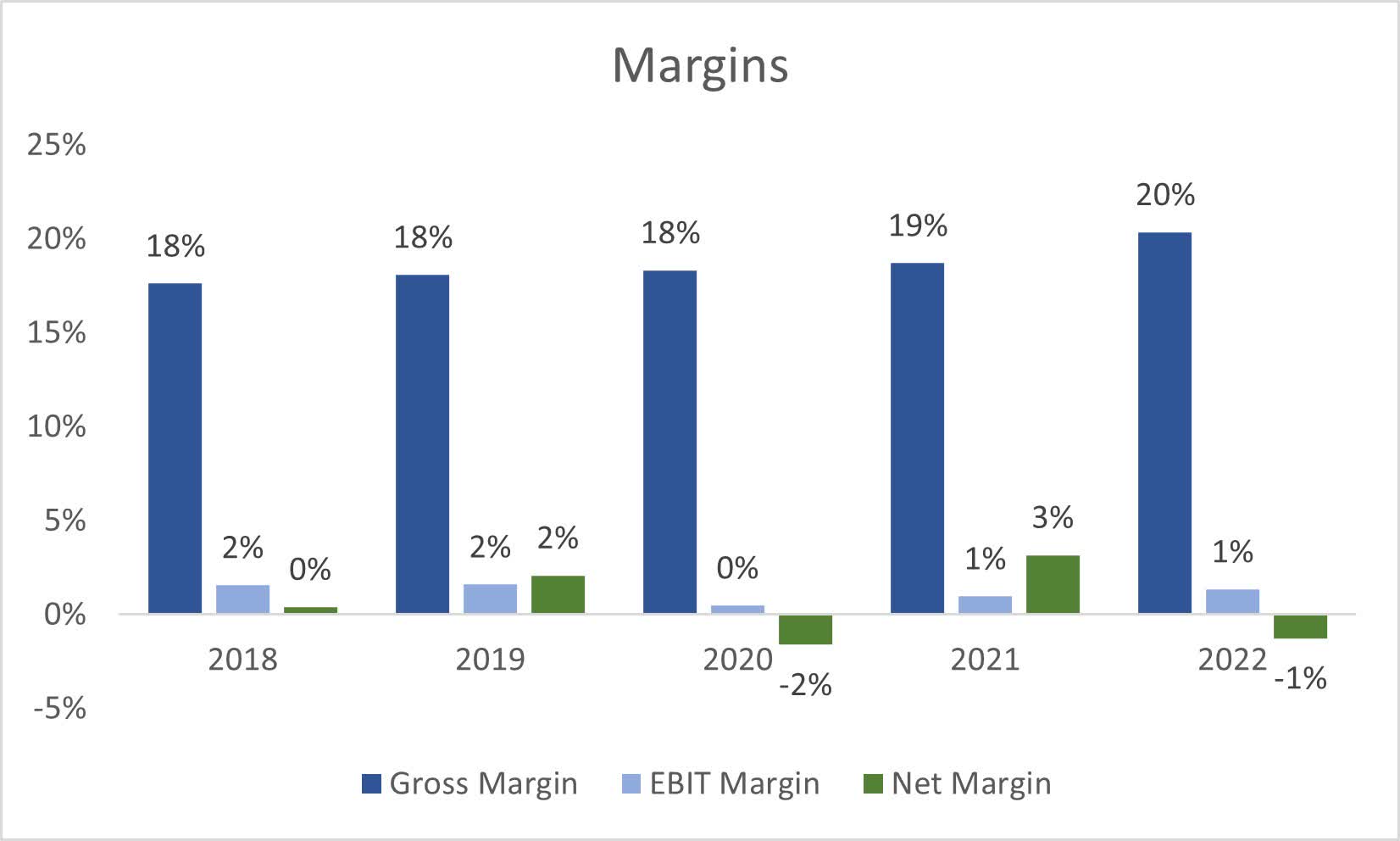

Another thing I don't like is how thin the margins are for this company. The gross margin of around 20% in the latest year is not very attractive. Just a quick look at another similar company that I did previously, which is BGSF, Inc. ( BGSF ), we can see that 20% margins are not very efficient. BGSF gets an additional 15% on top at least. So, there is not much wiggle room for the company.

Gross Margin comparison to BGSF (Seeking Alpha) Margins (Own Calculations)

{kind=link}

Unfortunately, these financials warrant a larger margin of safety when I go through my valuation assumptions in the next section.

Valuation

So, in the past decade, the company did not grow revenues at all, which explains the abysmal performance of the share price over the same period. With the only positive that I can see that could become a major revenue generator if it keeps going the way it has recently is the Education revenue segment. This has grown over 40% in the latest quarter showing basically no slowing down. Right now, this is the 4th largest revenue segment, but if it keeps growing this way, I can see it becoming one of the tops, if not the top revenue generator in the next 5 years or so. But I cannot be that optimistic in my assumptions because that's not my style.

For the base case, I decided to grow revenues, by around 4.3%, which is more than what it did in the past decade, however, I'll amuse the idea that the education segment will pick up the slack where the rest of the segments cannot. For the optimistic case, I went with an 8.1% CAGR. That is if everything goes its way, and all the segments start to come to life. For the conservative case, I went with 2.3%, which would barely keep up with the inflation. And I still think it's a little generous.

In terms of margins, I decided to improve these by around 260bps or 2.6% on gross margins, and 300bps or 3% on operating margins over the next decade. I figured the company finds efficiencies by cost-cutting eventually. For the optimistic case, margins are around 200bps better than in the base case, and vice versa in the conservative case.

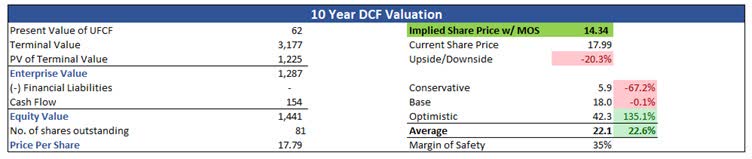

I also added a 35% margin of safety to have a little extra cushion and a better risk/reward profile. With that said, the intrinsic value of Kelly Services is $14.34 a share, implying around 20% downside from current valuations.

Intrinsic Value (Own Calculations)

{kind=link}

Risks

The share price has been rangebound between $15 and $30. Without any strong catalyst, the company may continue to be in this range, which means that the shareholders will not going to be rewarded in the long run for their loyalty.

Currently, the share price is close to that bottom range so anyone who is holding the shares right now, and if they are looking to buy more can wait a little while longer for it to come back down a little more and average down because the upcoming macroeconomic headwinds will likely bring the stock price down.

The shares are trading on low volume so expect some higher-than-average volatility on a daily basis, sometimes 3%-4% a day without any news. So, make sure you have the stomach for it.

Closing Comments

While the potential to outperform is there with the education segment growing at such a fast pace, I wouldn't jump in right now to buy because, with the above assumptions, the risk/reward profile is not very attractive for a new investor in the company. If you are already invested in the company, I'm sure if you haven't sold earlier, there is no point in selling right now either. I wouldn't add to an existing position at these prices because the macroeconomic environment can still get worse in the next couple of months or so, which I have no doubt will bring down the price of the shares.

For further details see:

Kelly Services: Not A Buy For Now